RPM - RPM International: Put This Wealth Compounder On Your Radar

2023-12-28 08:10:00 ET

Summary

- RPM International is a materials conglomerate with a strong track record of growth and profitability.

- The company's diverse portfolio of market-leading brands and its scale contribute to its success.

- RPM is well-positioned to benefit from global trends such as infrastructure spending and the reshoring of manufacturing.

There’s value to be had in following under-the-radar names that have strong dividend growth track records. These companies may not be “sexy” like Microsoft ( MSFT ) and NVIDIA ( NVDA ) but have a number of growth catalysts in their own right that should propel them in the near to medium term.

Such may be the case with RPM International ( RPM ), which has 50 years of dividend growth under its belt, and provides products and services that work behind the scenes in driving the economy and the world around us. In this article, I highlight its operating fundamentals, outlook, and discuss why RPM may be a potentially solid pick for strong total returns at the right price, so let’s get started!

Why RPM?

RPM International is an industrial conglomerate that owns a number of leading products in specialty coatings, sealants, building materials, and related services. Its diverse portfolio of market-leading brands may be familiar to contractors and do-it-yourself consumers who frequent Home Depot ( HD ) or Lowe’s ( LOW ). They include Rust-Oleum, DAP, Zinsser, Varathane, DayGlo, and Legend Brands, among others.

While RPM itself may not be a household name, with just 9,700 followers on Seeking Alpha, the scale and its enterprise, brand recognition of its products, and growing business has produced a total return that’s strongly rivaled that of the S&P 500 ( SPY ). As shown below, RPM has produced a 235% total return over the past 10 years, surpassing the 209% return of the S&P 500.

{kind=link}

One of the key drivers for RPM’s growth is its scale, enabling efficiencies and higher profitability. This is reflected by RPM’s B+ grade for profitability with a trailing 12-month Gross Margin of 39%, sitting ahead of the 28% median for the materials sector, and a TTM return on total capital of 9.7%, sitting ahead of the 5.6% sector median.

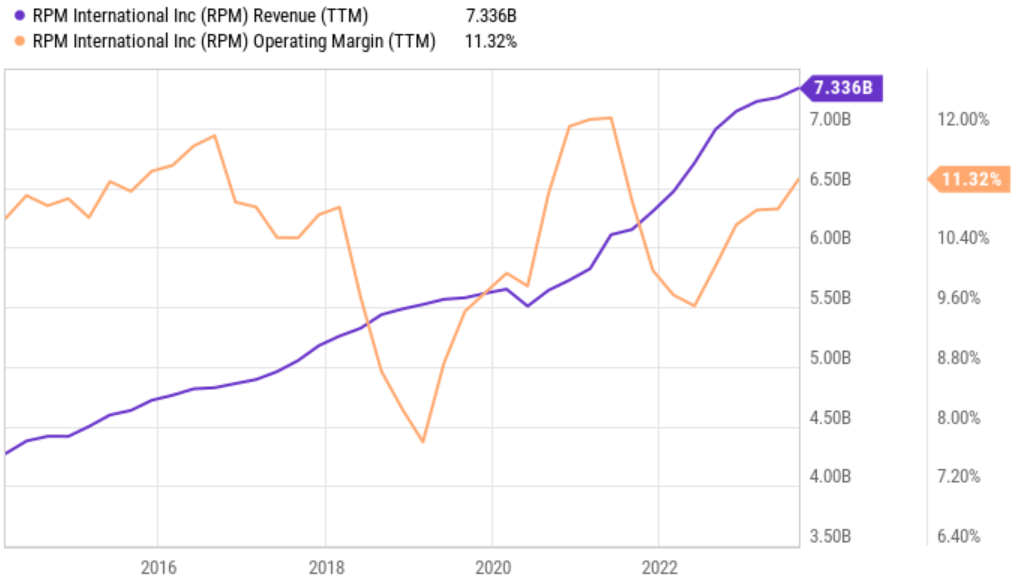

Meanwhile, RPM has demonstrated strong results with record fiscal first quarter revenue of $2.0 billion, rising 4.1% over the prior year period. Operating efficiencies contributed to faster bottom line growth, with adjusted EPS and EBIT rising by 11.6% and 12.3% YoY, respectively. RPM also generated record first quarter operating cash flow of $359 million. As shown below, RPM had a fairly successful track record of growing its revenue from $4.3 billion to $7.3 billion over the past 10 years, all while maintaining a slightly higher operating margin (albeit sometimes volatile) than a decade ago.

{kind=link}

Importantly, RPM is demonstrating pricing power as price increases contribute to revenue and bottom line growth. In addition, RPM is a beneficiary of the infrastructure bill as increased spending on projects around the U.S. including waterways, roads, bridges, and rails undoubtedly results in higher demand for RPM’s products. Other contributing factors include reshoring of manufacturing and double-digit growth in Latin America, Africa/Middle East, and Europe driven by continued demand for infrastructure projects and construction.

Looking ahead to fiscal Q2 results and beyond, I see no signs of RPM slowing down, as it's well positioned to take advantage of global growth trends, including highway/bridge construction, airport expansion, continued onshoring of manufacturing, and infrastructure projects such as the Gare du Nord train station in Paris ahead of the 2024 Olympics.

Other promising initiatives include RPM’s MAP 2025 , an operational improvement plan that’s designed to accelerate growth and increase efficiencies while working toward $8.5 billion in revenue (an increase of 16% from the current level) and 42% gross margin (an increase of 300 bps from present) by the middle of 2025. Some of RPM’s recent innovations such as Nudura soundproofing building material and TremPro’s multipurpose adhesive and sealant are examples of RPM’s track record of R&D innovation to drive top-line growth. At the same time, supply chain swings over the past couple of years have driven RPM to be more agile and efficient with its inventory processes, which are aimed at driving gross margin improvement.

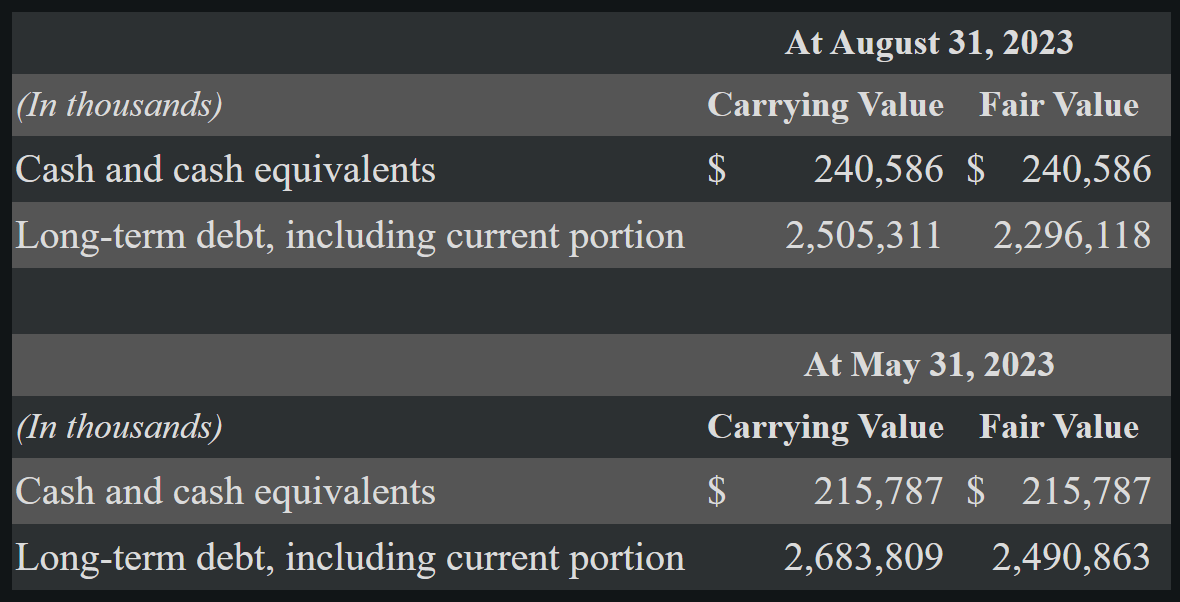

Meanwhile, RPM is reasonably levered with a 2.7x net debt to EBITDA ratio, sitting under the 3.0x level generally considered to be safe by ratings agencies, and it has a BBB investment grade credit rating from S&P. Management would be wise to pay down debt at present, considering the higher interest rate environment, which has reduced the fair value of its debt. As shown below, RPM’s long-term debt traded at 92 cents on the dollar (based on $2,296K fair value divided by $2,505K carrying value) as of the last quarter’s close, which means that RPM could repurchase its debt at an 8% discount.

{kind=link}

While the dividend yield of 1.6% isn’t particularly high, it is well-covered by a 38% payout ratio and comes with a respectable 5-year dividend CAGR of 12.4%. This compares favorably to the S&P 500’s 1.4% yield and 5-year CAGR dividend CAGR of just 5.4% . RPM’s payout ratio also leaves plenty of retained capital for bolt-on acquisitions as an external growth driver. Over the past 30 years, RPM has made 175 such acquisitions.

Risks to the thesis include potential for higher-than-expected inflation, which could result in higher interest rates and consumer pressure in the home building and improvement market. Higher interest rates could also pressure government budgets, leading to a lower inclination to pursue capital-intensive projects that consume RPM’s materials. Plus, higher competition and wage inflation could lead to margin pressure.

Turning to valuation, I believe RPM is fairly valued at the present price of $112.70 with forward PE of 22.6. With the current valuation sitting higher than the normal PE of 20.8 over the past 10 years, I believe near-term catalysts such as the Infrastructure Bill and global tailwinds are currently priced into the stock. Analysts expect 13% to 14% annual EPS growth over the next 2 years, and I believe patient value investors would do well to wait for a 10% discount from the current price, resulting in a forward PE close to 20x, which I believe would be a fair valuation considering all the above.

{kind=link}

Investor Takeaway

Overall, RPM International has a strong track record of growth and profitability, with a well-diversified portfolio of businesses that are poised to benefit from global trends such as infrastructure spending and reshoring of manufacturing. The company's recent initiatives, such as MAP 2025 and focus on R&D innovation, position it for continued success in the future.

However, it seems that most of the near to medium-term catalysts are fully baked into the price, making the stock fairly valued. As such, value investors may do well to wait for a share price downturn due to a potential upcoming earnings surprise or negative overall market sentiment before buying. As such, I rate the stock as a 'Hold' that’s well worth putting on the watchlist.

For further details see:

RPM International: Put This Wealth Compounder On Your Radar