SAIA - Saia: Great Company But The Market Is Too Optimistic

2023-12-29 10:56:13 ET

Summary

- Saia, Inc. is a North American transportation company specializing in LTL, with 95% of revenue coming from LTL services.

- In 2022, Saia achieved record highs in gross profit, operating profit, net income, free cash flow, and returns on capital.

- The company has a low risk profile, but low insider ownership and high multiples make the stock less attractive at its current price.

Saia, Inc. ( SAIA ) is a North American transportation company that specializes in LTL. 95% of their revenue comes from LTL, with the rest coming from various logistics services. They operate close to 200 terminals, with 27,000 tractors, trailers, and forklifts. They employ around 30,000 non-unionized employees.

Below are the returns since IPO in 2002, followed by the period of best returns:

dividend channel

dividend channel

Here is how SAIA’s market share looks in the industry:

SAIA investor presentation

Next let's look at the return metrics versus peers:

| Company |

| Revenue 10-Year CAGR |

| Median 10-Year ROE |

| Median 10-Year ROIC |

| EPS 10-Year CAGR |

| FCF/Share 10-Year CAGR |

| SAIS |

| 9.8% |

| 15.6 |

| 12.7 |

| 26.4% |

| 19.7% |

| 11.4% |

| 21.2% |

| 20.8% |

| 26.2% |

| n/a |

| 0.4% |

| 13.1% |

| -7.8% |

| n/a |

| -5.5% |

| 39.4% |

| 6.7% |

| 2.5% |

| n/a |

| n/a |

| 9.9% |

| 8.7% |

| 6.4% |

| n/a |

| 20.4% |

In 2022, SAIA hit a record high for the following: gross profit, operating profit, net income, free cash flow, and returns on capital.

Capital Allocation

Below we look at how capital was allocated over the past decade:

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| EBIT |

| 74 |

| 86 |

| 90 |

| 79 |

| 95 |

| 141 |

| 153 |

| 180 |

| 335 |

| 470 |

| FCF |

| -25 |

| 4 |

| 56 |

| 26 |

| -29 |

| 33 |

| -15 |

| 78 |

| 97 |

| 106 |

| Acquisition |

| 22 |

| Repurchases |

| 3 |

| 1 |

| 1 |

| 1 |

| 3 |

| 4 |

| 7 |

| 12 |

| Debt Repayment |

| 246 |

| 14 |

| 68 |

| 36 |

| 225 |

| 46 |

| 681 |

| 758 |

| 107 |

| 20 |

| SBC |

| 3 |

| 4 |

| 4 |

| 5 |

| 5 |

| 6 |

| 6 |

| 8 |

| 9 |

| 9 |

As we can see, they’ve made infrequent acquisitions, never paid a dividend, never aggressively repurchased shares, but have continuously been paying down debt. So far the capital allocation must be commended simply because of how earnings have compounded. ROIC has been above 20% for the past two years, so now will be the true test to see if they can reinvest at incrementally high rates.

Risk

The fundamental risk is very low with this business. Losing market share over time is possible, but that would merely slow the growth rate at this point, not shrink the revenue.

In 2022, the company hit all-time highs in terms of revenue, profits at all levels, and returns on capital. This is a company where again I see an overlap of being cyclical, yet a long term compounder as well. The cyclical risk is real, but this stock is less volatile than many other cyclicals.

I wouldn’t call it a red flag, but the low percentage of insider ownership (0.4%) is something I don’t like to see. High insider ownership is no guarantee of success, but for a company this size of such quality, I personally prefer seeing more skin in the game.

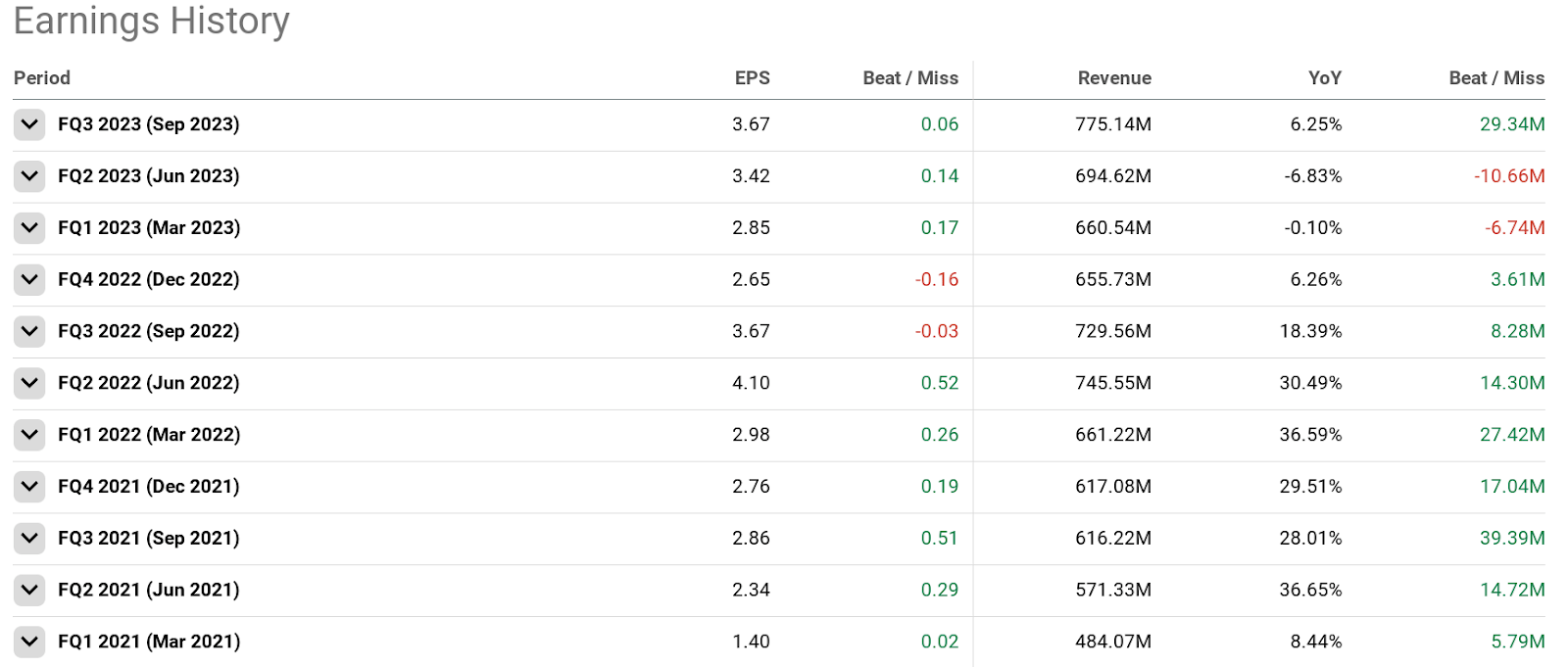

Q3 Earnings

They had a smaller than usual beat last quarter, but I don’t expect any major drop in EPS in the near term.

{kind=link}

Seeking Alpha

I expect strong earnings for the next few quarters, but as I will get to in the valuation section, I welcome a couple of misses which sets up a better entry point.

Valuation

First we’ll look at the multiples comp versus peers, followed by the DCF model:

| Company |

| EV/Sales |

| EV/EBITDA |

| EV/FCF |

| P/B |

| Div Yield |

| SAIA |

| 4.2 |

| 19.1 |

| 98.4 |

| 6.5 |

| n/a |

| ODFL |

| 7.7 |

| 22.9 |

| 75.4 |

| 11.1 |

| 0.3% |

| XPO |

| 1.6 |

| 13 |

| 305.4 |

| 8.7 |

| n/a |

| ARCB |

| 0.6 |

| 8.5 |

| 21.9 |

| 2.4 |

| 0.3% |

It’s no surprise that SAIA has such high multiples, since share prices recently hit an all-time high. The market is bullish on the stock from a multiples perspective, so let's look at the DCF next:

moneychimp

My EPS estimates are very optimistic, yet the market is wildly more optimistic than me. This leads to me apply a “hold” rating on the stock, but it is definitely worthy of going on the watch list of any serious growth and/or quality investor. The returns on capital are great right now, but this business will inherently tend to grow assets faster than revenue, and at some point this will drive those returns back down.

The runway is long enough for good growth, but there will be a tipping point where more capital will be needed to fund slower growth.

Conclusion

I personally love learning about market crushing compounders that achieved success in a non-sexy industry. SAIA is a great example of this, but the market is far too optimistic about future success. This year they hit a record high share price, but this has pushed the price up too much for me to consider right now.

The high multiple and record share price are no surprise given the great results recently

For further details see:

Saia: Great Company, But The Market Is Too Optimistic