CA - Ritchie Bros. Auctioneers: A Financial Performance And Growth Analysis

2023-05-03 03:06:20 ET

Summary

- Ritchie Bros. Auctioneers has shown impressive growth in revenue and free cash flow, and maintained a solid ROE over the past decade.

- The company's acquisition of Insurance Auto Auctions is a significant strategic move, enabling RBA to tap into IAA's expertise in the salvaged vehicle market, a segment with strong growth prospects.

- According to the DCF analysis, RBA seems to be slightly overvalued, but when compared to its peers using various popular valuation ratios, there appears to be significant value in RBA.

Opening

Ritchie Bros. Auctioneers Incorporated ( RBA ) is a leading auctioneer of industrial equipment and other assets worldwide. The company's unique business model, which connects buyers and sellers in a transparent and efficient marketplace, has successfully attracted a wide range of customers, including small businesses, large corporations, and government agencies.

In this article, we will provide an in-depth analysis of financial performance and its prospects for future growth. We will examine the company's revenue and profitability trends, free cash flow generation, and balance sheet strength. Additionally, we will estimate RBA's intrinsic value using various valuation techniques to provide investors with insights into whether the company is a good investment opportunity in today's market.

Track Record

Over the past decade, RBA has consistently grown its revenue and free cash flow and maintained a solid return on equity (ROE). Let's look closer at the company's financial performance and potential as an investment opportunity.

Revenue Growth: RBA has shown impressive growth in revenue over the past ten years, with only one year of decline in revenue. In the past decade, RBA has grown its revenue from $467 million to $1.7 billion last year. This is a phenomenal growth rate, and it demonstrates the company's ability to capture market share and expand its operations.

Data by Stock Analysis

Free Cash Flow: Another critical metric to consider is the company's free cash flow, which measures the amount of cash generated by the business that is available to be used for investment, acquisitions, or shareholder payouts. Over the past ten years, RBA has grown its free cash flow from $109 million to $556 million. This represents a healthy growth rate and shows the company is generating substantial cash flows from its operations.

Data by Stock Analysis

Return on Equity: ROE is a key metric that investors use to evaluate a company's performance. RBA has had an average ROE of 16.1% over the past ten years, which is impressive considering the company's large size and established market position. A high ROE suggests that the company effectively uses its resources to generate profits for its shareholders.

Balance Sheet: RBA's debt-to-equity ratio of 0.47 indicates that the company has a manageable amount of debt and that its balance sheet is in good health. However, the current ratio of 1.21 is a little low, suggesting that the company may face liquidity issues in the short term.

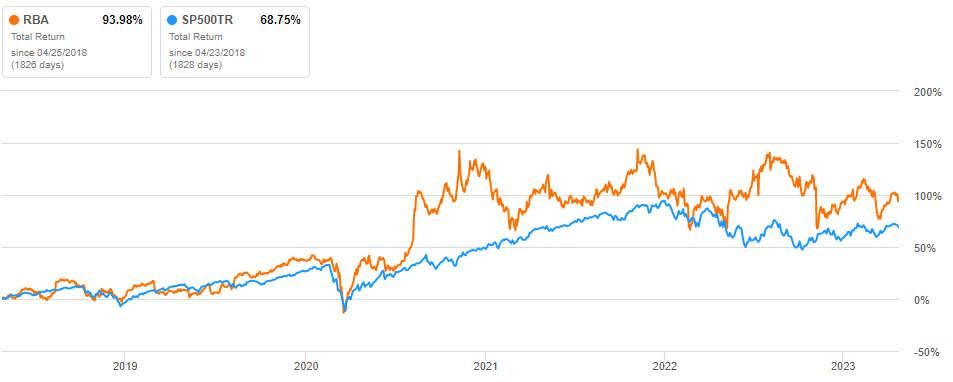

Total Return: Over the past five years, RBA's total return has outpaced the total return of the S&P 500, delivering a total return of 93.98% compared to the S&P 500's return of 68.75% over the same period. This is an encouraging sign for investors considering investing in the company.

{kind=link}

In conclusion, RBA has shown consistent revenue growth and free cash flow and maintained a solid ROE over the past ten years. Additionally, the company has a manageable amount of debt and has outperformed the S&P 500 in total return over the past five years. While the company's current ratio is slightly low, its strong financial performance and market position make it a potential investment opportunity.

Forecast

RBA had an exceptional year last year , breaking several records. One of the most impressive record sets was the $6 billion annual gross transactional value (GTV). Additionally, the company's marketplace-E platform also saw over $700 million in transactions, while over $1 billion in volume was funded by Ritchie Bros. Financial Services.

RBA's strong performance was also reflected in its financial results, as adjusted earnings per share rose 24% year-over-year to $2.41. One of the reasons for the company's success in 2022 can be attributed to its track record of innovation. For example, RBA is currently testing an innovative digital check-out experience with self-serve invoices as part of its Ritchie Brothers 2.0 platform.

One of the company's critical moves for long-term future growth was the recent acquisition of Insurance Auto Auctions (IAA), a prominent company in the auto auction industry, selling a wide range of vehicles such as cars, trucks, SUVs, and motorcycles.

The acquisition is a significant strategic move for RBA, as it allows the company to tap into IAA's expertise in the salvaged vehicle market, a segment with strong growth prospects. IAA is a leading player in this market and has shown resilience even during economic downturns, which bodes well for RBA's long-term prospects. RBA's Chief Executive Officer, Ann Fandozzi, emphasized how significant the acquisition is for RBA on the company's most recent earnings call:

The key here is that we are better together and combining the footprints will allow us to create a network of locations that will provide us with the agility to meet all our customers' needs and unlock higher levels of growth and margin expansion. As we recently highlighted, we see a potential to unlock $350 million to $900 million in EBITDA growth opportunities, including our expected $100 million to $120 million or more of clearly identified and achievable cost synergies.

When it comes to what makes excellent mergers and acquisitions, there's no one-size-fits-all answer. However, a good merger or acquisition creates long-term value for the shareholders of both companies, and this deal brings RBA access to new customers, new markets, and precise cost savings. Overall, RBA's future looks bright with its focus on innovation and strategic acquisitions.

Intrinsic Value

We will use a discounted cash flow ((DCF)) analysis to assess RBA's intrinsic value. DCF is a valuation method that estimates an investment's intrinsic value by calculating the present value of its expected future cash flows.

To get started, we'll take the average of RBA's last five years of free cash flows, which amounts to $295 million, as the base year for our projections. Using a five-year average of a company's free cash flow as a starting point for a discounted cash flow calculation provides a more stable and reliable estimate of future cash flows. In addition, this approach smooths out any fluctuations and anomalies in a company's free cash flow over time, allowing for a more accurate projection of future cash flows.

Next, we'll use a growth rate of 7% for the first ten years based on the average analyst estimates of earnings growth. To determine the terminal value, we will employ a more cautious perpetual growth rate of 2.5%. Moreover, we will utilize a discount rate of 10%, which takes into account the long-term return rate of the S&P 500 with dividends reinvested. Based on these inputs, we can calculate the RBA's intrinsic value to be $49.94. This indicates that RBA may be somewhat overvalued, potentially resulting in a 12.81% decline for investors compared to the current market price.

{kind=link}

It is important to keep in mind that the precision of our DCF (Discounted Cash Flow) analysis is reliant on the accuracy of the inputs we use, including the growth rate and discount rate. Although our assessments are sensible, they may be susceptible to alteration due to unforeseen circumstances that could influence the company's performance. Therefore, it is crucial to use multiple valuation techniques to comprehensively understand a stock's intrinsic value, as different methods highlight different factors.

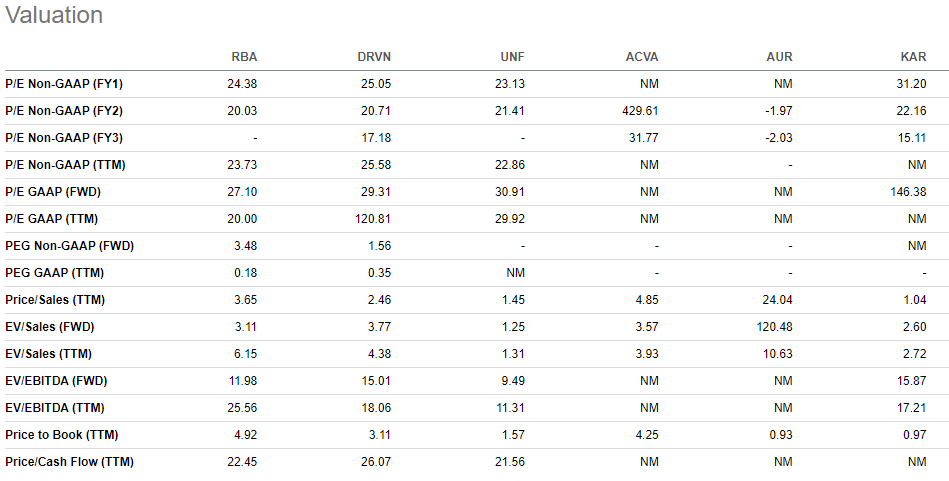

When evaluating a potential investment, I also compare the company's current valuation to its industry competitors to determine if it is priced favorably. I utilize various common valuation ratios, including P/E, P/S, and P/B, to assess the value of an investment. Seeking Alpha's " Peers " page is an excellent resource for finding a range of these popular valuation ratios for a company like RBA and seeing how it compares to its industry peers.

{kind=link}

The lower the value of these valuation ratios above, the more undervalued the company is perceived. By averaging these ratios, we can identify the most undervalued company by identifying the one with the lowest score. According to this analysis, RBA appears to be more undervalued than its industry rivals, with a score of 14.05, the lowest recorded score. The rest of the results are listed below.

1) RBA - 14.05

2) UNF - 14.68

3) DRVN - 20.89

4) AUR - 25.35

5) KAR - 25.53

6) ACVA - 79.66

It's important to note that this comparative analysis has its limitations. Apart from the PEG ratios, the other ratios do not explicitly take into account a company's future growth prospects, which play a vital role in evaluating the company's true value. In addition, there are much missing data points above, which may affect the accuracy of this comparative analysis. As a result, I advise to combine the outcomes of this valuation method with the findings of the DCF analysis.

In conclusion, RBA is overvalued based on the DCF analysis. Still, the company has substantial value when comparing RBA to its peers based on the average of multiple popular valuation ratios. Therefore, I favor the DCF analysis more than the comparative analysis, but ultimately these results indicate that RBA isn't an objectively undervalued investment that investors covet.

Final Word

RBA is a global auctioneer of industrial equipment and other assets, connecting buyers and sellers in a transparent and efficient marketplace. The company has shown impressive growth in revenue and free cash flow and maintained a solid ROE over the past decade, with only one year of decline in revenue.

Additionally, the company has a manageable amount of debt and has outperformed the S&P 500 in total return over the past five years. Although the current ratio is slightly low, its strong financial performance and market position make it an attractive potential investment opportunity.

RBA had an exceptional year last year, breaking several records and achieving an adjusted earnings per share rise of 24% YoY to a record $2.41. In addition, the company's acquisition of Insurance Auto Auctions is a significant strategic move, enabling RBA to tap into IAA's expertise in the salvaged vehicle market, a segment with strong growth prospects.

Ultimately, investment decisions all come down to the valuation. According to the DCF analysis, RBA is slightly overvalued, but compared to its peers using various popular valuation ratios, there appears to be significant value in the company. While I prioritize the DCF analysis over the comparative analysis, the results suggest that RBA is not an investment considered objectively undervalued by investors.

For further details see:

Ritchie Bros. Auctioneers: A Financial Performance And Growth Analysis