CA - Rogers Communications: The Worst Of The Canadian Telecommunications Giants

2024-01-18 07:52:17 ET

Summary

- Rogers Communications is losing customers to competitors, impacting growth and profitability.

- The regulatory environment for telecommunications companies in Canada is becoming less favorable, potentially leading to lower prices and reduced profitability.

- The recent actions of the Rogers family in the company's governance raise concerns about shareholder interests and the level of control they have over the company.

- With a highly levered balance sheet and high capex costs, I would stay away from Rogers' shares today.

Please note all $ figures in , not , unless otherwise stated.

Investment Thesis

If you're a Canadian like I am, you're no doubt familiar with Rogers Communications ( RCI.B:CA ), one of the largest telecommunications companies in Canada along with Telus ( T:CA ) and BCE ( BCE:CA ). In fact, because of the oligopolistic nature of the telecommunications industry, you're likely a customer, or have been a customer, of Rogers through its wide range of services including wireless home phone, landline, cable, data roaming, and more.

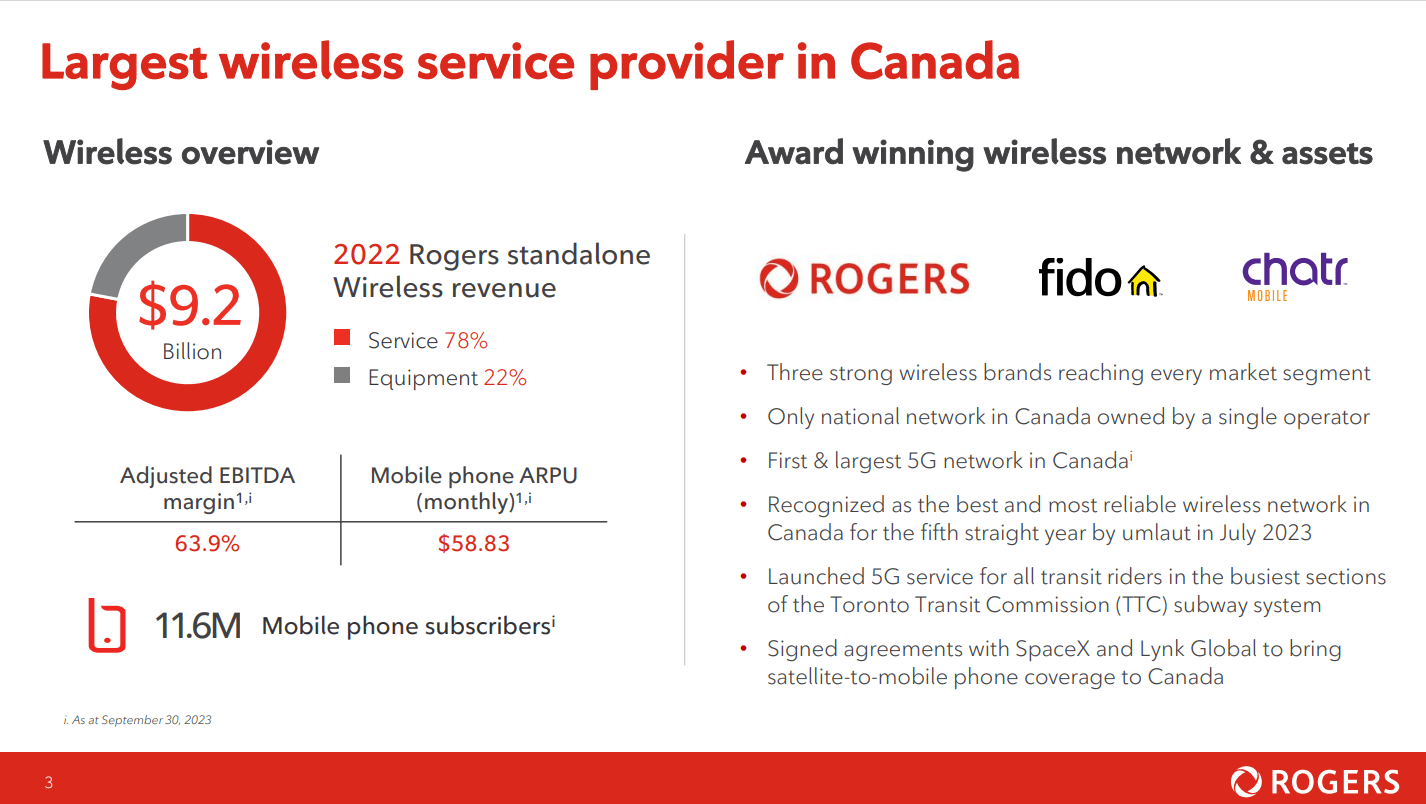

Rogers Overview (Investor Presentation)

{kind=link}

As a key service provider for over 11.3 million customers, about 1 in 3 Canadians are customers of Rogers. While I'm a customer of Rogers, I'm certainly not a shareholder. And based on my analysis, I'll be avoiding shares of the company for now.

In this article, I'll discuss six main reasons why I believe investors should not invest in Rogers Corporation's shares: (1) the company is losing customers to competitors, (2) the regulatory environment looks less favorable going forward, (3) the Rogers' family involvement isn't shareholder friendly, (4) rising capital expenditures are eating up a decent chunk of company's earnings, and (6) the company has a highly levered balance sheet.

Losing Customers To Competition

Rogers operates in an oligopoly with Telus and BCE (the parent company that owns Bell) being the main players in the telecommunications industry. There's a few smaller competitors like SaskTel in Saskatchewan, as well as Quebecor ( QBR.B:CA ) and Cogeco Communications ( CCA:CA ) in Ontario and Quebec, but they are much smaller and don't have national coverage like the 'Big 3' do.

While all three have your standard wireless, landline, and cable, there are a few differences. For example, Rogers and Bell have media divisions that they own, and Telus has a home alarm system service they offer now, following the acquisition of ADT Security Services Canada in 2019 for $700 million , which is now called TELUS SmartHome Security and Secure Business. Overall though, despite a few difference here and there, they tend to compete in the same arena.

One of the biggest aspects of my investment thesis is that Rogers seems to be losing customers to its peers Bell and Telus. In a report published by the Complaints for Telecom-Television Services ((CCTS)), Rogers received the most customer complaints for the first time in 15 years, outpacing Bell with complaints rising 43.6% from last year. I view this as terrible performance on the part of Rogers as the average increase for all service providers was just 14% by comparison. Rogers alone accounted for 1 in 5 complaints received by the CCTS.

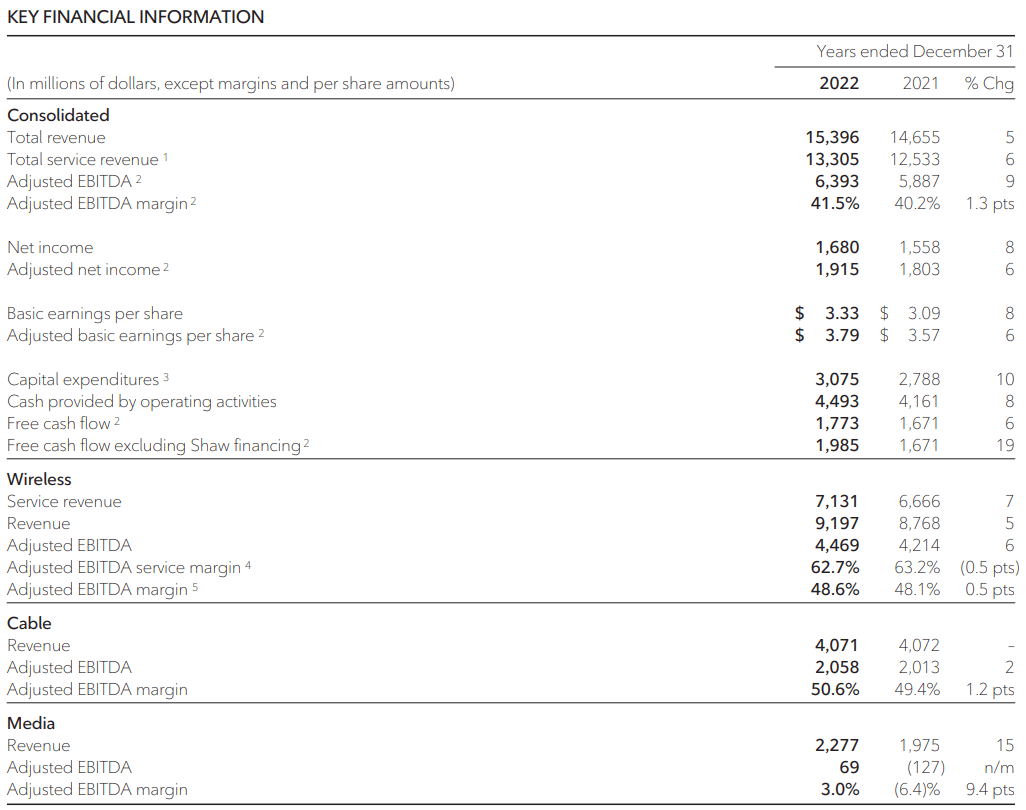

While the specific reasons were not highlighted, wireless issues made up 45% of all complaints received. To me, this is a troubling sign at Rogers as wireless makes up 59.7% of revenues and 70.0% of EBITDA (on an adjusted EBITDA margin of 48.6% segment). As the major contributor of the company's sales and earnings, this could be a significant factor that impacts both growth and profitability going forward.

Revenue and EBITDA Breakdown (Annual Report)

{kind=link}

With a few major outages and several smaller disruptions in service, Rogers has gotten a lot of pushback from customers and neither Telus nor Bell have seen nearly the same volume of outages and disruptions in wireless service. In addition, as Rogers plans to increase the price of cell phones for customers not on contracts, I believe Rogers could potentially see customers switch from the company's network to Telus and Bell who haven't announced aggressive price hikes.

Finally, with the introduction of BCE's fiber-to-the-home strategy, BCE could potentially grab market share from Rogers and impair the companies pricing power as Rogers will not be the only company when it previously was the de facto option due to its better network .

Regulatory Environment Looks Less Favorable

The next part of my investment thesis I want to discuss is the regulatory environment. Like utilities, telecommunications companies in Canada operate very similarly to regulated utilities, in that they provide an essential service and earn returns that are somewhat guaranteed by the government, in this case, the Canadian Radio-television and Telecommunications Commission, or CRTC , the primary regulator for telecommunications companies in Canada.

Canada is the second largest country by land mass, meaning its geographical reach is vast and requires more investment to have broadband and other wireless networks span great distances. With about 1 in 5 Canadians living in a rural area, the CRTC incentivizes investment by essentially limiting competition for the telecommunications companies. And now that more than 99.7% of Canadians now have access to mobile services with 96.0% having LTE-A connection, most rural areas are now connected. So there's a real chance that the CRTC may say that to have healthier price competition now, telecommunication companies need to lower their prices. As it is, Canadians pay some of the highest cellphone bills in the world.

With telecommunications companies being highly levered (as a result of low returns on assets, much like utilities), there's a real risk that if pricing were to come down that that could seriously impair the pricing power and profitability of the three large telecommunications companies in Canada. We've already seen evidence of pressures on the telecommunication companies to reduce their prices and so I believe this will hurt the profitability and hamper top-line growth of Canadian telecommunications companies in the future.

Finally, while Rogers has experienced strong synergies (around $600 million expected by year end) as a result of acquiring Shaw at a 69% premium in Spring 2021, there still remains integration risk as it's still early days. Furthermore, I believe regulators will be watching what Rogers does very closely to make sure it doesn't start to raise prices and actually follow through on its promises of cutting prices for Canadians.

Rogers Family Involvement

I'm not really an ESG investor but the biggest factor of ESG that I care about is governance. Governance is important because it plays a crucial role in determining how a company is managed, overseen, and held accountable.

And in the case of Rogers Communications, I don't believe these three things are being carried out fairly by the board or by management. For one thing, the shareholder structure of having both A shares and B shares ensures that the Rogers family retains 97% of the company's votes despite only owning 29% economic interest. For the minority shareholder who owns the class B shares, this doesn't seem very shareholder friendly.

At present, the former CEO is also suing the company for $24 million, alleging that he was unfairly ousted by chairman Edward Rogers, claiming that he was responsible for "malicious, high-handed, and oppressive conduct". But this isn't the first time the Rogers family have been involved in quarrels at the board level. Earlier, the chairman wanted to get rid of Rogers' CEO and promote the CFO to the role. Through the Rogers Control Trust, which is the entity that gives them 97% voting control, he tried to get rid of 5 directors and replace them with his own nominees. In my view, all of this shows that the Rogers' family likely don't have the best interest of minority shareholders in mind. At best, it demonstrates the power, control, influence one man (and his family) have over the future of the company.

Capex Spend Eats Up Most Of Earnings

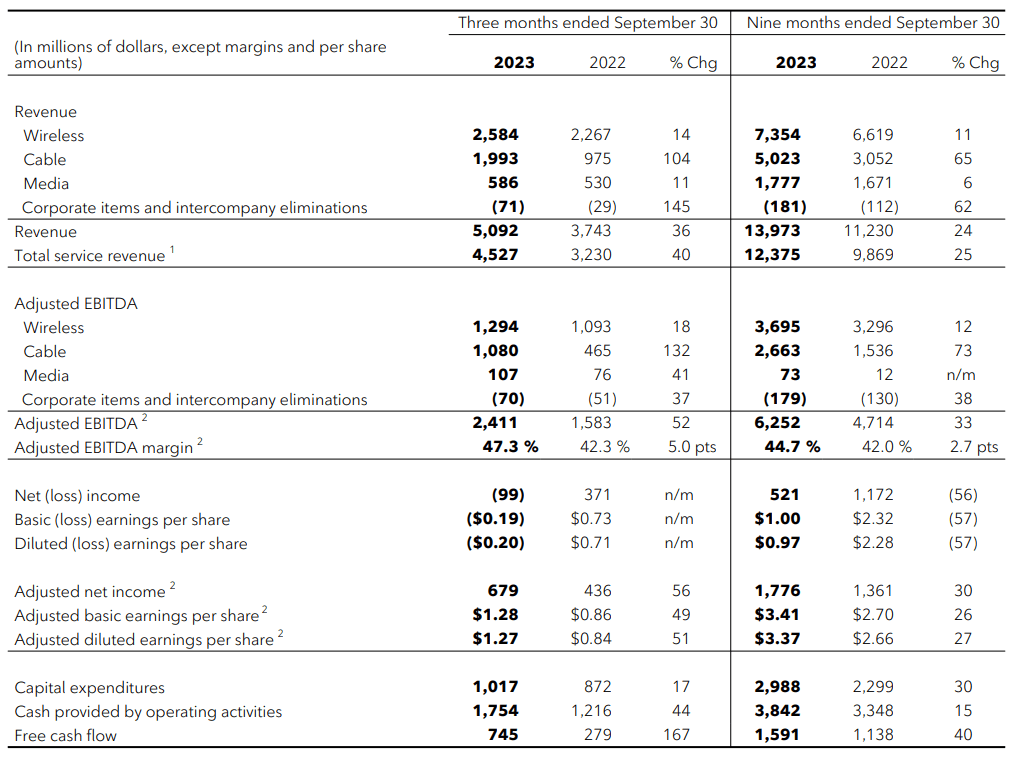

When we take a look at the Rogers' cash flow statement below, we can observe a good chunk of the company's adjusted EBITDA goes into capex (about 42.2%). Along with high debt on the company's balance sheet , the company paid around $512 million in interest for the quarter ($1,324 million year to date) so this takes another 21.2% out of adjusted EBITDA. At the end of just these two major items, this doesn't leave us with much left. When we consider that $264 million is paid out in dividends each quarter ($769 million year to date), Rogers is currently paying out 102% of its adjusted distributable earnings for the quarter or about 48.3% of free cash flow based on year to date figures.

{kind=link}

With the current dividend yield clocking in at 3.1%, this suggests that if Rogers were to pay out all of its free cash flow as a dividend, it would barely be 6.2%. For a company with $41.3 billion of debt against its $34.0 billion market capitalization, the EV to Free Cash Flow multiple looks atrocious. Despite the interest on the debt being long-term (weighted average of about 10.1 years) and at low interest rates (4.88% weighted average), the debt leverage ratio of 4.9x indicates that it will take time for the company to de-lever the balance sheet to get to a more comfortable level.

Moreover, this doesn't really leave much room for dividend increases or share repurchases because the operating income is going primarily to capex, interest payments, and supporting the 3.1% dividend yield. So this tells me that we shouldn't expect to see much growth out of the company.

Valuation

Based on the 10 sell-side analysts with one-year target prices on Rogers' stock, the average target price is $75.94, with a high estimate of $82.00 and a low estimate of $72.00. From the current price to the average target price one year out, this implies potential upside of 18.6% not including the company's 3.1% dividend (which would put the total return potential at 21.7%). This indicates that analysts are pretty bullish on the company's near term outlook.

I think analysts are being overly optimistic when it comes to Rogers' stock. When we look at the peer group, we can see that with less leverage, a slightly higher payout ratio, and a better expected EBITDA CAGR, investors in Telus' stock can get nearly double the yield (albeit at a higher valuation). I am inclined to assign a lower valuation to Rogers because it hasn't been able to generate the same returns as BCE and Telus despite being more leveraged. As such, I see better opportunities in Rogers' two competitors, BCE and Telus.

Comparable Companies Analysis (Author and TD's Estimates)

{kind=link}

When it comes to the risks to my investment thesis, I have to give credit to Rogers making some progress on the balance sheet front. In the last six months, they've dropped their leverage ratio by 0.5x and have realized $600 million of synergies year to date on the Shaw acquisition. If they're able to achieve more synergies than expected, continue to increase average revenue per user in a material way, or de-lever faster than expected, these are factors that would get me to reconsider my investment thesis.

Conclusion

Ultimately, Rogers is not the type of company I like to own. I want to buy businesses that take care of their customers, have significant pricing power, take a disciplined approach to managing their balance sheets, and align management incentives with shareholder interests. I can't feel I can say the same for Rogers given the headwinds ahead in the regulatory environment, customers switching to BCE and Telus, turbulence at the board and senior management level, and a poor, overleveraged balance incapable of generating outsized returns, I don't see value in shares today and would rate the shares as a sell for now.

For further details see:

Rogers Communications: The Worst Of The Canadian Telecommunications Giants