REIT - REITs Lead Quarter-End Rally

2023-07-02 09:00:00 ET

Summary

- U.S. equity markets closed-out a volatile first-half at their highest-levels of the year as investors cheered data showing continued resilience in economic activity alongside further signs of cooling inflationary pressure.

- Rebounding from its worst week since March, the S&P 500 advanced 2.3% to close at its highest-levels since April 2022. The Mid-Cap 400 and Small-Cap 600 each rallied over 4%.

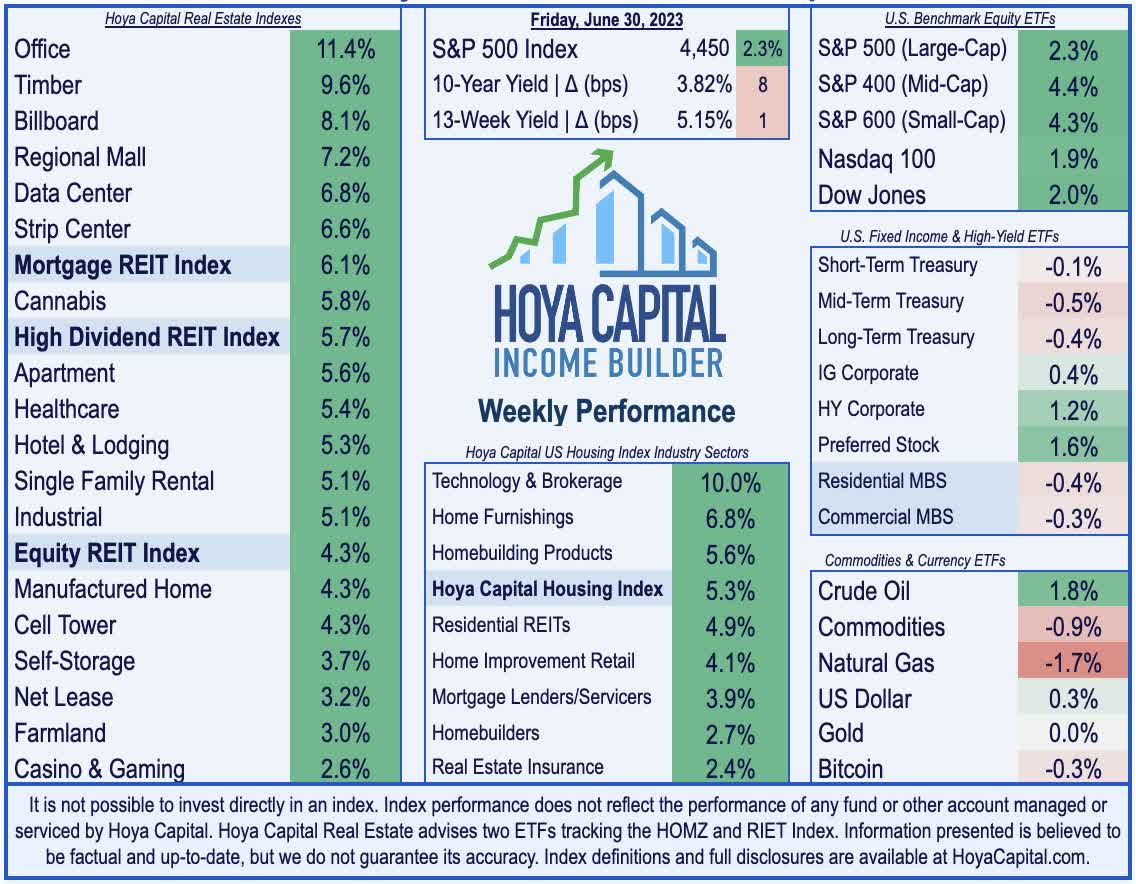

- Lifted by a recovery in the most beaten-down property sectors, real estate equities led the rally on the week. The Equity REIT Index advanced 4.3% while Mortgage REITs surged 6%.

- Leading a sharp rebound this week across the office REIT sector, SL Green rallied nearly 30% after it announced that it sold a 49.9% interest in 245 Park Avenue to Japanese developer Mori Trust at a gross asset valuation of $2.0 billion - nearly double the valuation implied by public market pricing of office REITs.

- Prologis - the largest industrial REIT - rallied nearly 5% this week after it announced a $3.1 billion deal to acquire from Blackstone nearly 14 million square feet of industrial properties from its opportunistic real estate funds. Blackstone is reportedly also seeking to sell its BREIT casino properties as it struggles to meet investor redemption requests.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on June 30th.

U.S. equity markets closed out a volatile first half at their highest levels of the year as investors cheered data showing continued resilience in economic activity alongside further signs of cooling inflationary pressures. Departing from the "good news is bad news" theme that prevailed for much of the first-half of the year, this week's rally came alongside a surprisingly strong slate of housing market, employment, and GDP data, but perhaps most importantly, another slate of inflation data via the PCE Index and several PMI reports showing that price pressures continue to cool rather significantly.

{kind=link}

Hoya Capital

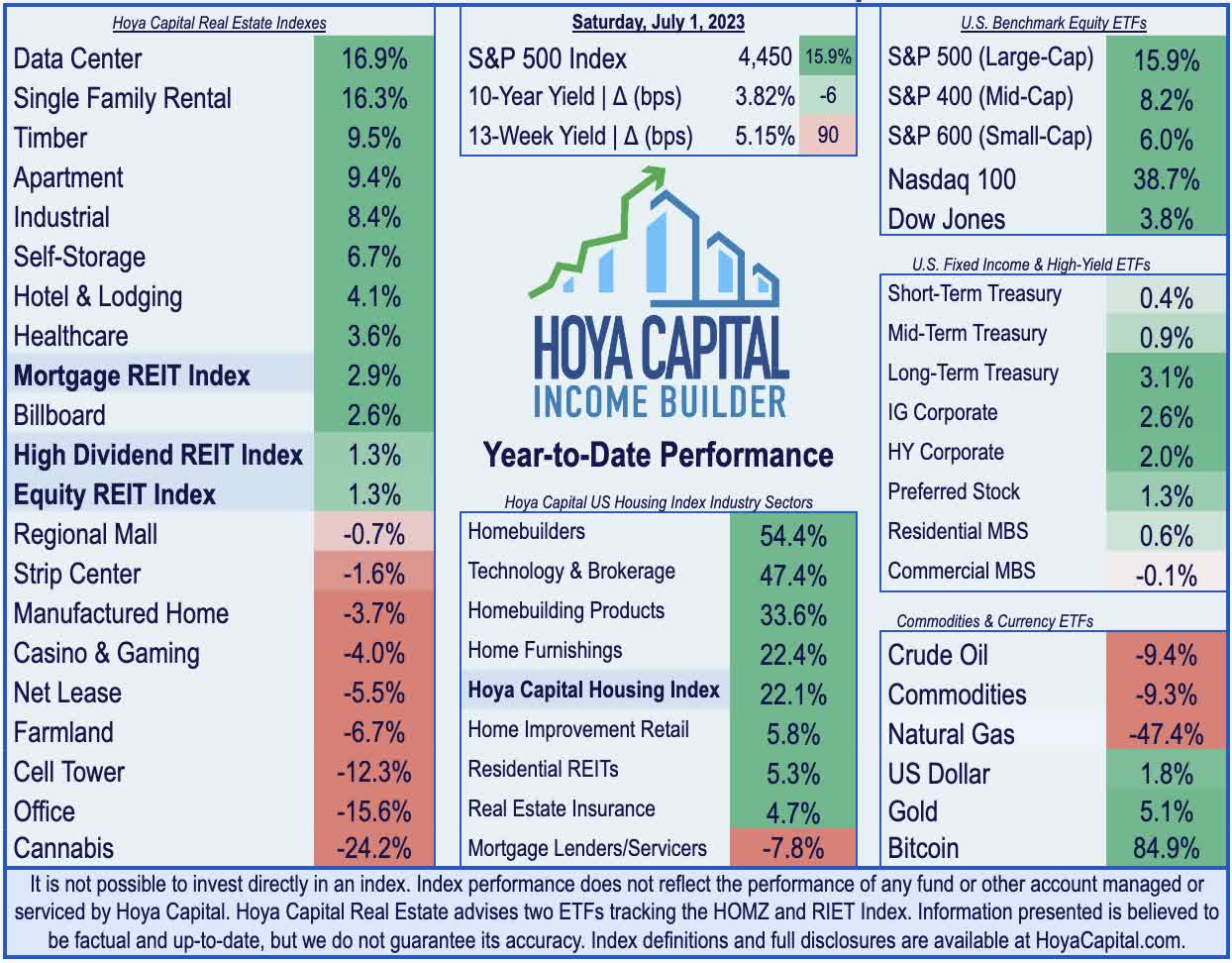

Rebounding from its worst week since March, the S&P 500 advanced 2.3% this week to end the first half at its highest levels since April 2022. While large-cap technology stocks powered the first-half advance, the rally this week was fueled by many of this year's laggards with the Mid-Cap 400 and Small-Cap 600 each advancing more than 4%. The tech-heavy Nasdaq 100 advanced 1.9% on the week to lift its first-half gains to a record-setting 39%. Real estate equities led the rally on the week, lifted by a rebound in many of the most beaten-down property sectors. The Equity REIT Index advanced 4.3% this week with all 18 property sectors in positive territory, while the Mortgage REIT Index rallied 6.1%. Homebuilders and the broader Housing Index continued their impressive rebound this year as another round of upbeat housing market data showed continued stabilization - an even glimmer of strength - as the industry emerges from a year-long recession.

{kind=link}

Hoya Capital

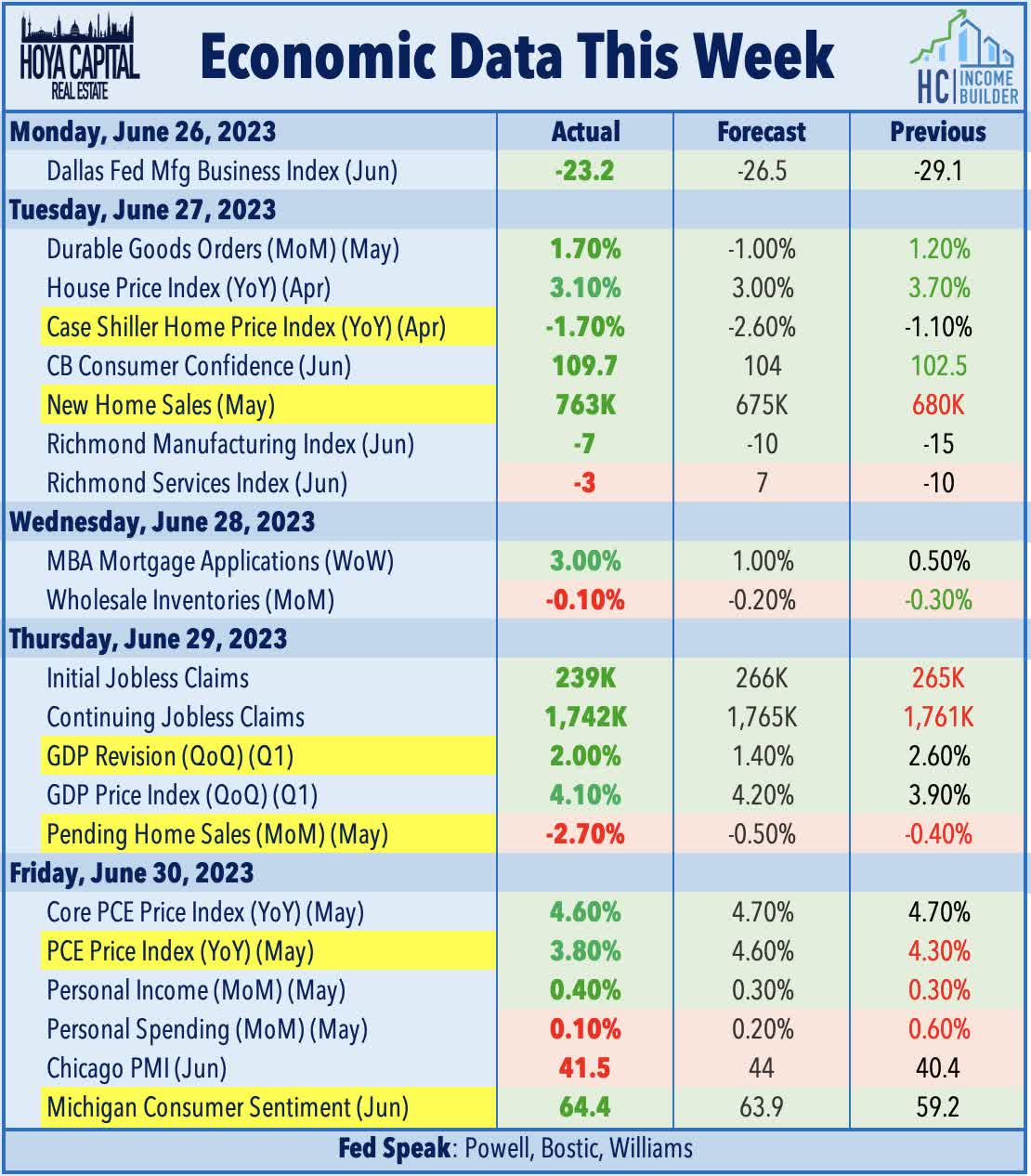

In addition to the strong slate of housing data, initial jobless claims retreated in the holiday-shortened week, challenging some of the softness seen over the prior three weeks of reports. First quarter GDP data was also revised upward to a 2% annualized pace, while Core PCE prices - the report's primary inflation metric - was revised downward. The strong slate economic data lifted the policy-sensitive 2-Year Yield higher by nearly 20 basis points on the week to 4.90, while the 10-Year Yield climbed by 8 basis points to close at 3.82% - each at the highest end-of-week close since early March. Swap markets now imply an 85% probability of a 25 basis point Fed rate hike this month and a nearly 40% chance of a second Fed rate hike by year-end. All eleven GICS equity sectors finished higher on the week, led to the upside by the Real Estate ( XLRE ) and Energy ( XLE ) sectors. WTI Crude Oil prices - a key "swing input" in the domestic inflation outlook - rebounded by about 2% this week but remains more than 35% lower from last year.

{kind=link}

Hoya Capital

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

Hoya Capital

As discussed this week in Homebuilders: Why This Time Was Different , to the surprise of countless pundits, the U.S. housing industry has quietly started to emerge from its year-long recession, thawing from a deep freeze induced by historically aggressive monetary tightening. Higher mortgage rates have delayed - but not permanently altered - the existing secular fundamentals supporting the single-family market: a "lost decade" of single-family construction ahead of a wave of demographic-driven demand. After dipping to eight-year lows in late 2022, data this week showed that New Home Sales surged in May to the strongest level since early 2022 to a seasonally-adjusted annual rate of 763k - significantly higher than the 675k consensus expectation - which marked the first year-over-year increase in two years. The rebound in new construction activity comes as housing inventory levels continue to hover around historic lows, a low-supply dynamic that has provided support to home values during the housing correction from mid-2022 through early 2023 induced by aggressive monetary tightening. This week, the Case Shiller Home Price Index showed that home prices rose for a third straight month in April, following a stretch of seven-straight monthly declines.

{kind=link}

Hoya Capital

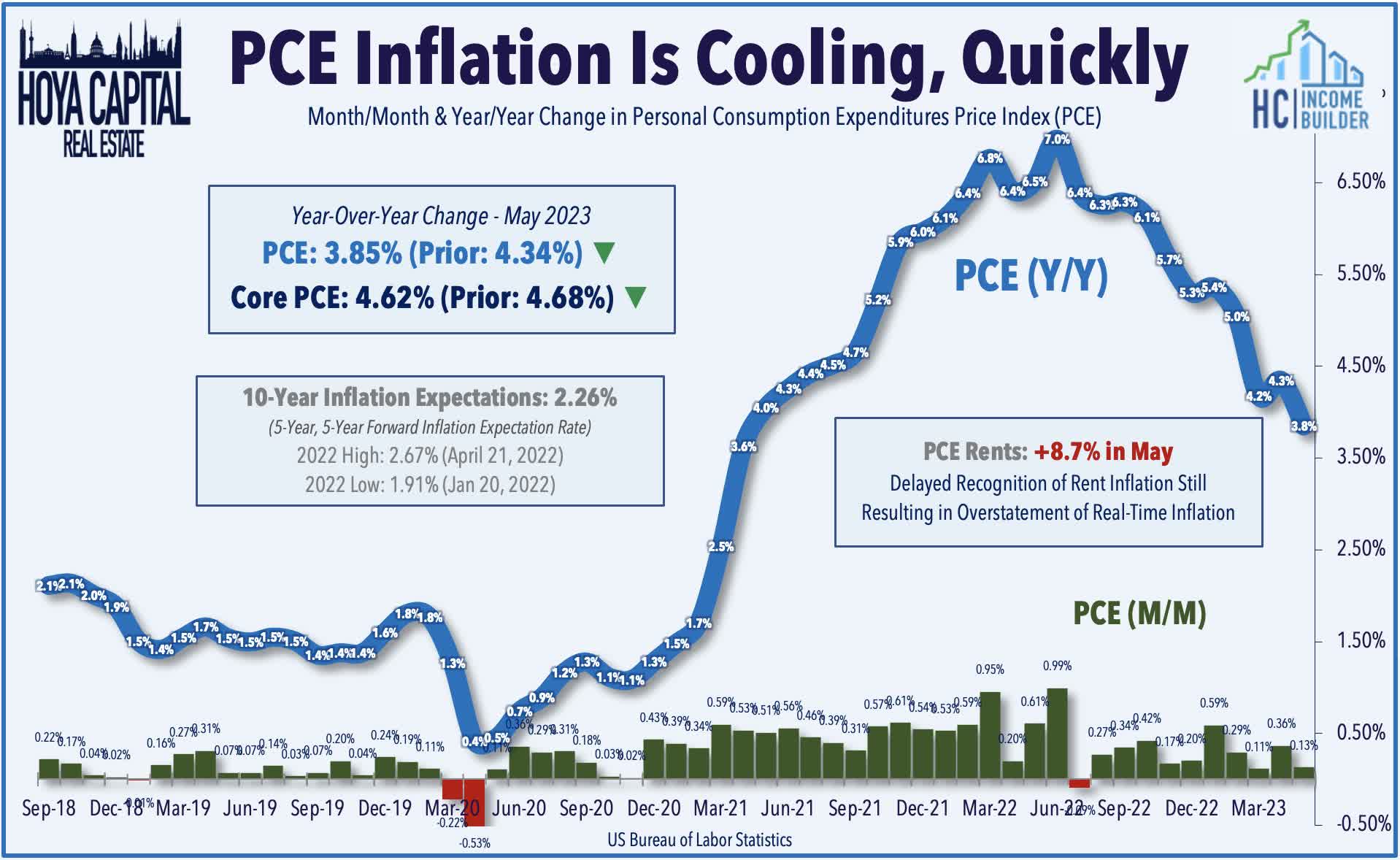

Continuing the stretch of "good news" on the inflation front seen over the past several months, the closely-watched PCE Index provided further evidence that price pressures have cooled rather significantly in recent months. The Personal Consumption Expenditures (PCE) Price Index rose just 0.1% in May - well below the 0.5% consensus expectation - which dragged the year-over-year increase to below 4% for the first time in over two years. The delayed recognition of shelter inflation continues to heavily distort the headline and core metrics, however, resulting in a significant understatement of inflation from mid-2021-2022 and an overstatement of inflation since mid-2022. Consistent with the trends observed in the Consumer Price Index, the PCE Index has averaged less than 2% since last July when excluding the shelter component.

{kind=link}

Hoya Capital

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Hoya Capital

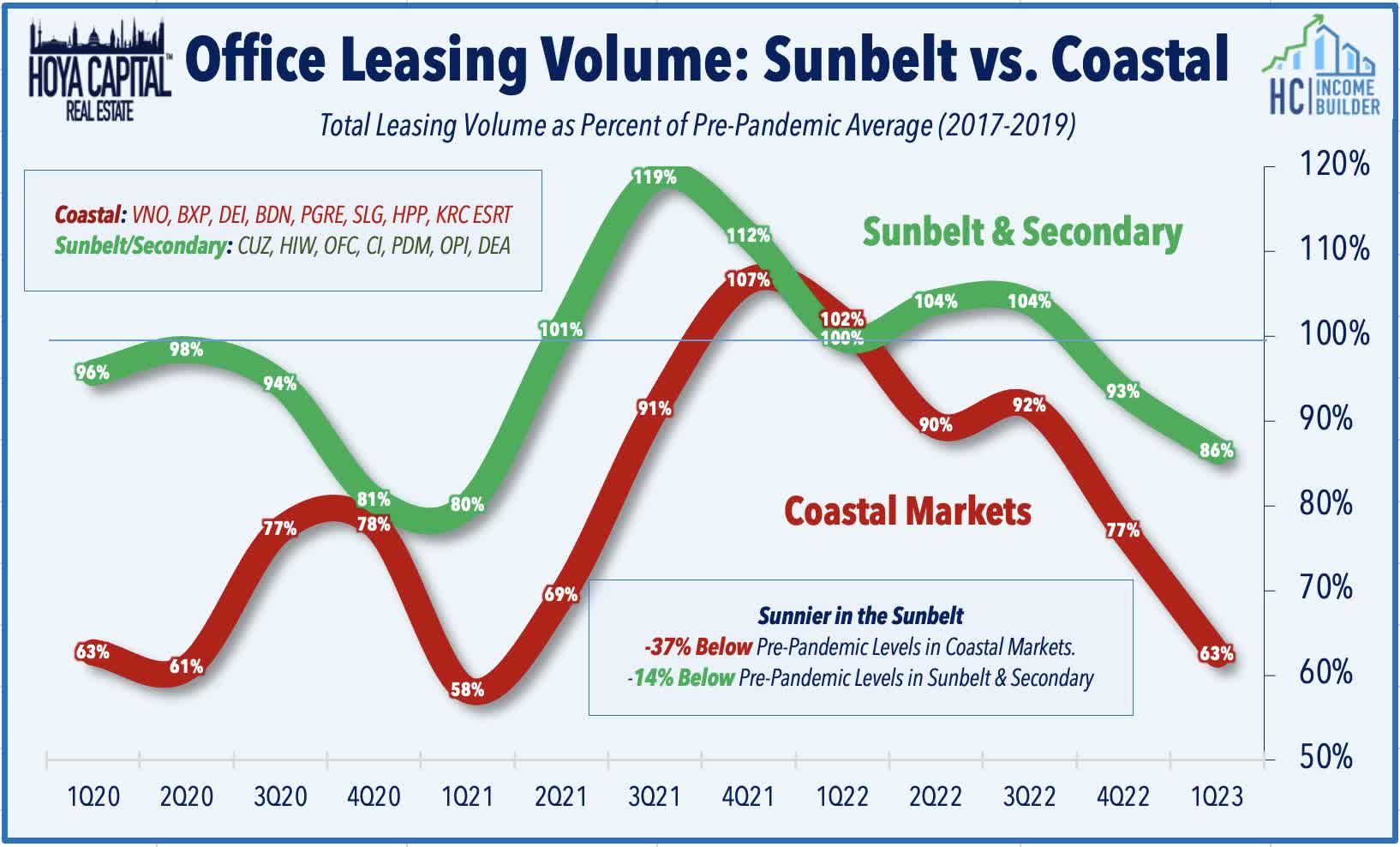

Office : Leading a sharp rebound this week across the office REIT sector, SL Green ( SLG ) rallied nearly 30% after it announced that it sold a 49.9% interest in 245 Park Avenue to Japanese developer Mori Trust at a gross asset valuation of $2.0 billion - a notably strong print that was consistent with the valuation provided by SL Green last September when it acquired the property out of bankruptcy from China’s HNA Group. The purchase price implies a capitalization rate in the high 3% range, a head-turning print that comes as SLG and other office REITs trade in public markets at implied cap rates at more than double those levels. Nearly a dozen office REITs posted double-digit gains this week, including a 25% rally from fellow NYC-focused office REIT Vornado ( VNO ) and a 14% surge from Boston Properties ( BXP ), the largest office REIT. SLG noted that the sale represents the largest part of the company's fundraising plan for 2023, following its $500M refinancing of 919 Third Avenue in April. In our latest Office REIT report, we noted that debt service expenses - not property-level cash flows - has been the primary culprit behind the wave of recent loan defaults and discussed that there's more nuance to the story than the prevailing narrative would suggest.

{kind=link}

Hoya Capital

Net Lease : EPR Properties ( EPR ) rallied nearly 8% this week after it announced that it reached a comprehensive lease restructuring deal with struggling movie theater operator Regal Cinemas which includes a new master lease for 41 of the 57 properties and the termination of operations at 16 properties. Roughly 40% of EPR's revenues come from movie theater operators, an industry that has struggled to regain its footing following a year of COVID-related shutdowns. EPR expects the deal to achieve 96% of total pre-bankruptcy rent in 2024 if certain performance-based thresholds are fully met. The restructured deal will be anchored by a new master lease for 41 properties, a triple-net lease with $65 million in total annual fixed rent, which will escalate by 10% every five years. EPR will reimburse Regal for "revenue enhancing improvements" to these properties up to a maximum of $32.5M. The weighted average lease term was increased by four years to 13 years. EPR will take back 16 theatres previously operated by Regal, four of which will now be operated by Cinemark and one will be operated by Phoenix Theatres. The remaining 11 theatres will be marketed for sale.

{kind=link}

Hoya Capital

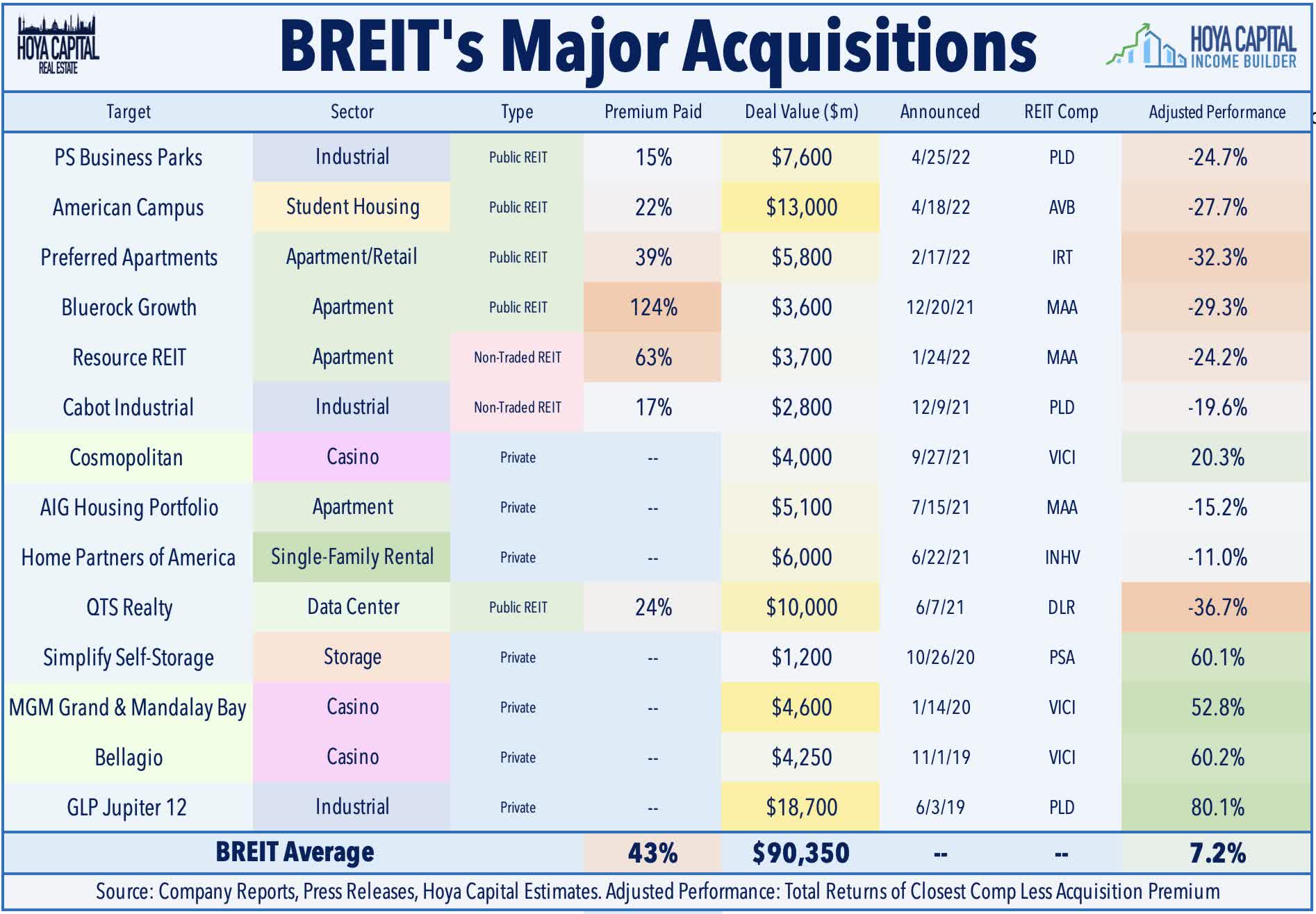

Casino : As predicted in our Casino REIT report earlier this year, Bloomberg reported this week that Blackstone ( BX ) is indeed fielding offers for its stake in the Bellagio hotel in Las Vegas held by its non-traded fund, BREIT, as it seeks to raise capital to meet investor withdrawal requests. BREIT had acquired the Bellagio from MGM Resorts ( MGM ) in 2019 for $4.25B, and we noted in the report its four casino holdings were among the few assets owned by BREIT that it could sell for more than what it paid, which may be relevant as its self-reported mark-to-market valuations come under closer scrutiny. In late 2022, BREIT sold two of these four casinos - MGM Grand and Mandalay Bay - to VICI Properties ( VICI ) for $5.5B. The report comes a day after Blackstone's opportunistic fund sold $3.1 billion of logistics properties to industrial REIT Prologis ( PLD ) and several weeks after BREIT sold a Texas report to Ryman Hospitality ( RHP ) for $800M in cash, which have served as prime examples of a public REITs using their balance sheet "firepower" to take advantage of opportunities presented by debt-burdened private portfolios.

{kind=link}

Hoya Capital

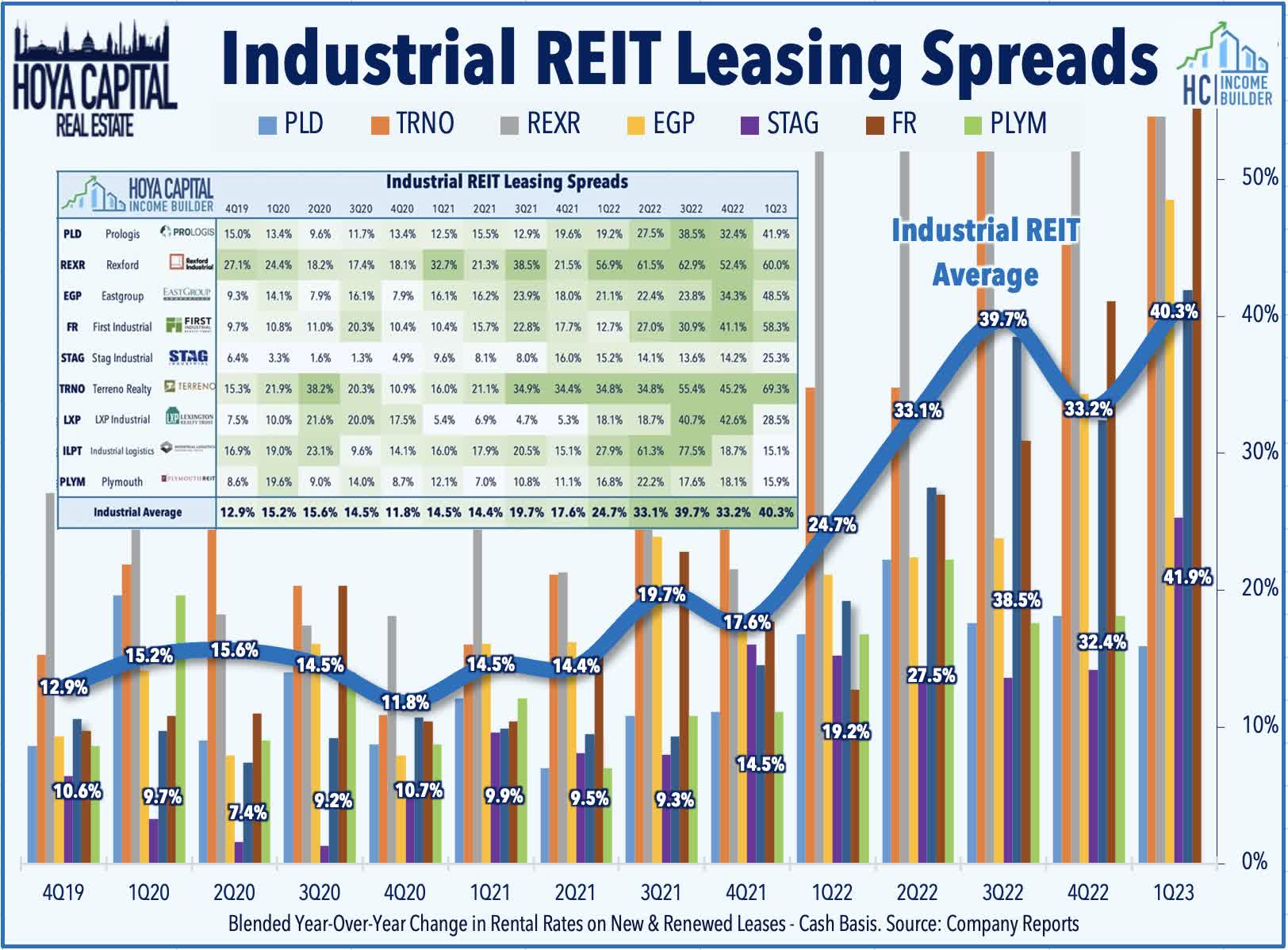

Industrial : On cue, Prologis ((PLD)) - the largest industrial REIT - rallied nearly 5% this week after it announced a $3.1 billion deal to acquire from Blackstone nearly 14 million square feet of industrial properties from its opportunistic real estate funds. The industrial portfolio consists of approximately 70 properties across the country, and the deal is expected to close within a month. The acquisition price, funded by cash, represents an approximately 4% cap rate - another remarkably strong valuation print - which equates to roughly 6% adjusted cap rate using current market rents. In our latest Industrial REIT report, we noted that recent earnings results showed that demand continues to substantially outpace available supply, fueling a continued acceleration in rent growth. Rental spreads averaged over 40% in Q1, while occupancy rates climbed to fresh record highs. Strengthening rent growth comes despite substantial downward pricing power across other areas of the supply chains and concerns of weakness in West Coast logistics markets. The Freightos Global Container Freight Index is now nearly 90% below its peaks seen in late 2021 and 80% lower on a year-over-year basis, serving as a powerful disinflationary force on goods prices.

{kind=link}

Hoya Capital

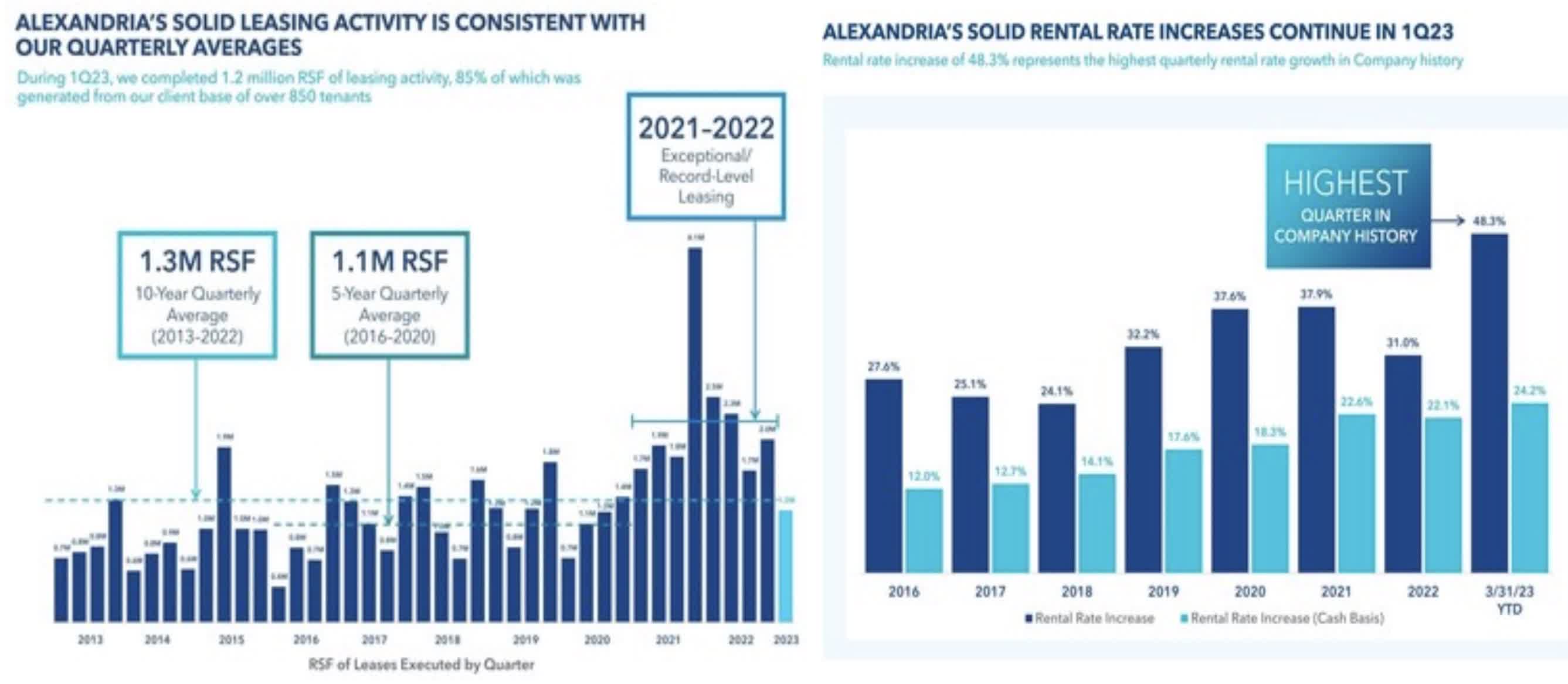

Healthcare : Alexandria Real Estate ( ARE ) - which is the latest REIT that has fallen into the cross-hairs of short-sellers - advanced 5% this week after it announced that it sold a new development property within its Alexandria Center for Life Science in Boston for $155M, which follows the announcement last week of the sale of five properties in Boston for $365M. ARE also announced an expanded credit facility which increases its borrowing capacity by another $1B. Activist firm Land and Buildings published a short report earlier this month focused on the daily utilization rate of ARE's lab space facilities, which L&B says is 50% below pre-pandemic levels based on cell phone data estimated by data firm Placer AI. L&B - which has a short position in ARE - says that combined with the high levels of supply growth, "lab space fundamentals appear set to rapidly deteriorate." ARE pushed back with a business update this week in which it reiterated its full-year outlook calling for FFO growth of 6.4%, which would lift its cumulative FFO growth since the end of 2019 to nearly 30%, among the highest in the REIT industry.

{kind=link}

Hoya Capital

Healthcare : Sticking in the healthcare space, small-cap Diversified Healthcare ( DHC ) rallied over 10% despite disclosing that a non-monetary event of default has occurred under its $450 million credit facility after a property reappraisal resulted in a value 22% decline from $1.34 billion to $1.05 billion, below the $1.09 billion threshold required under the facility. DHC reported that it is working with lenders to obtain a waiver through September 30, the outside closing date for DHC’s pending merger with Office Properties Income Trust ( OPI ), at which time DHC’s $450 million credit facility will be fully refinanced. The controversial merger continues to receive pushback, however, as Flat Footed filed a definitive proxy statement and sent a letter to shareholders outlining its opposition to the proposed merger between two struggling REITs that are both externally managed by RMR Group.

{kind=link}

Hoya Capital

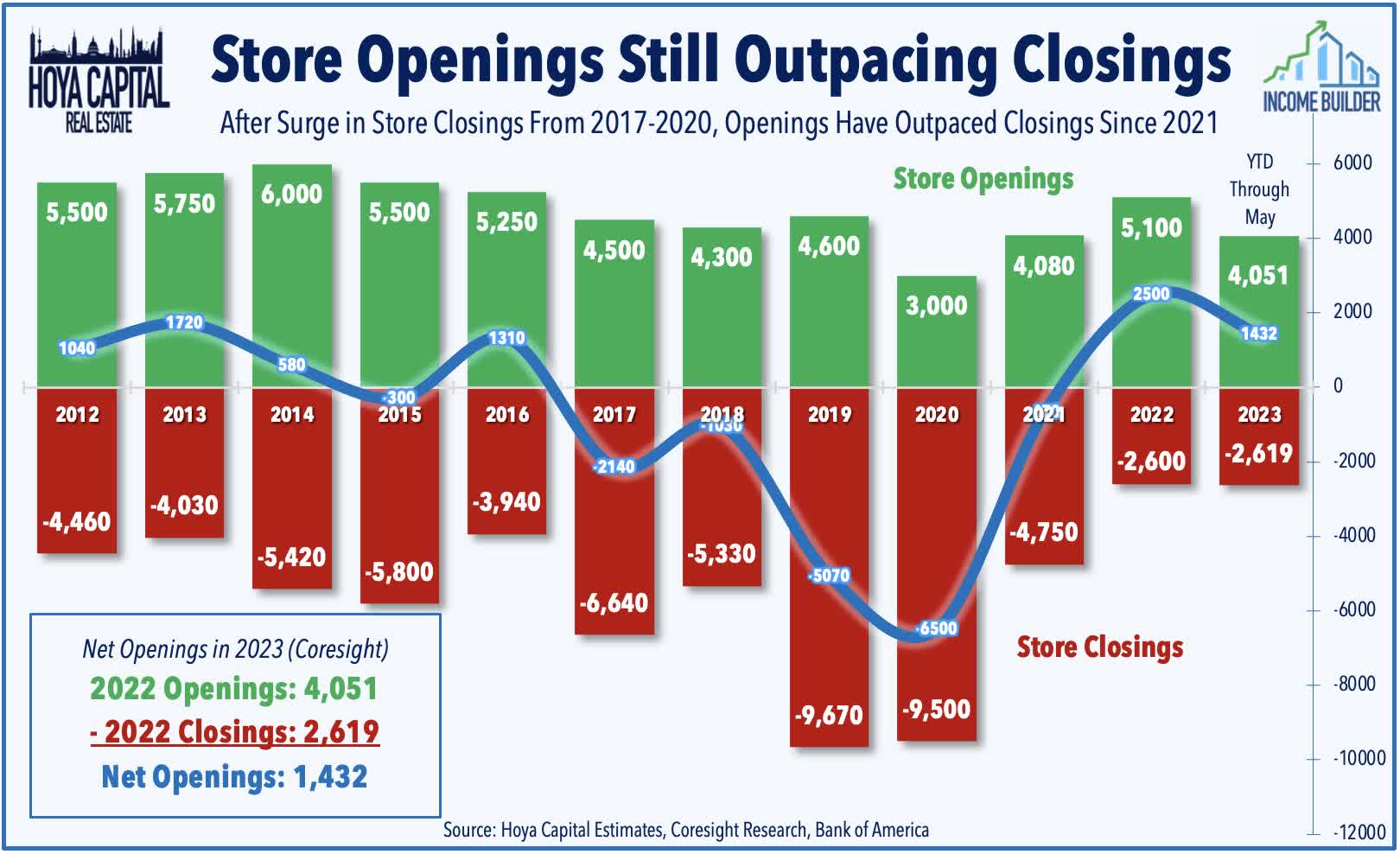

Strip Center : Last week, we published Strip Center REITs: Back on Sale . Strip Center REIT fundamentals have improved materially over the past year and continue to be underappreciated in the market as a decade-long “retail apocalypse” narrative has been tough to shake. The combination of near-zero new development and positive net store openings since 2021 has driven occupancy rates to record-highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. These favorable property-level supply/demand fundamentals have translated into impressive double-digit rent growth spreads since mid-2022 and the best earnings “beat rate” of any property sector during that time. Despite several high-profile retail bankruptcies - including Bed Bath & Beyond and Party City - store openings have continued to outpace store closings by 50% so far in 2023, led by demand for space in large-format open-air strip centers. A "higher for longer" monetary environment may be ideal for well-capitalized Strip Center REITs with the balance sheet firepower to accretively consolidate as debt-dependent private owners seek an exit.

{kind=link}

Hoya Capital

REIT Capital Raising & REIT Preferreds

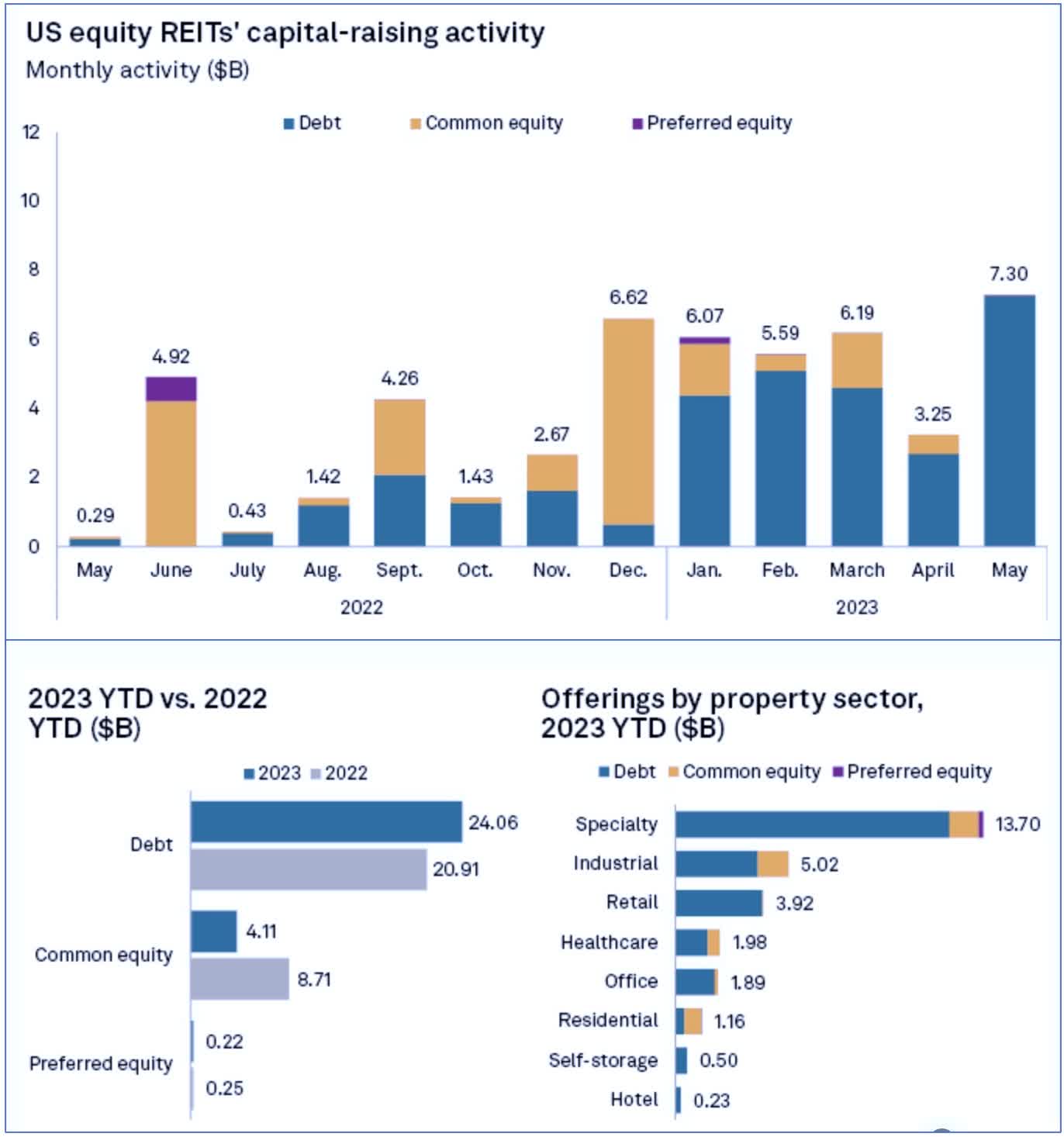

Several REITs were active on the capital-raising front this week. As noted above, Realty Income ( O ) raised $1.2B in Euro-denominated debt split into two tranches: €550 million of 4.875% senior unsecured notes due July 2030 and €550 million of 5.125% senior unsecured notes due July 2034. Fellow net lease REIT Agree Realty ( ADC ) announced it has received commitments for an unsecured $350 million 5.5-year term loan. S&P Global Market Intelligence reported this week that U.S. equity REITs have picked up the pace of capital raising after a slow start to 2023. REITs raised $7.3B in new capital in May, the biggest monthly haul since early 2022. Nearly all of the capital - $7.28B - came through debt offerings as REITs took advantage of a modest pull-back in interest rates. American Tower ( AMT ) raised $2.7B during the month, while Welltower ( WELL ) and Iron Mountain ( IRM ) each raised $1.0B in new capital. The offerings in May brought the year-to-date total to $28.40 billion, which is roughly 5% below the capital raised during the same period in 2022.

{kind=link}

Hoya Capital

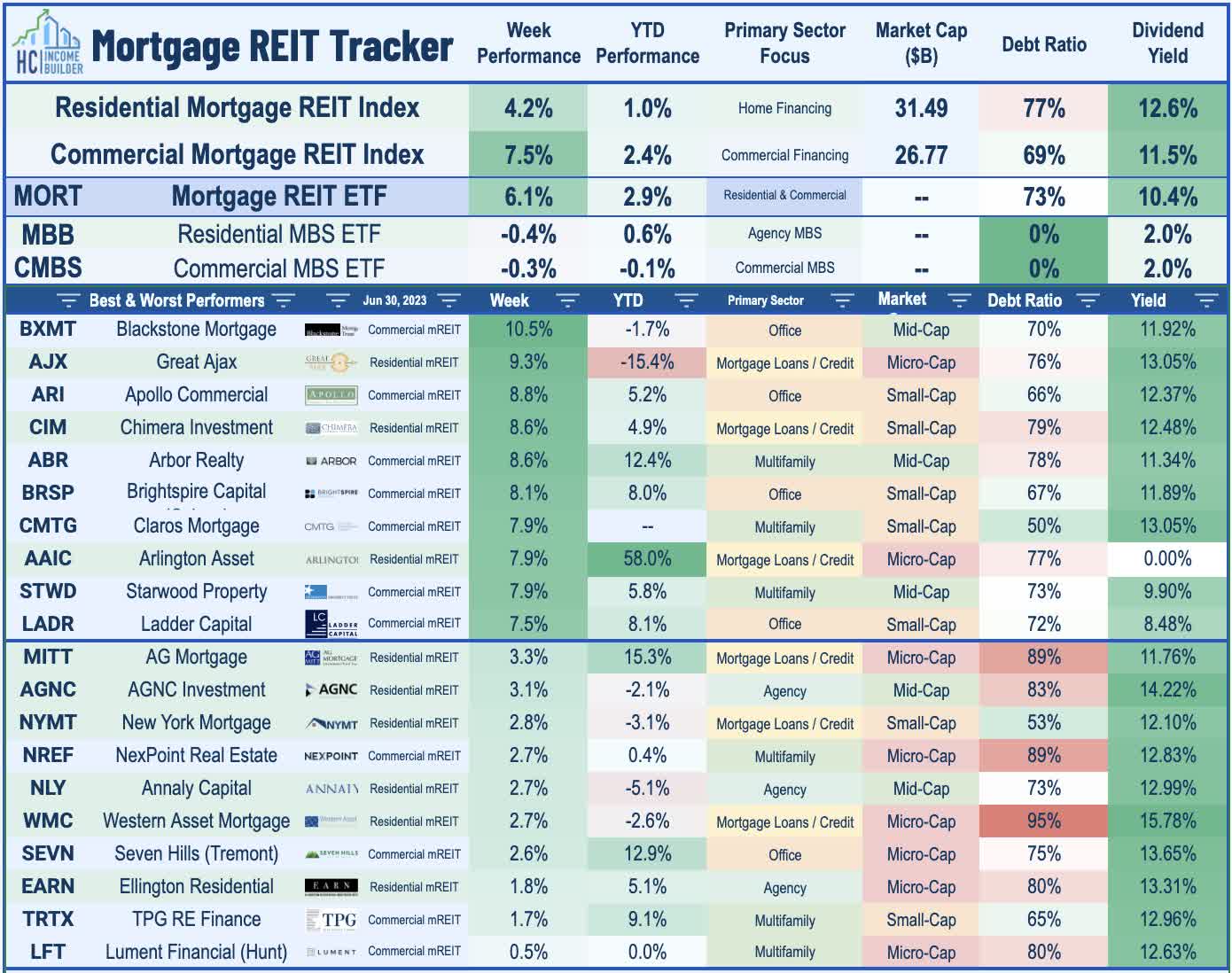

Mortgage REIT Week In Review

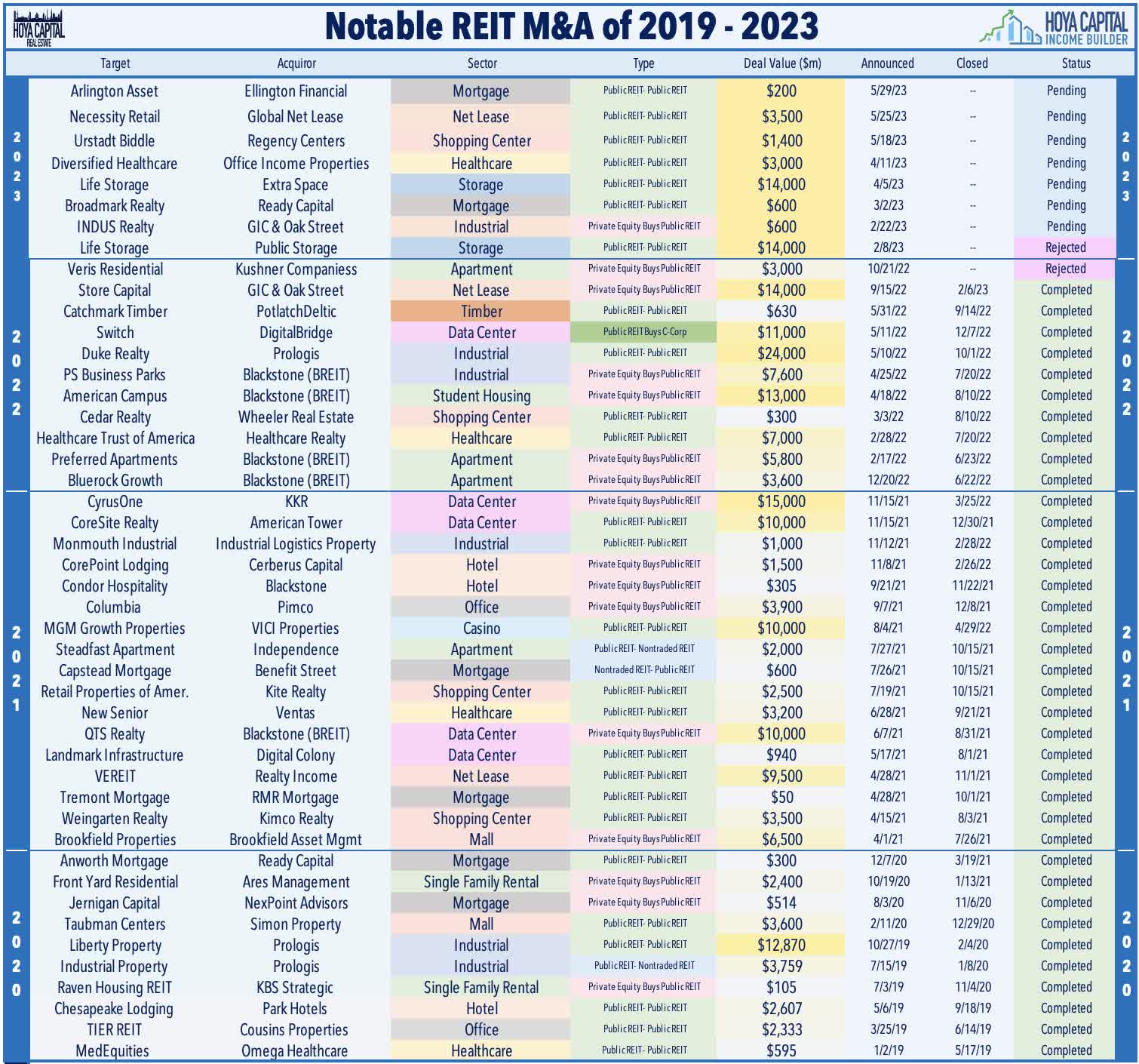

Mortgage REITs rebounded this week, with the iShares Mortgage REIT ETF ( REM ) advancing more than 6%, concluding a volatile first half that saw the benchmark dip nearly 30% in the wake of the Silicon Valley Bank collapse in March before gaining back essentially of this lost ground over the subsequent quarter. This week saw the third merger involving a mortgage REIT this year. Micro-cap Western Asset Mortgage ( WMC ) was among the laggards this week after it announced that it would merge with Terra Property Trust - a non-traded mortgage REIT externally managed by Mavik Capital Management - in an all-stock deal that is expected to close in Q4. The combined company - which will continue to be listed on the NYSE under a new name - will have a combined asset base of $1.2B and $436M of adjusted book value. The deal follows a pair of mREIT-to-mREIT mergers earlier in 2023, including Ellington Financial's ( EFC ) acquisition of Arlington Asset ( AAIC ) in May and Ready Capital's ( RC ) acquisition of Broadmark Realty in March.

{kind=link}

Hoya Capital

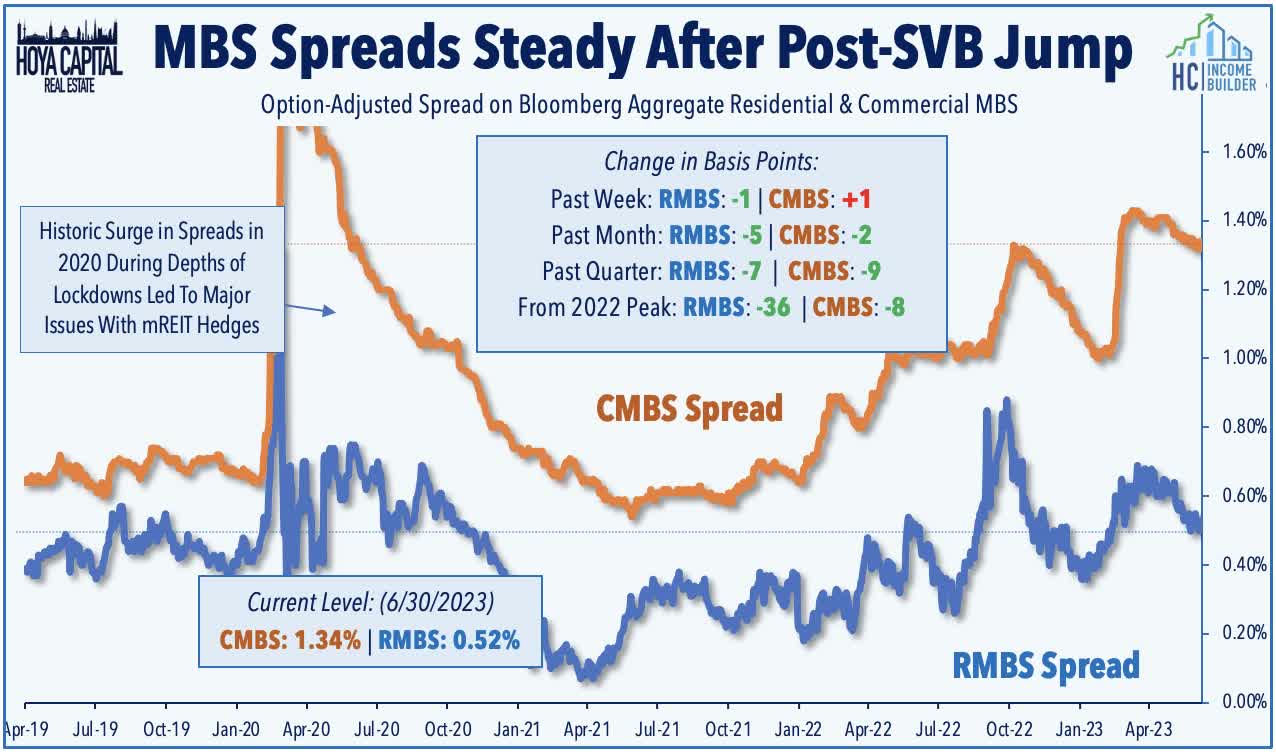

This week, we published Mortgage REITs: High-Yield Risk and Opportunity . Recovering from a sharp sell-off in the wake of the Silicon Valley Bank collapse, Mortgage REITs have rebounded as turmoil across interest rate markets has calmed. Distress in the commercial and residential real estate markets has been more isolated than the 'scary' magazine covers would suggest. Outside of urban office properties, default rates remain near pre-pandemic lows. Dividend cuts have come as a 'ripple' rather than a 'wave' with 10 of 40 mREITs reducing their dividends this year, but industry-wide payouts are only down about 5% YTD versus 60% in 2020. The squeeze on highly-levered private market portfolios is still in the early innings, however, but an orderly unwind remains the base case. Spreads on mortgage-backed bonds ("MBS spreads") narrowed during the second quarter - an important input into Book Value models. At 0.52%, Residential MBS spreads have tightened by about 7 basis points since the end of Q1. Commercial MBS spreads are still relatively elevated at levels that are roughly even with their 2022 highs at 1.32%, but down about 9 basis points since the end of Q1.

{kind=link}

Hoya Capital

2023 Performance Recap & 2022 Review

Through the first half of 2023, the Equity REIT Index is now higher by 1.3% on a price return basis for the year (+3.4% on a total return basis), while the Mortgage REIT Index is higher by 4.0% (+7.3% on a total return basis). This compares with the 15.9% gain on the S&P 500 and the 8.2% advance for the S&P Mid-Cap 400 . Within the real estate sector, 9-of-18 property sectors are in positive territory on the year, led by Data Center REITs, Single-Family Rental, Timber, and Apartment REITs, while Office and Cell Tower REITs have lagged on the downside. At 3.82%, the 10-Year Treasury Yield has declined by 6 basis points since the start of the year - up from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 2.1% this year. Crude Oil - perhaps the most important inflation input - is lower by 9% on the year and roughly 40% below its 2022 peak.

{kind=link}

Hoya Capital

Economic Calendar In The Week Ahead

Employment data highlights a critical week of economic data in the holiday-shortened week ahead, headlined by ADP Payrolls data, the JOLTS report, and Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 200k in June, which follows a strong month of May in which the economy added 339k jobs. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for April - is expected to show a cooldown in wage growth in June to 4.2%. 'Good news is bad news' will likely be the theme of these reports as several Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on a long-awaited cooldown in labor markets. As noted above, swaps markets imply a 85% probability that the Fed will hike rates by 25 basis points in their mid-July meeting to a 5.50% upper bound, continuing the swiftest rate hike cycle since the early 1980s. U.S. equity and bond markets will be closed on Tuesday for Independence Day and have a shortened session on Monday.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

REITs Lead Quarter-End Rally