REPX - Riley Exploration Permian Inc.: Strong Dividend Play In A Resilient Sector

2024-01-07 00:29:22 ET

Summary

- Small caps, particularly Riley Exploration Permian Inc, are a promising investment in 2024 due to the US's high oil production levels.

- REPX has a low stock price and generates consistent free cash flow, making it an attractive dividend play.

- REPX focuses on the San Andres Formation in the Permian Basin, a region known for its favorable production costs and infrastructure, indicating strong growth potential.

Investment Rundown

In 2024 I think one of the best parts in the market to look at is small caps. A theme tends to be that sectors or parts of the market that were losers in one year are somewhat likely to be winners the next. One such company I am looking at right now is Riley Exploration Permian, Inc. ( REPX ). Following the output cuts that OPEC announced earlier in 2023 the US has seen rapid increases in its production levels to help offset some of this and for oil prices to remain stable. In 2023 the US managed to break the oil output record and produced 13.3 million barrels per day. This number is higher than any other country in the world, in the history of oil production. I think this quite clearly shows our continued demand for the material despite the vast investments going into renewables and green energy. Oil is here to stay for a lot longer and benefiting from that I find very appealing.

The stock price for REPX has been on a steady decline for the last several months and trades at a low p/e of 4.8 right now. One of the appealing factors with REPX is the consistent FCF they are generating. In the last quarter , the company generated more in FCF than they are paying out in dividends during a whole year, which is $27 million. The dividend has been consistently raised as well and I think apart from the large upside potential, REPX also has a lot of qualities as a business that makes it a strong dividend play too. I am initiating coverage on the company and my rating will be a buy.

Company Segments

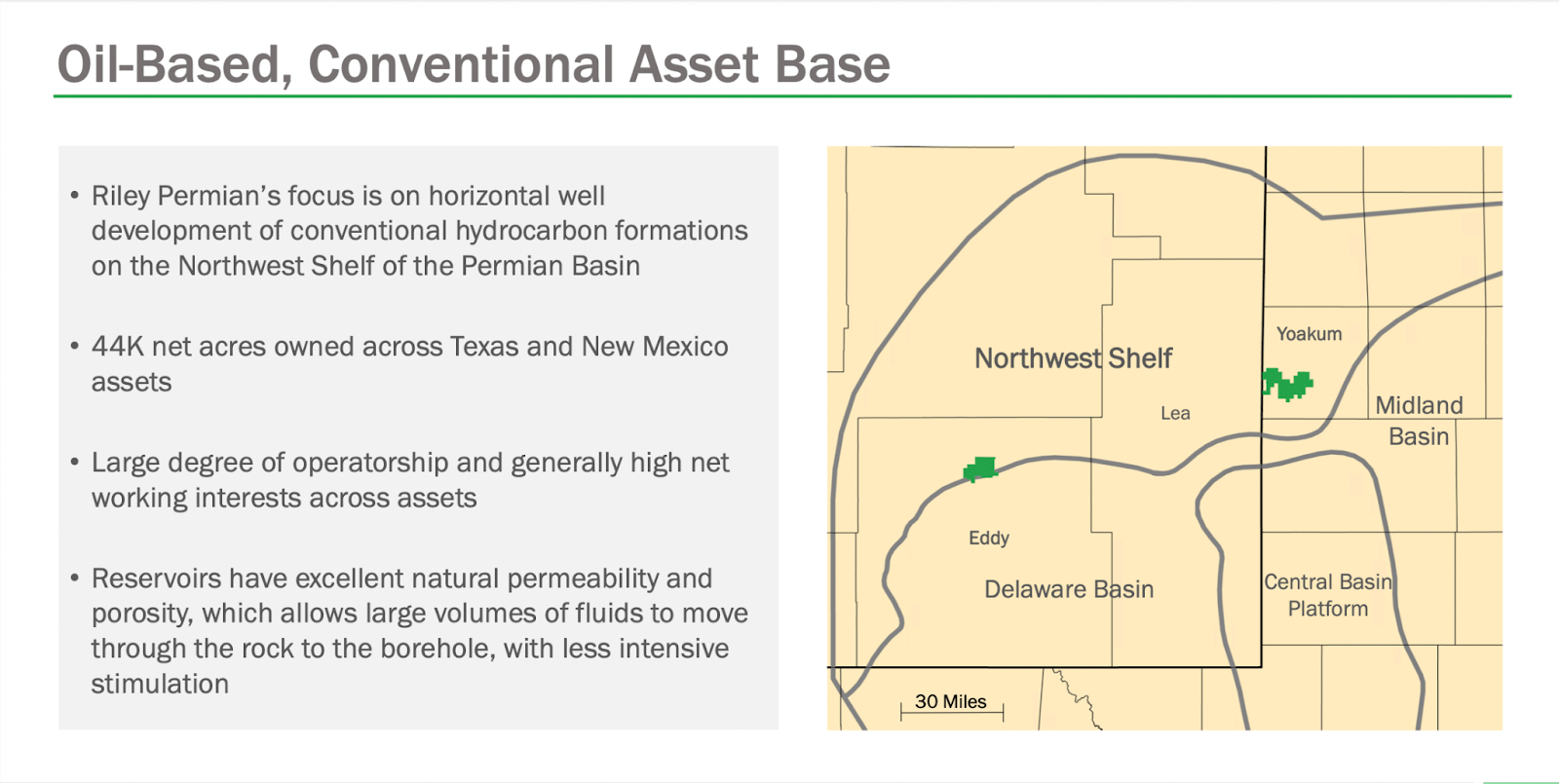

REPX is an independent player in the oil and natural gas sector, actively involved in the comprehensive lifecycle of energy resources. The company's operations encompass the strategic acquisition, exploration, development, and production of oil, natural gas, and natural gas liquids across key regions in Texas and New Mexico.

A central area of focus for REPX is the San Andres Formation, a significant geological feature located on the Central Basin Platform and Northwest Shelf. This shelf margin deposit presents a valuable exploration opportunity for the company, and its concentrated efforts in this area underscore its commitment to maximizing resource potential and operational efficiency.

Asset Base (Investor Presentation)

{kind=link}

The Permian Basin , situated in West Texas and southeastern New Mexico, stands out as a highly productive and significant region for oil and natural gas extraction. Its appeal in the energy sector is attributed to various factors contributing to its strategic importance. Economically, the Permian Basin is favorable for oil exploration and development. Its relatively low production costs and proximity to well-established infrastructure, including pipelines and refineries, contribute to its attractiveness for oil and gas operators.

Growth Plan (Investor Presentation)

{kind=link}

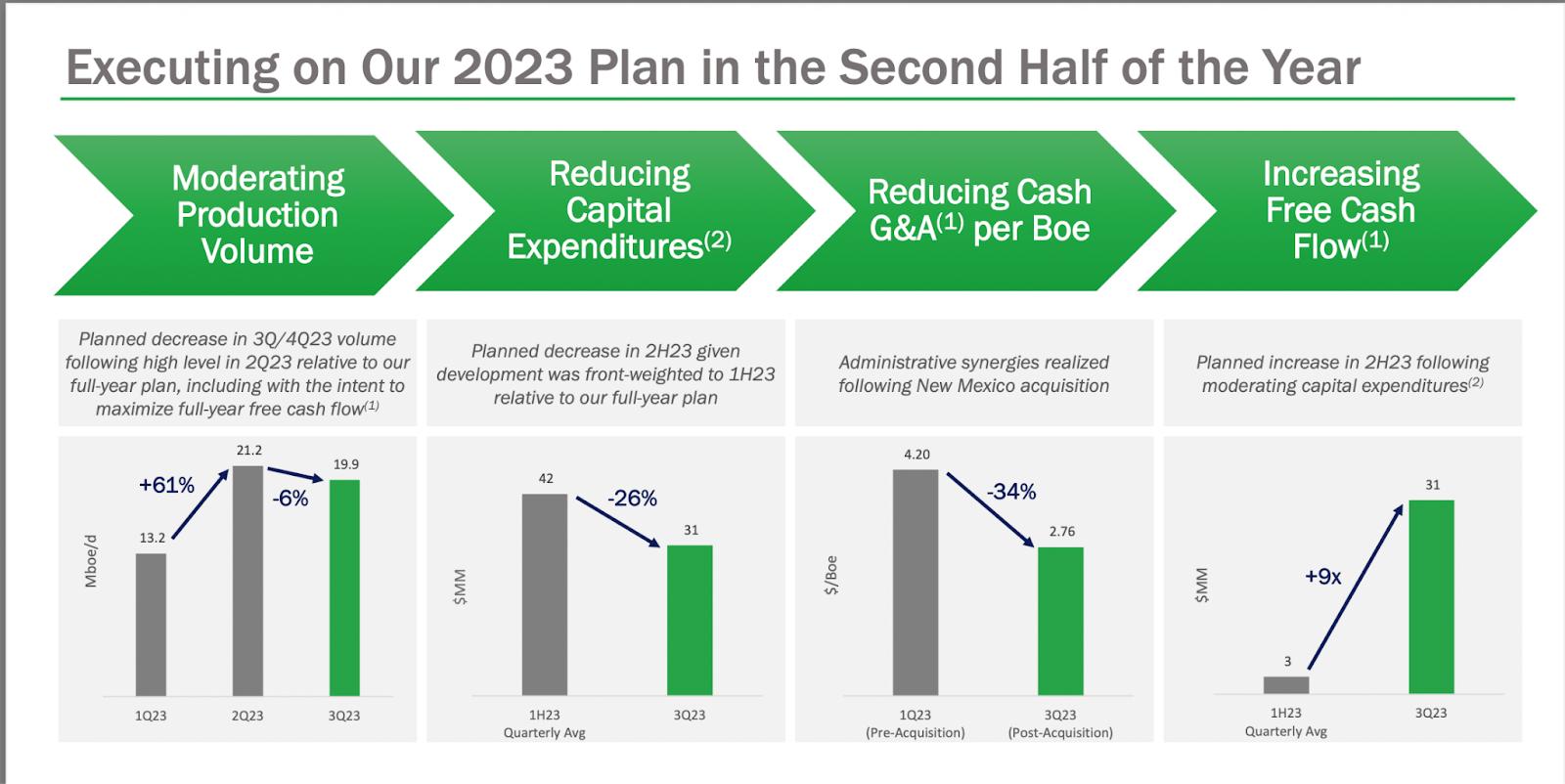

With the US increasing production, the same has been visible with REPX as well, which had production levels grow by 49% YoY to 14.0 MBbls per day. It was a slight decrease perhaps to the second quarter of 2023, but seeing this sort of momentum I think speaks very well about the growth prospects that still exist in the Permian Basin, both for REPX and also other companies as well. Going forward REPX is seemingly continuing to focus on increasing FCF generation having more moderate production levels too. I think that if REPX remains at these production levels the dividend will be easily payable and with the discount, the company trades at, which I think comes from the low valuation and market share still means there is plenty of value to be had here over the long-term.

Earnings Highlights

Income Statement (Earnings Report)

{kind=link}

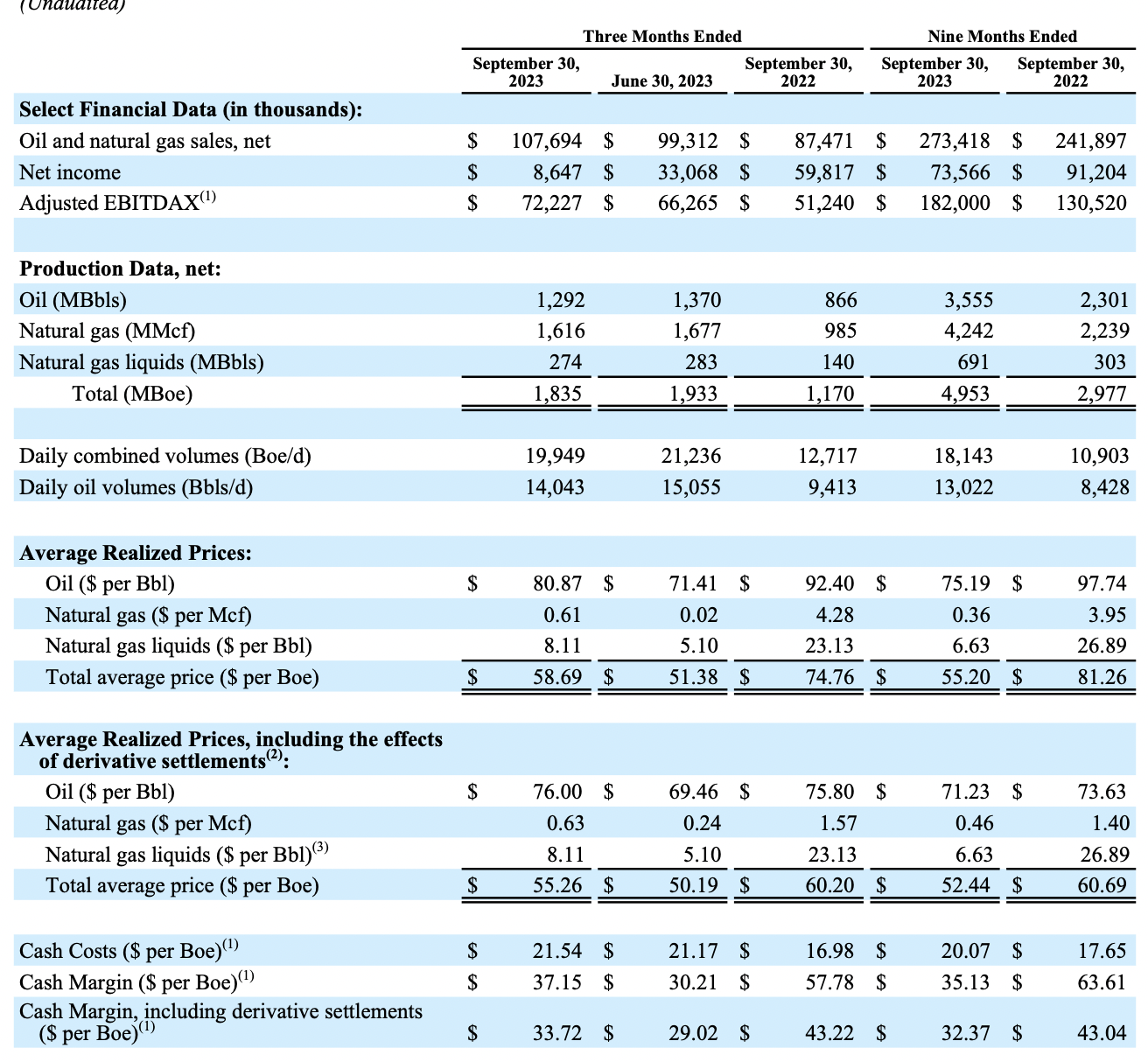

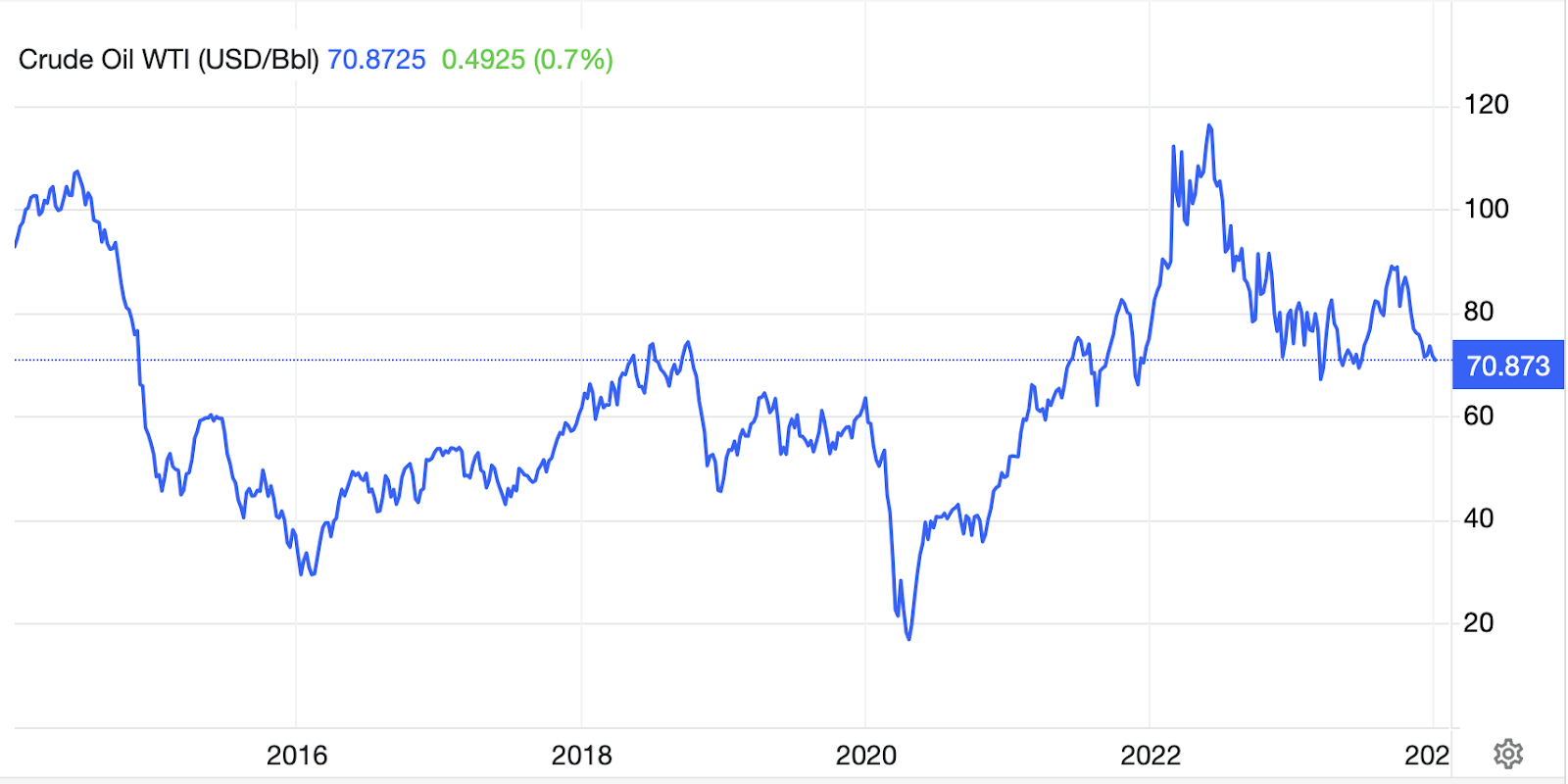

Taking a look at the last earnings report from the company released on November 11, some things stand out to me. The company has been able to very well raise the production levels YoY which I have mentioned before. But what has perhaps been the greatest gain is the increased FCF growth, last quarter reaching $31 million in total. Oil prices have fallen YoY to around $80 per barrel, but the increase in production levels helped offset a decent chunk of this and I think this proves the quality of REPX and how it can fare very well in a tough macro climate anyway. Going into the Q4 report I think we will continue to see lower oil prices but for the FCF that REPX generated to remain quite similar to Q3, around $26 - $30 million.

Balance Sheet (Earnings Report)

{kind=link}

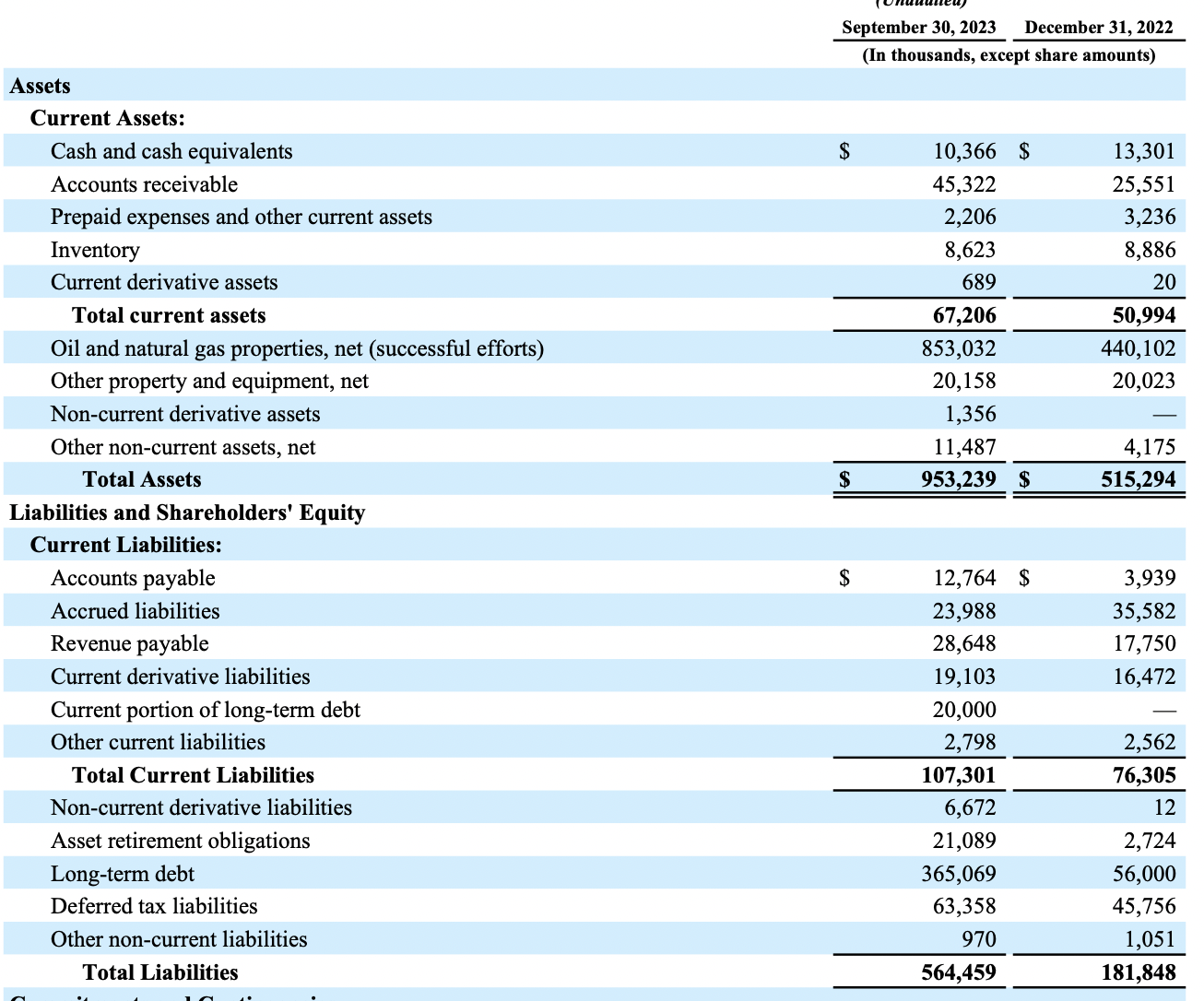

With this increased level of FCF for the business they have managed to put it to good use reducing the total debts by $10 million in the last quarter. Now, we still see the long-term debts at $365 million right now, which is a significant increase from the $56 million in late 2022. But I think the results of taking on more debt have been largely positive, seeing as production levels have reached record highs and the dividend is now well supported too. The EBITDA/debt ratio is just at 1.6 right now, which is far below the 3 I tend to have as a threshold for investments.

{kind=link}

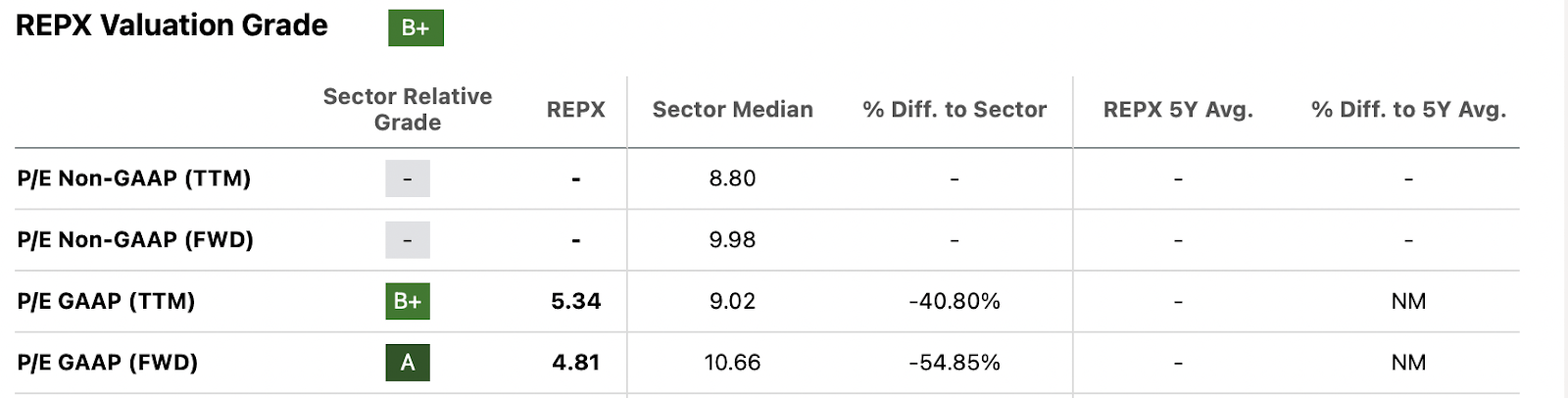

Valuation-wise the company is quite far below the rest of the sector indicating an over 50% discount based on p/e GAAP FWD. I think that a more fair multiple here would be around 7.5 at least, leaving a near 25% upside. I argue that this multiple is fair given the growth that REPX has managed to achieve in recent years and how it hasn't meant they are overly leveraged either. With a 7.5 p/e multiple we land at a price target of $48 in 2024 should REPX manage to grow 15% YoY in terms of EPS from 2023 and reach $6.4 EPS. I don’t see this as something impossible and will therefore be rating REPX a buy here.

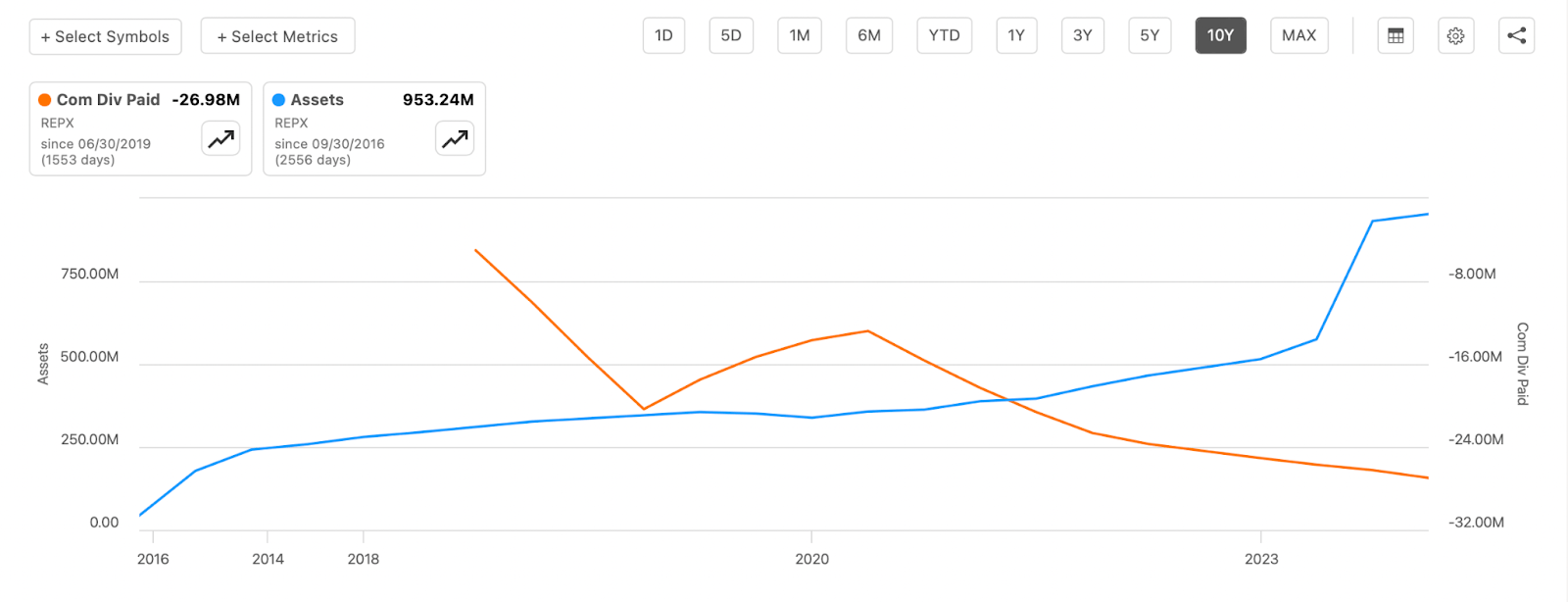

Going up against a peer like Obsidian Energy Ltd. ( OBE ) I think that REPX looks like the better option right now. The company has a dividend unlike OBE and with the additional assets it has acquired through expansion, I think growth is also likely to be higher for REPX. Over the past decade, the assets for OBE have actually declined by nearly 17% annually which is not the type of trend I want to see. With REPX the assets have instead expanded very quickly, being at $178 million in 2017 and now nearing $1 billion . Growth initiatives seem stronger with REPX and with the dividend and shareholder value, I think it represents the better option right now.

Risks

REPX currently faces a notable risk tied to the volatility of oil prices. The company's financial performance relies on favorable oil prices to generate robust FCF and distribute high dividends to its shareholders. Any disruptions in production, whether due to weather-related incidents or operational issues such as depreciation and insufficient maintenance, could potentially lead to a decline in earnings.

{kind=link}

It's worth noting that oil prices have experienced a significant decrease from their peak levels. Despite this decline, REPX has demonstrated resilience by maintaining strong FCF generation. This suggests that the company has navigated challenges effectively and can sustain its current dividend payout while potentially considering increases. I still see oil price volatility as a risk to REPX, but perhaps less than that of other countries given the strong resilience it has showcased in terms of continuing to increase FCF generation. A factor for this I think has to do with the increased production capabilities in the last few quarters too.

{kind=link}

However, investors must remain vigilant about factors influencing the oil market, as price volatility can impact REPX's revenue and profitability. External factors such as geopolitical events, global economic conditions, and shifts in demand for oil can introduce uncertainties. REPX has in the last few years been able to consistently increase its asset base through expansion in the Permian Basin and a result of this has been a rising dividend payout for shareholders, a trend I think will continue. But should there be stagnation here or poor expansion results, then the market may see REPX better trading at a lower valuation, causing some short-term pain in the stock price for investors.

Final Words

I think that the oil industry continues to be very appealing to make investments in and one of the better options right now seems to be REPX. The company has managed to grow its FCF generation very well over the past few years and it's now capable of covering the full-year dividend payout in a single quarter if oil prices remain at these levels, which I think they will as a floor seems to have been found. Investors seeking a small cap and one that has a strong dividend payout yield should consider REPX right now. I am rating the company a buy at these price levels, and have a PT of $48 for next year.

For further details see:

Riley Exploration Permian, Inc.: Strong Dividend Play In A Resilient Sector