RWAY - Runway Growth Finance: A Different Kind Of VC-Focused BDC

2023-12-28 16:36:58 ET

Summary

- Runway Growth Finance focuses on providing capital to VC-backed late-stage growth companies that have reached a sufficient level of maturity where it makes sense to avoid equity dilution.

- While RWAY is a VC-focused BDC and currently provides a very high dividend yield of 12.6%, the underlying portfolio and leverage are structured in a very conservative manner.

- In this article, I explain why RWAY is a clear buy for investors, who seek high and stable dividend yield.

Runway Growth Finance ( RWAY ) is a relatively decent sized BDC with a focus on providing capital to late-stage and growth companies, which seek to attract other sources than equity. So, RWAY lends capital to businesses that are looking to fund growth by avoiding any further equity dilution, which, in turn, confirms that the companies are indeed at a more advanced stage than typical early stage VC-funded companies.

Portfolio structure

The primary focus is put on first lien, senior secured loan category with an average loan ticket size ranging from $10mm to $100mm.

RWAY 3Q23 Earnings Presentation

As we can see in the chart above, currently RWAY holds ~94% of its allocations in senior secured first lien term loans.

The picture is further enhanced by the following facts :

- Average Revenue $57.1M

- Average LTV 17.6%

- Cumulative Gross/Net Loss Rate 0.34%/0.12%

What this means is that RWAY has indeed biased its portfolio to a more predictable and less speculative spectrum of VC backed businesses as on average the underlying businesses are able to already generate notable sales, while carrying extremely low leverage profiles.

Typically, an LTV metric of ~40-50% could be deemed satisfactory in terms of the assumed financial risk. So the fact that RWAY's portfolio constituencies has this at only ~18% clearly indicates a high degree of conservatism in the structure (and the cumulative loss ratios confirm this).

RWAY 3Q23 Earnings Presentation

Moreover, the situation of RWAY's portfolio risk scores is very sound as ~98% of the portfolio has a weighted average risk rating of 3 or better (1-5 rating scale, with a lower number reflecting a higher credit quality rating).

Here, it is worth noting that even more conventional BDCs that do not invest in VC-backed companies tend to have higher concentration of their portfolios into 4 and 5 risk rating categories. It varies case by case, but on average this number lands at ~6-10%.

RWAY 3Q23 Earnings Presentation

And if we look at the deal volumes conducted by RWAY, I think we can understand why the quality has been so rock solid. From the chart above, it is quite evident that RWAY is selective and holds to its tight underwriting standards when sourcing new volumes, even though that would imply less accelerated growth.

In the most recent earnings call , Greg Greifeld - CEO - painted a similar picture, confirming RWAY's continued focus on quality over quantity:

Our focus on underwriting low loan-to-value loans to high-quality companies has allowed us to build a portfolio that can continue to succeed and not just survive ... Our patience in deploying capital during 2023 has been strategic and the current environment is more lender-friendly than earlier this year. We expect this lender-friendly environment to continue into 2024 and we are beginning to see an increase in favorable investment opportunities.

Thesis

There are really two aspects, which I like about RWAY on top of the defensive characteristics of its portfolio (as elaborated above).

The first is the Fund's portfolio yield, which as of Q3, 2023, stood at 18.3%. This is one of the highest portfolio yields we will notice in the BDC space.

RWAY 3Q23 Earnings Presentation

Interestingly, by looking at the chart above, we can notice how the weighted average yield has consistently marched higher - mostly thanks to almost 100% exposure to floating rate debt. Granted, not everything is explained by higher SOFR; there has also been a marginal uptick in the credit risk premium that RWAY attaches to its investments.

As a result of this lucrative yield, RWAY's dividend also provides an attractive yield in the context of the overall BDC segment. Currently, RWAY offers 12.6% in dividend yield, which is between 150 to 200 basis points above the BDC average.

An additional layer of safety in relation to the RWAY's ability to accommodate these distributions stems from rather healthy coverage ratios (e.g., ~120% based on Q3 data points).

{kind=link}

The second aspect, which, in my opinion, de-risks the fund even further and renders the investment story appealing, is RWAY's leverage profile.

Currently, RWAY carries a debt to equity level at 79%, which is one of the lowest in the sector as the corresponding average stands at 117% .

This is a great addition to the prudently structured portfolio and well-covered dividend yield that introduces a great margin of safety for RWAY to defend its 12.6% yield from potential struggles in the economy or in general increasing default levels across the below investment grade level businesses.

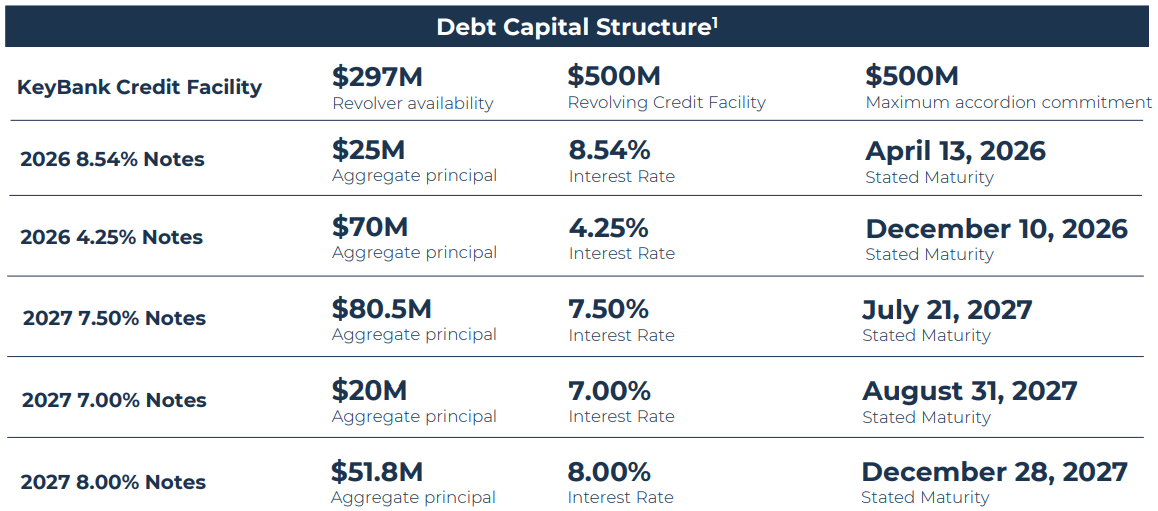

Finally, the prevailing spread seems to also be rather stable given the distant debt maturity profiles, which the fund has assumed as an external leverage to facilitate an expansion of NAV base. If we adjust for the revolver, RWAY has five fixed-rate notes with maturity dates spread across 2026 and 2027 that should help avoid spread compression from more expensive cost of capital.

The bottom line

While RWAY is a VC-focused BDC, which per definition brings many risks to the equation, the underlying structure of its portfolio and the dynamics on the leverage front render this BDC an interesting investment to consider.

The current dividend yield of 12.6% is well-covered and underpinned by a conservative portfolio, which should provide investors with an opportunity to capture high and stable streams of income.

For further details see:

Runway Growth Finance: A Different Kind Of VC-Focused BDC