SAH - Rush Enterprises Deserves More Upside Despite Recent Mixed Results

2023-12-23 00:14:25 ET

Summary

- Rush Enterprises, a commercial vehicle sales company, has seen its stock rise by 6.1% due to a sizable share buyback program and cheap shares.

- While revenue continues to rise, the company's bottom line metrics have shown signs of weakness, with net profits declining.

- Despite mixed financial performance, the stock remains cheap and management has initiated a new $150 million share buyback program.

One of the great things about buying stocks that trade at low multiples is that you don't need financial performance to always come in strong in order to justify upside. A good example of this can be seen by looking at Rush Enterprises ( RUSHA ) ( RUSHB ), a business that focuses on the sale of commercial vehicles that operates throughout parts of North America. For the most part, revenue at the company continues to rise, but some of its bottom line metrics have shown signs of weakness. Even in spite of that, however, a rather sizable share buyback program, combined with how cheap shares are, has led to the stock rising by 6.1% since I last rated the company a ‘buy’ back in late June of this year. Unfortunately, that does fall short of the 8.3% increase seen by the S&P 500. But in this volatile market, any sort of upside should be considered a positive.

A mixed picture

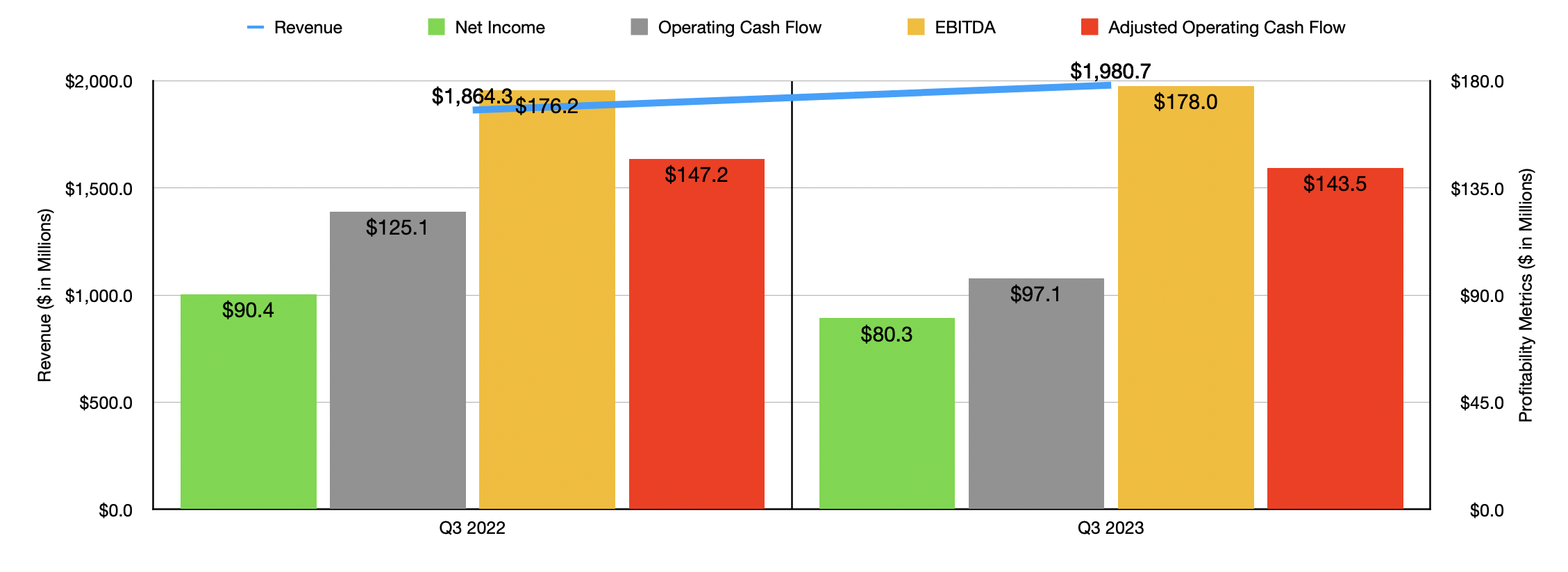

Recently, financial performance achieved by Rush Enterprises has been fine, but far from great. Consider data for the most recent quarter , which would be the third quarter of the 2023 fiscal year. During that window of time, revenue for the company came in at $1.98 billion. That represents an increase of 6.2% over the $1.86 billion the business reported one year earlier. There were a couple of key drivers behind this sales increase. For starters, the firm saw a 3% rise in the number of new heavy-duty vehicles sold, with the number of units climbing from 4,200 in the third quarter of 2022 to 4,326 the same time this year. Actual revenue associated with this sales increase jumped by 9.9%, with that spread driven by an increase in pricing. Even more impressive was the new medium duty vehicle category, with the number of units rising by only 0.7% from 3,223 to 3,244, but the revenue associated with these vehicles spiking 17.2% Management stated that there is still limited production of these vehicles, so it stands to reason that overall revenue jumped as much as it did because of higher prices.

{kind=link}

On the bottom line, the picture has been a bit more complicated. Net profits have actually declined from $90.4 million to $80.3 million. A rise in the cost of products sold from 79.5% of sales to 80.1% a decrease in margin associated with truck lease and rental sales was driven by lower rent utilization rates. The company also suffered from a drop in gross profit margin associated with aftermarket parts and services from 39.1% to 36.2%. This was due mostly to the continued stabilization of parts pricing and weakening demand caused by economic conditions. The company also reported a surge in interest expense from 0.3% of sales to 0.7%. This increase, according to management, was driven by high interest rates.

{kind=link}

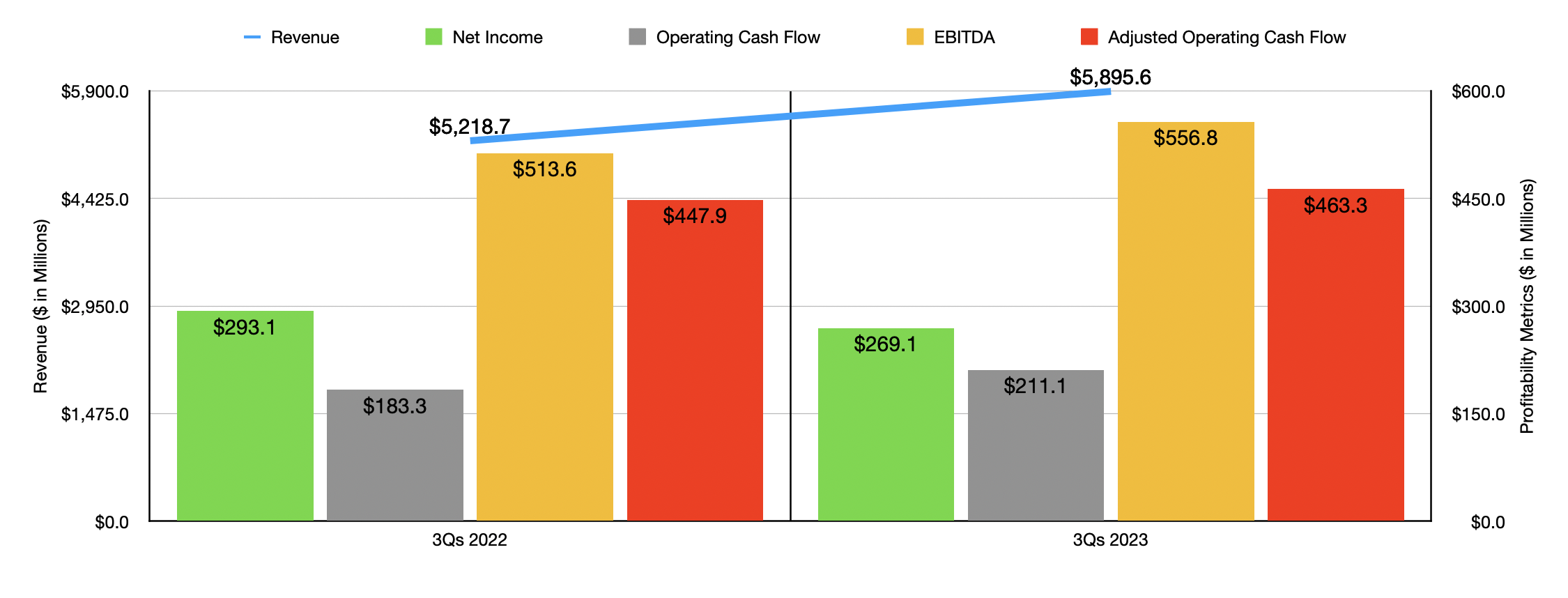

Other profitability metrics were mixed as well. On the downside, we had operating cash flow, which dropped from $125.1 million to $97.1 million. If we adjust for changes in working capital, we still get a drop from $147.2 million to $143.5 million. The only profitability metric to show an improvement year over year was EBITDA. And it managed to inch up slightly from $176.2 million to $178 million. The third quarter on its own was not a blip on the radar. In the chart above, you can see financial results for the first nine months of this year relative to the same window of time last year. Revenue increased, but profits fell. What does set this apart, however, is that all three of the other profitability metrics for the company showed improvements year over year.

{kind=link}

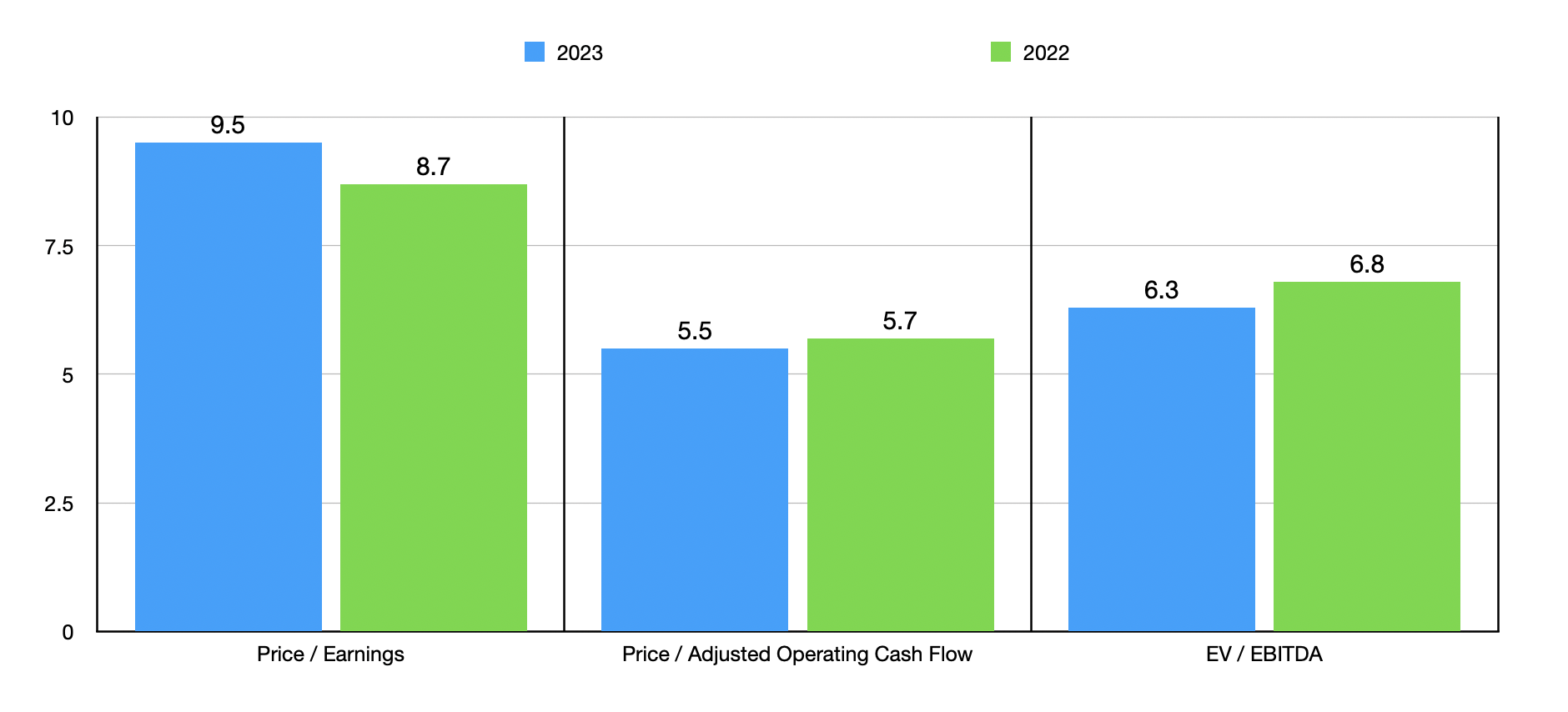

At this time, we don't really know what to expect for this year as a whole. But if we annualize the results experienced so far for the year, we would expect net profits of $359.4 million. Adjusted operating cash flow would be somewhere around $619.5 million, while EBITDA would come in somewhere around $761.9 million. Using these figures, I was then able to value the company as shown in the chart above. On a forward basis, shares look more expensive than if we use the data from 2022 when it comes to one out of the three valuation approaches. I then, as part of my analysis, created the table below. In it, you can see how shares of the business are priced relative to shares of other businesses. When it comes to the price to earnings approach, one of the companies ended up being tied with our prospect, while another two are cheaper. It ended up being the cheapest of the group when it came to the price to operating cash flow approach, and only one of the companies was cheaper than it using the EV to EBITDA approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Rush Enterprises |

| 9.5 |

| 5.5 |

| 6.3 |

| Sonic Automotive ( SAH ) |

| 76.6 |

| 22.1 |

| 15.7 |

| Group 1 Automotive ( GPI ) |

| 6.5 |

| 9.2 |

| 6.7 |

| Penske Automotive Group ( PAG ) |

| 9.5 |

| 8.7 |

| 8.2 |

| Asbury Automotive Group ( ABG ) |

| 5.3 |

| 17.7 |

| 5.7 |

| Camping World Holdings ( CWH ) |

| 122.1 |

| 8.3 |

| 10.9 |

Given how cheap the stock is and the fact that bottom line performance is far from awful, management has decided to initiate a new $150 million share buyback program. So that he can use most of the proceeds in order to repay a $40 million personal loan that has a $37 million balance secured by stock, by selling $65.3 million of his shares, leaving him with 180,339 Class A stock units and just over 7.49 million units of Class B stock. This large purchase, combined with the fact that the company has net debt of $1.38 billion, might deter the company from exercising any more of the $84.7 million it has remaining under that share buyback program. But as time goes on, the low share price and attractive cash flows, should result in additional rewards to shareholders.

Takeaway

Operationally speaking, things are not going great, but they are not going horribly wrong either. Shares of Rush Enterprises look cheap and management is making the most of it to buy back some stock. Revenue continues to climb and some profitability metrics, though not all, are showing improvement year over year. Given all of these factors, I do not think that this is a robust prospect for investors, but I do think it warrants a bit of additional upside. And because of that, I have decided to keep the company rated a soft ‘buy’ at this time.

For further details see:

Rush Enterprises Deserves More Upside Despite Recent Mixed Results