CA - Restaurant Brands International: High-Quality Brands With Substantial Opportunity

2023-12-30 09:00:00 ET

Summary

- Restaurant Brands International is one of the largest quick-service restaurants in the world.

- I believe the appointment of J. Patrick Doyle as Executive Chair of the Board should create value for shareholders.

- RBI is underpinned by strong high quality brands that should enable for predictable cash flow.

- Using a discounted cash flow analysis, I arrived at an implied share price of $83.88.

Investment Thesis

I assign a "BUY" on Restaurant Brands International ( QSR ) with an implied share price of $83.88. RBI is an asset-light business with growing royalties underpinned by high-quality brands such as Burger King, Tim Horton, Popeyes, and Firehouse Subs. I believe the involvement of the new chairman can benefit the company, given his deep industry knowledge and experience. Additionally, the company is also trading at an assertive valuation.

1. High-Quality Brands

Although RBI operates in an industry with intense competition, I think the company commands a competitive advantage, given its brand equity. As of September 30, 2023, Burger King had 19,035 units, solidifying its position as the second-biggest burger player after McDonald's. BK Store count has grown at 6% CAGR from 2017 to 2022, and system-wide sales by +8%. In 2017, 21% of sales were digital; that figure has expanded to 51% TTM, which is impressive, to say the least.

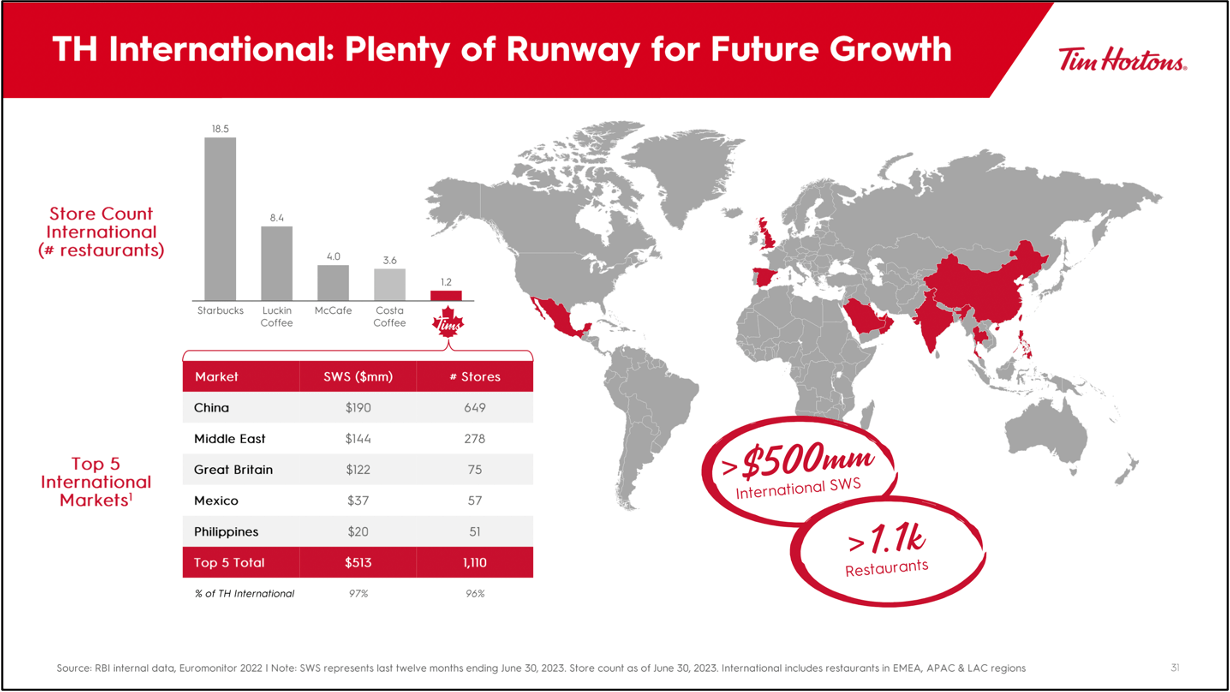

Unlike RBI's other brands, which are involved in burgers and sandwiches, Tim Hortons' "TH" is more of a coffee, donut, and tea restaurant chain. It is one of the largest in North America and the largest in Canada, as measured by the total number of restaurants. As of September 30, 2023, TH had 5701 units, up by 18% from December 31, 2018 (4,846 units). Sales have grown at a 5% CAGR over the same time period, including the big drop in 2020 and 12% excluding it.

I don't believe TH will add units as fast as RBI's other brands, such as PLK, despite having a similar opportunity abroad . The reason I say this is because coffee chains are highly competitive, and brand recognition plays a vital role. Starbucks (SBUX) already has a big presence abroad and a strong brand. It is extremely hard to get customers to shift from their SBUX coffee or drink to TH, speaking from personal experience. Dunkin' Donuts is also another major player.

{kind=link}

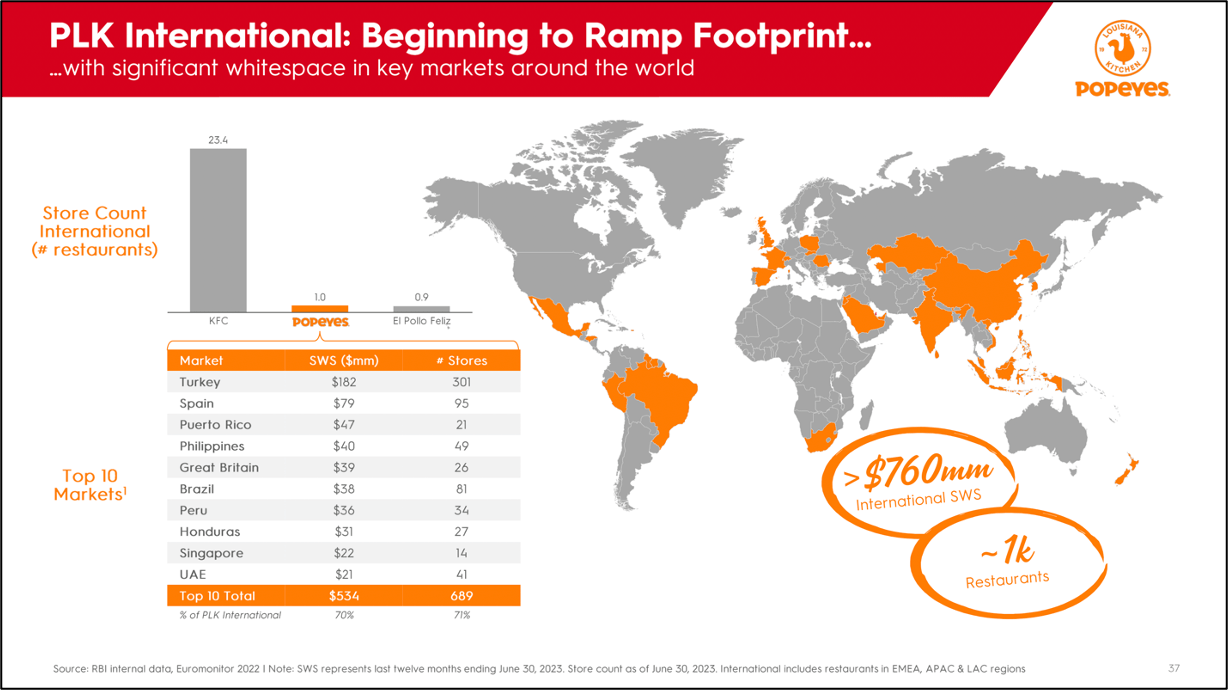

Popeyes Louisiana Kitchen is the world's second-largest chicken "QSR" (behind KFC), with a store unit of 4,373 compared to KFC's 23.1 thousand. As you can see below, unlike BK, PLK has substantial room for international expansion, given its small store presence abroad. Despite growing revenues at a CAGR of 12% over the past four years, I believe PLK can potentially grow sales in the mid-double digits, if not higher. In the recent quarterly earnings, PLK had the most net restaurant unit growth year-over-year, and sales grew by 16%.

{kind=link}

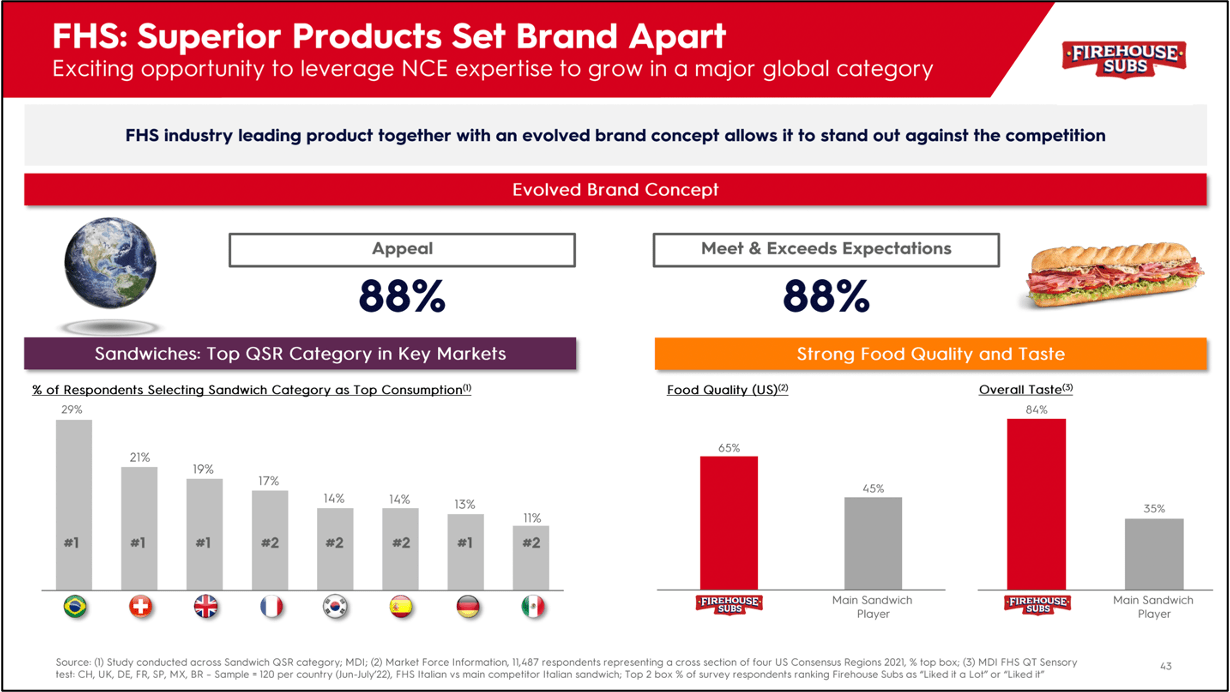

As for Firehouse Subs, it is a relatively new brand to the portfolio, acquired by RBI in 2021 for $1 billion. FHS is a leading player in the QSR sandwich category in North America. As of the recent quarter, FHS had 1,266 units featuring hot and hearty subs piled high with quality meats and cheese, as well as chopped salads, chili and soups, soft drinks, and other things.

Same story with FHS as PLK: RBI opened the first FHS restaurant outside of the U.S. and Canada in June 2023, located in Switzerland. I believe FHS will start to grow exponentially as the company expands into countries where sandwiches are a top pick for customers in the QSR market, such as Brazil, Switzerland, the U.K., and more.

{kind=link}

I believe the company's strategy to acquire high-quality brands will allow them to sustain their business in the long term, given the intense competition within the sector. Additionally, I like the firm's brand diversification, which enables it to capture more of the QSR market and reduce risk in terms of both brand dependency and geography.

2. New Chairman

Effective January 2, 2023, RBI's board appointed J. Patrick Doyle as Executive Chair of the Board. Mr. Doyle has deep knowledge of how the quick-service restaurant industry works. He had an outstanding and long career at Domino's Pizza ( DPZ ). Serving as the Chief Executive Officer from March 2010 to June 2018, having served as president from 2007 to 2010, as executive vice president of Domino's Team USA from 2004 to 2007, and as executive vice president of Domino's Pizza International from 1999 to 2004.

Not only did he hold multiple positions at DPZ, but he also served as an executive partner focused on the consumer sector of the Carlyle Group (one of the largest PE firms) from September 2019 through November 2022. Bill Ackman's Pershing Square has a ~7% stake in the company. Mr. Ackman has had his ups and downs in turning around companies, but his track record tends to shift more toward the positive side. Pershing Square first took a stake in the company in 2012. I believe as long as he is involved in the firm, shareholders can sleep well at night.

3. Valuation

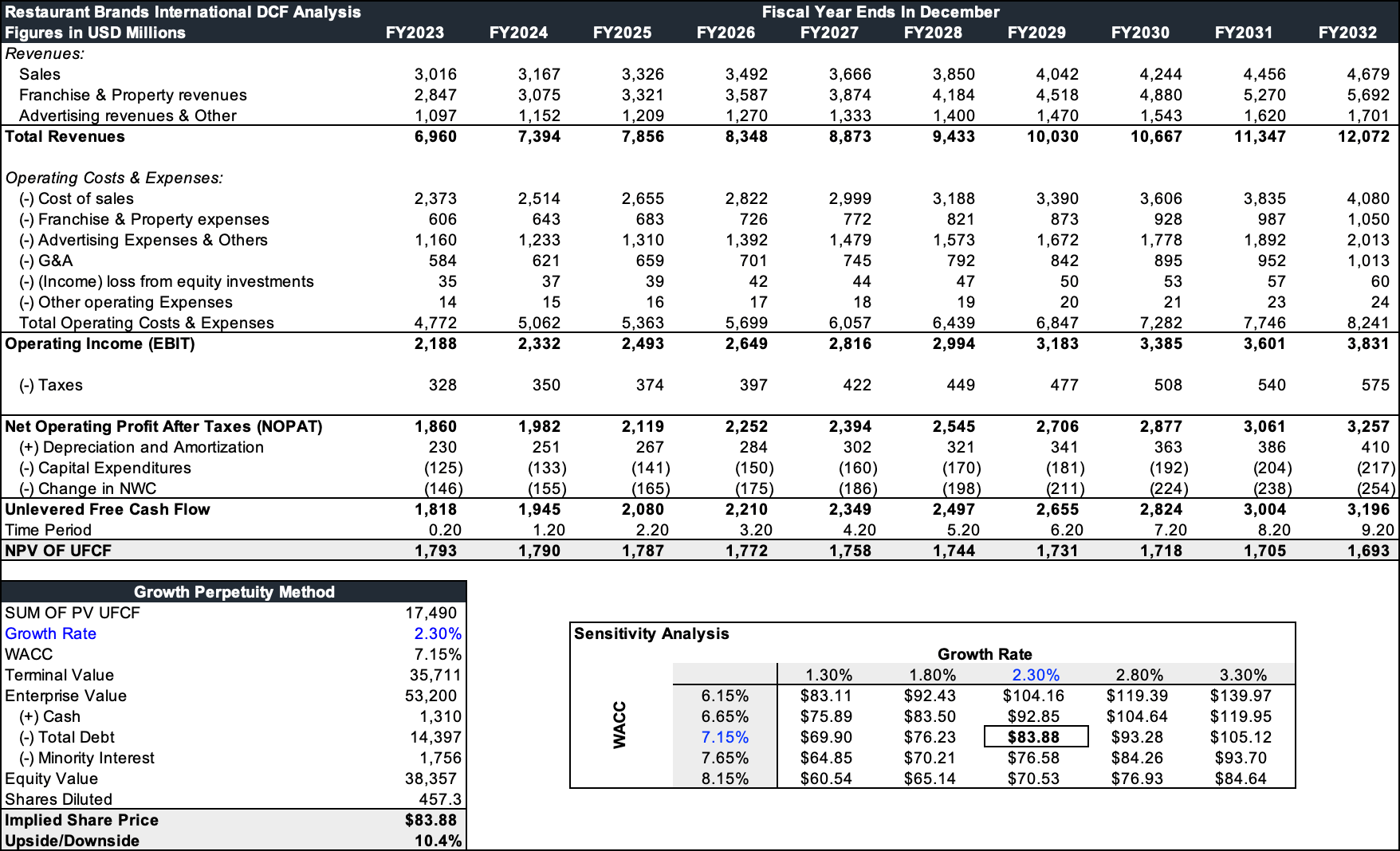

Given the nature of its predictable cash flow, I valued RBI using a discounted cash flow approach. As of the time of this writing, the stock is trading at $77.09 per share. I estimate total revenue to compound at an annual rate of 6.13% from FY2022-FY2032, underpinned by 5% growth in sales, 8% in franchises and property, and 5% in advertising and others. I believe the company can reach its long-term goal of 40,000 stores, given its strong leadership and the substantial opportunity for its brand internationally.

As for my expense assumptions, I went based on historical figures, given that RBI is a relatively stable business. My assumption can be seen below, alongside the historical figures. Using these assumptions, a 2.3% perpetuity growth rate, and a calculated WACC of 7.15% WACC, I arrived at an implied share price of $83.88, which translates into a 10.4% return. RBI is trading at a forward PE of 24.21x the FY23 consensus of $3.23 and 22.48x the FY2024 consensus of $3.43.

{kind=link}

Recent Earnings

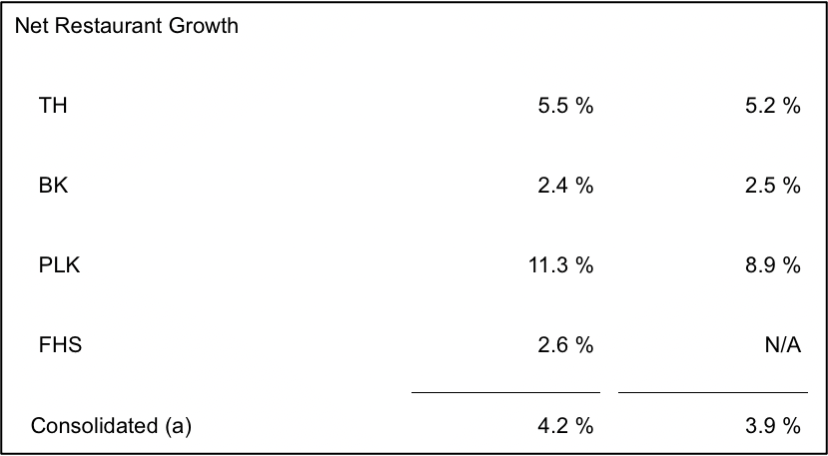

On November 3rd, 2023, RBI reported Q3 results; ADJ EPS came in at $0.90, beating estimates by $0.05 but down from $0.96 from the prior year. Despite missing revenue estimates, RBI posted a strong net restaurant of 4.2%, better than the previous year by 0.3%. As I noted above, PLK still has substantial room for growth internationally; it experienced the most unit growth on a year-over-year basis, with BK coming in second and TH coming in third.

{kind=link}

TH experienced 9.6% system-wide sales growth, BK by 10.3%, PLK by 16.1%, and FHS by 6.9%. Total ADJ EBITDA was $698 million, increasing 9.3% organically, yielding an 80-bps improvement versus the prior year. All in all, I believe the quarter was pretty solid despite the missed revenue. Aside from the strong growth in units and ADJ EBITDA, free cash flow (9% increase YoY) and liquidity.

Key Risks

I believe the key risks facing the RBI are competition, inflation, and consumer health. As I have noted before, The QSR market is highly competitive, with dominant players such as McDonald's ( MCD ), Yum! Brands ( YUM ), Chipotle ( CMG ), and more. It goes without saying that the RBI is highly dependent on consumer spending; elevated inflation levels make consumers tighten their belts, and that could put pressure on the firm's top line.

As for consumer health, given the intense competition, even the slightest news or concerns that the company's food might cause illness, customers' tastes can dramatically shift, leading to millions or perhaps billions of sales lost, as we witnessed with other brands multiple times.

Bottom Line

The main takeaway is that RBI is one of the largest quick-service restaurants underpinned by high-quality brands. I believe even with intense competition. RBI will be able to deliver strong growth and free cash flow as a result of its brand equity and substantial international opportunity. Judging by the last quarterly results, RBI is definitely on the right path, and with the addition of J. Patrick Doyle, I think investors can sleep well at night.

For further details see:

Restaurant Brands International: High-Quality Brands With Substantial Opportunity