MELI - Rondure Global Advisors Q1 2023 Commentary

2023-05-18 03:30:00 ET

Summary

- Rondure Global Advisors is a women-owned investment adviser focused on high-quality equity investing for the long-term. We are deeply client-focused and actively cost-conscious, as we are heavily invested alongside our clients for the long haul.

- Rondure New World outperformed the benchmark by approximately 116 bps during the first quarter of 2023.

- We remain conservatively positioned in terms of stock selection.

What Lies Beneath

A system, artificially stabilized, and of course, you have hidden risks under the surface, and you don't know where the risks are." - Nassim Nicholas Taleb

Push any complex system long enough in an attempt to stabilize it - and eventually, the system pushes back on you.

That was the lesson of the first quarter of 2023. Here is what we mean by that:

Central bankers and legislators have worked overtime since the Great Recession to keep the world's economies on an even bearing. By many measures, they have succeeded: Market volatility has been lower, by some metrics, since 2009 than at any other time in recorded history.

Yet every balancing act requires something falling out of kilter in order to keep something else level.

This time is no different. Yes, much appears to be orderly in terms of market functioning, asset prices, and the broader economy (despite exceptional volatility in sovereign debt markets). Proliferating crises have been averted in U.S. and Swiss banking circles for the time being. Main Street has avoided the worst of it, as has Wall Street. Few landings have been hard - at least for now.

In fact, market behavior in the last few weeks seems downright bullish, suggestive of a newfound risk appetite. Two favorite equities trades have been going long deep-value stocks and go-go growth stocks, as investors embrace the view that looser monetary policy ahead may provide salvation to the riskiest among us.

Yet not far below the surface, we still feel a deep sense of unease that neither the real economy nor financial markets are on an entirely firm footing.

We are maintaining our trademark caution in outlook and positioning. We are not ready to run off to the races quite yet. Why? Mainly because we do not think valuations warrant it, with few exceptions.

As far as last quarter goes, the yield on the U.S. 2 Year Treasury tells the story.

2-Year U.S. Treasury Yield (Year to Date)

{kind=link}

The quarter began with a surge of optimism, thanks to cooling inflation in advanced economies and the hope that China's post-Covid reopening might spark the global growth engine. After a tough 2022, markets breathed a collective sigh of relief, bidding up risk-on assets like technology stocks and growth companies that had fared woefully over the prior twelve months.

Then the fireworks exploded: News of the cascading collapse of several U.S. banks and others teetering on the edge. U.S. Treasuries caught a fierce bid in what was both a flight to safety as well as a recognition that banking crises are inherently contractionary, which could limit how much future rate hiking the Fed would need to do.

Spring's banking shock was a reminder that just because a risk is not understood by the market - or does not come to fruition - does not mean it is not lying in wait.

It may simply lie beneath.

That observation implies that caution may still be warranted even after prudence has fallen out of fashion, as traders return to the same bullish trades that have worked like a charm over the last decade or longer.

If we had told you last December that markets would shortly be facing the most serious banking crisis since 2008; or that Credit Suisse, a 167-year-old Swiss icon, would fail and be swallowed by its domestic rival; or that gold would make a play for its all-time high as investors flocked to safety, you would likely have thought us too bleak.

Thankfully, our research process proved effective in keeping us out of the eye of the storm last quarter (distressed banks). We were underweight financials in both strategies, which served us well given that the sector was one of the poorer performers during the quarter.

Unfortunately, media hype about Chinese weather balloons over North America derailed what had been a positive start to the year in emerging markets. It played to investors' worst fears that a new Cold War between the United States and China may be unfolding. We think the whole episode was largely inconsequential - but made for good news copy. It did not change our thinking or positioning. The media and politicians have moved on to new storylines, making the series of events seem like market noise.

One of the beautiful things about being able to invest down the market capitalization spectrum and in places far from the United States is that the banking drama in Silicon Valley left our holdings unscathed. It was largely inconsequential to either Rondure fund in any direct sense. That is the power of geographic diversification and an argument for investing both within and without one's own country. Even when there are tremors in your home market, another market may be enjoying relative calm.

Rondure New World Strategy

Rondure New World outperformed the benchmark by approximately 116 bps during the first quarter of 2023.

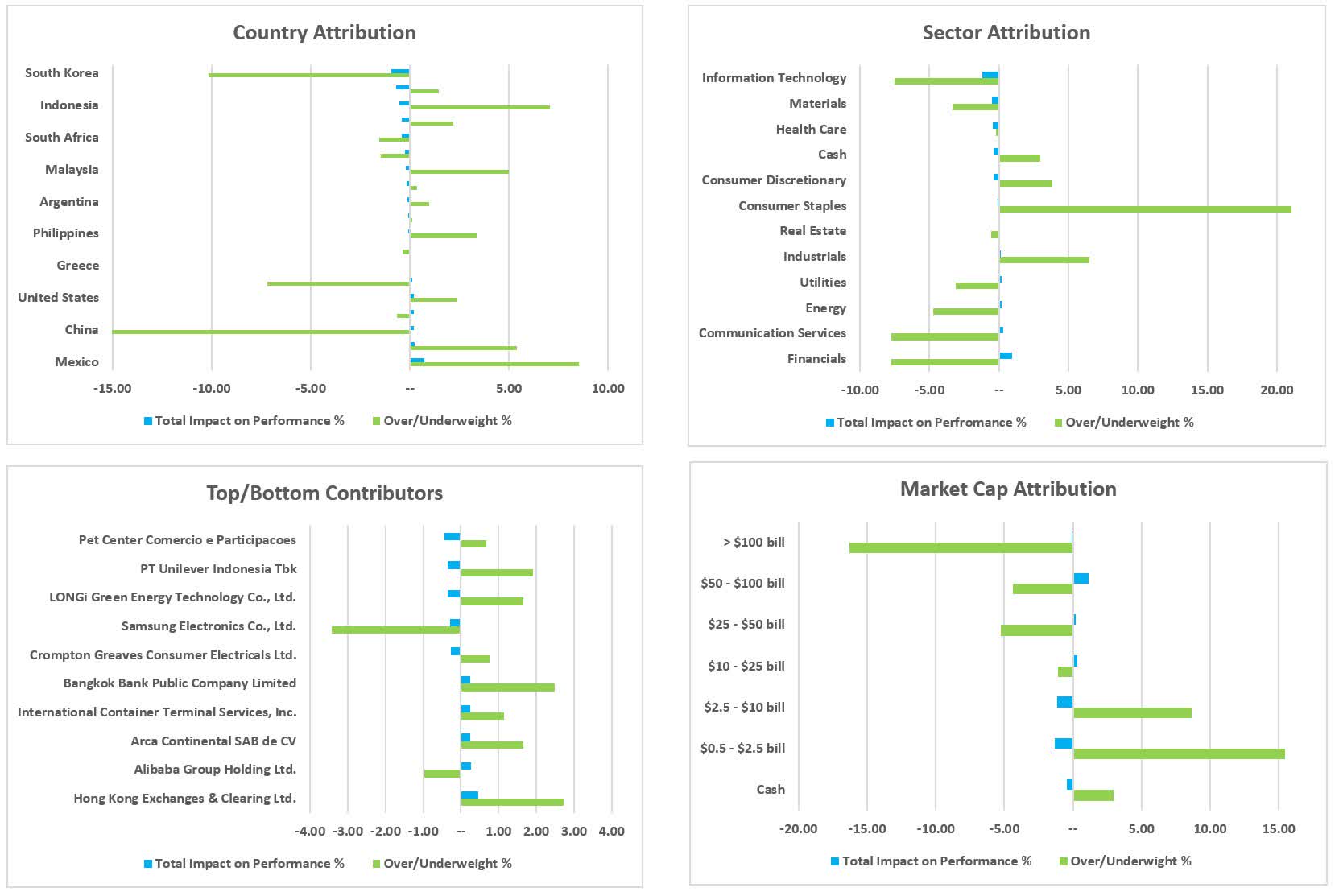

In terms of sectors, Industrials and Consumer Discretionary were the top contributors to relative performance while Information Technology and Communication Services were the largest detractors. With respect to Industrials, Mexican transportation stocks, both air and rail, drove outperformance. The post-covid recovery in tourist traffic coupled with multiple reranking drove the airports, while the rail company, GMexico Transportes (GMXT* MM) ( GMXTF ) benefited from robust topline growth as well as improving operational efficiency. MercadoLibre ( MELI ), the largest e-commerce and payment ecosystem in Latin America, was the main contributor to Consumer Discretionary outperformance. The company has significant room for growth as e-commerce and digital payment penetration rates improve. Information Technology was the best-performing sector in the MSCI Emerging Markets Index during the first quarter, thus our underweight hurt relative performance. The stock selection also weighed on relative performance. Specifically, we were underweight mega-cap stocks such as TSMC ( TSM ) (2330 TT) and Samsung ( SSNLF ) (005930 KS), both of which performed well. Our underweight in Communication Services, the second-best performing sector, also weighed on relative performance.

With respect to countries, Mexico, India, and Argentina were relative outperformers while South Korea, Taiwan, and Malaysia were relative underperformers. As mentioned above, our Mexican transportation stocks were strong contributors. India was the second worst performing country in the benchmark during the quarter after the UAE, yet Rondure's stock selection was accretive to relative performance. Our overweights in IndiaMART InterMESH (INMART IN), Tech Mahindra (TECHM IN), and HCL Technologies (HCLT IN) were beneficial. IndiaMART is an Indian e-commerce company seeing strong revenue momentum and stabilizing margins. Both Tech Mahindra and HCL Technologies are software companies that performed relatively well versus the local market during the quarter. Argentina's outperformance was a function of MercadoLibre.

Rondure Overseas Strategy

Rondure Overseas underperformed the benchmark by approximately 166 bps during the first quarter of 2023.

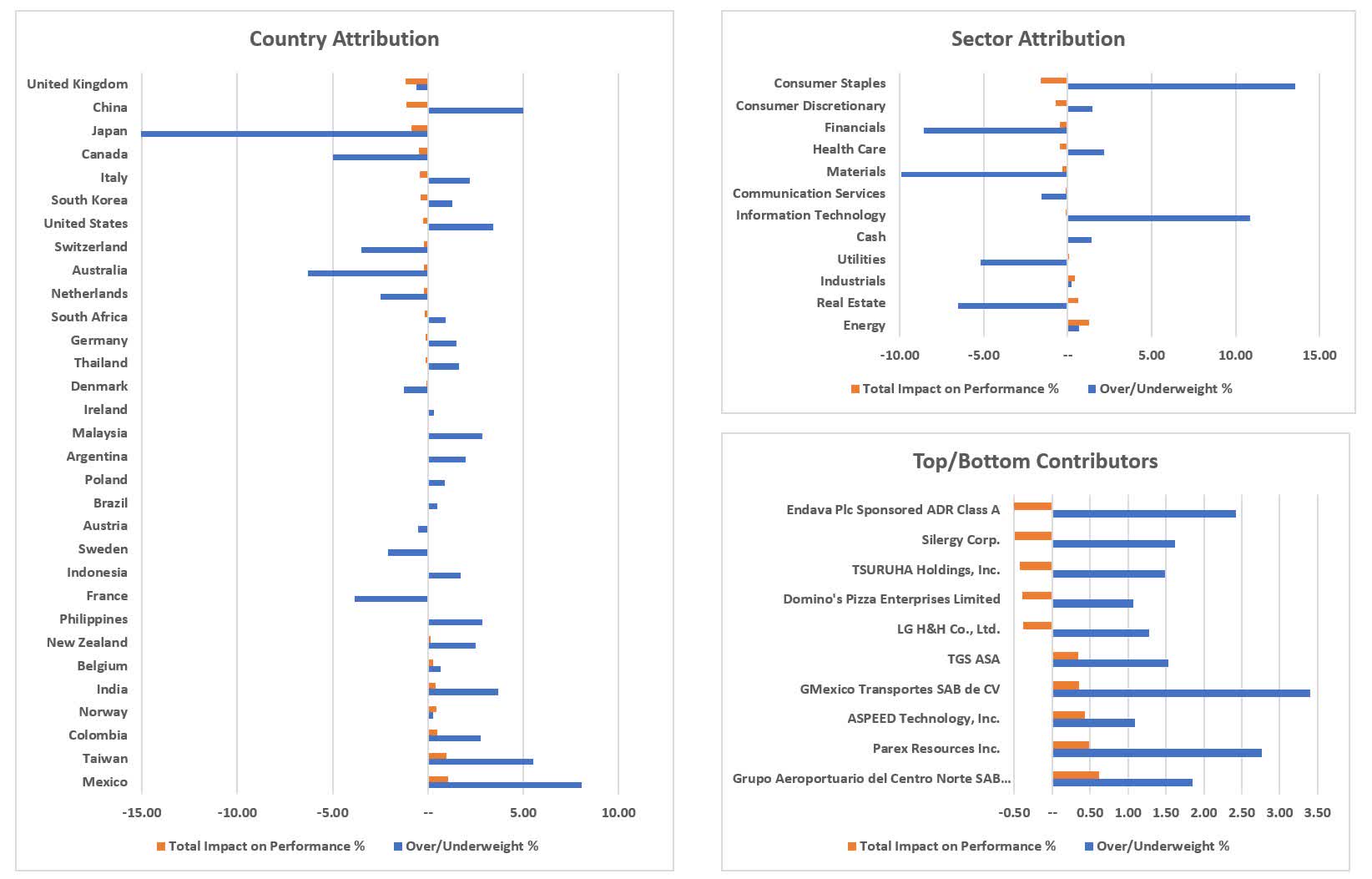

Energy and Real Estate were the top contributors to relative performance while Consumer Staples and Consumer Discretionary were the largest detractors. While Energy was one of the poorer sector performers during the first quarter, down over 3%, our energy stocks rose almost 30%. Parex Resources (PXT CN), a Colombian exploration and production company continues to drive production growth and improve capital efficiencies. TGS (TGS NO), a seismic data company, is benefiting from improved demand as oil companies increase exploration budgets. The real estate sector also performed poorly during the quarter, thus the fact we had de minimis exposure here was beneficial.

Our large overweight in Consumer Staples was a drag on performance as were a number of owned names. Japanese drugstores Tsuruha Holdings ( TSUSF ) (3391 JP) and MatsukiyoCocokara ( MSMKF ) (3088 JP) lagged due to a thus far disappointing rebound in sales to inbound tourists. We believe we will see more robust topline growth and earnings recovery as we move through the year. LG H&H (051900 KS), a Korean personal and household goods company, has yet to see a rebound in either duty-free or Chinese sales. We maintain our conviction regarding a recovery in sales and earnings over the course of 2023.

The Consumer Discretionary sector performed well during the quarter and our overweight here was additive. Our stocks fared less well, specifically Domino's Pizza Enterprises ( DPZUF ) (DMP AU) and Puma ( PMMAF ) (PUM GR). Domino's Pizza Enterprises is the global chain's master franchisee covering Australia, New Zealand, France, Belgium, The Netherlands, Japan, and Taiwan. They are struggling to adjust to higher inflation and discovering that pizza is price elastic. Although recent earnings were weak, we believe this is transitory. Puma struck a cautious tone during the quarter, issuing 2023 guidance below expectations based on a muted Chinese recovery and subdued gross and operating margins. We continue to believe in the medium-to-long-term margin expansion potential of Puma as China reopens and both inventory and raw material costs normalize.

By country, Mexico, Taiwan, and Colombia were the top contributors to relative performance while the United Kingdom, China, and Japan were the largest detractors. In Mexico, air and rail stocks performed well while Taiwan and Colombia were helped by our holdings in Information Technology (Aspeed Technology, Sinbon Electronics) and Energy (Parex Resources ( PARXF ) (PRX CN)). Our overweight in all three regions was additive. Stock selection hurt us in the UK, specifically, Endava ( DAVA ), an IT consulting firm that lowered 2023 guidance early in the year as customers slowed decision cycles on new projects, particularly in the TMT segment. Our overweight in China as well as stock selection contributed to underperformance. Silergy ( SLEGF ) (6415 TT), a semiconductor manufacturer, is in a sales correction while Hangzhou Oxygen Plant (002430 CH), one of the largest industrial gas suppliers in China, posted a less-than-stellar quarter due to higher labor costs and receivables and inventory impairment. We believe the longer-term theses for both these names are intact.

Outlook

From a top-down perspective, two critical variables this year will be the future direction of U.S. monetary policy and Chinese business policy, in our view.

Our Chief Investment Officer, Blake Clayton, is fond of saying that interest rates are like the sun - everything in the market revolves around them. In the case of emerging and international markets, that can be doubly true. Emerging markets tend to suffer disproportionately from rising U.S. interest rates. A strong U.S. dollar tends to suck capital out of emerging economies and aggravate local debt burdens. Yet when U.S. inflation cools faster than expected and the Fed charts a course toward easier money, it can disproportionately benefit emerging markets. It is not coincidental that the great bull markets in international equities over the last 40 years occurred when interest rates were falling and the U.S. dollar was weakening.

China is the all-important wild card. China is by far the largest country in the MSCI Emerging Markets Index (33%). Beijing has been largely hostile to private enterprise over the last two years in its regulation and public statements, but that is starting to change as Xi's deputies adopt a friendlier tone. Still, small disturbances like the purported spy balloons over North America can cause major dislocations in foreign markets in the short term. An ironing out of the relationship between Washington and Beijing would be a major positive catalyst for emerging markets, while a deterioration would almost certainly prove the opposite.

Many of our favorite holdings right now are companies whose earnings we expect to positively inflect coming out of Covid-era lockdowns. A few examples:

We remain overweight Mexico, a standout contributor to performance last year, in both strategies. The country is a sleepy pocket of the international market where reliable dividend stocks have been attractively priced. We continue to like a handful of what we believe are excellent businesses there.

We are also excited about our holdings in Southeast Asia. Our New World strategy is overweight Thailand, Malaysia, and Indonesia. These countries have been broadly out of favor yet there are gems in these markets. We think they will benefit from China's reopening and higher raw materials prices.

East Asia's post-Covid reopening is another opportunity we are bullish about. China's reopening should have positive ramifications for cross-border travel across East and Southeast Asia. Outside of China itself, we believe South Korean and Taiwanese companies will benefit disproportionately.

Thai private hospitals, which cater to foreign medical tourists, and Mexican airports, whose performance hinges on passenger volumes, rebounded strongly coming out of Covid lockdowns. Our holdings in Rondure New World did well as a result. We have taken some profits in both areas.

Both our New World and Overseas strategies are perpetually underweight deep-value stocks, which tend not to be a process fit for us. The portfolio tilts toward quality companies that tend to trade at a higher price-to-book ratio than traditional value stocks, such as volatile banks and materials companies. The portfolio tends to outperform when these low-quality companies do poorly and vice versa. We believe that quality outperforms over time if bought at a reasonable price.

One opportunity we are monitoring is the ongoing sell-off in the Indian stock market. We believe valuations are becoming more attractive as this formerly hot market cools and earnings growth slows. Headline risks around the Adani Group have contributed to negative sentiment there. There is a wealth of excellent businesses in India. We would love the chance to pick out a few favorites and hold them over many years.

We remain conservatively positioned in terms of stock selection. We sleep well that way. We are focused on companies with strong balance sheets (net cash), consistent dividends, reliable returns on capital, and competitive moats, which are trading at reasonable valuations, in our view.

Thank you for your continued support for Rondure Global Advisors. We appreciate your partnership and trust.

- The Rondure team

New World Attribution Dashboard 4Q 2022

{kind=link}

Source: FactSet - 9/30/22 - 12/31/22. Current and future holdings are subject to risk and may change at any time. References to specific securities are not a recommendation to buy or sell. Past performance is not a guarantee of future results. References on this page to Over/Underweight are based on comparison to the MSCI Emerging Markets Total Return USD Index. Please see attached disclosures.

Overseas Attribution Dashboard 1Q 2023

{kind=link}

Source: FactSet - 12/31/22 - 03/31/23. Current and future holdings are subject to risk and may change at any time. References to specific securities are not a recommendation to buy or sell. Past performance is not a guarantee of future results. References on this page to Over/Underweight are based on comparison to the MSCI Emerging Markets Total Return USD Index. Please see attached disclosures.

Rondure Funds Performance as of 03/31/2023

| Rondure New World Fund |

| QTR |

| YTD |

| 1 Year* |

| 3 Year* |

| 5 Year* |

| Since Inception* |

| Institutional |

| 4.96% |

| 4.96% |

| -2.68% |

| 12.14% |

| 2.03% |

| 4.33% |

| Investor |

| 4.99% |

| 4.99% |

| -2.93% |

| 11.87% |

| 1.78% |

| 4.07% |

| MSCI Emerging Markets TR Net Index[1] |

| 3.96% |

| 3.96% |

| -10.70% |

| 7.83% |

| -0.91% |

| 2.63% |

| Rondure Overseas Fund |

| QTR |

| YTD |

| 1 Year* |

| 3 Year* |

| 5 Year* |

| Since Inception* |

| Institutional |

| 5.53% |

| 5.53% |

| -8.43% |

| 7.75% |

| 1.69% |

| 3.90% |

| Investor |

| 5.46% |

| 5.46% |

| -8.75% |

| 7.47% |

| 1.44% |

| 3.64% |

| MSCI ACWI ex US Mid Cap TR Index[2] |

| 6.51% |

| 6.51% |

| -7.21% |

| 12.52% |

| 1.67% |

| 3.81% |

| MSCI EAFE TR Index[3] |

| 2.61% |

| 2.61% |

| -0.86% |

| 13.52% |

| 4.03% |

| 5.41% |

*Annualized

[1] The MSCI Emerging Markets Total Return USD Index is an unmanaged total return index, reported in U.S. Dollars, based on share prices and reinvested dividends of approximately 1,383 companies from 26 emerging market countries. You cannot invest directly in an index.

[2] The MSCI ACWI ex USA Mid Cap Index captures mid-cap representation across 22 Developed Markets ((DM)) and 24 Emerging Markets ((EM)) countries*. With 1,200 constituents, the index covers approximately 15% of the free float-adjusted market capitalization in each country. You cannot invest directly in an index.

[3] The MSCI EAFE Total Return USD Index is an unmanaged total return index, reported in U.S. dollars, based on share prices and reinvested net dividends of approximately 900 companies from 21 developed market countries excluding the US and Canada. You cannot invest directly in an index.

Data shows past performance, which is not indicative of future performance. Current performance may be lower or higher than the data quoted. To obtain the most recent performance data available, please visit www.rondureglobal.com . The Advisor may absorb certain Fund expenses, without which total return would have been lower. These expense agreements are in effect through August 31, 2023. Investment returns and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost.

The Advisor has agreed to waive and/or reimburse fees or expenses in order to limit Total Annual Fund Operating Expenses After Fee Waiver/Expense Reimbursement (excluding acquired fund fees and expenses, brokerage expenses, interest expense, taxes, and extraordinary expenses) to 1.35% and 1.10% of the Fund's average daily net assets for the Fund's Investor Class Shares and Institutional Class Shares, respectively. This agreement ("the Expense Agreement") shall continue at least through August 31, 2023. The Adviser will be permitted to recapture, on a class- by-class basis, expenses it has borne through the Expense Agreement to the extent that the Fund's expenses in later periods fall below the annual rate set forth in the Expense Agreement or in previous letter agreements; provided, however, that such recapture payments do not cause the Fund's expense ratio (after recapture) to exceed the lesser of (i) the expense cap in effect at the time of the waiver and (ii) the expense cap in effect at the time of the recapture. Notwithstanding the foregoing, the Fund will not pay any such deferred fees and expenses more than three years after the date on which the fee and expenses were deferred. The Expense agreement may not be terminated or modified by the Adviser prior to August 31, 2023, except with the approval of the Fund's Board of Trustees.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. Visit www.rondureglobal.com to obtain a Rondure Funds Prospectus, which contains this and other information, or call 1.855.775.3337. Read the prospectus carefully before investing.

See the prospectus for additional information regarding Fund expenses. Rondure Funds will deduct a 2.00% redemption proceeds fee on Fund shares held 60 days or less. Performance data does not reflect the deduction of this redemption fee or taxes, which if reflected, would reduce the performance quoted. For more complete information including charges, risks, and expenses, read the prospectus carefully.

The objective of all Rondure Funds is the long-term growth of capital.

RISKS: Investing in foreign securities entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investments in emerging and frontier markets are subject to the same risks as other foreign securities and may be subject to greater risks than investments in foreign countries with more established economies and securities markets. Diversification does not eliminate the risk of experiencing investment losses.

Rondure New World Fund ([[RNWOX]]/[[RNWIX]]) - Inception date of 05/01/2017.

Expense ratios as of the prospectus dated 08/31/2022 are:

RNWOX: 1.58% Gross / 1.35% Net, RNWIX: 1.27% Gross / 1.10% Net

Rondure Overseas Fund ([[ROSOX]]/[[ROSIX]]) - Inception date of 05/01/2017

Expense ratios as of the prospectus dated 08/31/2022 are:

ROSOX: 1.88% Gross / 1.10% Net, ROSIX: 1.56% Gross / 0.85% Net

RON000485

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Rondure Global Advisors Q1 2023 Commentary