RPM - RPM: Integration Should Offset Housing Pullback And Foster Growth

2023-04-04 17:40:29 ET

Summary

- RPM beat on EPS and missed on revenue but remains positive on 2023 guidance.

- The company pays out a healthy dividend and repurchases shares.

- Acquisitions in the construction supplies segment will diversify the core business into more maintenance revenue streams, avoiding the construction industry.

- After completing a DCF analysis, RPM is relatively undervalued.

RPM International (RPM) has recently fallen from its high amid recent pullbacks in the housing market. With a recent underperformance in the construction supplies segment of their core business, strategic acquisitions and integration of purchases will promote strong growth and possibly offset drops in sales.

Business Overview

RPM International Inc. is a multinational company based in the United States that specializes in the production and sale of specialty coatings, sealants, and building materials. RPM operates through its subsidiaries and offers a broad range of products and services to a variety of industries, including construction, automotive, marine, and industrial.

The company was founded in 1947 and is headquartered in Medina, Ohio. RPM's business operations are divided into three segments: the industrial segment, the specialty segment, and the consumer segment. The industrial segment focuses on the production of high-performance coatings, sealants, and adhesives for the construction and industrial markets. The specialty segment focuses on the production of industrial cleaners, restoration services, and specialty chemicals. The consumer segment focuses on the production of consumer products such as paint, coatings, and caulks for the DIY and professional markets.

RPM has a global presence with operations in over 150 countries and more than 15,000 employees worldwide. The company has a strong commitment to sustainability and has implemented various initiatives to reduce its environmental impact, such as using renewable energy sources, reducing waste and emissions, and promoting sustainable practices throughout its supply chain.

{kind=link}

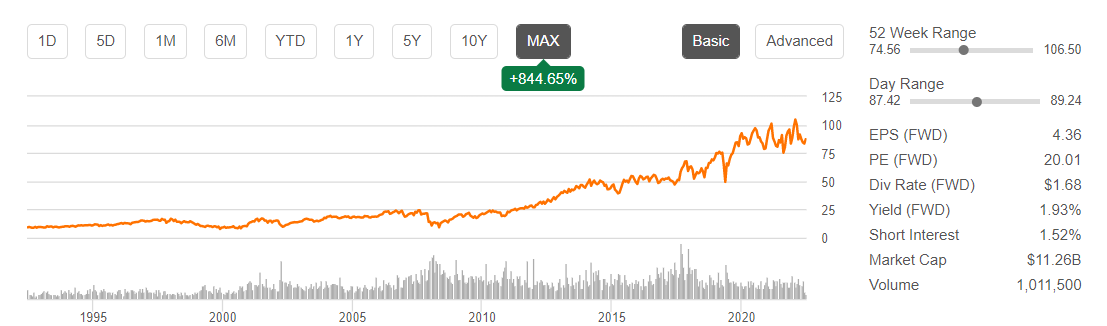

With a market capitalization of $11.7 billion, a growing ROIC of 11.62%, a 52-week high of $106.50, and a low of $74.56, a price of $88.35 with a 21.44 P/E displays effortless growth potential may be available at a significant markdown.

RPM also pays a healthy dividend of 1.88% representing a safe payout ratio of 39.33% giving them ample room in FCF to execute their CapEx plans to create connections within their operating model and innovate upon products. The company has also bought back a small number of shares which I believe is positive as RPM is reaching value territory and purchasing such shares could create value for shareholders and put excess FCF to use.

{kind=link}

With Q2 2023 results exceeding expectations on EPS with a 0.04% beat ($1.10 compared to $1.10) but a 1.14% miss on revenue ($3.46 billion compared to $3.53 billion), RPM is demonstrating mixed results which might be due to macroeconomic headwinds, specifically a possible housing slowdown which impacts their core business model. Nevertheless, RSG still achieved a 9.3% growth in net sales YOY displaying that even with a rough quarter, the company continues to excel within its industry and use its high ROIC to compound its growth. Even with such headwinds, the company expects to grow at low single-digit values displaying slight resilience in tough times.

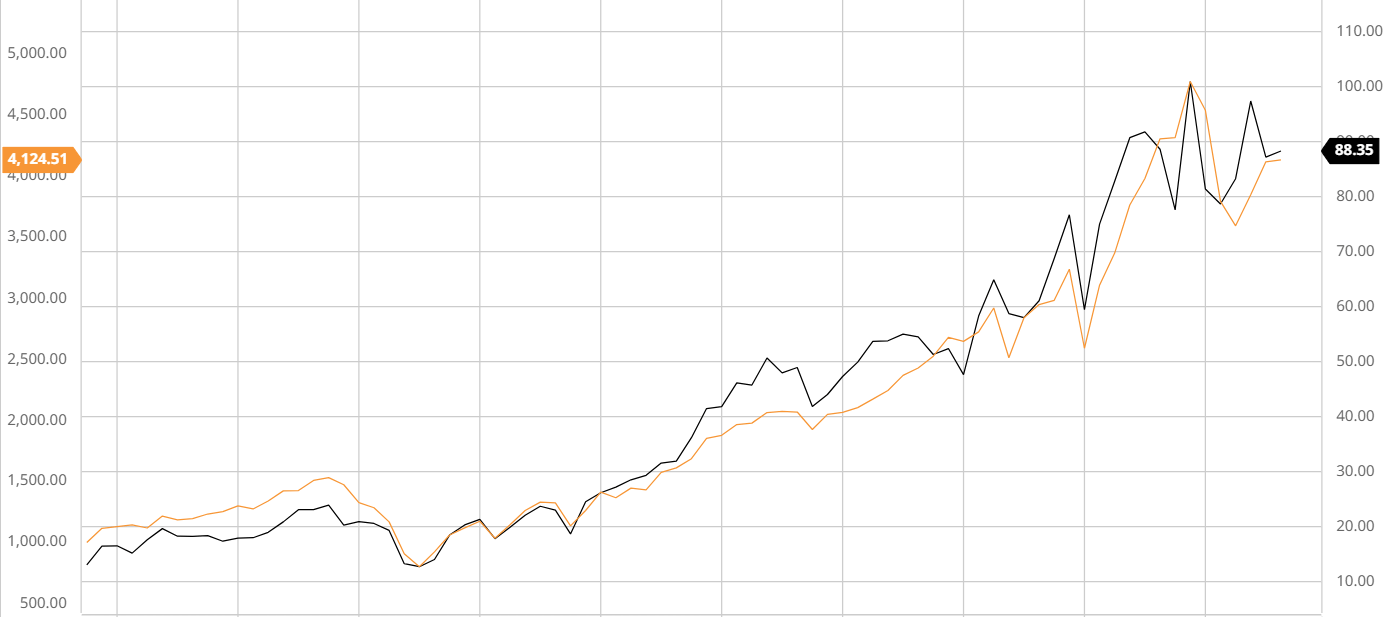

In-Line Performance with the Broader Market

RPM's continuous reinvestment of FCFs into its core business model along with its strong ROIC has allowed the company to compound its growth and achieve recurring revenues. This allowed RPM to maintain an in-line performance with the S&P 500 even during times when housing is a segment that experienced a pullback.

{kind=link}

Offsetting the Housing Pullback Through Growth in Construction Supply Segment

Over the last 30 years, RPM International has made over 175 acquisitions with 60 being in the last decade. RPM has made eight acquisitions in 2022 with many being to further integrate their core business model and also expand to new geographies and increase their brand recognition and reputation across the globe. One key acquisition in 2022 that RPM International made was Pure Air Control Services, Inc. Such a purchase allowed RPM to expand its vertical integration when it comes to its building supplies segment as they are now able to install and inspect HVAC systems. Such acquisitions are all part of RPM's plan to become a one-stop shop for customers creating great value for their other segments.

{kind=link}

This acquisition along with others can also preserve sales even if the housing pullback continues. With declines in the construction segment, RPM is using its strong FCF to purchase companies in weakness and integrate them into their overall business to boost the struggling construction segment and generate compounded growth for the long term.

{kind=link}

Analyst Consensus

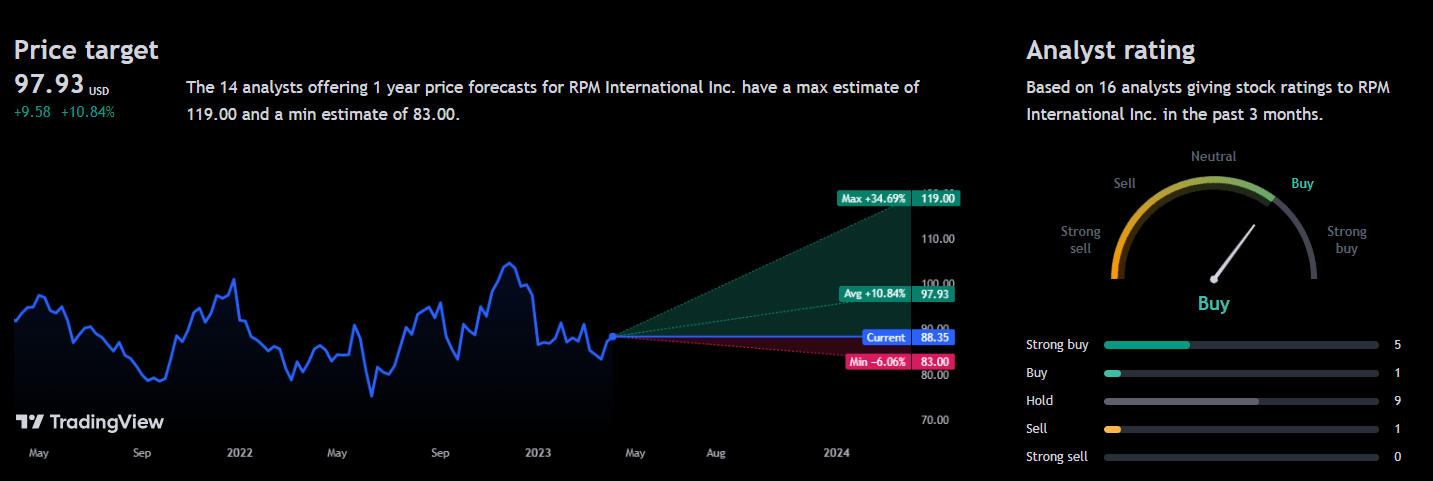

Analyst consensus rates RPM International as a "buy" as it is reaching value territory. With an average 1Y upside of 10.84% at $97.93, it demonstrates that analysts also realize the growth potential RPM has in the long-run.

{kind=link}

Valuation

Before creating my assumptions and calculating my DCF, I will calculate the Cost of Equity and WACC for RPM International using the Capital Asset Pricing Model. Factoring in a risk-free rate of 3.42%, I was able to conclude that the Cost of Equity was 8.05% as displayed below.

Cost of Equity Calculation (Created by author using Alpha Spread)

Assuming this Cost of Equity value, I was able to calculate the WACC to be 7.04% as shown below, which is under the industry average of 11.39% .

WACC Calculation (Created by author using Alpha Spread)

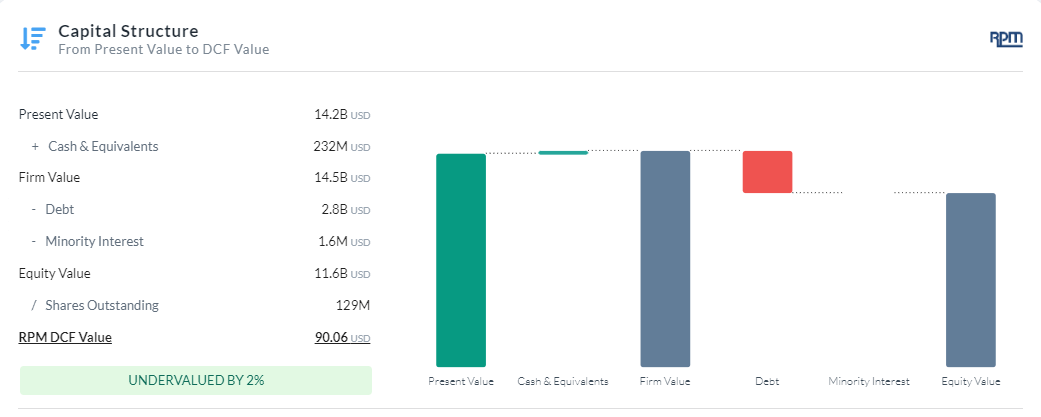

After performing a Firm Model DCF analysis using FCFF, I have determined that RPM International is currently undervalued by 2% with a fair value of approximately $90.06. To arrive at this conclusion, I utilized a discount rate of 7.04% over a 5-year period. Additionally, I estimated a low-single-digit growth rate for revenue beyond 2023 due to the company's expansion into new markets and increased revenue in existing ones. I also predicted that RPM International will continue to improve its operations by acquiring more efficient assets, resulting in a gradual increase in operating margin over time, as shown in my DCF analysis.

RPM Capital Structure (Created by author using Alpha Spread)

{kind=link}

{kind=link}

Risks

Potential Macroeconomic Headwinds: RPM International may face a decline in revenue due to the potential recession in the next 12 months, as the housing market possibly continues to decline. With such a decline, there would be a decrease in construction projects and subsequently housing upgrades which RPM provides. This trend may be exacerbated by high inflation and rising rates, which could weaken buyer power.

Integration and Expansionary Issues: The company has set high expectations for itself to continue its successful strategy of making strong acquisitions, which have led to improved performance in recent years. However, if the company slows down on acquisitions due to few options and focuses on innovating existing segments using FCF, it may experience stagnant growth for several years.

Conclusion

To summarize, RPM International is a strong company with great prospects for growth in existing segments and new geographic areas as well. With a healthy dividend and slight share buybacks along with a slightly undervalued price, a buy rating best suits the stock as I think it will yield long-term success.

For further details see:

RPM: Integration Should Offset Housing Pullback And Foster Growth