BBBY - Rite Aid Shareholders Could Face Massive Dilution Or Being Wiped Out In Ch.11

2023-03-07 10:52:12 ET

Summary

- Rite Aid can only sell up to 12.6 million shares without getting shareholder approval to increase the number of authorized shares.

- Because the company continues to burn cash and is highly leveraged it could end up in Ch.11 if there is a recession.

- Under the revolver agreement, Rite Aid is allowed to repurchase second lien notes and unsecured notes.

- Covid-19 vaccines continue to decline.

- The 2022/2023 flu season is much worse than last year.

Rite Aid Corp. ( RAD ) shareholders have endured terrible results the last few years and the future does not look very promising either. Since my February 26, 2021 sell recommendation article RAD stock has plunged 82%. To long-term RAD shareholders the current price of $3.57 is actually about $0.18 per share after adjusting for the 2019 1-20 reverse stock split. That is all in the past. Investors want to read about what might happen over the next year or two. Basically, I am expecting significant dilution for current shareholders, or they might be completely wiped-out in a Ch.11 bankruptcy process. This is an update to prior RAD articles.

Sell Stock to Raise Cash = Dilution

In order to stay out of bankruptcy court, in my opinion, Rite Aid needs to greatly reduce their debt. An exchange offer of stock for debt is often used to deleverage. Another way is to sell new shares and use the cash to pay down debt. This method has become popular in the last few years. AMC Entertainment Holdings ( AMC ), for example, has sold a massive number of new shares to pay down their debt. They went from having 109.3 million total number of A and B shares in August 2021 to 517.6 million shares currently, which does not even factor in the preferred shares ( APE ).

Many RAD investors are wondering if the company could try to raise a large amount of new cash via massive new stock offering something like Bed Bath & Beyond's ( BBBY ) offering in early February. BBBY deal was for over $1 billion, but it will increase the number of BBBY shares outstanding to almost 900 million shares from 117.3 million. That implies BBBY will receive an average amount of approximately $1.28 cash per new share outstanding. That is a LOT of dilution. The heart of the offering was the "sweetheart" deal offered to those institutions that bought at least $75 million under the offering, which effectively allowed them to purchase BBBY shares significantly below the market price. The trade by institutions was to sell short BBBY stock, participate in the sweetheart deal, and then use those cheap shares to cover their short positions.

In theory Rite Aid issuing additional shares to raise cash to pay down debt seems doable, but it may not be so easy. Rite Aid had 56,523,354 shares outstanding as of December 22, 2022. The total authorized shares are only 75 million. Based on my calculations using the 2022 proxy statement , a total of 5.816 million shares either have been granted as part of awards given or are reserved for future awards under incentive plans already approved by shareholders. This means that only about 12.6 million RAD shares could be sold in a stock offering without receiving shareholder approval to increase the number of authorized shares. With the stock selling at $3.57, that would imply they might be able to raise about $45 million, which is a "token" amount compared to their $3.2 billion in long-term debt.

Originally AMC did not face the need to get shareholder approval to increase the number of authorized shares because when they started selling new shares, they were already authorized to issue 524.2 million shares, but when management tried to get authorization to increase the number, they pulled the proposal for lack of shareholder support. BBBY already had authorization for 900 million shares.

If Rite Aid tries to seek shareholder approval to increase the number of their shares outstanding, they will not have the element of surprise that was associated with the BBBY stock sale. I don't, however, see any organized "meme" trader opposition to RAD shareholders voting to increase the number.

Assuming for a moment that they do get authorization to increase the number of shares and are successful selling them, there could be massive dilution for current RAD shareholders. Noteholders and holders of Rite Aid debt could benefit by using the cash raised to pay down debt, but there could also be a repeat of a S&P determination that Rite Aid technically "defaulted", which I covered in a July RAD article.

The clock is working against Rite Aid. In the past the company has filed their proxy for the annual meeting around May 21 with a voting record date approximately June 2. The shareholder meetings are usually held the last of July. That is a long time before a potential for a vote on the increase in the authorized shares. There is, however, the possibility of a special meeting could be called much earlier under the company's by-laws ( text of the by-laws ) to vote specifically on this matter.

Debt Reduction

Rite Aid would get more "bang for their buck" by buying back debt selling at steepest discount to par and/or closest to maturity. Assuming that they are able to raise a significant amount of cash via a stock offer, what are the restrictions on what debt can be paid down? The amended revolver "allows for the voluntary repurchase of any debt or other convertible debt, so long as the Currently Effective Facilities are not in default and the Company maintains availability under its revolver of more than $375.95 million", according to their latest 10-Q .

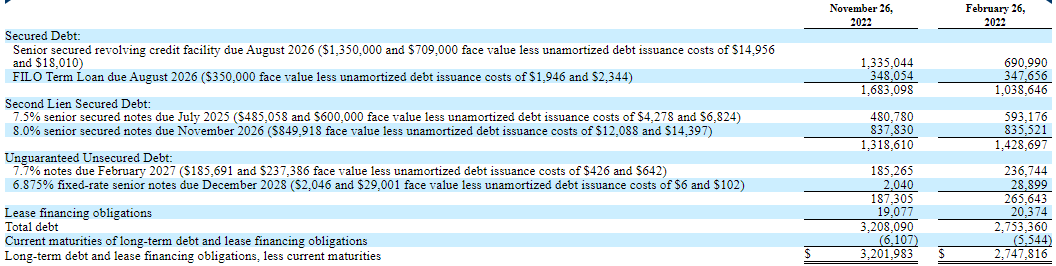

Long-Term Debt

{kind=link}

Their revolver has a current credit limit of $2.850 billion, which was increased by $50 million last December 1, and as of November 26, 2022, they borrowed $1.335 billion under the revolver. This implies they had $1.515 billion still available at the end of November. Initially it would seem that there is plenty of room for them to be able to repurchase debt under the $375.95 million restriction. There are, however, two problems. First, Rite Aid has been burning cash and borrowing more. They burned up $318.852 million cash from operations for the nine months ending November 26, 2022. Second, if results worsen in the near future the revolver limit could get reduced.

Having a massive stock offering most likely would greatly benefit debt holders, including holders of 7.7% 2/15/2027 unsecured notes (CUSIP 767754AJ3). These unsecured notes are extremely risky because there is a high probability that if Rite Aid does not raise new cash via a stock/rights offering and it continues to burn cash that it could be in Ch.11. Under a Ch.11 reorganization plan, in my opinion, it is unlikely unsecured notes would get any recovery because there is just too much debt that has a priority for recoveries, unless they receive a "gift" from a higher priority class. I would also expect RAD shareholders would be wiped out under a Ch.11 reorganization plan.

Some Factors That Could Impact 4Q Results

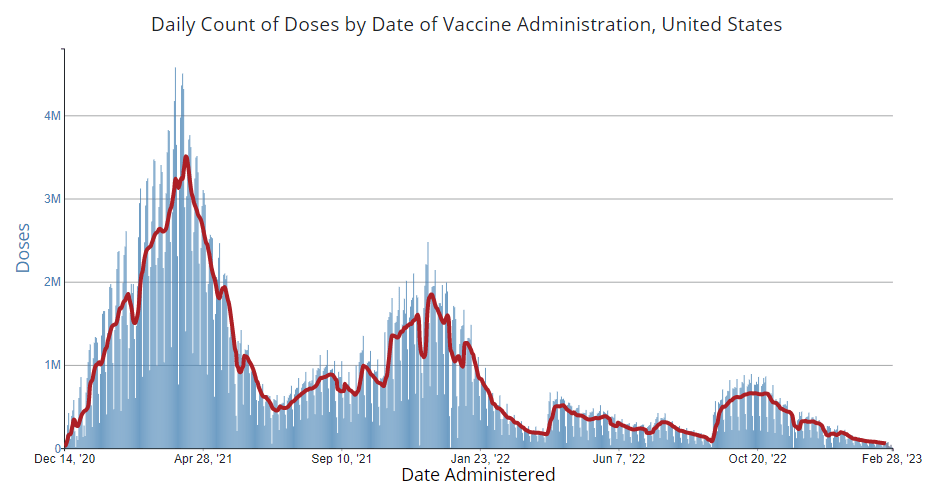

The positive impact of Covid-19 vaccines on Rite Aid continues to drop to a very low number. The chart below is for all Covid-19 vaccines in the U.S. and not just for Rite Aid, but it does give the general idea of the vaccines administered at Rite Aid stores. Besides the revenue from the vaccines, there is increased foot traffic into Rite Aid stores and that often results in other purchases. Without the revenue related to Covid-19 vaccines, 4Q could compare negatively to 4Q 2022 fiscal year's results.

{kind=link}

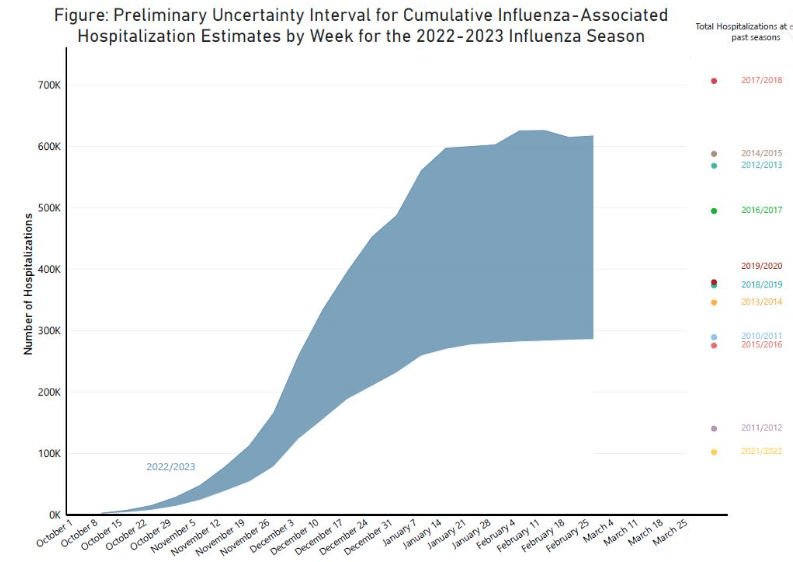

The 2022/2023 flu season seems to be much worse than the prior year. The number on the table below for 2021/2022 flu season is the bottom right figure. The chart itself is for estimates, which has a very wide estimate range, of hospitalizations, but the estimates do indicate that there most likely will be a significant number of consumers shopping for medications at Rite Aid stores during the 4Q. This should be a major positive for Rite Aid as it should increase foot traffic.

{kind=link}

Conclusion

Since I am expecting a recession starting in 2Q or early 3Q and Rite Aid is extremely leveraged, the company may need to take drastic steps to keep out of bankruptcy court. I covered issues in prior articles about selling Elixir and I think raising cash via a massive stock offering might be their best hope at this point.

While a stock offering would help debt holders, I am not recommending the purchase of their unsecured notes because of the risk of not getting any recovery if Rite Aid does eventually file for Ch.11. I am maintaining my neutral/hold recommendation on RAD stock because there is still the potential of a turnaround or some white knight riding in to buy them. Investors must understand that RAD is a very risky trade.

For further details see:

Rite Aid Shareholders Could Face Massive Dilution Or Being Wiped Out In Ch.11