CA - Sabina Gold & Silver: Buy The Dips

Summary

- Sabina Gold & Silver just came off a busy year, with it successfully financing its Goose Project, enjoying exploration success near-mine, and advancing the project with significant underground development completed.

- Assuming all goes to schedule, Sabina will become one of Canada's lowest-cost gold miners in H2-25 when it reaches commercial production, with a 300,000-ounce production profile at sub $800/oz AISC.

- So, with Sabina trading at a 50% discount to fair value & set to be a free cash flow machine in 2026, I would view sharp pullbacks as buying opportunities.

Just over two months ago, I wrote on Sabina Gold & Silver ( OTCQX:SGSVF ), noting that while my previous bullish view on the stock (December 2021) was poorly timed as the stock suffered a 30%+ plus drawdown, the setup looked much better heading into November 2022. This was because the stock was even more undervalued at ~0.50x P/NAV; the company had continued to enjoy exploration success that could potentially pull forward high-grade ounces, and it had a high probability of reserve growth on top of its 2021 mine plan with new zones identified that included Hook and Wing.

Since November, the stock has begun to trend higher with the improving sentiment we've seen sector-wide, attributed to the ~$300/oz rise we've seen in the gold price. However, the gold developers (including Sabina) have lagged behind their producer peers, with Sabina up just 6% year-to-date vs. a 13% rally in the Gold Miners Index ( GDX ). This has left the stock trading at a deep discount to its producer peers on a relative basis, and we should see much of this gap close over the next 18 months as the company progresses towards a Q1 2025 gold pour. So, with Sabina being fully funded with a world-class project in a Tier-1 jurisdiction, I would view sharp pullbacks as buying opportunities.

{kind=link}

Goose Project - Underground Portal (Company Presentation)

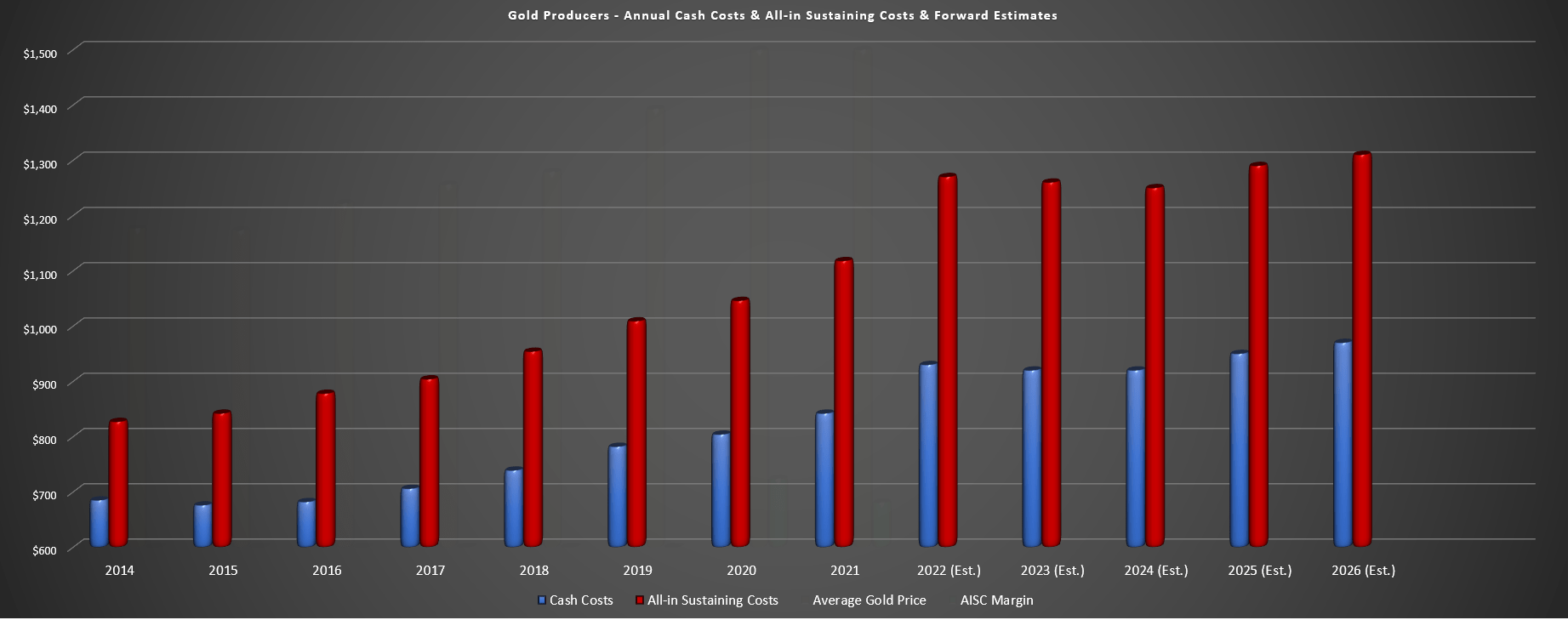

While the Gold Miners Index has enjoyed a strong recovery from its lows after suffering a 2-year cyclical bear market with a 52% peak-to-trough correction, many developers have lagged the group, still carving out bottoms in the bottom portion of multi-month bases after 70% plus corrections. Some investors might be confused by the significant underperformance, but the problem with the exploration/development sector is that we've seen a material degradation in the fundamentals for the sector on balance. Of course, this doesn't just apply to the developers, with sector-wide average cash costs of sub $800/oz in FY2019 being a distant memory. However, we'll focus on the developers here:

{kind=link}

Gold Sector Average Cash Costs/AISC + Forward Estimates (Company Filings, Author's Chart & Estimates)

For starters, inflationary pressures and rising contractor costs have made exploration/development more expensive, and labor tightness in prolific regions has made retaining current employees more expensive. Secondly, building projects have become much more costly due to the inflationary environment, meaning that many economic studies completed before H2-2021 are stale, and cut-off grades may have to rise to incorporate higher mining/processing costs. Finally, the environment for raising money is the worst in years due to multi-year highs for interest rates, and there continues to be distrust of the sector due to recent blow-ups like Pure Gold ( OTC:LRTNF ), Great Panther ( OTC:GPLDF ), and Aurcana ( OTCPK:AUNFF ).

Adding insult to injury, share prices for explorers/developers have fallen to their lowest levels in years. The result is that those companies that must raise money from the equity market (which applies to nearly every company) are getting much less capital per share sold. To summarize, each dollar is going less far due to rising costs, and each share has less worth after a bear market that has sent the share prices of most developers into the abyss. The result is that the outlook for maintaining tight share counts is bleak, making it much more difficult to grow resources/reserves per share when the share count grows at a similar pace as ounces are drilled out. In fact, some explorers may have to stop drilling altogether or cut back on drill programs.

Fortunately, there are some exceptions to the rule, just as there are in the producer space, and like Agnico Eagle ( AEM ) who has bucked the trend of rising costs due to a merger, some developers are already well-advanced or have done a great job avoiding share dilution during a challenging two years. One example of a junior that has avoided share dilution and grown ounces per share is Liberty Gold ( OTCQX:LGDTF ), benefiting from the ability to divest non-core assets in a strong market to fund drilling. Meanwhile, although Sabina saw a decent amount of share dilution to fund Goose Project construction, it's done a solid job with procurement and avoided further dilution by securing a streaming deal. Hence, it looks like all the share dilution is in the rearview mirror, and a capex blowout seems highly unlikely .

{kind=link}

It's also worth noting that Sabina has a track record of adding ounces at the cost of just ~$20/oz, which is certainly nice when the cost to get them out of the ground is likely closer to $850/oz on an all-in-sustaining cost [AISC] basis. Meanwhile, this project looks to have considerable exploration upside, and banded-iron formation-hosted gold deposits can be massive, as we've seen with the Homestake Mine in South Dakota (40 million ounces of gold produced before its closure) and the Musselwhite Mine in Ontario (~5.0 million ounces of gold produced to date).

So, with a low discovery cost for Sabina, considerable upside at depth near the mine, and triple the iron formation length at its George Project (vs. its main project under construction, which is Goose), Sabina is in a position to grow resources and net asset value per share despite higher drilling costs. This makes it unique vs. other developers, and with the company able to drill using cash flow vs. equity raises now that it's a near-term producer, Sabina has separated itself from the explorer/developer group finally, which is an area of the sector (as discussed above) that has become less desirable from an investment standpoint.

Recent Developments

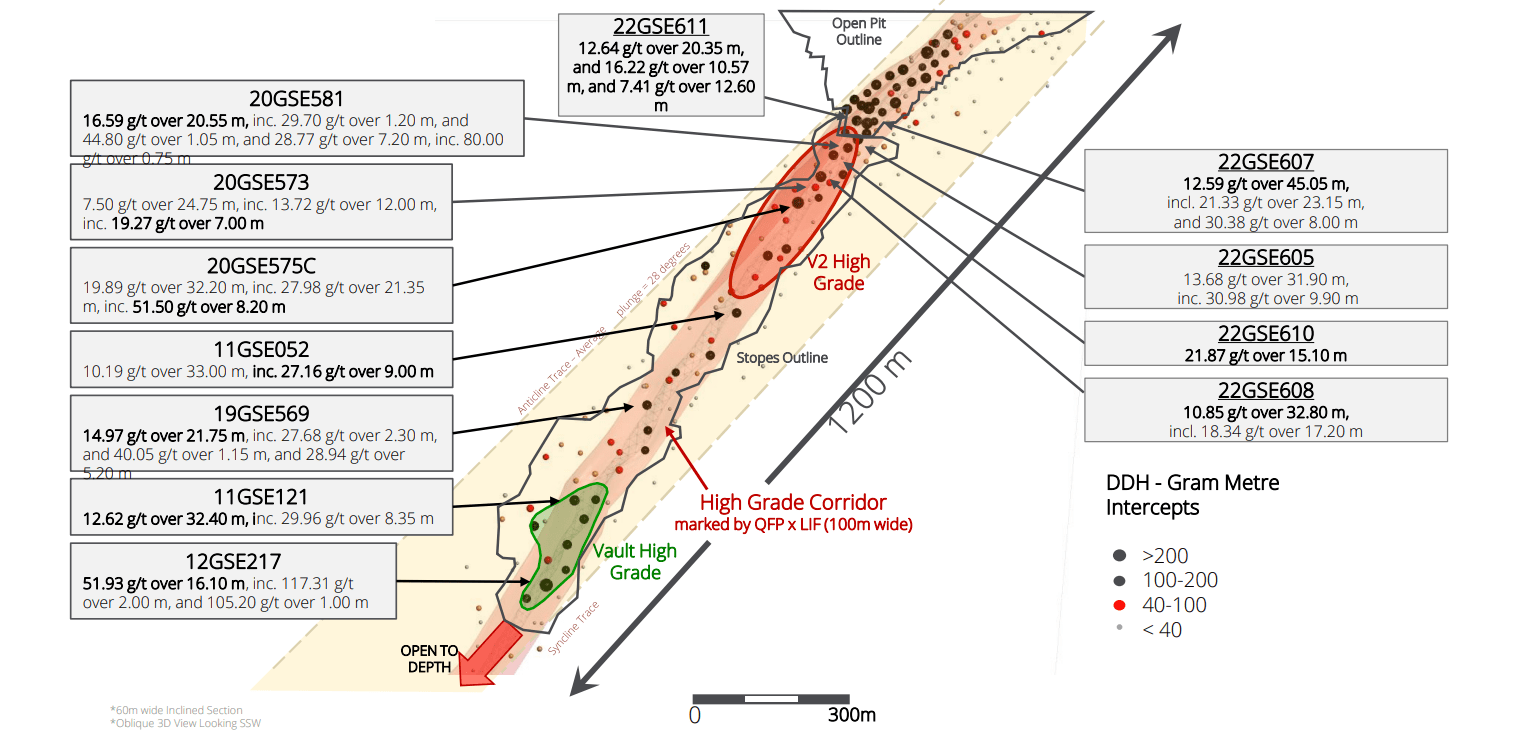

Digging into recent developments, there are a few key takeaways worth discussing. The first is that Sabina has continued to see exploration success at Umwelt, with highlight intercepts including 20.35 meters at 12.64 grams per tonne of gold, 31.9 meters at 13.68 grams per tonne of gold, 32.80 meters at 10.85 grams per tonne of gold, and 15.10 meters at 21.87 grams per tonne gold. These intercepts are all in the lower portion of its Umwelt Open Pit or in the V2 high-grade corridor just beneath the open pit, suggesting Umwelt's grades appear to improve at depth, with highlight hits like 32.20 meters at 19.89 grams per tonne gold, 7.00 meters at 19.27 grams per tonne of gold, and 20.55 meters at 16.59 grams per tonne of gold drilled further at depth.

{kind=link}

Umwelt Underground is expected to be mined by cut & fill, and these impressive grades that are well above the current reserve grade suggest the possibility of increasing Goose's production profile (currently ~315,000 ounces for the first five years) with incremental tonnes fed to the mill at higher grades. Also worth noting is that Hook and Wing are two new opportunities that could add further ounces to the project, and both are also showing solid grades over very mineable widths. Lastly, Sabina has re-opened the George Camp with drilling set to begin this spring, providing a steady stream of drill results during what's otherwise often a quiet period as a company focuses on construction.

As it stands, Sabina already has ~6.9 million ounces at Goose, but this number could easily grow to 9.0 million ounces post-2025 as new high-grade resources enter its mineral inventory.

Secondly, from a development standpoint, Sabina recently completed a lump-sum bid agreement for materials and labor for plant construction and ancillary buildings for ~$106 million, only slightly above the previously planned cost in its 2021 Study. While the contract has a rise and fall mechanism and other mechanisms to adjust for changes in bid quantities due to design growth and scope changes, this contract has further de-risked the project, in addition to the fact that procurement was 90% completed as of November. Meanwhile, Sabina noted that underground development is advancing well, with 1,200 meters complete, and the first lateral access to the Umwelt Zone has commenced.

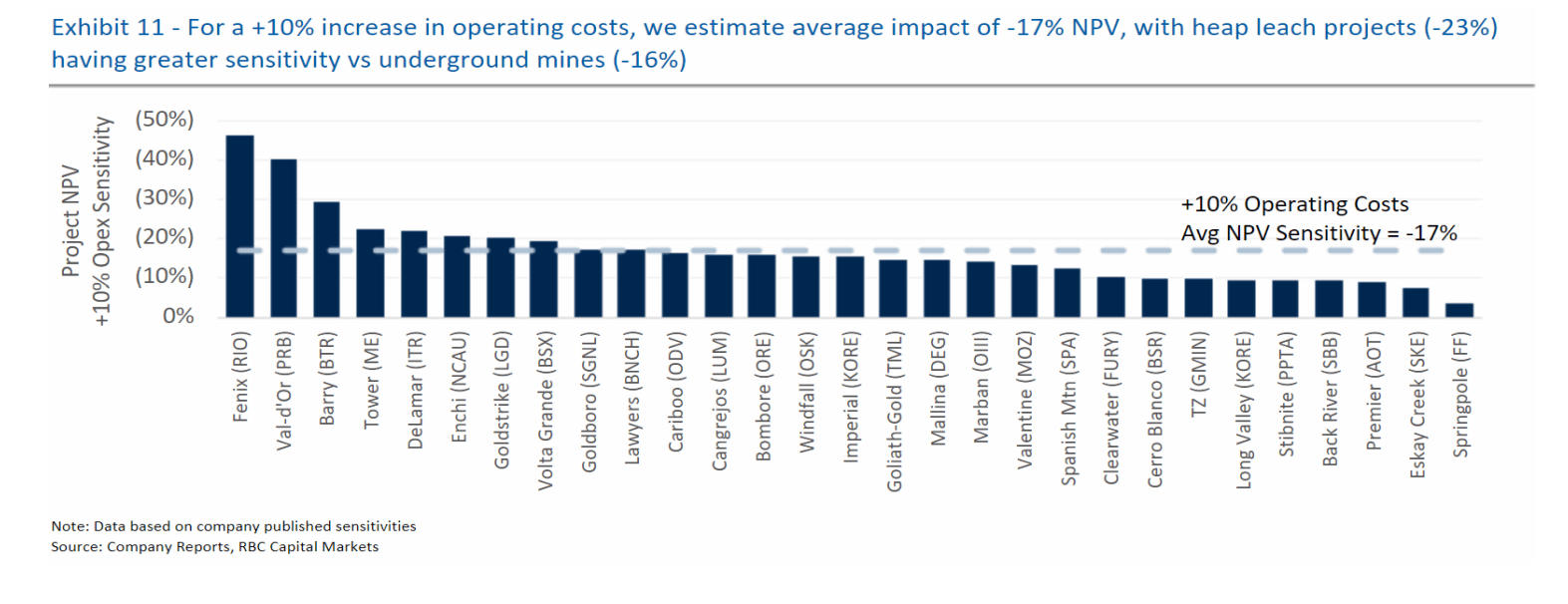

In terms of avoiding capex blowouts as we've seen from Marathon Gold (MGDPF), IAMGOLD ( IAG ), and Argonaut ( OTCPK:ARNGF ), it's worth noting that Sabina's remote location actually benefited it from an inflationary standpoint given that diesel, equipment, and other materials must be acquired and sent over in seasonal sealifts. This meant it brought critical components to the site even ahead of major construction starting this year, reducing the impact of inflationary pressures. Lastly, while higher-volume heap-leach development projects are very sensitive to increases in operating costs from inflationary pressures, this isn't the case for most underground mines, with Sabina being less at risk than other peers like Rio2 ( OTCQX:RIOFF ), DeLamar ( ITRG ) that have yet to begin construction of their projects.

The latter point suggests that while cash costs of $679/oz and AISC of $775/oz are likely too ambitious given the impact of inflationary pressures (even when factoring in the benefit of higher grades and a 4,000 tonne per day plant build at the onset vs. Year 3), this project is still highly profitable at whatever bear case gold price that one chooses to use even after incorporating for inflationary pressures. This is important because many projects and operating mines may need to see major changes to their mine plans due to the impact of inflationary pressures, but given Sabina's industry-leading grades (6.0 grams per tonne gold), and relatively low operating costs compared to its per tonne rock value (~$107/tonne operating costs vs. $350/tonne rock value), there's a lot of margin for error even if operating costs are higher or the mine slightly underperforms estimates in the FS.

Opex Sensitivity - Undeveloped Gold Projects (Sabina Presentation, RBC, Company Reports)

{kind=link}

The last point worth discussing is that Sabina is quite de-risked from a production standpoint, given that it will have two years of stockpiles sitting ready to be processed once gold production begins. This is due to Goose's unique setup, with a plan to store thickened tailings in pits as they become available, with the Echo Pit set to be mined out as a tailings storage facility before processing begins in 2025. So, with underground development being well advanced already, the benefit of having a large stockpile in case mining rates come in below plans and the project is fully funded even if capex comes in closer to $500 million ($466 million estimate), there are lots of things to like about the Sabina story, and this is about as de-risked as it gets in terms of investing in a gold developer.

Valuation

Based on ~567 million fully-diluted shares and a share price of US$1.05, Sabina trades at a market cap of ~$595 million, a dirt-cheap valuation for a company that could generate upwards of $150 million in average annual after-tax free cash flow in the earlier years of its mine life. If we compare this to an estimated fair value of ~US$1.14 billion ($1,725/oz gold), which includes $330 million in upside related to its George Project and resource growth, this leaves Sabina trading at a near 50% discount to fair value. This represents a meaningful margin of safety for a well-advanced developer, and I would argue that Sabina can command a P/NPV multiple of 1.0x once nearing its first gold pour, given its exceptional economics. The result is a fair value of US$2.00, assuming ~570 million fully-diluted shares.

{kind=link}

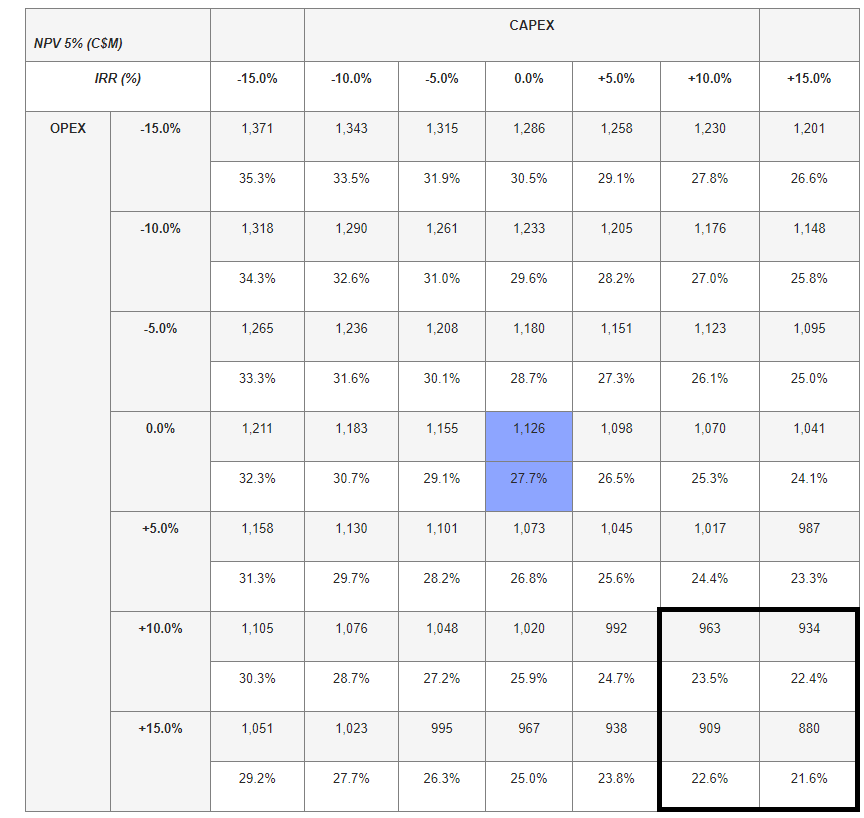

Back River Project 2021 Study -- Capex/Opex Sensitivity (Company Filings)

However, it's worth noting that this valuation assumes that we will see cost inflation from the initial capex estimate ($464 million) and that we will also see higher costs from a sustaining capital and operating cost standpoint due to inflationary pressures. I think these are very fair assumptions, and I think it's safer to assume an upfront capex of at least $510 million to be on the safe and at least 10% higher operating costs. That said, there are opportunities to boost NPV (5%) outside of the higher gold price that isn't factored into this valuation, and they are as follows:

1. The company continues to see exploration success at Umwelt, with a high-grade zone (V2) identified just beneath the Umwelt open pit, with the potential to pull these ounces forward in the mine plan. These ounces appear to be much higher grade than the reserve grade (5.97 grams per tonne of gold), potentially providing a material lift to production early in the mine life.

2. Sabina's mine plan is based on a 4,000-tonne-per-day throughput rate, representing just two-thirds of its permitted throughput rate of 6,000 tonnes per day. Even assuming the company was to increase capacity to 5,000 tonnes per day (1/2 of additional capacity) post-2028, this could provide a ~65,000-ounce increase in Goose's incremental production, assuming a 6.0 gram per tonne feed grade.

3. While much longer-term, the high-grade George Project could be a satellite or stand-alone opportunity depending on its size, which could justify an increase in throughput to 6,000 tonnes per to accommodate higher additional high-grade material from this nearby project.

While there's no guarantee that the company will optimize its mine plan, expand its plant, or turn George into its second mine, the first opportunity could push annual production above 370,000 ounces per annum (earlier years of mine life). Meanwhile, the second and third opportunities could allow this operation to maintain a 300,000+ production profile over the mine life vs. ~223,000 ounces over the life of the mine based on the 2021 mine plan. Hence, I would argue that this 18-month target price of US$2.00 is conservative and points to a 90% upside from current levels.

Summary

Sabina continues to be one of the most advanced gold developers in the sector, and the company benefits from a district-scale land package that makes it highly attractive to potential suitors. This is based on the potential for multiple mines (Goose and potentially George) over multiple decades at industry-leading margins due to the phenomenal grade profile of these deposits. Given this setup, I continue to see Sabina as a top takeover target. However, with Sabina fully-funded and development underway, the story has a second dimension to it, given that it finally controls its destiny, meaning there are two paths to a substantial upside re-rating.

To summarize, I see Sabina as one of the more attractive names under a $1.0 billion market cap sector-wide, and I would view sharp pullbacks as buying opportunities.

For further details see:

Sabina Gold & Silver: Buy The Dips