RTX - RTX Corporation: Short-Term Pain Long-Term Gain

2023-11-26 08:35:36 ET

Summary

- I view RTX as an excellent play on structural tailwinds in the aerospace and defense industries, given favorable outlooks for volume and mix in both markets.

- Backlog development has accelerated recently with peer leading >10% YoY growth since Q4 '22 and a current sales coverage of 2.6 years for RTX and 3.9 years for commercial aerospace.

- Issues in Pratt & Whitney’s GTF engine have induced a sell-off in shares, mostly driven by multiple contraction, with the stock currently trading 21% below 3Y average forward P/E.

- While acknowledging the possibility of further near-term multiple depression due to the GTF issues, I view current levels as an attractive entry point due to upward skewed risk/reward for long-term holders.

- Based on a DCF analysis and a risk-adjusted FY23 EV/EBITDA multiple, I estimate a fair value per share of $104 and initiate RTX stock at Buy.

[Note: All RTX-stated projections are from Investor Day June 2023]

Company Overview

RTX Corporation ( RTX ), formerly known as Raytheon Technologies is an Arlington, Virginia-headquartered Aerospace & Defense company formed in 2020 through the merger of United Technologies and Raytheon employing more than 180,000 people as of 2022. The company operates as an industrial conglomerate across three roughly equal size segments which mainly serve the aerospace and defense industries with an exposure to both civil and military end markets.

Collins Aerospace - $23bn of FY22 sales

Collins Aerospace manufactures and sells aircraft equipment ranging from avionics over aerostructures to mission systems with c.$160bn of Collins products installed on more than 110k aircraft as of FY22. The segment offers its solutions to both civil (63%) and military (37%) customers with 20% of sales allocated to the large commercial aircraft duopoly of Boeing and Airbus. Next to original equipment (58% of FY22 sales), Collins also provides customers with spare and replacement parts and offers training solutions for pilots and general aviation purposes (42% of FY22 sales). Due to the fragmented nature of the aerospace equipment industry Collins has a wide range of peers ranging from SMEs to listed US and international suppliers with the most notable ones being Safran ( SAFRF ) and Honeywell's avionics ( HON ) business as well as aeroframe manufacturers Howmet ( HWM ) and TransDigm ( TDG ).

Pratt & Whitney - $21bn of FY22 sales

Pratt & Whitney primarily manufactures jet engines for civil and military purposes as well as spare parts used to service sold products over their lifetime with 85k engines currently in service. Additionally it provides maintenance, repair and overhaul ("MRO") to its customers. While the business is primarily known for its engines deployed among large commercial aircraft (including the Geared Turbofan "GTF" engine), through subsidiary P&W Canada it also the global leader in smaller jet and turboprop engines for regional aircraft. As of FY22, Airbus is Pratt's largest customer with 33% of revenue given the role of its GTF engine in the ongoing Airbus neo program with the GFT one of the engines chosen to power the highly in-demand A320neo. Other significant customers include the US military industrial complex with P&W engines as sole current choice for the 5th generation fighter program which includes the Lockheed Martin F35. Key competitors include GE Aerospace ( GE ) as well as European engine manufacturers Safran and Rolls-Royce ( RYCEY ).

Raytheon - $25bn of FY22 sales

Raytheon operates as one of the US prime defense contractors, offering solutions across a wide range of military purposes including missiles, radars and intelligence with key products such as the Patriot missile defense system and the Tomahawk cruise missile. The segment has been created in Q3 23 from merging the Raytheon Intelligence & Space and Raytheon Missiles & Defense segments and transfering the mission systems product line to Collins. Next to US government agencies Raytheon also generates a significant portion of sales (26%) from international US-allied militaries. Key competitors are the major US prime defense contractors Lockheed Martin ( LMT ), Northrop Grumman ( NOC ) and General Dynamics ( GD ) ("defense peers").

Key Investment Thesis

Well positioned to capture structural Recovery in commercial Aerospace with growing Share of High-Margin Aftermarket Business

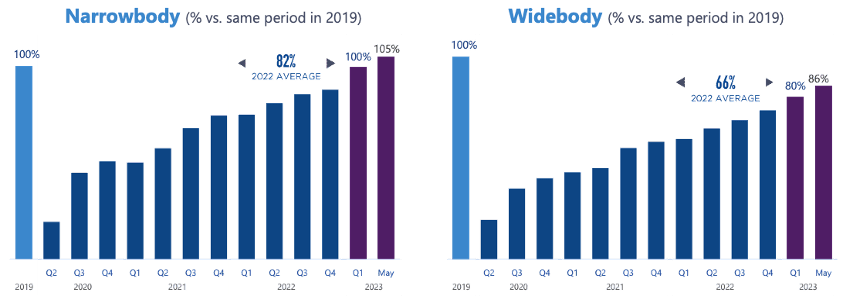

I see RTX in a highly favorable position to leverage its best-in-class footprint in both general aerospace and propulsion to profit from the growing aerospace demand and structural recovery of the sector over the coming years. The amount of narrowbody aircraft in service (which includes the likes of the A320 and B737) has already reached pre-Covid levels in early 2023 with the Widebody segment (such as the A350 and the B787) expected to surpass pre-Covid levels from 2024-2025.

{kind=link}

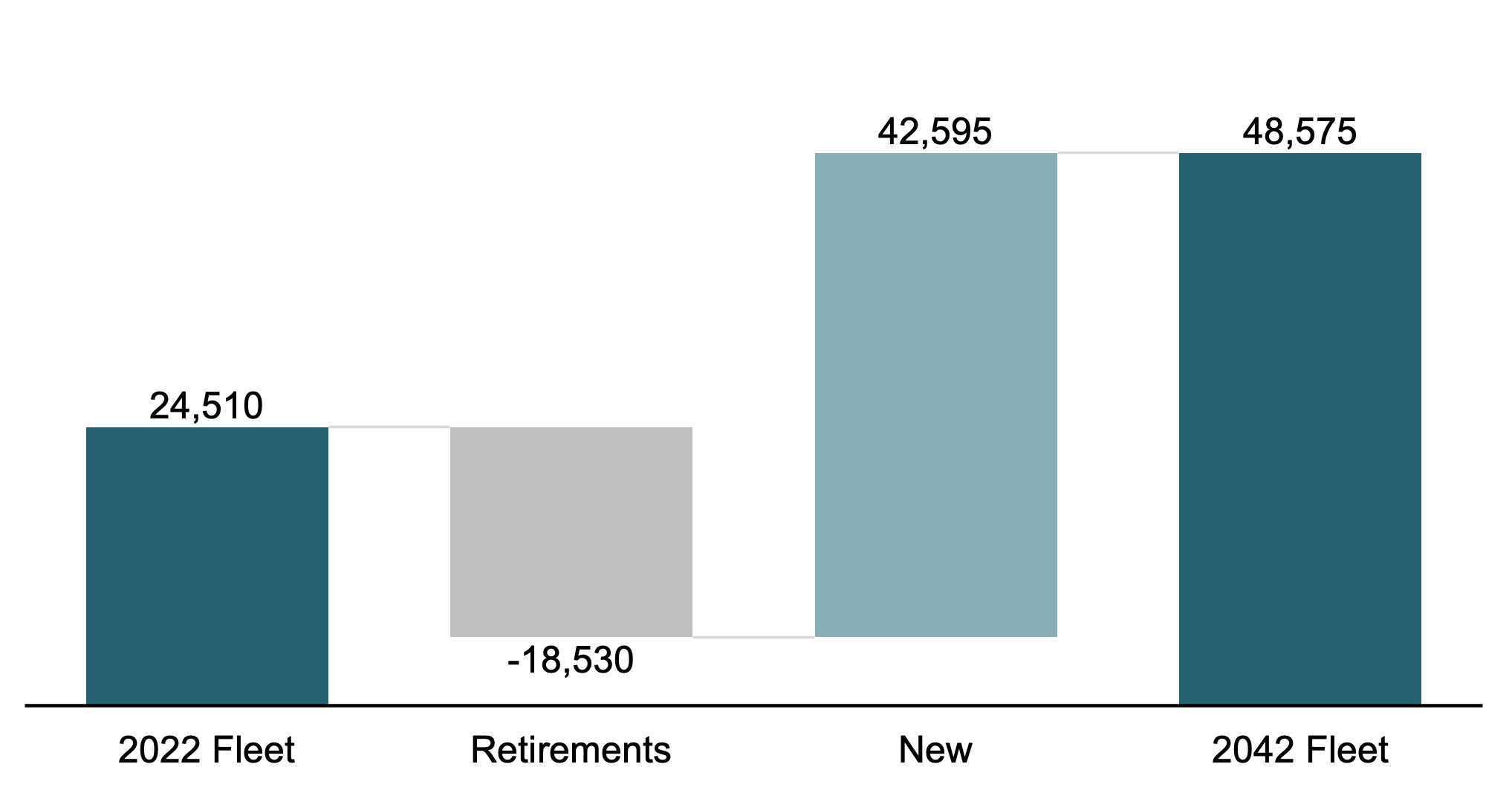

Going forward, industry analysis from both Boeing and Airbus anticipates the demand for commercial aviation to further rise with Boeing expecting c.43k new aircraft to the added to global fleets through 2042, the majority of which (c.3/4) comprised of narrowbody jets. With most of the growth anticipated to come from Asia and intra-Chinese travel expected to overtake intra-US and intra-European demand over the period, those smaller and cheaper jets are poised to capture an even greater share of the market in the future. Another key driver of narrowbody growth is the continuing rise of low-cost-carriers such as Ryanair and Wizz Air in Europe and Southwest and JetBlue in the US which tend to operate almost exclusively narrowbody fleets on shorter and more frequent flights. Overall, fleets are expected to grow at a 20-year CAGR of c.3.5% over the period.

20 Year Fleet Forecast (Boeing CMO 2022)

{kind=link}

With an increasing amount of supporting equipment in avionics and other systems on board (2x value of content on current gen vs prior gen aircraft expected by RTX) and the premier role P&W's GTF engine plays in powering the A320neo, the highest market share narrowbody jet with a current order backlog of 7.2k, I estimate this structural development to be highly favorable for RTX in providing ample growth opportunities in OE.

While OE sales might be the more visible business from an outside perspective, arguably the even more important driver for RTX in the aerospace business is the continued growth of aftermarket sales in both products and services. With c.$160bn worth of Collins equipment in service and more than 85k P&W engines across both commercial and military, RTX has a massive installed base which it can leverage to grow its higher margin and less volatility aftermarket business in what is the textbook example of a razor/razorblade business model. Through a mix of higher pricing power in exclusively sourced spare parts and provision of MRO services, McKinsey expects aerospace aftermarket sales to have at least double the profitability of OE.

Through the almost shutdown of commercial aviation and subsequent grounding of large parts of the global aircraft fleet during the Covid-19 pandemic, the post-Covid recovery has seen a surge in demand for aftermarket products, specifically spare and replacement parts, due to Covid-era under-maintenance. With supply chain and labor shortage issues, deliveries of new aircraft have also been subdued in recent years leading to a significant aging in aircraft fleets. While this is expected to normalize in mature regions such as the US and Europe which have already operated with on average older fleets prior to Covid, the trend is expected to continue in higher growth regions including China and the broader Asia Pacific region. Next to providing the OE manufacturer with a longer timeframe for general aftermarket coverage, this also increases the total flight hours engines and parts will be exposed to after their warranty period has ended with RTX expecting an 8% CAGR for out-of-warranty flight hours from 2022 to 2027.

Average Fleet Age by Region (Statista)

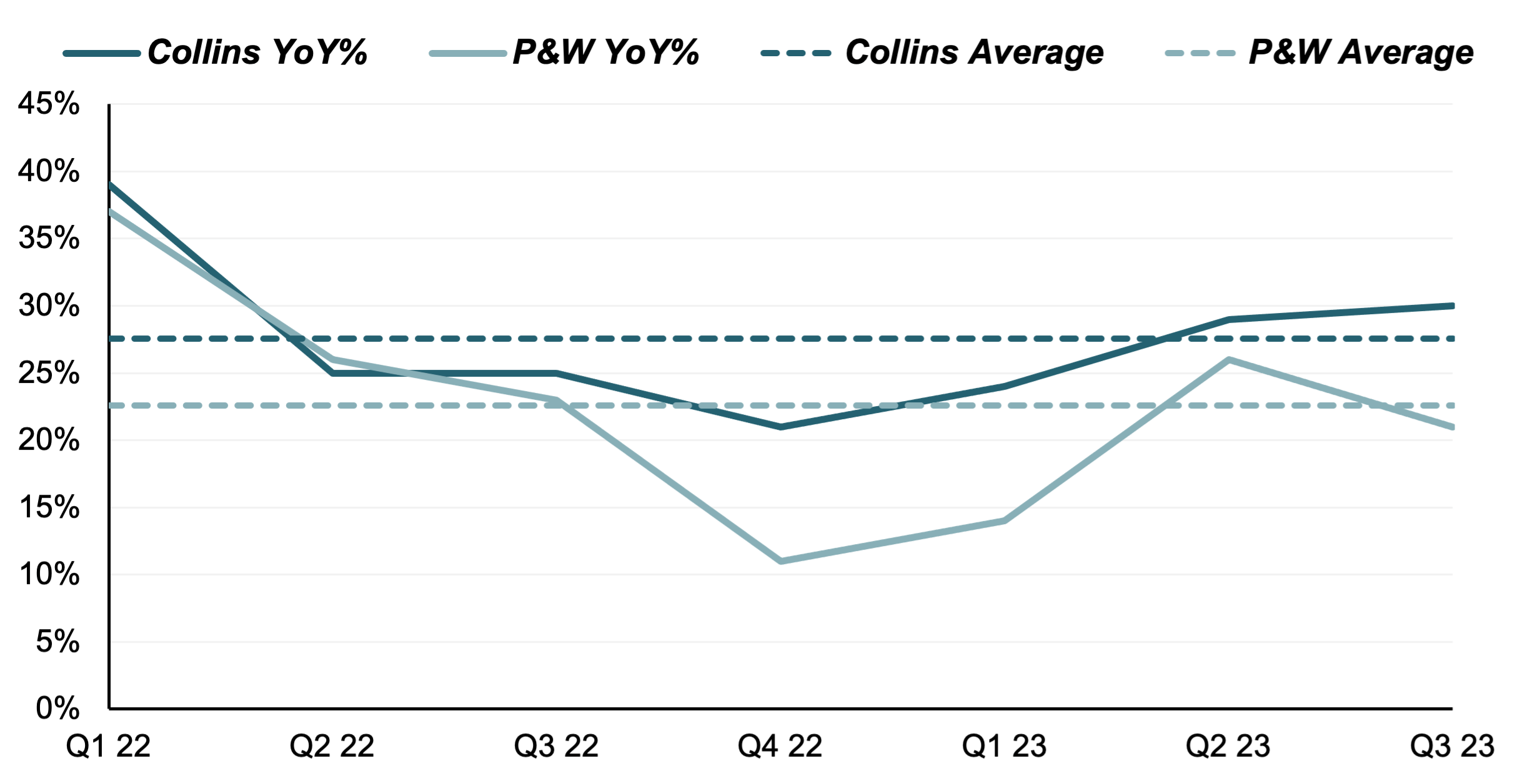

The impact of this structural shift in the industry becomes evident when looking at YoY growth rates for the respective aftermarket businesses of both Collins and P&W. Since FY21, aftermarket sales in both segments have grown on average in the high 20s (Collins) and the low 20s (Pratt), strongly outperforming the wider segments and RTX as a whole.

Quarterly Aftermarket YoY Growth (Company Filings)

{kind=link}

Going forward I estimate Pratt and Whitney in particular to further drive this shift towards aftermarket as its leverages its large installed base in its mature programs including P&W Canada small engines and the V2500. Coupled with further rollout of the GTF program this will have a compounding effect on growth in parts volumes and MRO shop visits in the coming years. With over 3k GTF engines currently in service and an order book of around 10k, RTX estimates shop visits for its new generation programs to grow at a CAGR of 26% through 2025, which together with c.6% for its mature programs puts Pratt & Whitney total shop visits at an anticipated CAGR of 9%. Using the GE/Safran Joint Venture manufactured CFM engine as a proxy due to its largely similar application on twin engine narrowbody jets, I estimate aftermarket sales growth for the GTF to average LDD-MDD in the long run which, together with stable aftermarket demand for Pratt's mature engines, should become a large part of the segments future potential once early issues have been resolved.

Aftermarket YoY Growth for Safran/GE CFM Engine (Safran SA)

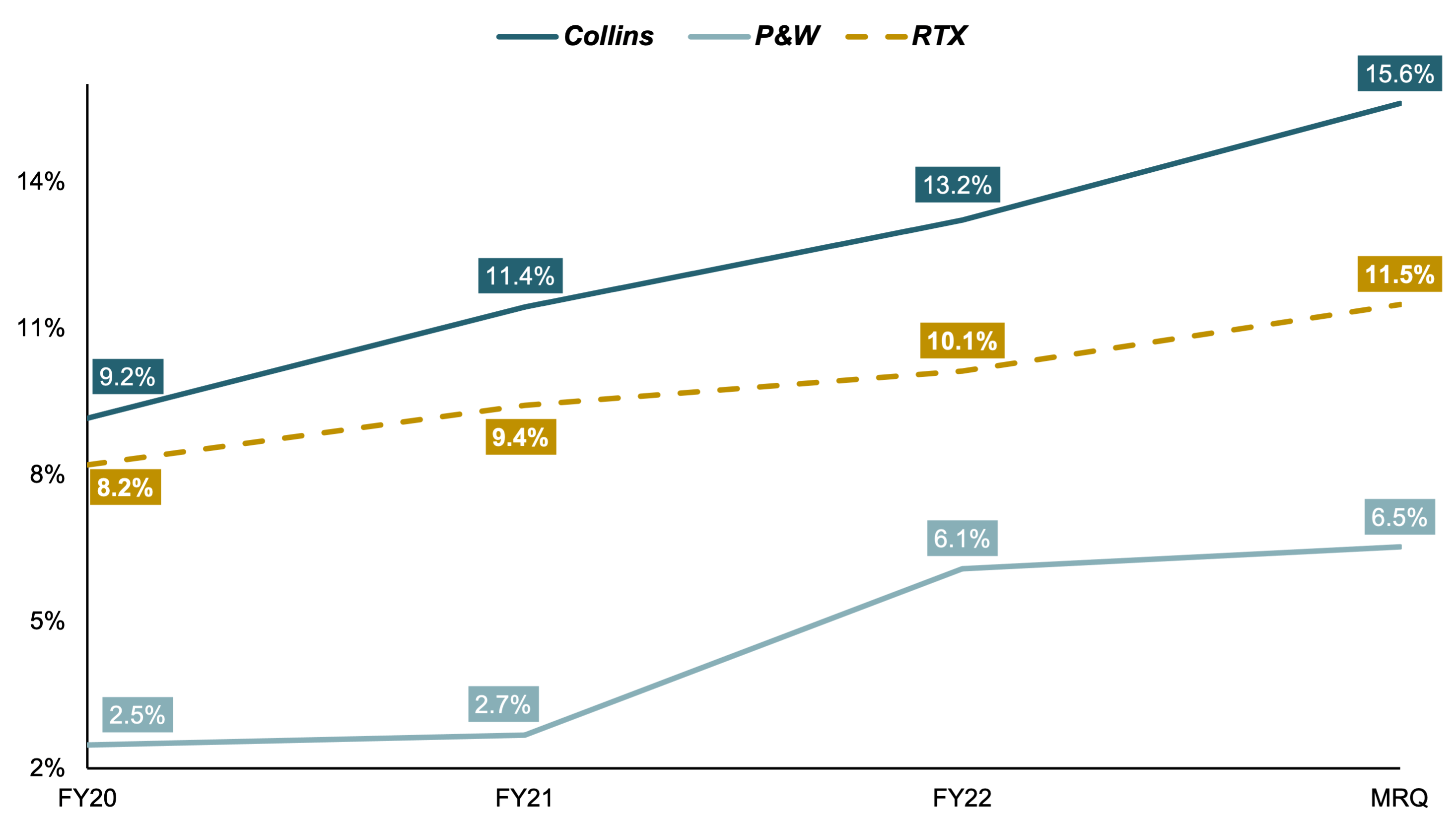

While RTX does not break up its segment sales into OE and aftermarket on a regular basis in their financials, using YoY growth rates for commercial OE and aftermarket provided in RTX quarterly reported I estimate the share of aftermarket of total commercial aerospace sales having grown up to 10 percentage points from FY19 to FY22. Given on average double the gross margins achieved in aftermarket sales vs OE as indicated by McKinsey, RTX' aerospace business has recorded a strong growth in profitability since FY20 with Collins margins expanding from below 10% as of FY20 to more than 15% in Q3 23 and Pratt profitability more than doubling from 2.5% to 6.5%. Riding the wave of strong aftermarket demand and recovery in OE volumes this development can be expected to continue into the next years with RTX management guiding for mix/volume attributable margin expansion of c.300bps for Collins and c.225bps for P&W through FY25. Regarding P&W, the GTF engine broke even in profitability in FY22 and is expected to achieve 10x FY22 levels by FY25, reaching MDD aftermarket profitability which is further projected to increase throughout the decade as the engine matures and the GTF Advantage version rolls out.

RTX Aerospace Business Margin Development (Company Filings)

{kind=link}

Defense Portfolio to benefit from geopolitically driven Demand Growth and Transition to next Generation Technologies

Regarding RTX' defense business, most of the key drivers behind its future potential have been already discussed by me more in depth in my article on LHX . In short, the war in Ukraine and the recent breakout of violence between Israel and Hamas have greatly increased global threat perception to levels we might not have seen since the early 2000s or perhaps even the Cold War. Coupled with the threat of a Chinese invasion of Taiwan and continued Chinese land grabs in the South China Sea, this will provide a clear tailwind for global defense spending to rise in the coming years and potentially decades. The war in Ukraine specifically has proven to be a catalyst for US-allied European and other NATO states to rethink their overreliance on US military protection with an array of new funds promised to increase national security including the announcement of a massive €100bn allocated to the German Bundeswehr . I estimate this development to further increase the share of international revenues in RTX defense business (26% as of FY22) which have historically provided higher margins and can thus be expected to not only grow the top line but also deliver an expansion in margin. This is already visible in the company's military backlog (as of FY22) which c.35% of backlog allocated to international US-allied armed forces thus providing a clear runway for growth towards and beyond management's target of c.33% international sales by 2025.

The Ukraine conflict also saw the highly successful use of some of RTX' most renown products including the Patriot Missile Defense systems and can thus be expected to create additional visibility on its effectiveness while the F-35 joint strike fighter, for which Pratt and Whitney's manufactures the sole sourced engine with the F135, continues to see ever increasing demand with recent orders from the US , Czechia and Canada .

With those key drivers for its existing portfolio in place and a growing share of new generation technology including but not limited to next generation PhantomStrike airborne radars, the LTAMDS aerial defense radar systems and hypersonic cruise missile family HACM, scheduled to enter service from 2024 (2026 for HACM), I see RTX in an excellent position to grow its defense business sustainably and profitably in the coming years. Through greater volumes I also expect production utilization in the Raytheon segment to tick up from 43% as of FY22 to management's target of c.50% in FY25 which should further benefit margins.

With the recent transfer of the unit from Raytheon Intelligence & Space, through Collins RTX also offers a wide array of solutions in the high-growth fields of C5ISR and connected battlespace including a leading platform in JADC2 (Joint All-Domain Command and Control) which, on itself, is expected by management to outgrow general defense sales at c.7% CAGR through 2027.

Record high Order Backlog with >2.5 Years of Sales Coverage provides high Earnings Visibility going forward

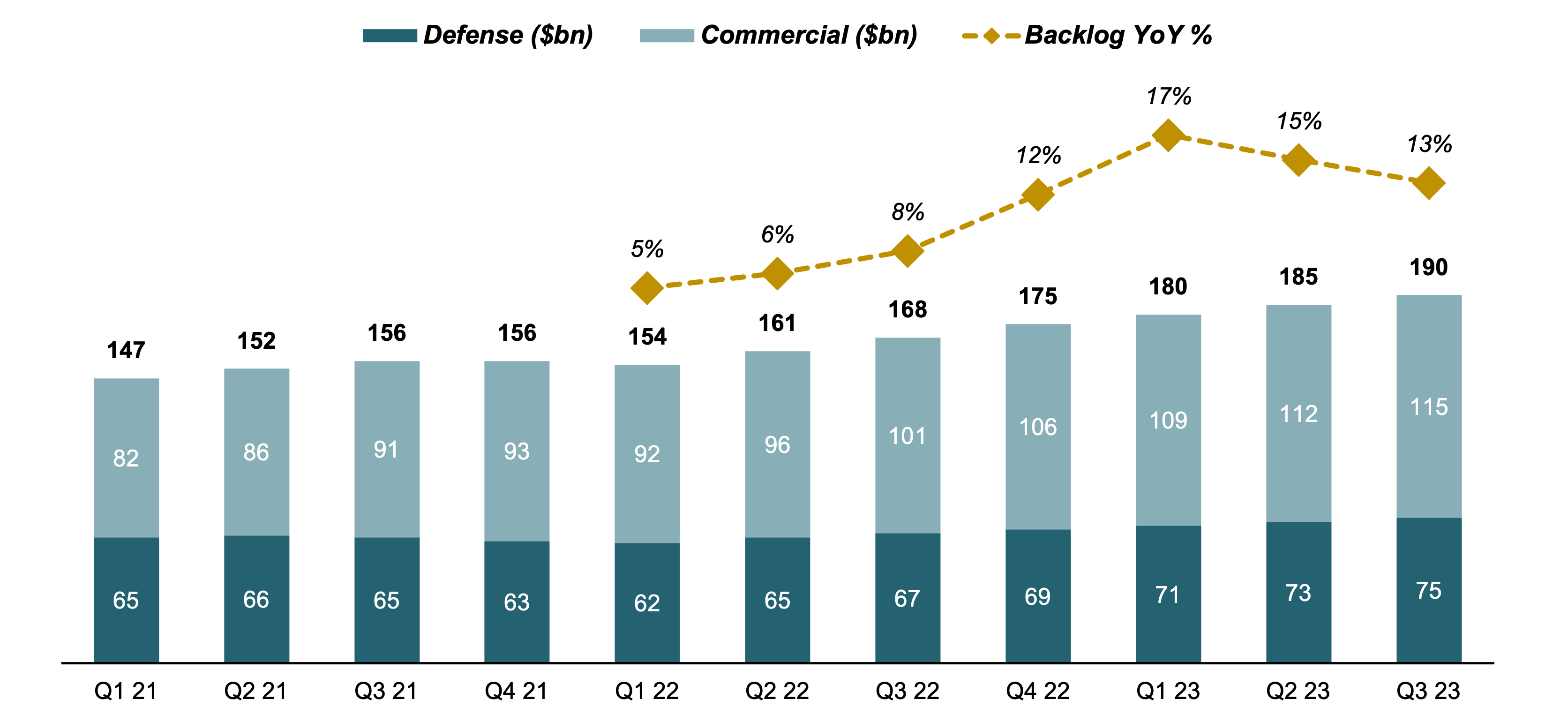

As of Q3 23, total RTX backlog stands at a record high $190bn of which $115bn falls into the commercial and $75bn falls into the defense segment. After a slow FY21, orders have accelerated with YoY backlog growth rates above 10% since Q4 22 driven by exceptionally strong demand in commercial due to aftermarket demand and GTF engine orders in P&W (rolling four quarter average 15.7% YoY). After a largely flat defense backlog for FY21 and FY22, growth has also accelerated recently with a 4 quarter average of c.12%, benefitting from an increase in global threat levels and contract wins with the US and international governments.

Backlog Development (Company Filings)

{kind=link}

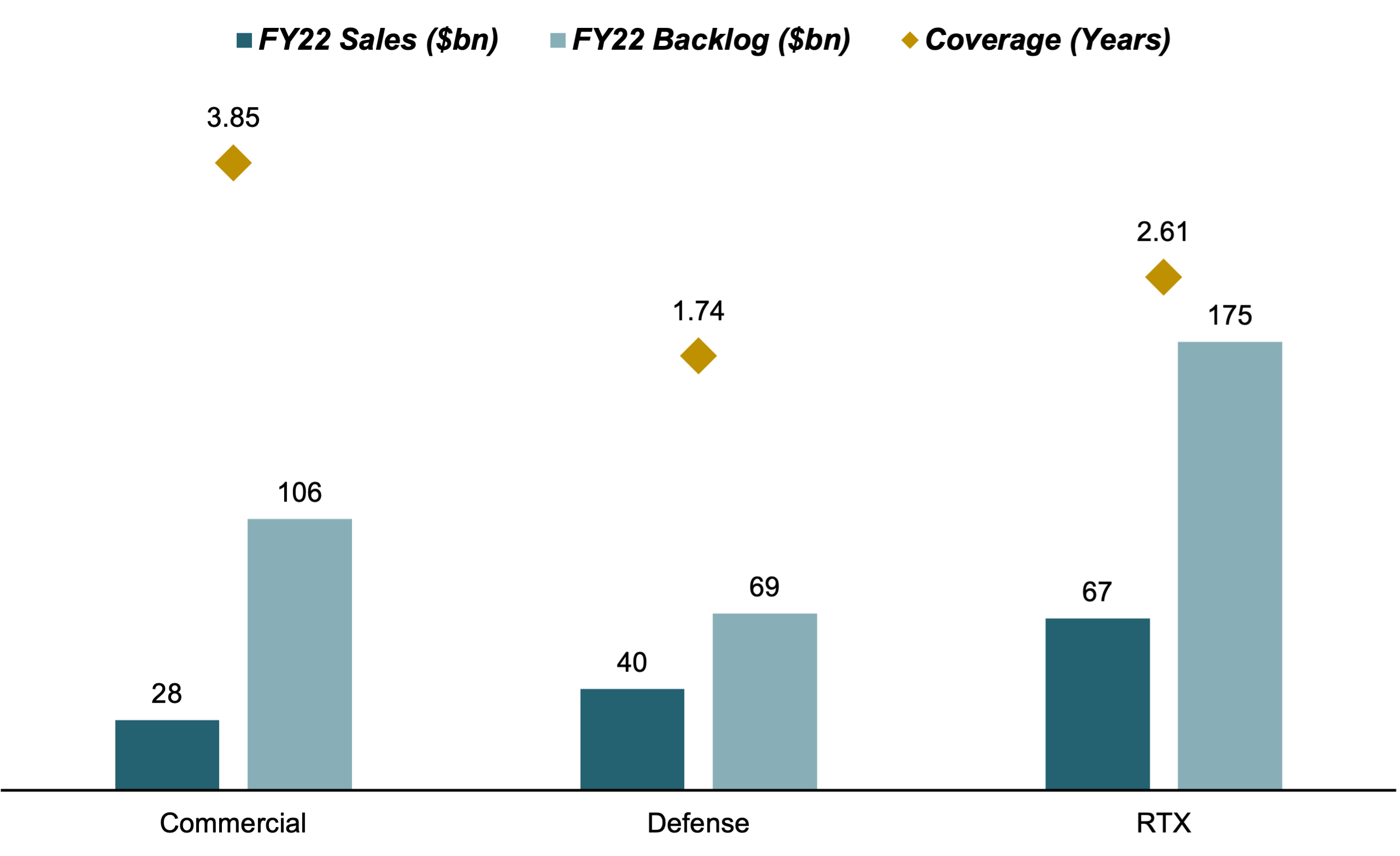

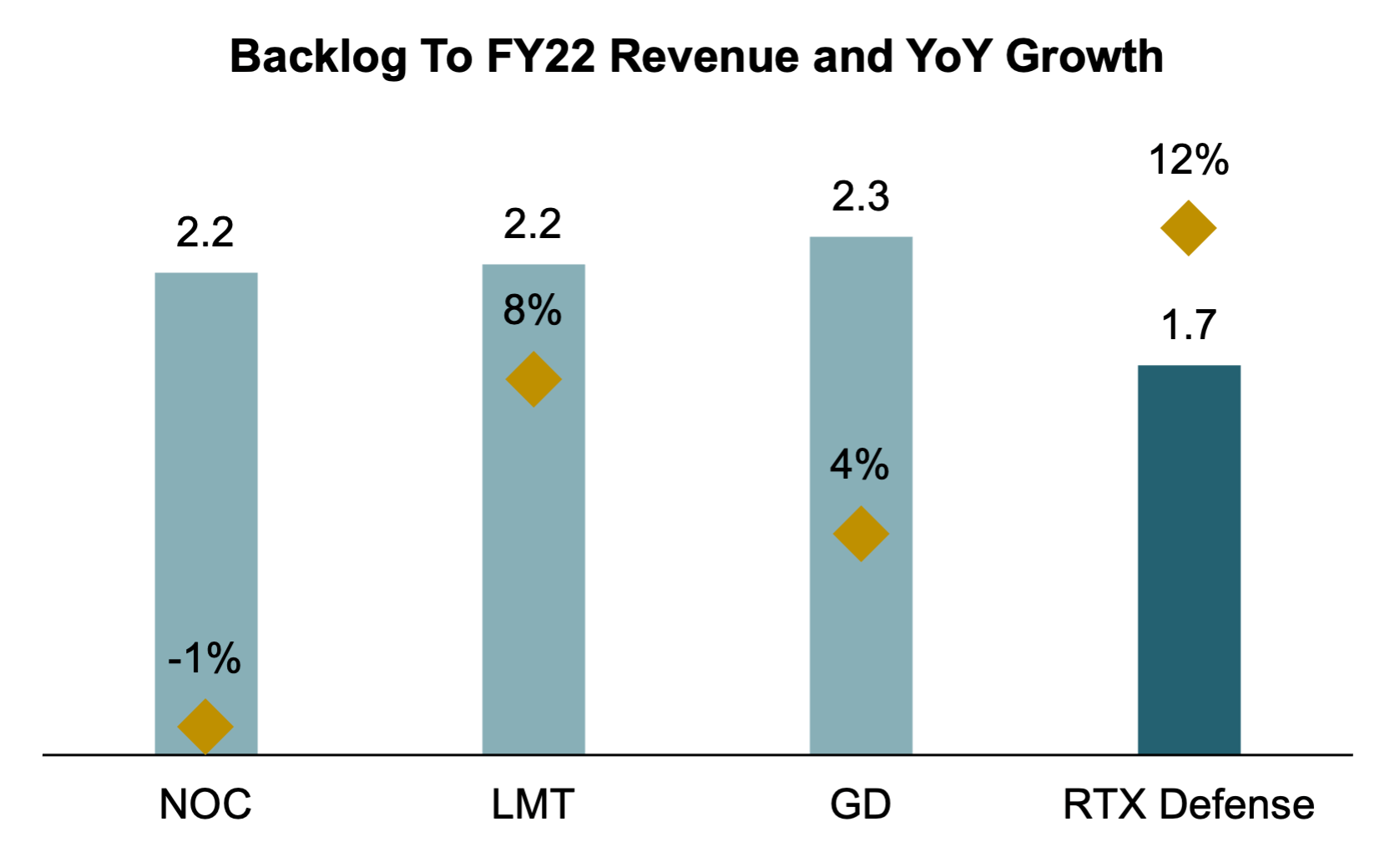

Looking at backlog from a sales cover perspective the exceptionally strong backlog position in commercial becomes even more apparent with a FY22 sales coverage of 3.85 years and 2.61 years on a WholeCo RTX basis. As mentioned before, defense backlog has been somewhat more subdued and with a sales coverage of 1.74 years it remains below company and US defense prime peers (LMT, NOC, GD) average. Compared to peers however, RTX's defense segment shows a higher YoY growth rate and (as explained in my note on LHX ) a lower backlog coverage is to be expected given RTX's platform agnostic and shorter cycle sales nature.

Backlog and Sales Cover by Business Area (Company Filings) Backlog vs Peers (Company Filings)

{kind=link}

{kind=link}

Internal Initiatives and Portfolio Optimization provide additional Upside for Margins going forward

Next to the beneficial effects that above discussed factors should have on margins across the aerospace and defense businesses, RTX is also investing heavily to restructure internal processes and drive efficiency gains across the value chain. As announced during their Investor Day in June 2023 and having come into effect from Q3 23 on, the former two Raytheon segments, Intelligence & Space and Missiles & Defense have been consolidated into one Raytheon segment and transferred the connected battlespace solutions and air traffic management units to Collins (c.$2.7bn in FY22 sales). Through this leaner business structure and better alignment to segment priorities, RTX expects to generate annual savings of $200-300MM and reduce intercompany eliminations by c.$1.4bn as well as generate considerable revenue synergies at Collins.

The company is also expecting to generate considerable savings by growing its capabilities in Industry 4.0 and the incorporation of advanced digital technologies. Investments to increase automation levels to 15.5MM hours by FY27 from 8.5MM FY23e base and the number of connected machines to 20k from 15k as of Q1 23 are projected to drive up to 20% improvement in unit production costs. The third pillar of internal initiatives to expand margins is the continued improvement in internal processes and elimination of redundancies and double competencies which has been ongoing since the initial Raytheon United Technologies merger. During their Investor Day, management recently raised their gross expected cost savings guidance from previously $5.1bn to $6.6bn by FY25 vs FY20 baseline, mainly an effect of mentioned segment realignment and greater expected savings in procurement due to newly launched component sourcing initiatives.

Post-Merger Cost Savings Outlook (Company Filings)

Some Thoughts on Valuation Regarding the GTF Issue

Of course, a key thing that needs to be addressed here is the newly emerged issue in powder metals used in the manufacturing of Pratt's flagship GTF engine. However, given my background which is as far away from material sciences and aerospace engineering as it possibly could, I will not dive into the technicalities here as other authors have done very well in explaining those but rather assess the situation from a purely financial standpoint.

Since the issue became public in July 2023 through its recent lows in October, RTX stock has lost c.28% of its value. However, consensus FY23e (non-GAAP) EPS did barely move from $5.02 to $5.01. In fact almost the entirety of this decline has been driven by multiple contraction with forward P/E multiple dropping from 19.3x (in line with 3Y average of 20.0x) to 13.9x. The stock has recovered somewhat since its October lows, mostly driven by the broader sector following the Israel-Hamas incursion, to currently trade at a forward P/E of 15.9x, still c.21% below 3Y average.

Arguing that, excluding the powder metals issue, RTX should trade at a relative premium to historic valuation given favorable outlook for all of its business segments and accelerating efficiency gains, I find this discount hardly warranted considering management's current outlook on the costs associated with maintenance and airline compensation. RTX currently projects $3bn of net cash headwinds through FY25, assuming an equal distribution of this for FY23, FY24 and FY25 and discounting at company WACC of 8% this yields a NPV of c.$3.2bn accounting for just around 2% of RTX's enterprise value as of July 24th, the day before management first revealed the issue. Of course, there remains the risk of management underestimating the impact of this, both financial and reputational, however I think this largely been priced in already given the currently depressed multiples.

Valuation

I would like to employ a similar approach to value RTX as I have done for LHX by using both a more market related multiple to my projected FY23 EBITDA and a longer-term intrinsic DCF-based method. However, as opposed to basing my price target on the multiple valuation solely, I will calculate a blended price target from both the DCF and the multiple. In doing so I try to balance short-term and long-term outlooks to get a more realistic view on how the company is trading rather than relying on only one angle.

Multiple Valuation

Financial Model as of Q3 23 (Company Filings and Author's Projections)

For Collins I expect FY23 to come in slightly ahead of RTX guidance of LDD to MDD, as continued strength in aftermarket and recovery in OE volumes should drive sales ahead of consensus. Margins should come down slightly from Q3's 15.6% but still ahead of H1 margins at 15%. Going forward I expect Collins' growth to lead the group due to above mentioned factors and the leading position the business has in its markets with FY20-25 CAGR at 7.1%, slightly above the 6-7% target RTX communicated during their latest investor day. Margins expand similarly driven by sales mix and internal initiatives to reach 19% in FY25 and generate a total CAGR in operating profit of 23.9%, in line with forecast of 22-25%.

Pratt & Whitney, despite the current challenges the segment faces due to powder metal issue related to its GTF engine, is also projected to see strong development in both sales and margins going forward. With adjusted sales up MDD for FY23 and a return to growth in FY25 after a more muted FY24, which I expect given the GTF problems, my total estimated FY20-25 CAGR for the segment comes in at the lower end of RTX guidance of 9-10% at 9.2%. While I do expect strong top line development for Pratt, I see more risk in margins at (even when using adjusted figures) the recent issues should have an impact in the near-term with margins in my forecast climbing less than projected to c.8% vs >10% as expected by management during Investor Day.

Lastly, for Raytheon I expect a stable sales growth utilizing the current record order backlog with sales in MSD for FY23 and FY24-25 sales weighted towards FY25 as communicated by management during their most recent Q3 analyst call . On a margin side I expect FY23 to be a trough as supply chain issues have begun to ease and the effect of decreasing inflation on fixed price contracts should lift bottom line considerably. By FY25 I expect margins to be slightly above 12.2% in line with management guidance.

On group level, I forecast total sales growth through FY25 at 8.6%, roughly at midpoint of the company's guidance of 8-9% and operating margin expansion of 544bps slightly below guidance range of 550-650bps vs FY20 base with continued strong growth and execution at Collins offsetting some short-term weaknesses at Pratt and Raytheon. Using a continued ratio of D&A to sales at 6.1%, my model estimates EBITDA growth in the MDD through FY25 with margins expanding to c.16.5%, again largely driven by strong execution in the Collins segment.

Over the past 3 years which cover the period since the Raytheon and United Technologies merger, RTX has traded at an average 13.9x next fiscal year EV/EBITDA multiple. Applying a 10% margin of safety due to the current situation concerning the GTF powder metals issue and the risk of further escalation in costs, I estimate a fair multiple of 12.5x. Applied to my FY23ae EBITDA of $13,607MM I calculate an Enterprise Value of c.$170bn which, adjusted for net debt and minorities yields a fair value of $137bn for RTX equity, or $95 per share.

Multiple Valuation (Company Filings and Author's Projections)

DCF Valuation

Flowing my projected financials through FY25 into a 5-year DCF model, I apply a 6% annual revenue growth for the remainder of the projection period as well as assume a FY27 operating margin of 14%, both of which I think are well achievable given my reasoning laid out above. Keeping a constant percentage of sales at FY22 level for FAS/CAS adjustments (1.3%) and any cash charges (D&A, Pension Income, SBC and Capex) as well as incorporating the currently projected GTF cash headwind of $3bn through FY25. I estimate a total unlevered FCF of $9.1bn for FY25, which on a levered basis, as reported by the company, comes in slightly below management guidance of $7.5bn. Discounting cash flows at 8% WACC (derived from CAPM using current US-10Y rate and a ß of 0.73) and assuming a 2.5% infinite growth rate (long-term US GDP growth assumption adjusted for aerospace above-GDP growth), I estimate an Enterprise Value of $195bn. Adjusting for net debt and minorities this implies a fair Equity Value of $162bn or $113 per share.

DCF Valuation (Company Filings and Author's Projections)

Blending both price targets together weighting multiple valuation and DCF at 50% each, I calculate a fair value per share of $104 implying a 31% upside to current trading levels as of November 24.

Price Target Calculation (Company Filings and Author's Projections)

Wrap-Up and Outlook

Overall, I see RTX as a very attractive long-term play on structural tailwinds in the commercial aerospace and defense industries. Leveraging its best-in-class competitive positioning at Collins and the maturing of the GTF engine should enable RTX' aerospace business to deliver solid and highly visible earnings from aftermarket sales and services for years to come while the global rise in defense spending and the transition to a new generation technologies portfolio will benefit its defense segment.

Based on both cash flows and historical trading levels RTX is clearly undervalued. I do expect this to remain the case in the near term as the GTF issue at Pratt & Whitney with still largely unknown long-term impacts should be powerful enough to create an overhang over the stock. Management also seems to have realized this situation and recently announced an accelerated stock buyback of $10bn, or c.9% of total market cap, which is to be completed in due course, providing investors with some much needed confidence in management being able to contain the situation. Having said this I see the current valuation as offering more than enough margin of safety for investors to start building up their position in the company while profiting from a generous 12% total equity yield from dividends (3% forward yield) and the $10bn accelerated buyback.

For further details see:

RTX Corporation: Short-Term Pain, Long-Term Gain