CA - Rogers Communications: LTV Growth And Earnings Performance Encouraging

2023-07-31 17:23:07 ET

Summary

- Rogers Communications has shown encouraging performance on LTV and earnings metrics.

- While long-term debt has increased as a result of the Shaw acquisition, I take the view that the company has the capacity to reduce this over time.

- I take a bullish view on Rogers Communications.

Investment Thesis: I take a bullish view on Rogers Communications (RCI), given strong customer lifetime value ((LTV)) performance, as well as continued earnings growth.

In a previous article back in March, I made the argument that Rogers Communications could see lackluster growth until the eventual outcome on the Rogers-Shaw merger becomes more clear and earnings growth starts to rebound towards pre-pandemic levels.

Since then, the stock has descended slightly to a price of $44.10 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Rogers Communications has the ability to see continued growth from here, taking recent performance into consideration.

Performance

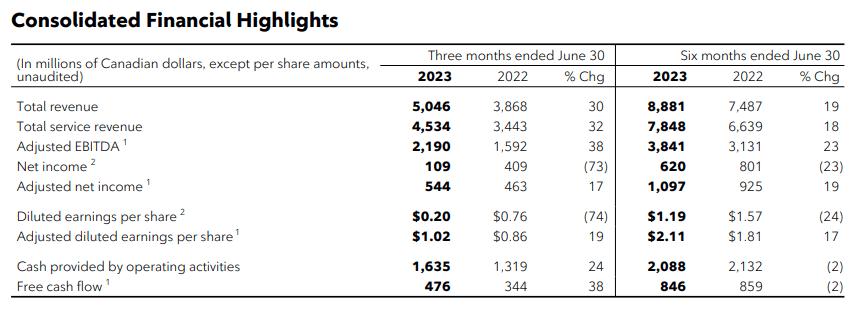

When looking at the most recent earnings results for Rogers Communications, we can see that adjusted diluted earnings per share was up by 19% from that of the same quarter in the previous year. We can see that while diluted earnings per share itself showed a sharp drop of 74% over the same period - this is due to an ongoing increase in quarterly depreciation and amortization of $0.5 billion due to the assets acquired through the $26 billion Shaw Transaction that was completed last April. In this regard, adjusted diluted earnings is used to gauge actual business performance:

Rogers Communications: Second Quarter 2023 Results

{kind=link}

Aside from earnings, I choose to also analyze the customer lifetime value across the postpaid segment for Rogers Communications. Customer lifetime value across the postpaid segment was calculated as ARPU / postpaid churn rate (%). Here are the results by quarter:

LTV calculated by author using ARPU and churn statistics from historical quarterly reports for Rogers Communications. Heatmap generated by author using Python's seaborn visualization library.

We can see that Q1 and Q2, 2022 showed the highest LTV. While LTV for the most recent two quarters was lower than that of last year - LTV still remained high compared to other quarters.

This was due to a combination of higher ARPU and a lower churn rate. For instance, the average ARPU for all the above quarters was $53.99, while churn came in at 0.97%. However, ARPU for the most recent quarter was $56.79 while churn was 0.87%.

On the whole, we can see an overall trend of LTV growth since 2019 - which is encouraging. This means that the total revenue an average customer brings in over the lifetime of their contract with Rogers is increasing.

Balance Sheet

With regards to short-term liquidity, we can see that the quick ratio of Rogers Communications (calculated as total current assets less inventories all over total current liabilities) remains below 1 and has fallen slightly from that of December.

| Dec 2022 |

| Jun 2023 |

| Total current assets |

| 6446* |

| 6721 |

| Inventories |

| 438 |

| 545 |

| Total current liabilities |

| 9549 |

| 10308 |

| Quick ratio |

| 0.63 |

| 0.60 |

Source: Figures sourced from Rogers Communications Q2 2023 Press Release. Quick ratio calculated by author.

* As a caveat, note that total current assets for December 2022 actually came in at 19,283. However, this was comprised of 12,837 in restricted cash and cash equivalents set aside solely for partially funding the Shaw transaction and not available for other purposes. As a result, this is deducted from the total current assets for this period.

Additionally, long-term debt to total assets also saw a slight increase on a percentage basis over this period:

| Dec 2022 |

| Jun 2023 |

| Long-term debt |

| 29,905 |

| 38,411 |

| Total assets |

| 55,655 |

| 69,739 |

| Long-term debt to total assets |

| 53.73% |

| 55.08% |

Source: Figures sourced from Rogers Communications Q2 2023 Press Release. Long-term debt to total assets ratio calculated by author.

I take the view that while investors will tolerate elevated levels of long-term debt and a lower quick ratio for the time being due to the Shaw acquisition as well as continued growth in earnings and LTV - a continued increase in long-term debt levels may raise concerns over a longer period now that the Shaw acquisition has been completed.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, growth in adjusted diluted earnings as well as an increase in LTV across the postpaid segment are both encouraging. While Rogers has been incurring further long-term debt on its balance sheet - I take the view that investors will be willing to tolerate this in the short to medium-term due to the acquisition of Shaw.

Over the longer-term, I take the view that investors will increasingly be expecting growth in earnings and LTV to translate into greater cash flow, as evidenced by an increasing quick ratio - as well as a reduction in long-term debt as Rogers pays off the costs of acquiring Shaw Communications.

Risks and Looking Forward

In terms of the potential risks to Rogers Communications at this time, there is always the possibility that the growth that we have been seeing in LTV may moderate. From a seasonal perspective, we have seen from the period analyzed that LTV has traditionally been lower in Q3 and Q4. This has been primarily due to higher churn - average churn in Q1 and Q2 since 2019 has been 0.84%, while it has been 1.13% for Q3 and Q4.

While it is uncertain as to whether the same trend will continue this year - it is a possibility - and this could mean more modest LTV and a slower rate of growth in earnings for the latter half of 2023.

Additionally, investors will have higher expectations of performance for Rogers going forward as a result of the Shaw acquisition. For instance, the company has raised its adjusted EBITDA growth outlook from 33% to 36% for this year, as compared to a prior 31% to 35% outlook. This is in addition to a free cash flow outlook of $2.2 billion to $2.5 billion from a prior $2.0 billion to $2.2 billion.

As a result, should Rogers not meet these targets - then investors may be skeptical as to whether the Shaw acquisition has in fact been successful, and we could see a risk of downside in the stock as a result.

Conclusion

To conclude, Rogers Communications has continued to see growth in earnings and strong LTV performance. While I take the view that Rogers Communications now needs to show improvement in its balance sheet metrics as well as evidence that it can meet its updated earnings and free cash flow targets - I am optimistic that the company has the capacity to achieve this, given the resilient performance we have seen to date in spite of costs incurred by the Shaw acquisition.

I take a bullish view on Rogers Communications.

For further details see:

Rogers Communications: LTV Growth And Earnings Performance Encouraging