RWAY - Runway Growth Finance: Should You Grab The Venture Debt Powered 13.1% Yield?

2023-10-04 11:05:35 ET

Summary

- Runway Growth Finance is paying out a 13.1% regular dividend yield that's 123% covered by net investment income.

- The BDC is currently swapping hands at a 15% discount to NAV per share as of the end of second quarter of its fiscal 2023.

- NAV has been dipping, with the BDC also taking a conservative approach to new investments.

Runway Growth Finance (RWAY) only went public in October 2021 but has since returned around 19% on a total return basis, with a dip in its net asset value and its share price countered by what's been five consecutive dividend hikes up until the start of 2023. The BDC last declared a quarterly cash dividend of $0.40 per share , in line with its prior payment, for a 13.1% annualized forward dividend yield. The quarterly distribution will also include a $0.05 per share supplemental payment for what would be an incremental 1.6% annualized yield. A 14.7% aggregate yield is huge, with the aggregate payout on an upward trajectory ever since the Fed raised base rates to 22-year highs. There are a few things to like about the externally managed ticker from its focus on the high growth venture debt space to its 100% floating rate broadly credit portfolio.

Further, with the BDC also last reporting fiscal 2023 second-quarter NAV of $14.17 per share, its commons at $12.22 per share are currently swapping hands at a roughly 14% discount to NAV. Hence, you're essentially buying a near-15% yield for 86 cents on the dollar. The BDC has dipped along with the market as the Fed reiterated it's higher for longer mantra as it kept rates unchanged at its last FOMC meeting in September. For some context, venture debt-focused BDC TriplePoint Venture Growth (TPVG) is trading at an 8% discount to NAV whilst blue chip Hercules Capital (HTGC) is trading at a premium. BDCs are not as inversely correlated with higher base rates as bonds and other fixed-income investments are. Higher for longer combined with what remains a resilient US economy directly translates to higher investment income.

The NAV Decline Set Against Rising Investment Income

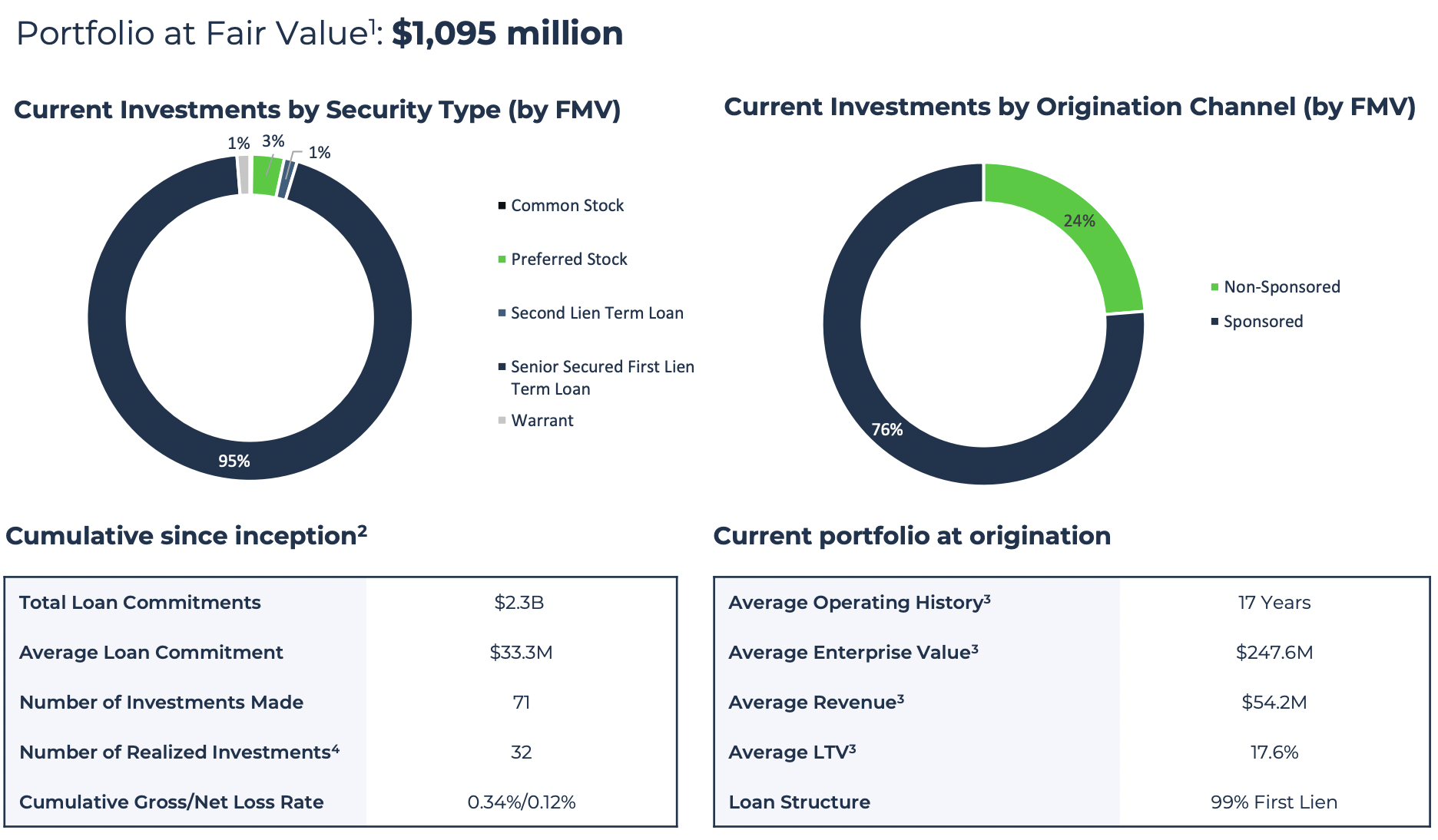

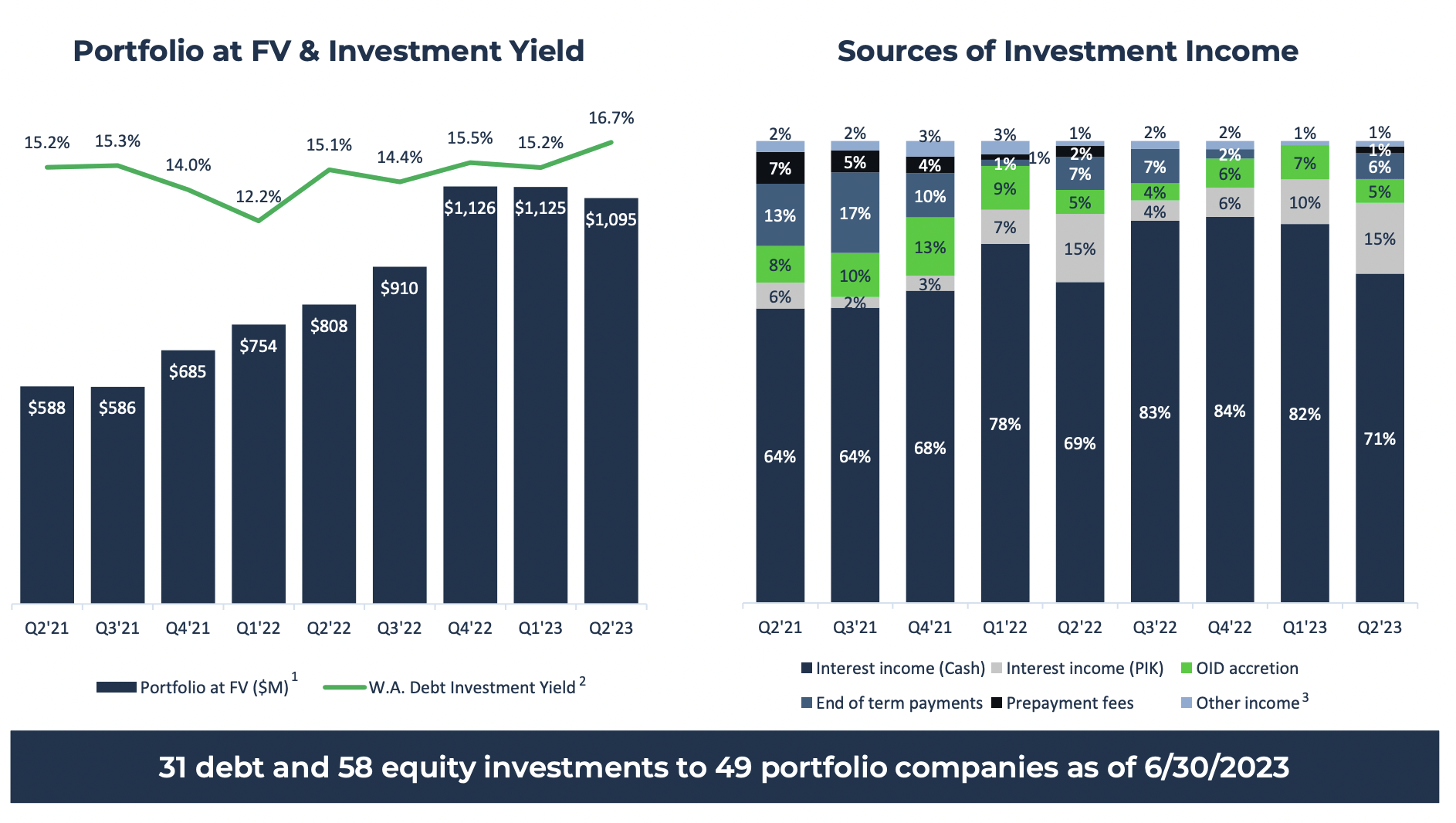

NAV has been declining, peaking north of $600 million at the start of 2022 and in decline since then. Runway Growth recorded a second-quarter total investment income of $41.9 million , up 66.3% from $25.2 million in the year-ago quarter. What does the BDC's portfolio look like? $1.1 billion spread across 49 companies as of the end of the second quarter, with Runway Growth focused on companies in the technology, life sciences, and consumer sectors. The BDC most recently updated the market on a $40 million senior secured term loan it extended to Elevate Services, a software company for law firms. It's also a portfolio that includes hair care and color brand Madison Reed and pulmonary and cardiac disease drug company VERO Biotech.

Runway Growth Finance Fiscal 2023 Second Quarter Presentation

{kind=link}

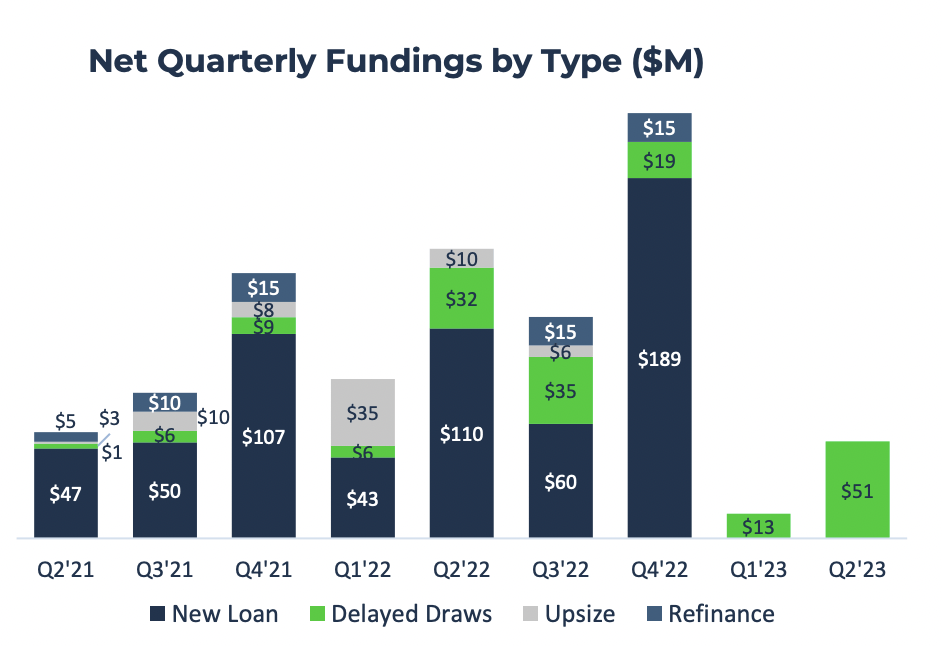

The portfolio currently has a 95% weighting towards senior secured first lien term loans, with preferred stock forming the second-largest weighting at 3%. The focus on first lien loans is great as these take seniority over other types of debt and give Runway Growth the first claim on its borrower's assets in the event of bankruptcy. The BDC funded $50.9 million in new loans during the second quarter to its existing portfolio companies. This was set against principal repayments of $88.7 million.

Runway Growth Finance Fiscal 2023 Second Quarter Presentation

{kind=link}

There has been a clear pullback in new funding since the start of the year with Runway Growth pulling back on making new loans and allowing net repayments to exceed new findings. This has the impact of slimming the overall size of the portfolio but reinforcing the safety of the BDC. Total debt to equity is also quite low at 95% but with a second-quarter investment yield that moved up 160 basis points over its year-comp to 16.7%.

Runway Growth Finance Fiscal 2023 Second Quarter Presentation

{kind=link}

Net Investment Income And Dividend Coverage

Runway Growth recorded a net investment income of $19.7 million, around $0.49 per share. This was up from $0.35 per share in the year-ago quarter, with the BDC comfortably covering its regular dividend payout by 123%. The BDC will likely need to ramp up funding, as it is perhaps being too prudent against what remains a resilient economic backdrop. The portfolio at fair value has already flat lined. This is as payment-in-kind ((PIK)) interest income as a percent of income rose to 15% from 10% in the prior first quarter. PIK is broadly used by companies facing financial difficulty and is sometimes a good barometer for the future direction of non-performing loans.

The BDC only had one portfolio company on non-accrual status, Pivot3, which held a loan of $11.6 million at fair value from Runway Growth as of the end of the second quarter. This amounted to 1.06% of the BDC's investment portfolio. Critically, Runway Growth currently represents a lowly geared play on venture debt with a fat yield that's fully covered by net investment income and set to be buffeted by the base rates remaining higher for longer. I'd rate the commons as a cautious buy on the yield, but shareholders need to watch the direction of NAV before building a full position.

For further details see:

Runway Growth Finance: Should You Grab The Venture Debt Powered 13.1% Yield?