REPX - Riley Exploration Permian: A Good Trade-Off For Those Desiring Safety

2023-07-11 07:06:34 ET

Summary

- Riley Exploration Permian offers a degree of stability that many other oil and gas firms do not currently provide.

- REPX has low leverage, which reduces the risk profile for investors now and moving forward.

- Despite not generating much excess cash flow, the company's low leverage ratio and potential for share price appreciation make it an interesting prospect for investors bullish on oil and gas.

When it comes to the oil and gas exploration and production space, it can be tempting to gravitate toward the high leveraged companies because of how cheap they are. The implied upside if all goes well is rather significant. But those who have been invested consistently in this space for the past decade know how that sometimes ends. When prices plunge and hedges are not enough and do not last long enough to keep cash flows elevated and to pay down debt, bankruptcy becomes a real probability. An alternative to taking this approach is to accept return prospects that are lower by investing in companies that have less upside but also less leverage. One of the companies that fits this description is Riley Exploration Permian ( REPX ).

Setting the stage for cash flow

{kind=link}

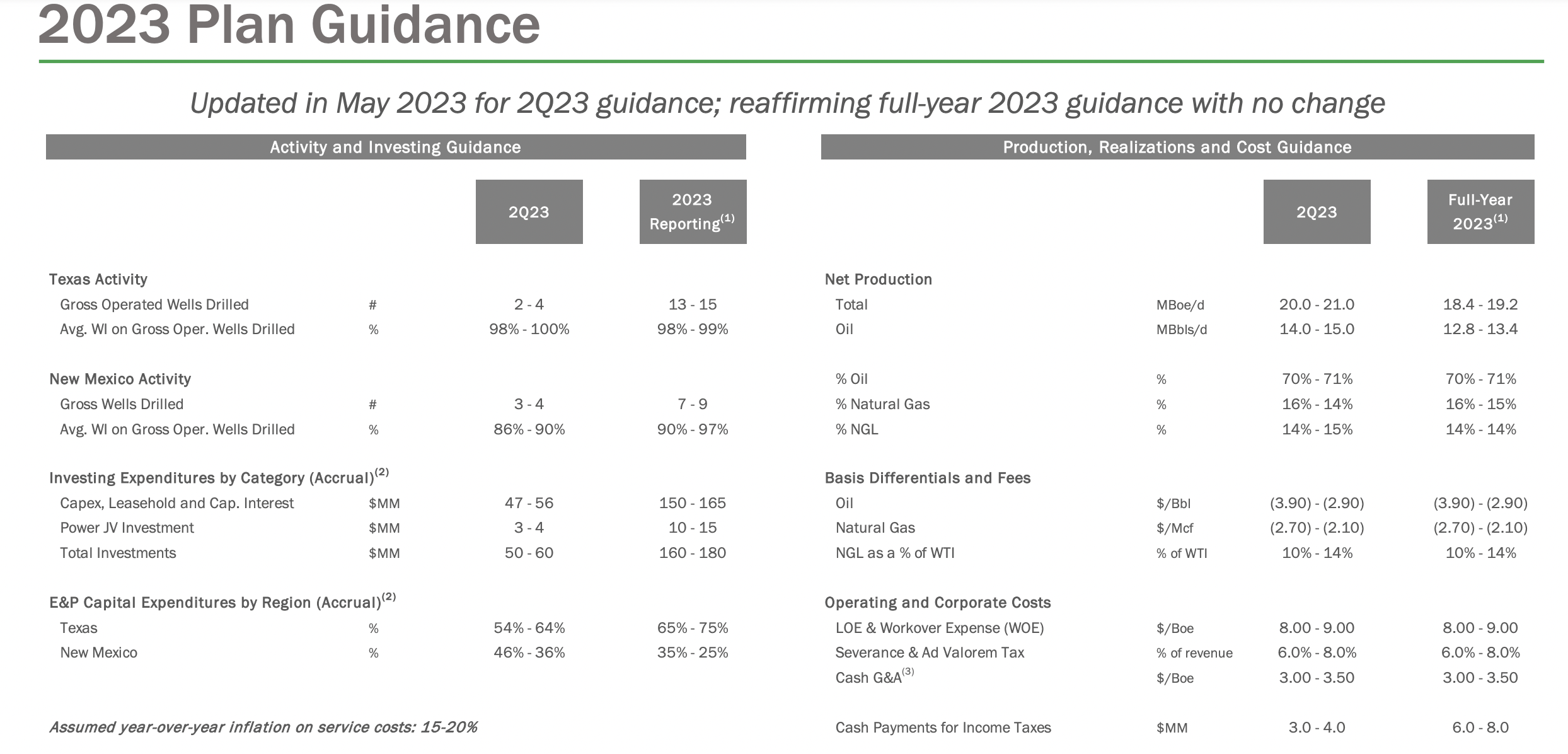

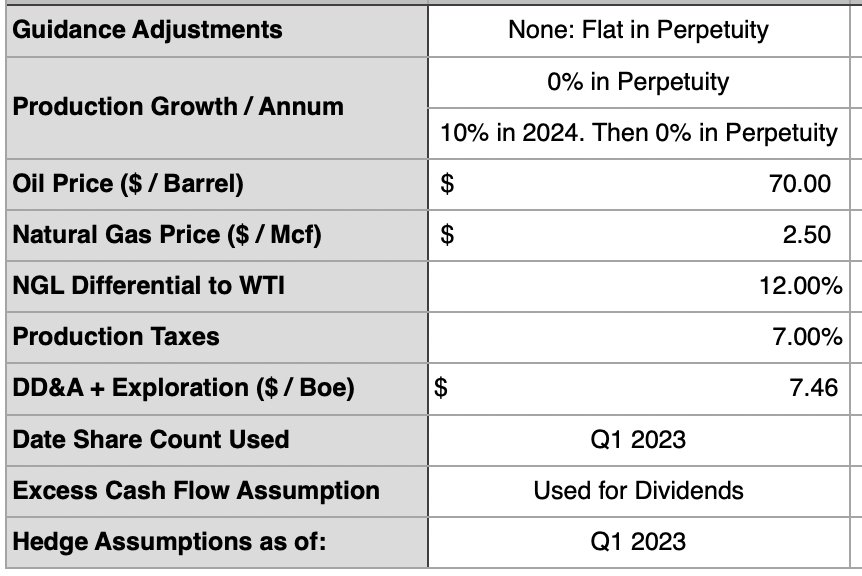

Before I get into matters too deep, I would like to say that the purpose of this article is to provide a cash flow deep dive of Riley Exploration Permian and to see how much upside potential, if any, the company offers based on its cash flow. To do this, I had to have certain assumptions that went into creating my cash flow model. Fortunately, the management team at Riley Exploration Permian is fairly detailed in terms of what they think the company should be capable of for the current fiscal year. These assumptions can be seen in the image above. However, there were a couple of assumptions that I had to create on my own based on a historical review of the company's financial performance . These can be seen in the table below.

{kind=link}

The big unknown from all of this is what to expect from future periods of time. Management has provided guidance for the current fiscal year. However, they continue to allocate capital toward growth and recently completed an acquisition. This muddies the waters to some degree. Because of this, I decided to look at two different scenarios. The first scenario is the most conservative one. It assumes that keeping capital expenditures flat at $170 million annually will keep output flat in perpetuity from what the company is expecting this year. The more liberal scenario, and a scenario that I think is more probable than the conservative one given the acquisition, is that this kind of spending will help production grow by 10% next year before leveling off in perpetuity thereafter.

Decent, but not great, cash flow

{kind=link}

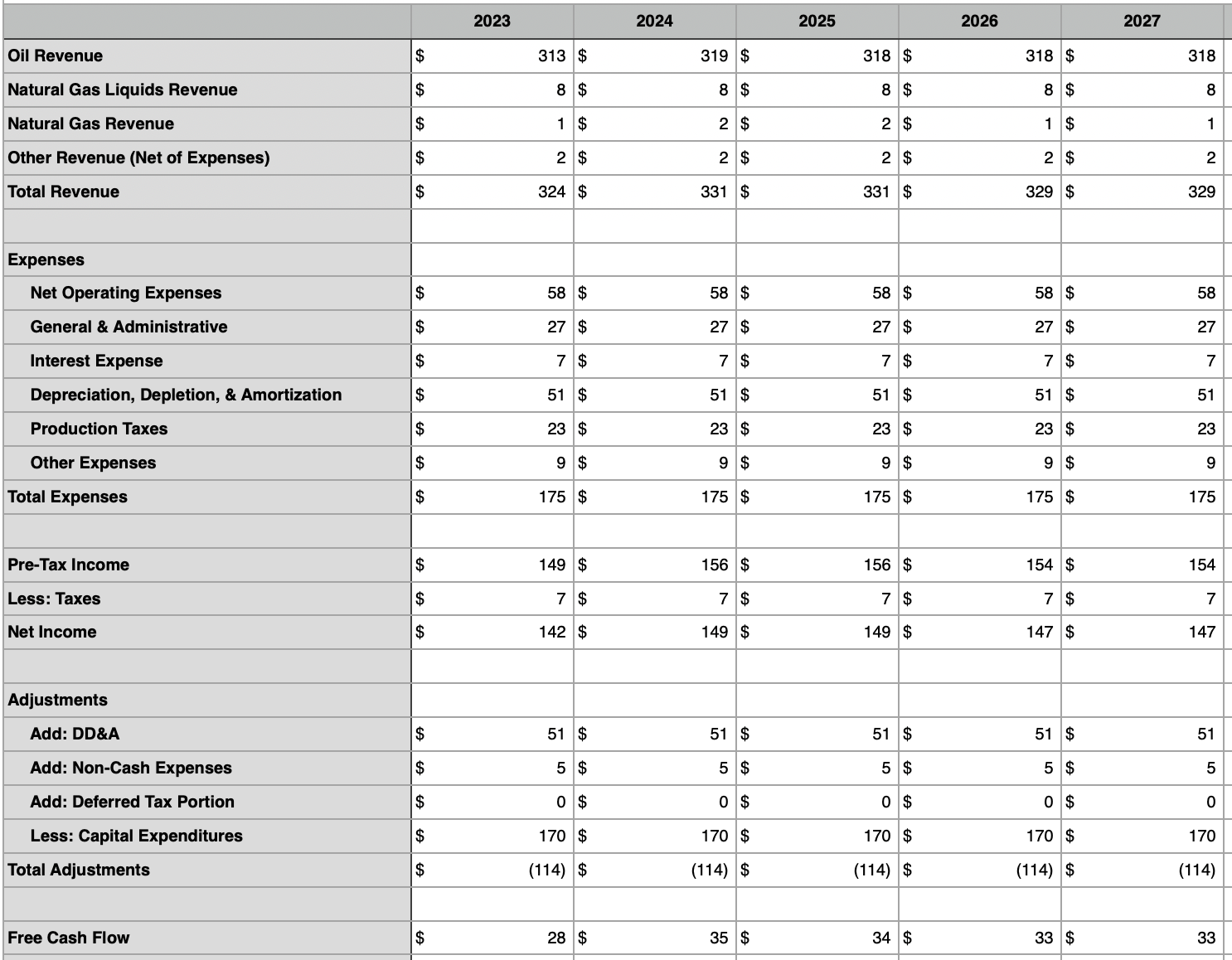

With the assumptions of my model now detailed, I would like to draw your attention to the table above. In it, you can see the revenue through the free cash flow that I calculated for the company for the 2023 through 2027 fiscal years. This is for the conservative scenario only. If all goes according to what my model suggests, the company should generate free cash flow of $28 million this year. It should then pop up to $35 million in 2024 before slowly declining over the following two years to hit $33 million per annum in 2026 and beyond. Even though production is not expected to grow during this time, there are certain hedges on the company's books that mature or expire. And that is why we should see some volatility on the bottom line.

{kind=link}

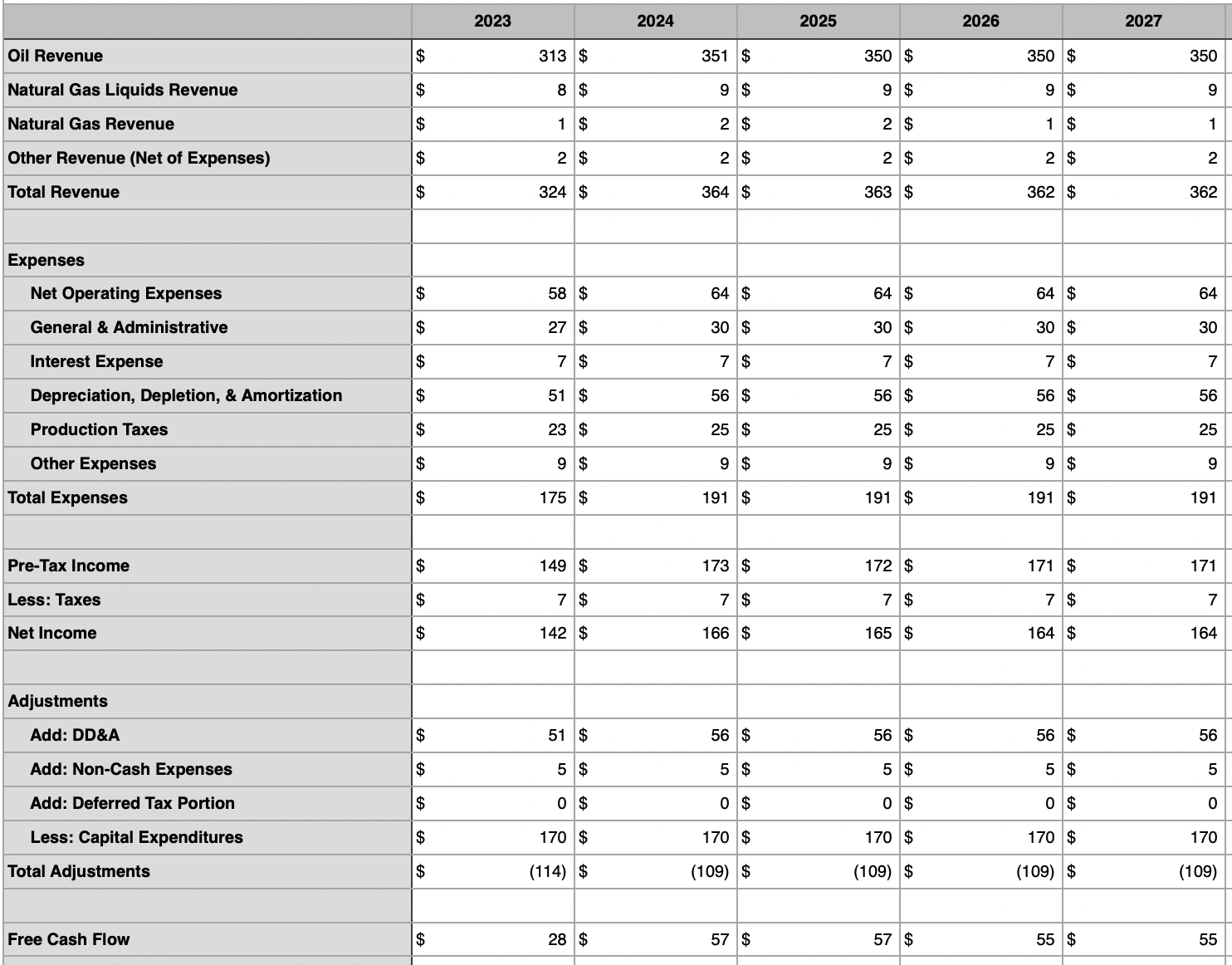

In the next table, shown above, you can see the same analysis repeated. The only difference is that this covers the liberal scenario. In this case, a 10% increase in output should push free cash flow up to $57 million in 2024. By 2026 and beyond, this number should stabilize at $55 million per annum. At the end of the day, free cash flow is the most important metric to pay attention to. But it's not the only metric that is relevant. We should also be paying attention to other profitability metrics like operating cash flow and EBITDA. In the first table below, you can see these calculated next to the conservative scenario for free cash flow. And in the table below that, you can see the same thing but for the liberal scenario. The key takeaway here is that the overall trajectory for these other profitability metrics is basically the same as it is for free cash flow.

{kind=link}

{kind=link}

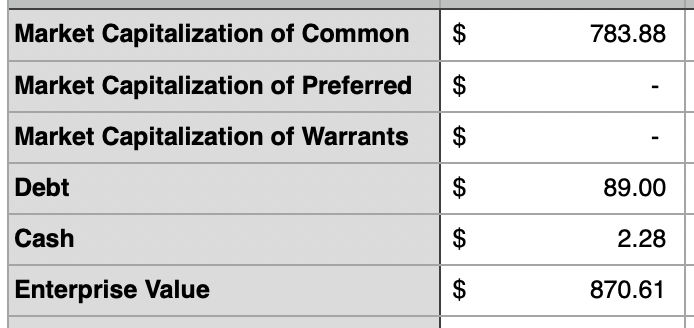

Setting the stage for valuation

{kind=link}

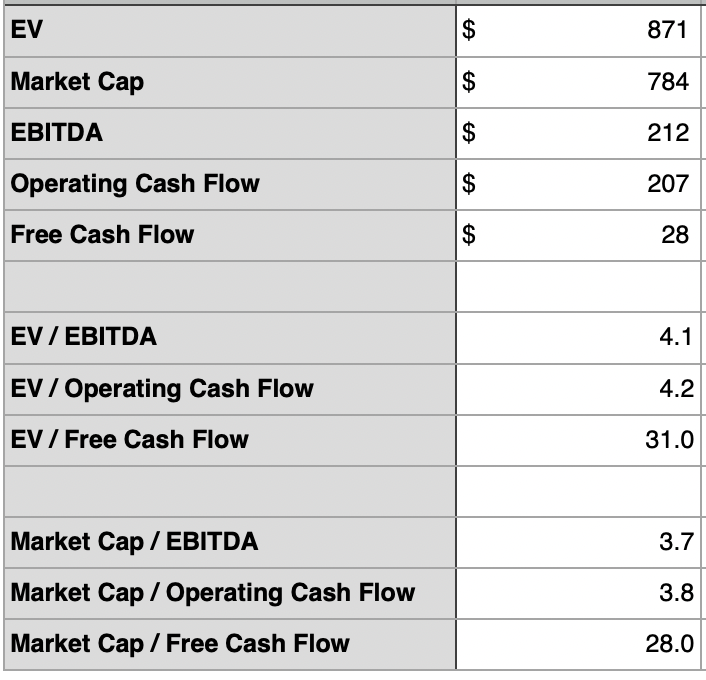

What my model suggests is that, for a company its size, Riley Exploration Permian does not generate that much in the way of excess cash flow. But this doesn't mean that there can't be some upside. To see whether or not this is the case, we need to first understand how to value the company. As I do with other companies in the space, I decided to value the firm by comparing the cash flow metrics that I calculated already to pricing metrics like its market capitalization and its enterprise value. These two metrics can be seen in the table above. In the table below, meanwhile, you can see how shares are priced using the estimates for the 2023 fiscal year. At present, Riley Exploration Permian is trading at an EV to EBITDA multiple of about 4.1 and at a price to operating cash flow multiple of 3.8.

{kind=link}

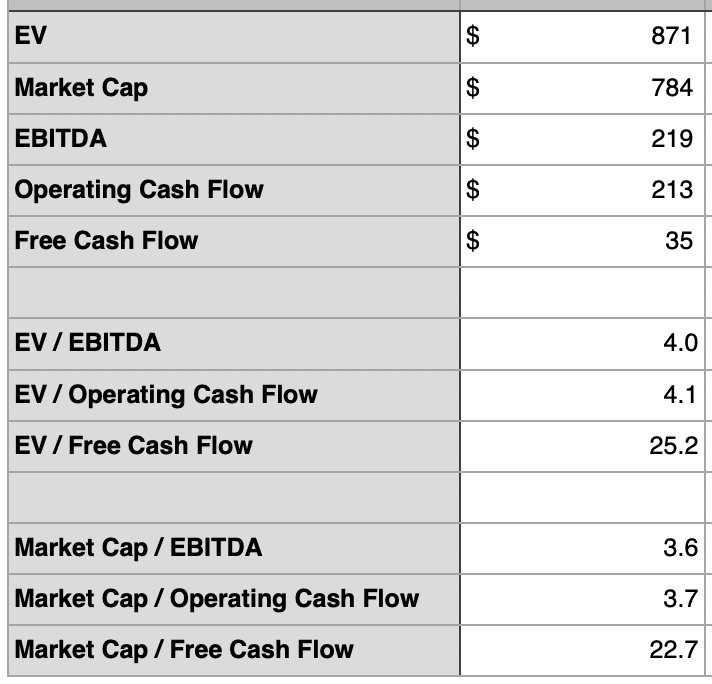

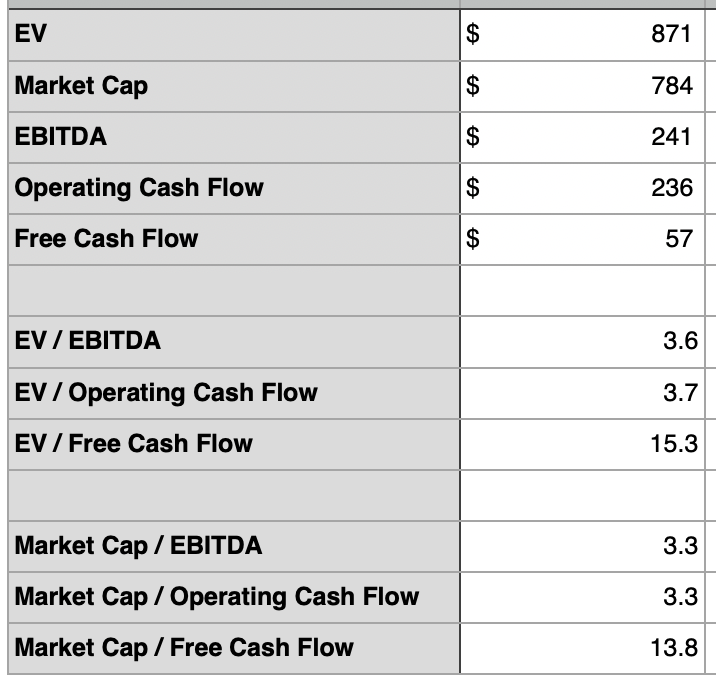

In a healthy environment, these numbers are not pricey whatsoever. But many other firms that I have looked at over the past year or so are trading at or around these levels. This suggests that, for the industry at least, shares might be closer to fairly valued. In the next table below, you can see the same thing repeated for the conservative scenario for 2024. And in the table below that, you can see the same thing but for the liberal scenario for next year. What I would say is that, while shares do get cheaper, they don't get so much cheaper as to deviate significantly from what else I have seen in the space.

{kind=link}

{kind=link}

To some extent, this pricing may very well be warranted. After all, companies that have a low amount of leverage can demand a higher trading multiple than their peers. And low leverage is exactly what Riley Exploration Permian has. As you can see in the table below, the net leverage ratio for the firm should range between a low point of 0.36 and 0.41 this year and next, assuming that management does not borrow more or use cash flow to reduce debt further. Generally speaking, the market doesn't like to see a net leverage ratio much in excess of 2. So to see this come in substantially lower is refreshing.

{kind=link}

Shares have some upside

{kind=link}

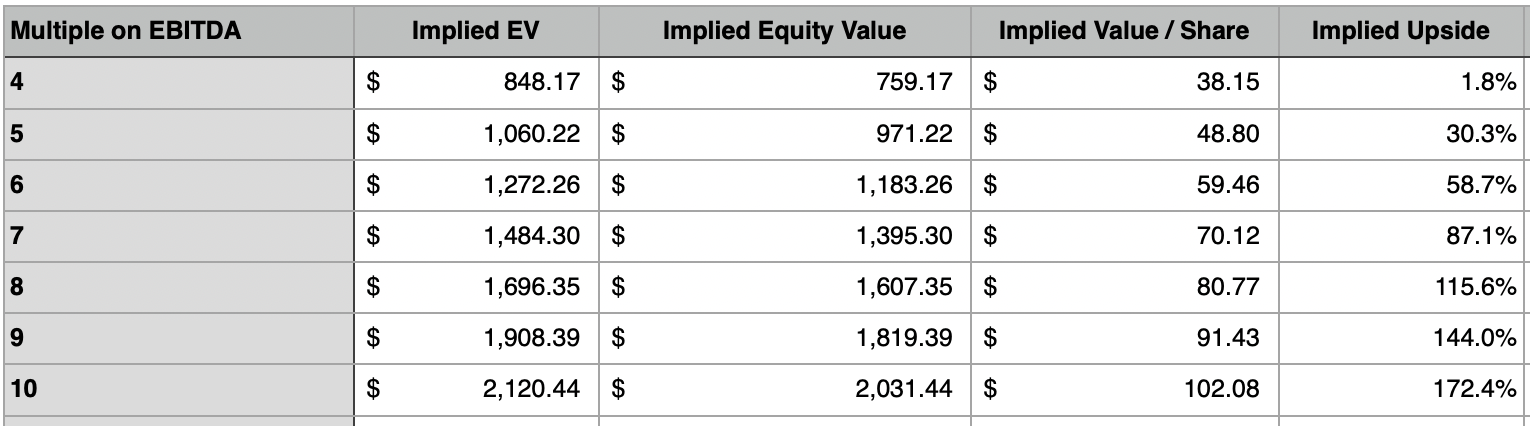

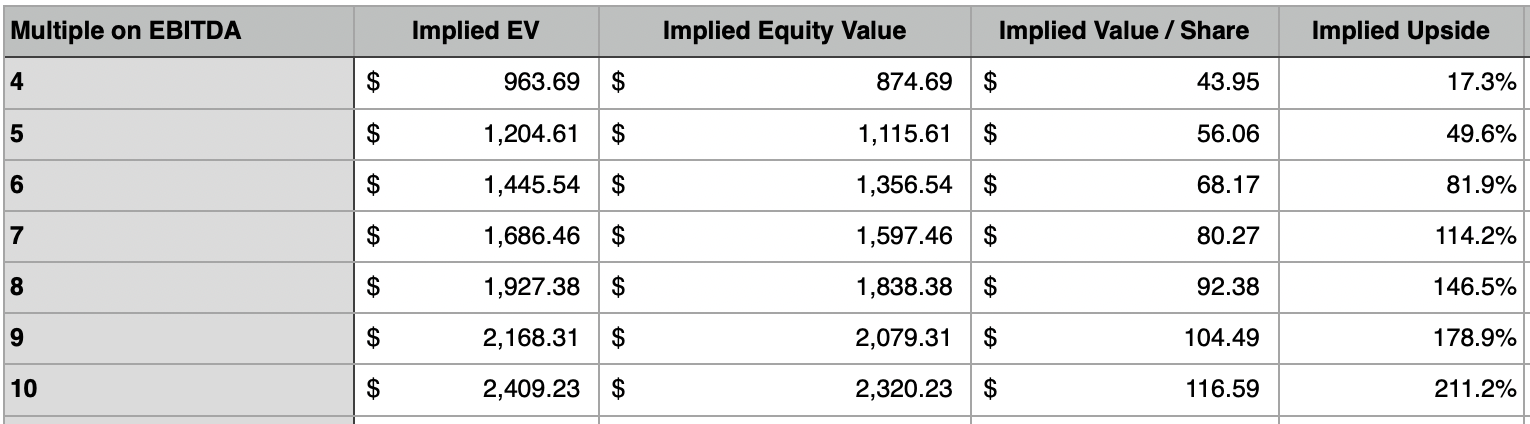

Now that we know how shares of Riley Exploration Permian are priced, we need to see what kind of potential, if any, the company has moving forward from an appreciation perspective. In the first table above, you can see a hypothetical range for the EV to EBITDA multiple. This ranges from a low of 4 to a high of 10. At each point, you can see what kind of share upside and share price Riley Exploration Permian should warrant if it were to trade at said point. As an example, if the company were to deserve an EV to EBITDA multiple of 6, then you would expect upside of 58.7%. If a more appropriate multiple would be 10, then upside potential would be 172.4%. As a note, this only covers the 2023 fiscal year analysis.

{kind=link}

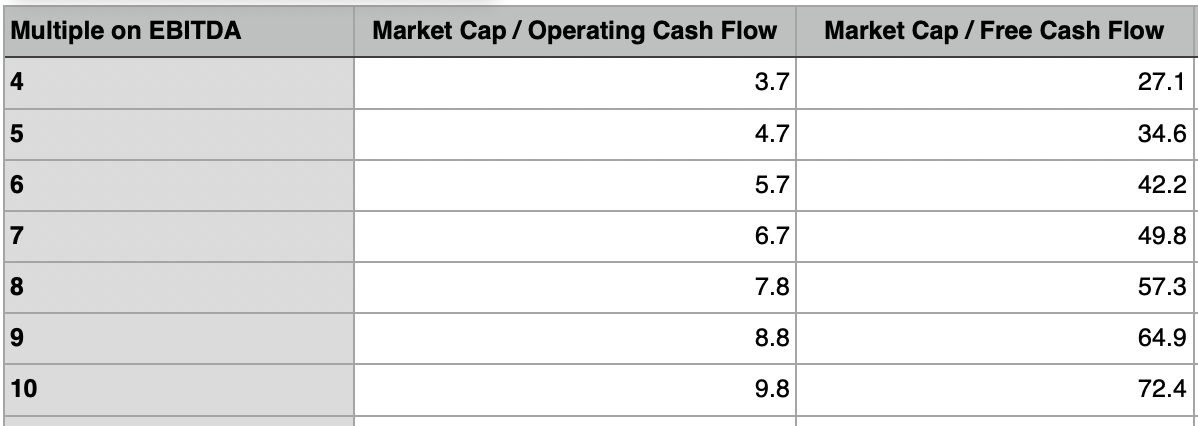

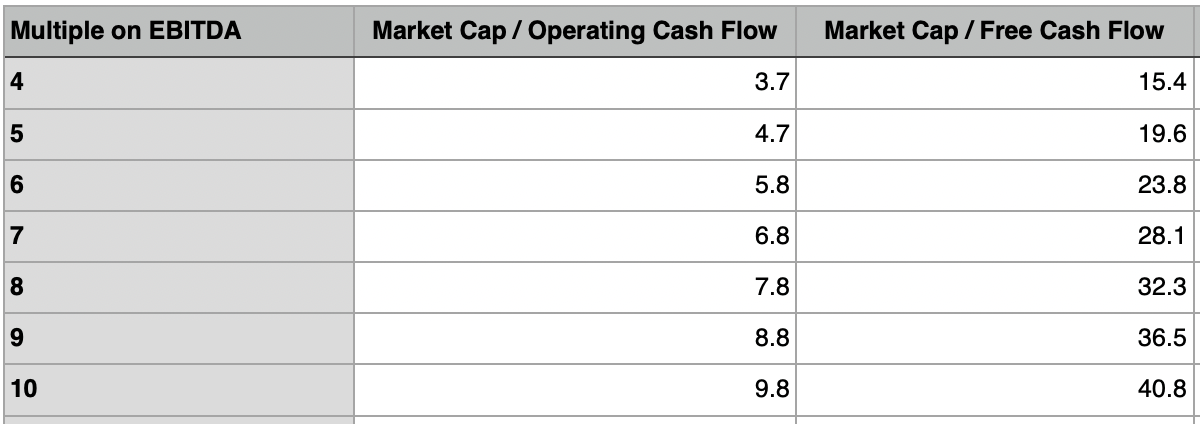

In the next table, shown above, you can see the same EV to EBITDA multiple range. The only difference is that this compares that multiple to the implied price to operating cash flow multiple and the implied price to free cash flow of multiple of the business. The most important thing is that, as the EV to EBITDA multiple approaches 10, so too should the price to operating cash flow multiple approach it. The fact that this does is positive and indicates that a value trap scenario is unlikely.

{kind=link}

{kind=link}

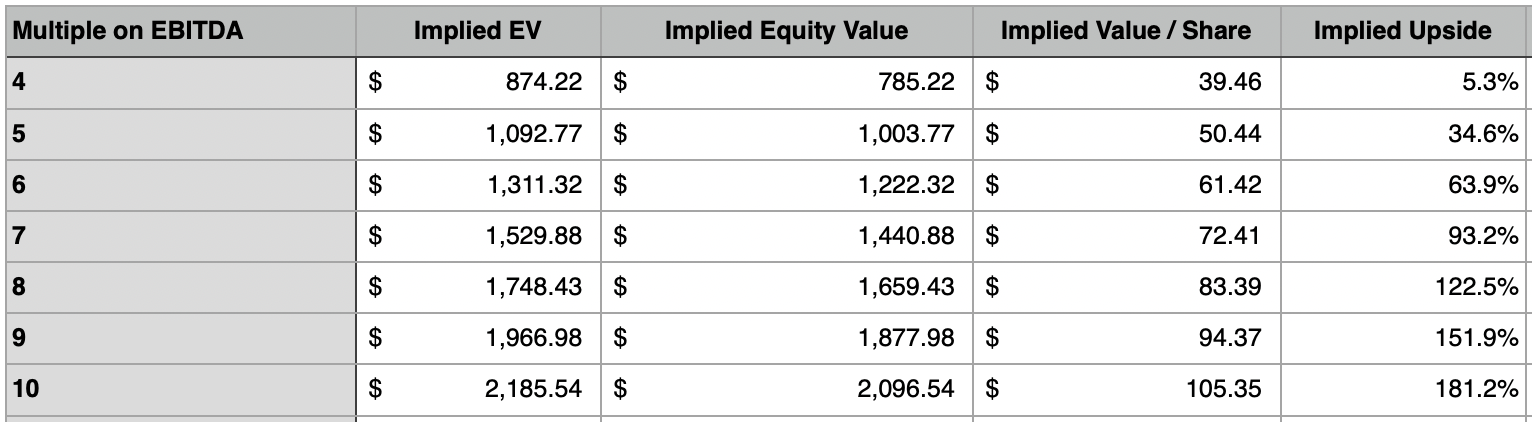

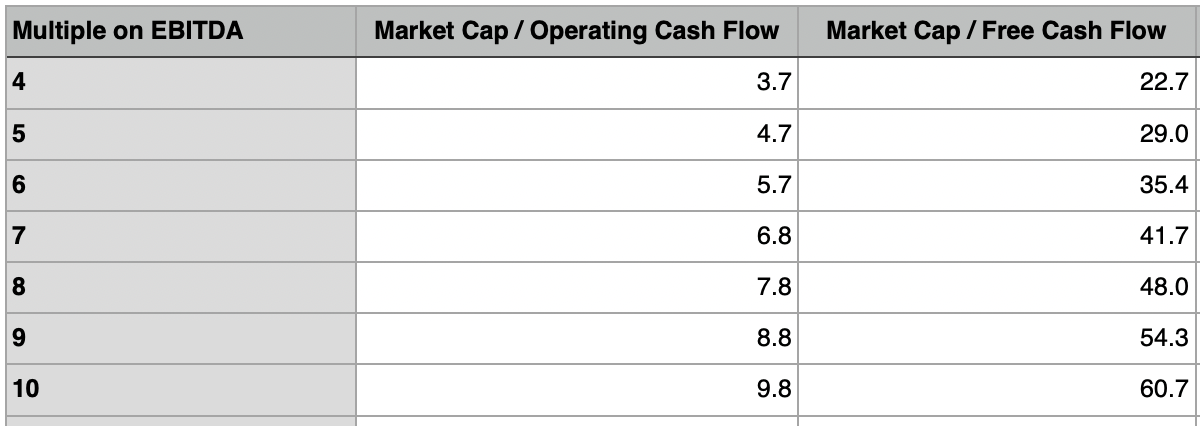

In the two tables above, you can see the same analysis repeated for the conservative scenario for the 2024 fiscal year. And in the two tables below, you can see the same thing but for the liberal scenario for next year. Obviously, the difference in hedges and the prospect of higher production under the liberal scenario for next year, or indicates more attractive upside than the data for the 2023 fiscal year suggests. This is great upside in and of itself, especially considering how low leverage actually is. But it's not as attractive as some of the more heavily leveraged players that I have seen.

{kind=link}

{kind=link}

Takeaway

All things considered, it looks to me as though Riley Exploration Permian is an interesting prospect that investors should pay attention to if they are bullish on oil and gas and want a prospect that may not have the most upside potential but that does offer a degree of stability that many other firms do not currently offer. This is not the kind of opportunity that will make you rich. But it could go on to generate some decent returns over time.

For further details see:

Riley Exploration Permian: A Good Trade-Off For Those Desiring Safety