SAH - Rush Enterprises Continues To Justify A Bullish Stance

2023-06-29 07:30:00 ET

Summary

- Despite high inflation and interest rates, Rush Enterprises, a company focused on the sale of commercial vehicles, has outperformed the broader market due to strong revenue and cash flow data.

- Rush Enterprises' Q1 2023 revenue increased by 22.3% to $1.91 billion, driven by a 28.6% surge in new vehicle units sold.

- Despite a decline in net income, other profitability metrics improved, with operating cash flow nearly tripling and EBITDA growing.

- The company's outlook for 2023 is positive, with expectations of modest increases in truck sales and growth in lease and rental revenue, as well as aftermarket parts and services revenue.

- I conclude that Rush Enterprises stock still has additional upside and continues to warrant a 'buy' rating.

Over the past two years now, high levels of inflation, combined with high interest rates aimed at combating that inflation, have created significant uncertainty when it comes to specific aspects of the economy. Anything related to the sale of vehicles should generally be considered unappealing because high-priced items that require large amounts of financing rarely perform well in an inflationary, high interest rate environment. One company though that has defied the odds and achieved rather impressive financial results is Rush Enterprises ( RUSHA ) ( RUSHB ). Unlike most companies in the automotive retail space, Rush Enterprises focuses on the sale of commercial vehicles throughout North America. It also has a significant ownership stake in Rush Truck Centres of Canada. Recently, shares of the company have outperformed the broader market. This has come on the back of strong revenue and cash flow data. Even with the move higher, shares look fundamentally cheap on an absolute basis and look a bit cheap relative to similar enterprises. Given these facts, I have no problem keeping the company rated a ‘buy’ at this time.

Results continue to impress

In late January of this year, I decided to revisit my prior bullish thesis regarding Rush Enterprises. Leading up to that point, the company was generating strong sales growth, impressive profit growth, and continued cash flow growth. It was seeing some weakness in the form of reduced backlog. But all things considered, shares of the company looked cheap and I believed that shareholders had attractive upside potential moving forward. This led me to keep the ‘buy’ rating I had on the stock previously. So far, my rating history with the company has been quite solid. Since the publication of my most recent article , shares of the business have seen upside of 14.6%. That's almost double the 8% increase seen by the S&P 500. And since my first bullish article on the company in May of 2021, shares are up 25.4% compared to the 6.8% increase the S&P 500 enjoyed.

{kind=link}

Author - SEC EDGAR Data

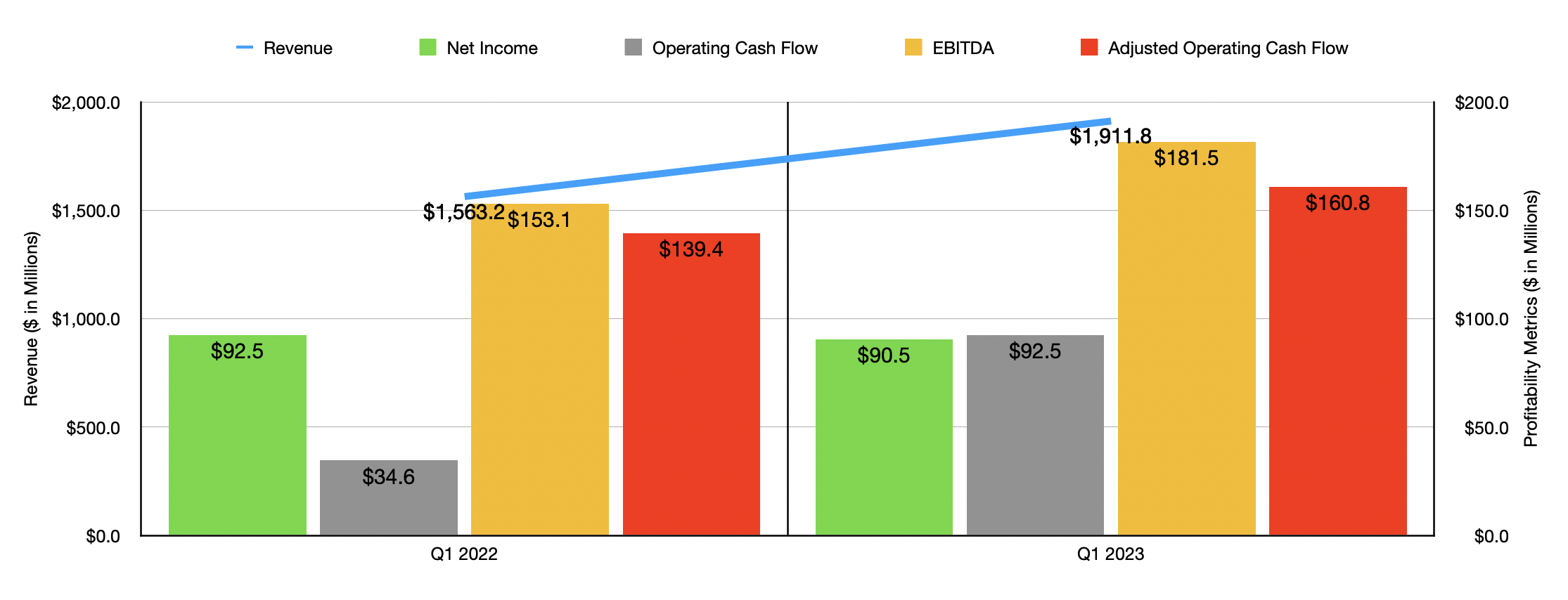

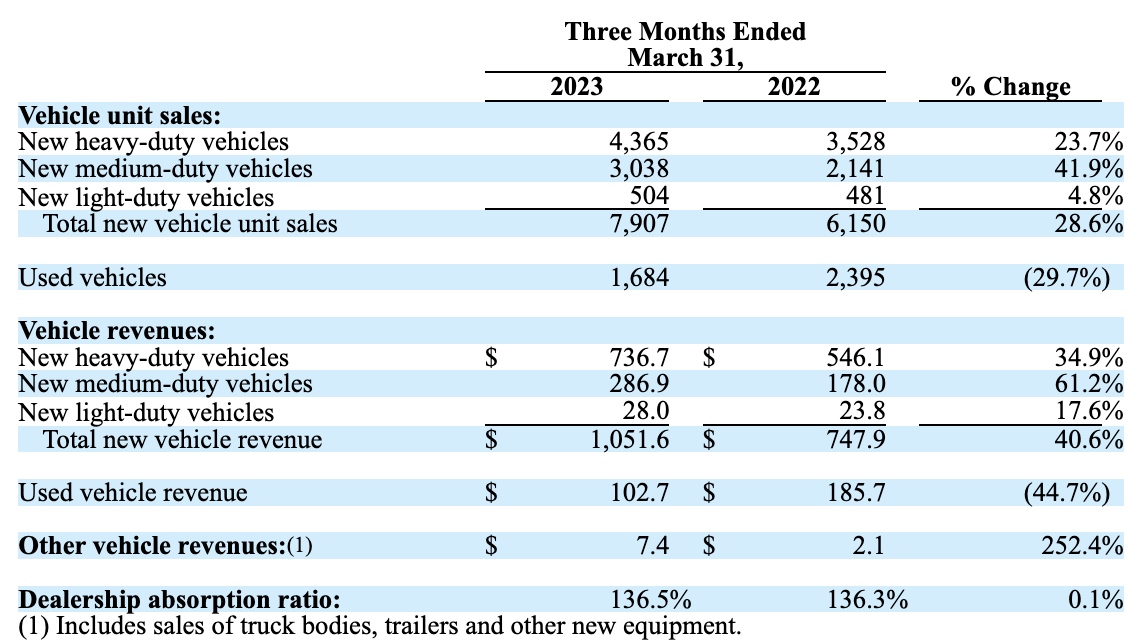

To understand why Rush Enterprises continues to outperform the market, we need only look at the first quarter of the company's 2023 fiscal year. This is the most recent quarter for which new data is available. Revenue for that time came in at $1.91 billion. That represents an increase of 22.3% over the $1.56 billion the company generated one year earlier. The big driver behind this increase was a 28.6% surge in the number of new vehicle units sold. This number climbed from 6,150 units in the first quarter of 2022 to 7,907 units in the first quarter of this year. This, combined with price increases, helped total new vehicle revenue for the company shoot up 40.6% from $747.9 million to $1.05 billion. Unfortunately, this was offset to some degree by a decline in used vehicle revenue of 44.7%. This, according to management, was largely attributable to a 29.7% decrease in used vehicle unit sales from 2,395 to 1,684.

{kind=link}

Rush Enterprises

There were other drivers to the company's revenue increase. For instance, aftermarket parts and services sales grew 19.3% from $543.3 million to $648.2 million. And lease and rental revenue jumped 21.5% from $71.3 million to $86.7 million. The only real weakness was on the finance and insurance side. But with revenue of only $6.6 million in the first quarter of 2023, this is little more than a rounding error in the grand scheme of things.

The rise in revenue for the company brought with it some mixed results on the bottom line. Net income actually declined from $92.5 million to $90.5 million. But this was largely the result of an $11.7 million decrease in other income and a $9.8 million increase in interest expense. The other income decrease was driven by a $12.5 million gain that the company realized on a financial transaction that should be considered one time in nature and that occurred in the first quarter of 2022. Even though net profits decreased, other profitability metrics for the company improved. Operating cash flow, for instance, nearly tripled from $34.6 million to $92.5 million. If we adjust for changes in working capital, we would see that number grow from $139.4 million to $160.8 million. And finally, EBITDA for the firm grew from $153.1 million to $181.5 million.

{kind=link}

Author - SEC EDGAR Data

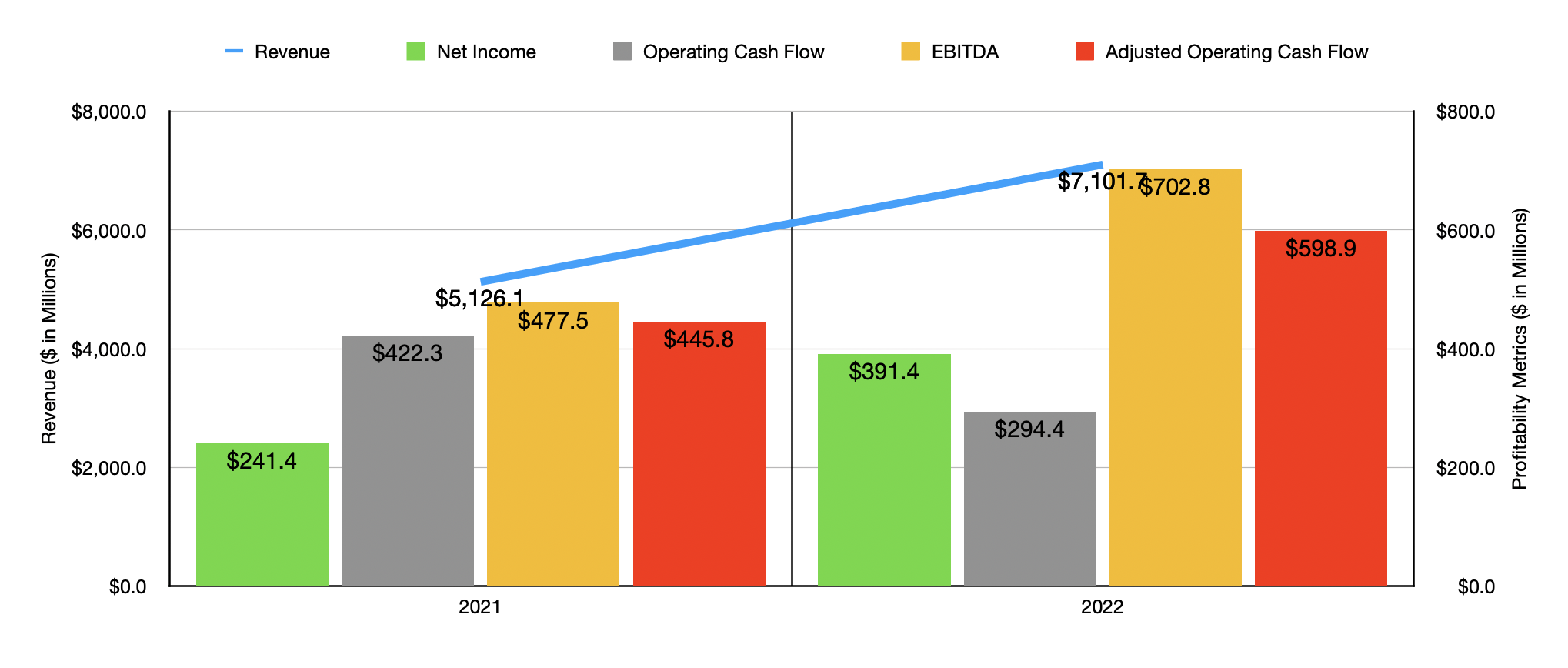

As you can see in the chart above, results experienced during the first quarter of 2023 were not a one-time event. 2022 also saw fantastic performance relative to 2021. Revenue of $7.1 billion beat out the $5.1 billion reported one year earlier. Net income shot up while two of the three cash flow metrics that I look at also increased. The only weakness on this front was when it came to operating cash flow. But on an adjusted basis, it also grew nicely year over year.

{kind=link}

Rush Enterprises

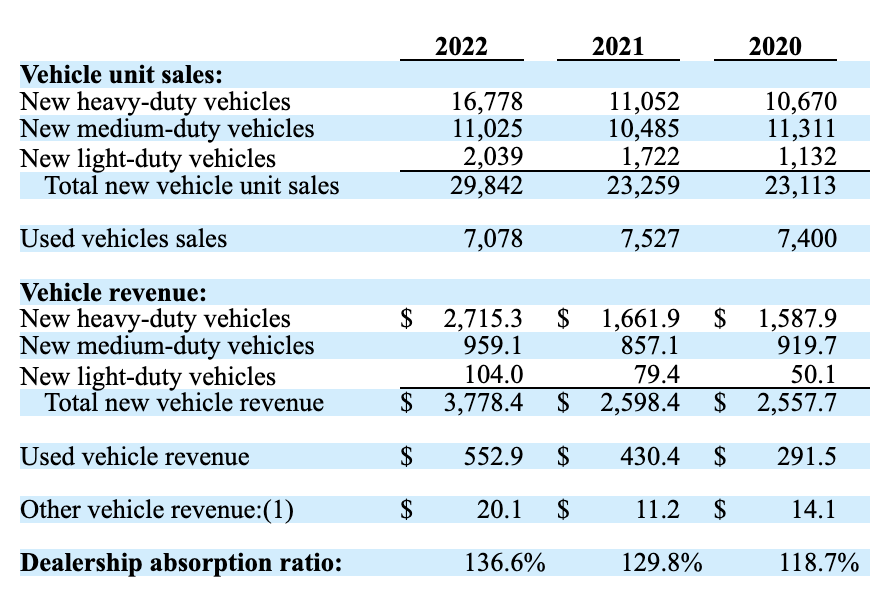

When it comes to guidance for 2023, management has not provided much in the way of detail from a monetary perspective. But they have provided a general outlook for what 2023 might look like. Citing A.C.T. Research Co., LLC, a commercial vehicle industry data and forecasting service provider, the company said that Class 8 retail truck sales should be around 259,018 units this year. That would be a modest increase of 0.1% compared to what the industry experienced last year. Management is forecasting market share in this category of between 6.2% and 6.8%. That would imply about 16,836 units at the midpoint. That compares to the 16,750 that the company sold last year. For the Class 4 through 7 categories, the forecast is 253,600 units. That would be 8.6% above what was seen in 2022. Management is forecasting a market share in this category of between 4.5% and 5.1%. That would be roughly 12,250 vehicles at the midpoint compared to the 11,025 that it sold last year. That's on top of another 300 units of Class 5 through Class 7 commercial vehicles it hopes to sell in Canada.

Management also has positive expectations when it comes to other activities. It expects to sell between 1,800 and 2,000 light-duty vehicles this year, which would be a bit below the 2,039 that it reported for last year. And it expects to sell between 6,500 and 7,500 used commercial vehicles this year, which, at the midpoint, would be roughly flat compared to the 7,078 reported for 2022. At the same time, however, lease and rental revenue should grow by between 9% and 11% year over year, while aftermarket parts and services revenue should climb by between 9% and 12%.

{kind=link}

Author - SEC EDGAR Data

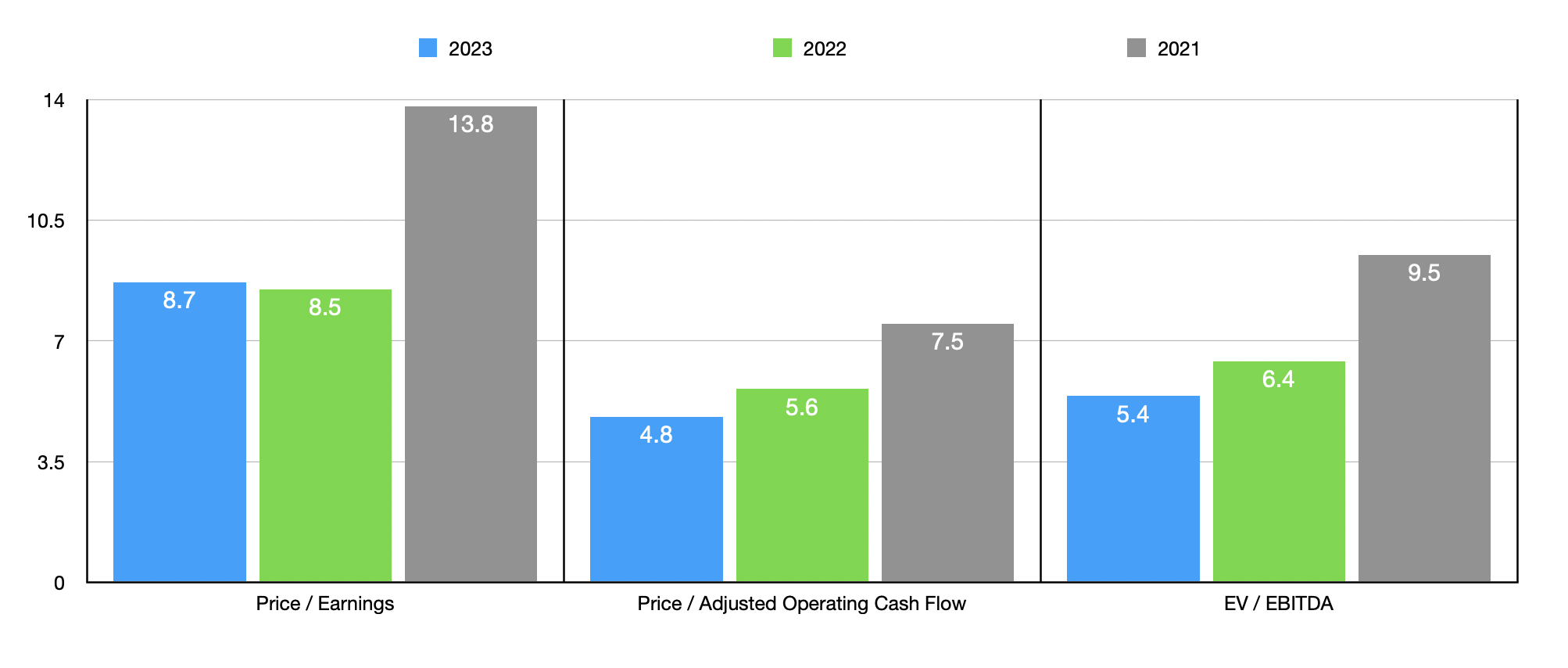

This is not enough to give us a firm understanding of what the fundamental picture of the business should look like. But if we annualize results experienced so far for 2023, we would expect net income of $382.9 million, adjusted operating cash flow of $690.8 million, and EBITDA of $833.2 million. Using these estimates, I was able to value the company as shown in the chart above. That chart also has valuation data using results from both 2021 and 2022. Even if we rely on the slightly more conservative 2022 estimates, shares look fundamentally attractive compared to similar enterprises. In the table below, I compared the company to five firms that have similarities to it. Using both the price to earnings approach and the EV to EBITDA approach, I calculated that two of the five firms ended up being cheaper than Rush Enterprises. And when it comes to the price to operating cash flow approach, only one of the five ended up being cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Rush Enterprises |

| 8.5 |

| 5.6 |

| 6.4 |

| Sonic Automotive ( SAH ) |

| 75.2 |

| 15.5 |

| 11.9 |

| Group 1 Automotive ( GPI ) |

| 5.5 |

| 7.5 |

| 5.8 |

| Penske Automotive Group ( PAG ) |

| 9.0 |

| 8.5 |

| 7.6 |

| Asbury Automotive Group ( ABG ) |

| 5.5 |

| 11.4 |

| 5.4 |

| Camping World Holdings ( CWH ) |

| 12.9 |

| 2.6 |

| 7.1 |

Takeaway

From all that I can see, Rush Enterprises continues to fare well in the current environment. Even though net income has taken a slight step back recently, revenue and cash flows are growing nicely and the general outlook for 2023 is positive. Shares are still cheap on an absolute basis and tilt toward the cheap end of the spectrum compared to similar firms. Given all of these factors combined, I do believe that the firm still has some additional upside. It offers enough, at least, to still warrant the ‘buy’ rating I have signed it previously.

For further details see:

Rush Enterprises Continues To Justify A Bullish Stance