SAH - Rush Enterprises: A Good Ride That's Not Over Yet

Summary

- Rush Enterprises continues to post strong sales, profit, and cash flow growth year-over-year.

- Some weakness is showing in the form of a reduced backlog, but the company is still doing well despite this.

- Shares are also cheap and likely offer additional upside from here.

Vehicle dealerships are a dime a dozen. But one company that has built for itself a rather niche operation is Rush Enterprises ( RUSHA ) ( RUSHB ). Instead of just focusing on vehicles in general, the company serves as one of the largest commercial vehicle dealer groups in North America. In fact, according to it, it is the largest such firm. It also owns an 80% stake in Rush Truck Centres of Canada, which has 14 international locations throughout Ontario. All combined, the company focuses on selling and servicing some of the major truck brands out there such as Peterbilt, Navistar, Hino, and Isuzu. Recent financial performance achieved by the company has been quite impressive. And on top of that, shares of the company looked to be trading on the cheap. There could be some headwinds moving forward. But given how cheap the stock is at this moment, it's difficult to imagine a scenario where shares might become overvalued. So even though shares of the company have risen nicely compared to the broader market over the past several months, I would make the case that the company offers further upside from here.

A great ride so far

Back in the middle of May of 2021, I found myself interested in the investment prospects offered by Rush Enterprises. Prior to the COVID-19 pandemic, the company had done quite well for itself. Although the pandemic did hit the business, even at that time we seemed to be experiencing something of a turnaround. Add on top of this how attractively priced shares were, and I could not help but to rate the company a 'buy', a rating that indicates my belief that shares should outperform the broader market for the foreseeable future. So far, that call has proven to be pretty positive. While the S&P 500 has dropped 3.1%, shares of Rush Enterprises have generated upside for investors of 4%.

{kind=link}

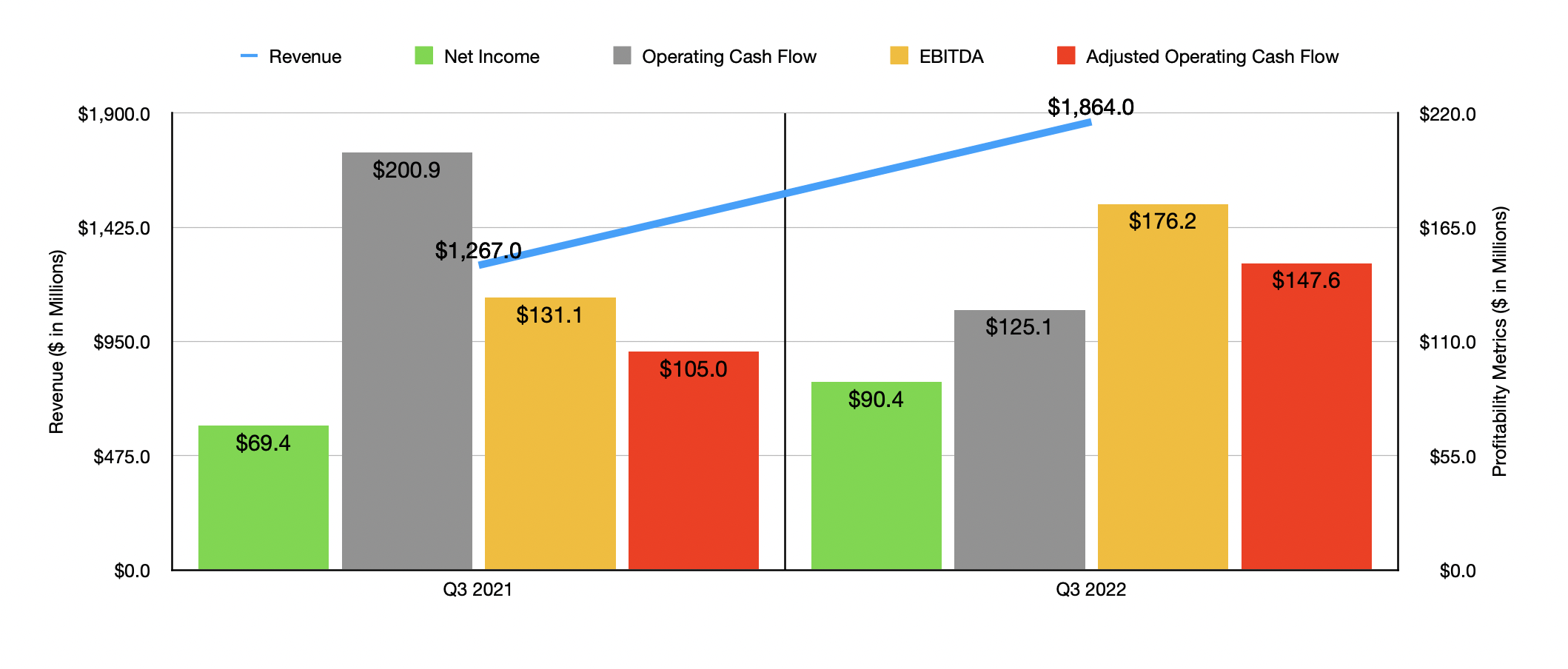

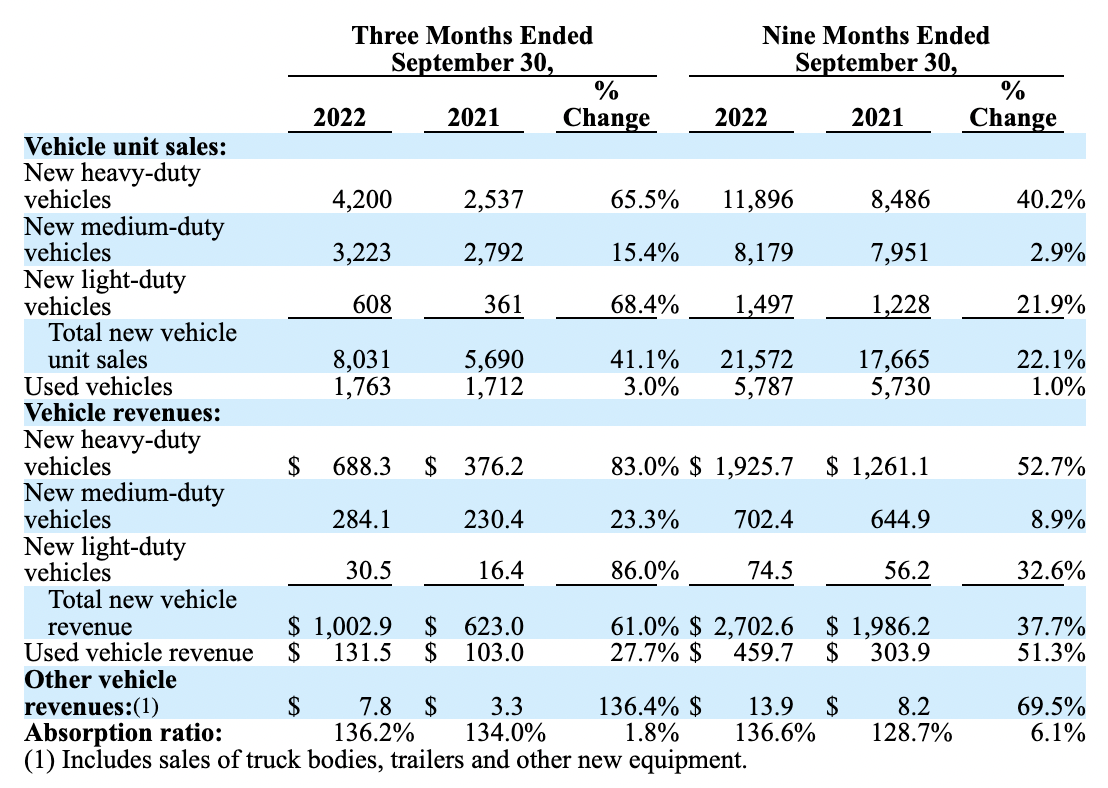

As of this date, the most recent data we have on the company covers through the third quarter of its 2022 fiscal year. For that quarter, sales came in at $1.86 billion. That represents a sizable improvement over the $1.27 billion reported the same time one year earlier. This increase in sales was driven largely by a surge in the number of vehicles the company sold. Total new vehicle unit sales jumped by 41.1% year over year, climbing from 5,690 to 8,031. This consisted of a 68.4% rise in new light-duty vehicle sales, a 15.4% increase in new medium-duty vehicle sales, and a 65.5% increase in new heavy-duty vehicle sales. Used vehicle sales for the company also increased by 3% year over year. All combined, the new vehicle revenue for the company jumped from $623 million to just over $1 billion, while used vehicle revenue increased from $103 million to $131.5 million. Strong demand helped the company immensely, as did its acquisition of Summit Truck Group for $262.3 million and its acquisition of 30% (taking its stake up to 80%) of Rush Truck Centres of Canada. The company also saw a 34.4% increase in sales for its aftermarket products and services, with a combination of strong demand, price increases resulting from inflationary pressures, and the aforementioned acquisitions, all contributing.

{kind=link}

From a profitability perspective, the picture for the company also improved. Net income of $90.4 million represented a sizable increase over the $69.4 million reported one year earlier. Other profitability metrics largely followed suit, with the exception of operating cash flow. That metric actually declined year over year, dropping from $200.9 million to $125.1 million. If we adjust for changes in working capital, however, the metric would have risen from $105 million to $147.6 million. Meanwhile, EBITDA for the company also improved, rising from $131.1 million to $176.2 million.

{kind=link}

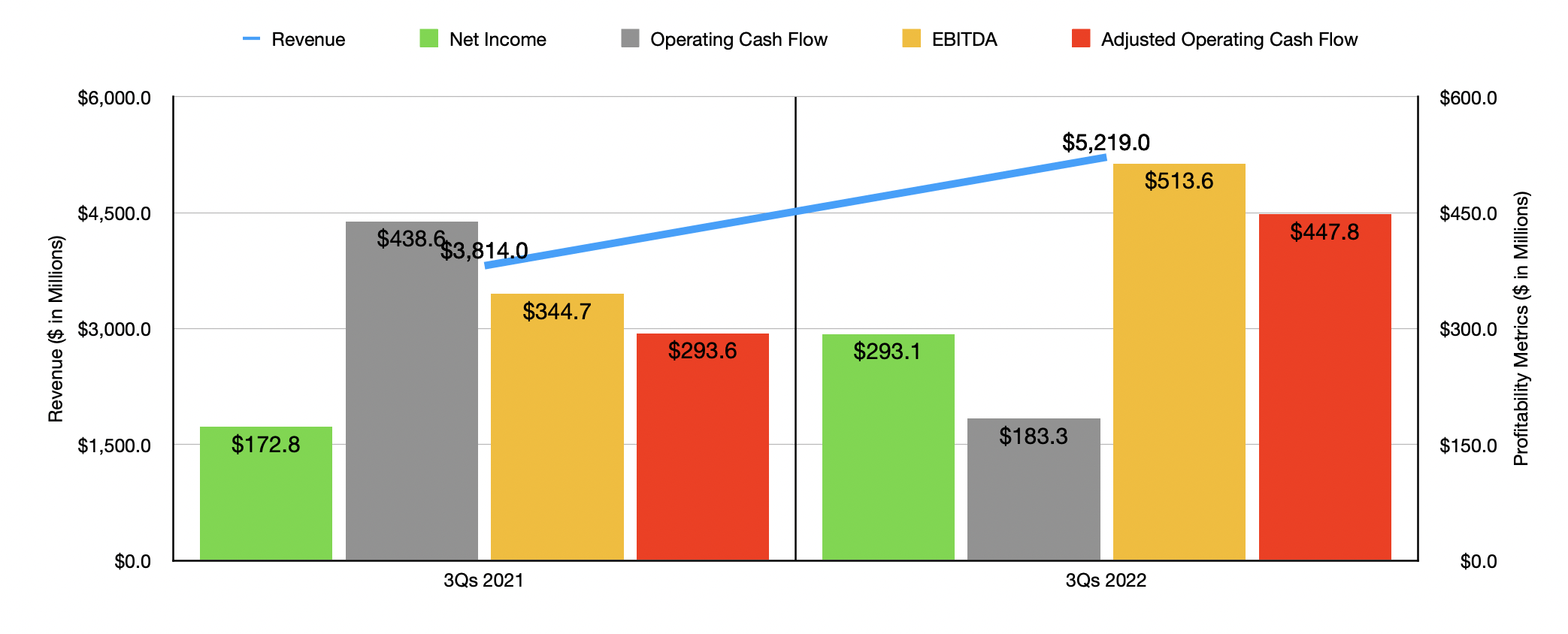

As you might expect, 2022 in its entirety, or at least the first nine months that we have data for, looked very similar to what the company reported for the third quarter alone. Sales of $5.22 billion came in meaningfully higher than the $3.81 billion reported one year earlier. Net income almost doubled from $172.8 million to $293.1 million. Operating cash flow once again dropped, plunging from $438.6 million to $183.3 million. But if we adjust for changes in working capital, it would have risen from $293.6 million to $447.8 million. And finally, EBITDA for the company increased year over year, rising from $344.7 million to $513.6 million.

At first glance, all of this looks great. But this is not to say that everything is fantastic about the firm. It is showing some signs of weakness. Backlog is the most significant example. As of the end of the latest quarter, backlog for the company came in at $3.30 billion. This represents a reasonable improvement over the $2.72 billion reported for the same quarter one year earlier. This was largely because of the aforementioned acquisition activities the company engaged in. But the number is actually down from the $3.68 billion that the company had as of the end of the second quarter. Some investors may wonder if there is a seasonal component to this. But that does not appear to be the case. After all, in the second quarter of 2021, backlog was $2.26 billion. So we have gone from sequential increases to sequential declines over just one year.

{kind=link}

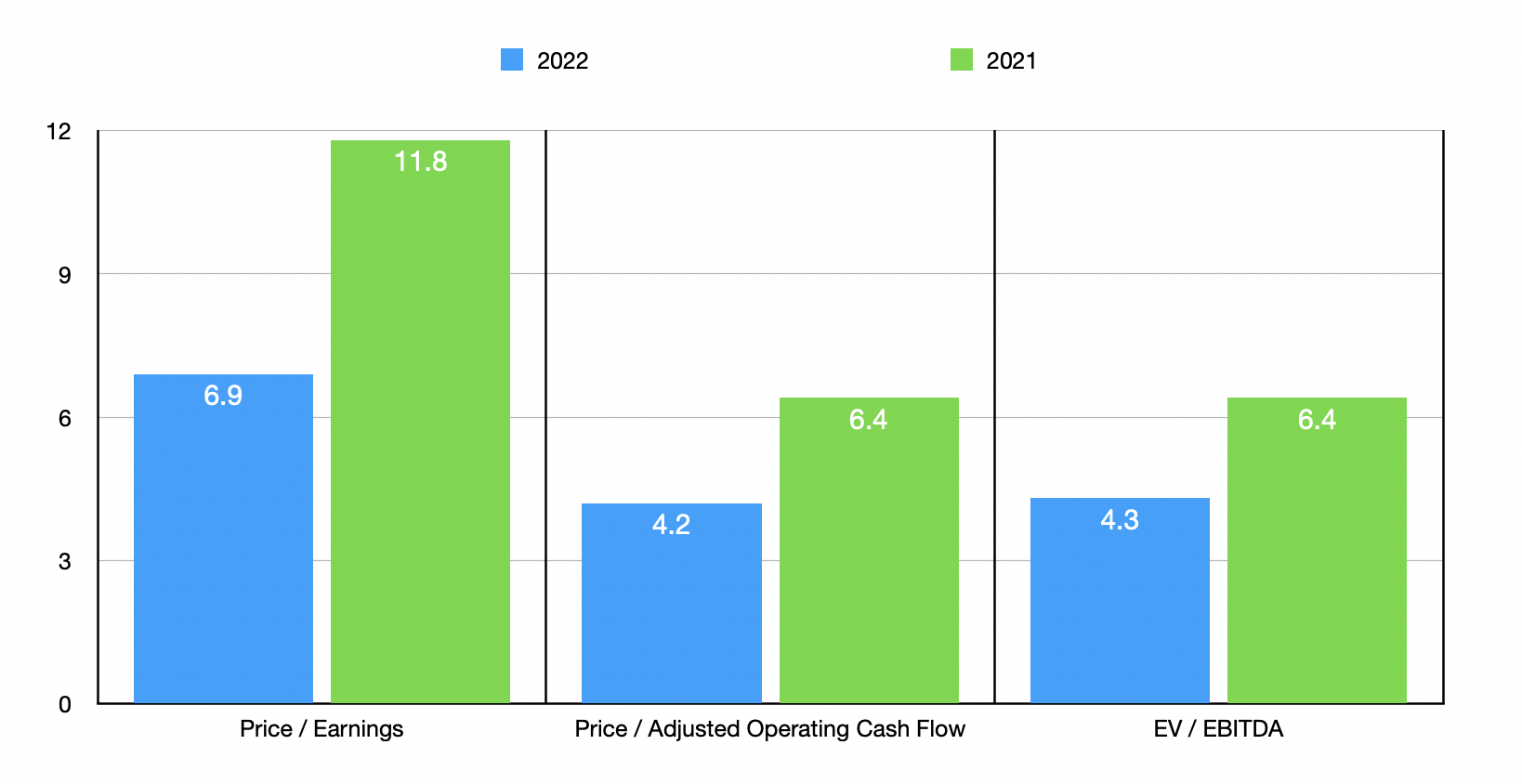

This makes relying on some sort of annualized approach to valuing the company a bit less reliable. But we can solve this by looking at data from prior years as well. If we do annualize the data for the company, we would anticipate net income for 2022 coming in at $409.5 million. Adjusted operating cash flow would be $679.9 million, while EBITDA would total $708.6 million. All of this would translate to a price-to-earnings multiple of 6.9, a price to adjusted operating cash flow multiple of 4.2, and an EV to EBITDA multiple of 4.3. If we were to use the data from 2021 instead, these multiples would be 11.8, 6.4, and 6.4, respectively. As part of my analysis, I did also compare the company to some other automotive retailers. On a price-to-earnings basis, these companies ranged from a low of 5.3 to a high of 6.4. In this respect, Rush Enterprises was the most expensive of the group. If we use the price to operating cash flow approach, the range would be from 3 to 9.8, with only one of the five firms cheaper than our target. And finally, using the EV to EBITDA approach, the range would be from 4.6 to 5.9. In this case, our target is the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Rush Enterprises |

| 6.9 |

| 4.2 |

| 4.3 |

| Sonic Automotive ( SAH ) |

| 5.4 |

| 3.0 |

| 5.9 |

| Group 1 Automotive ( GPI ) |

| 4.8 |

| 4.8 |

| 4.7 |

| Penske Automotive Group ( PAG ) |

| 6.4 |

| 7.7 |

| 5.9 |

| Camping World Holdings ( CWH ) |

| 5.3 |

| 9.8 |

| 4.6 |

| Asbury Automotive Group ( ABG ) |

| 5.4 |

| 4.9 |

| 5.8 |

Takeaway

For what data we have right now, it seems to me as though Rush Enterprises is doing really well for itself. Revenue, profits, and cash flows are all rising nicely. Shares of the company look incredibly cheap and still look affordable if we assume that financial results were to revert back to what they were in 2021. We are seeing some weakness in the form of backlog that investors should pay attention to. But this has not stopped the company from buying nearly $33.1 million worth of shares in the first nine months of 2022 and then, in early December of last year, initiating a $150 million share buyback program. What this tells me is that investors should monitor the company's financial condition going forward, but that shares are also still cheap enough to warrant a 'buy' rating at this time.

For further details see:

Rush Enterprises: A Good Ride That's Not Over Yet