FLYW - Riskified: Long Runway For Growth

2023-04-18 07:02:08 ET

Summary

- Riskified Ltd. is rapidly growing and focused on global eCommerce, benefiting from the trend toward digital commerce.

- The company's ability to collect and analyze large amounts of data positions it as a leader in risk modelling among third-party risk providers.

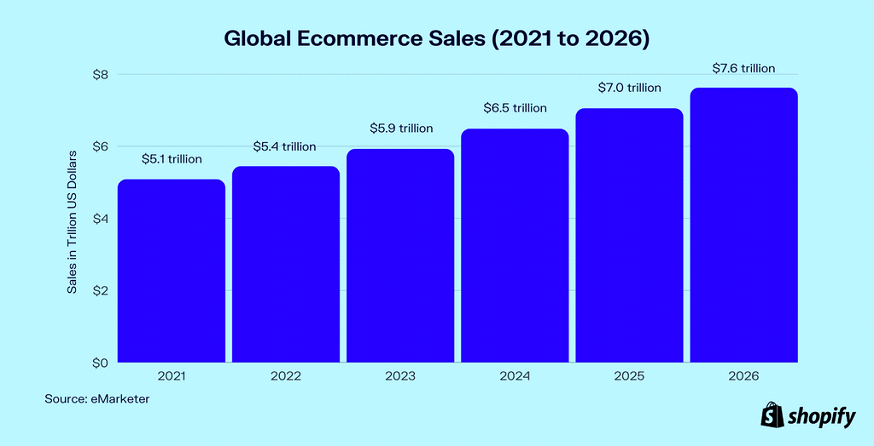

- RSKD has a vast TAM, with global eCommerce sales expected to grow at a CAGR of around 8.3% to $7.6 trillion by 2026.

- My end-of-year price target of $6.9 is based on a forward EV/Sales assumption of 2x, which is in line with the company's historical multiple and a Dec 2024 revenue estimate of $356 million.

Thesis

Riskified Ltd. ( RSKD ) is a rapidly growing company focused on global eCommerce, benefiting from the trend toward digital commerce. The company has a vast Total Addressable Market ((TAM)) and has a compelling value proposition offering several benefits to merchants helping to improve authorizations, reduce chargebacks, and lower operating expenses associated with managing risk. With coverage in approximately 120 countries worldwide, RSKD has a long runway for growth, and its ability to collect and analyze large amounts of data positions it as a leader in risk modeling among third-party risk providers. My end-of-year price target of $6.9 is based on a forward EV/Sales assumption of 2x, which is in line with the company's historical multiple and a Dec. 2024 revenue estimate of $356 million.

Large TAM with strong secular tailwinds from digital commerce

RSKD is focused on global eCommerce, which represents a large total addressable market ((TAM)). According to eMarketer , global eCommerce sales reached $5.1 trillion in 2021 and is expected to grow at a CAGR of around 8.3% to $7.6 trillion by 2026. RSKD is well-positioned to benefit from this growth as it leverages strong digital-commerce-related tailwinds to grow at a faster rate than the market. The trend of eCommerce growth has accelerated in recent years, with an annual growth rate of over 20%, a trend that was likely driven by the global pandemic. Although eMarketer predicts that global eCommerce growth will decelerate from post-pandemic levels, it will still grow much faster than broader retail sales, providing a solid secular tailwind for RSKD's rapid growth.

{kind=link}

Currently, RSKD's business mostly comprises U.S.-based merchants, with a small market share of total eCommerce volume outside the U.S. In Europe, Latin America, and Asia Pacific, the company's share of total eCommerce volume is around 1%. This small share of the global eCommerce volumes provides a long runway for RSKD's growth as the company expands its presence and captures a larger share of the market.

Compelling Merchant Value Proposition

RSKD's Chargeback Guarantee product provides a compelling value proposition to merchants by helping them improve authorizations, reduce chargebacks, and lower operating expenses associated with managing risk. This is proven by the company's annual cohort growth of billings. RSKD often starts with a trial of the solution and then expands the relationship once the merchant sees the benefits of increased conversion and lower costs related to fraud and chargebacks. RSKD's offerings also enable merchants to expand into new geographies where their in-house risk models may not be effective, with coverage in approximately 120 countries worldwide. In 2020, around 36% of the company's volume was cross-border.

{kind=link}

Best-in-class risk model and Impressive List of Customers

RSKD sets itself apart from other risk-scoring companies by collecting a large amount of data from its customers to make authorization decisions. This data collection allows RSKD to create more powerful predictive models, resulting in more accurate transaction decisions for its core product, the Chargeback Guarantee. As of December 2021, the company's models have been trained using data from over 1 billion full-lifecycle eCommerce transactions, 400 million unique consumers, 1 million chargeback transactions, and approximately 190 countries. The scale and geographic and vertical diversity of RSKD's business result in best-in-class risk modelling among third-party risk providers.

RSKD has an impressive roster of enterprise merchants as customers, including three of the top ten internet merchants by GMV. The company's customer base is diverse, covering sub-industries such as fashion, big-box retail, travel, electronics, marketplaces, and home/B2B. Although the majority of revenues come from North America, the largest industry concentration is in fashion and luxury goods.

While the company's total volume in 2021 was around $89 billion. Customer concentration among the top three merchants is relatively high, accounting for 36% of total revenues, with Macy's being the largest client representing an estimated 18% of revenues. In summary, RSKD's ability to collect and analyze large amounts of data from its customers, combined with its impressive customer base and diverse sub-industries, positions the company as a leader in risk modelling among third-party risk providers.

Financial Outlook and Valuation

The large TAM and growth opportunity ahead of RSKD will help the company to ramp significant ramp in business investment to expand market penetration rates in my view. While I am optimistic on the growth trajectory of RSKD, it is important for investors to be aware that the company does not expect to return to achieve profitability in the near term. As the majority of RSKD's revenues come from clients in North America, I believe that the company plans to invest strategically in geographic expansion to build capabilities and scale, particularly in Latin America and Asia Pacific.

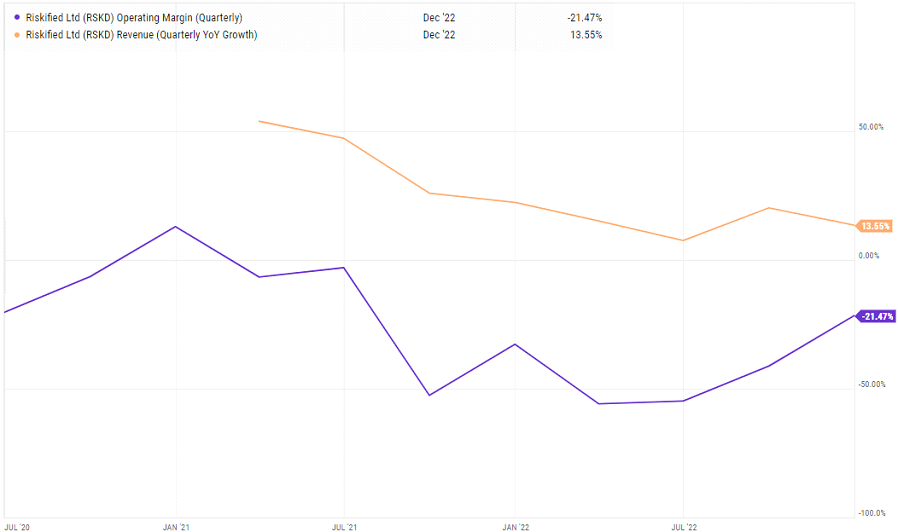

RSKD rev growth and margins (Ycharts)

{kind=link}

Valuation

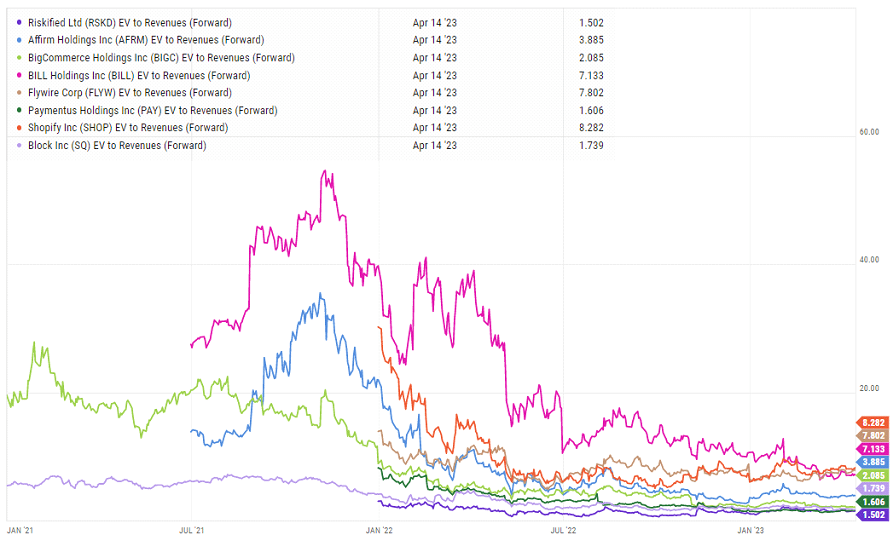

I believe that a relevant peer group for RSKD is a basket of high-growth digital commerce enablers, including companies like Adyen N.V. ( OTCPK:ADYEY ), Affirm Holdings, Inc. ( AFRM ), BigCommerce Holdings, Inc. ( BIGC ), BILL Holdings, Inc. ( BILL ), Flywire Corporation ( FLYW ), Paymentus Holdings, Inc. ( PAY ), Shopify Inc. ( SHOP ), and Block, Inc. ( SQ ). Since a lot of the companies in the sector are not yet profitable, I am using EV/Sales valuation multiple to value the company. When comparing EV/Revenue, the average forward EV/sales for the sector is around 2.7x.

My end-of-year price target of $6.9 is based on a forward EV/Sales assumption of 2x, which is in line with the company's historical multiple and a Dec 2024 revenue estimate of $356 million. Moreover, I believe that RSKD's future growth prospects and large TAM justify my price target. While the company's top-line growth profile may be slower than its peers, I believe that its strong growth potential, solid value proposition, and strategic investments make it an attractive investment opportunity for those interested in the digital commerce enabler space.

RSKD valuation metric vs Peers (Ycharts)

{kind=link}

Risks

There are several risks and considerations that should be taken into account for this business. Firstly, there is a possibility of increased competition from other providers of risk management, payment facilitators, and merchant acquirers, which could result in a more intense competitive environment. Secondly, the sales cycles may be lengthy, the data requirements may be demanding, and technology integrations may be deep, which could hinder growth. Thirdly, the second Payment Services Directive (PSD2) in the EU could prove to be a bigger challenge than expected, or new regulations could emerge.

Final Thoughts

I remain bullish on RSKD for several reasons. Firstly, the company is experiencing rapid growth due to the increasing trend of digital commerce and has a large TAM. Moreover, the company has highly skilled data capture and software engineering talent to create a best-in-class risk model. Lastly, RSKD has an impressive customer base across various industries and regions. My end-of-year price target of $6.9 is based on a forward EV/Sales assumption of 2x, which is in-line with the company's historical multiple and a Dec. 2024 revenue estimate of $356 million.

For further details see:

Riskified: Long Runway For Growth