COM - SandRidge Energy: Oil Production Growth Offers Upside With Hedged Natural Gas Downside

Summary

- SD is selling off with natural gas producer equities.

- The company is growing oil production quickly.

- SandRidge has much of its natural gas price exposure hedged.

- Opportunity for outperformance as this is recognized.

SandRidge Energy: Oil Production Growth Offers Upside with Hedged Natural Gas Downside

With natural gas prices in free fall, investors are rightfully concerned that gas-weighted producer profits could suffer materially, particularly as the forward price falls too. Gas prices are volatile and notoriously hard to predict, and we take no directional view on their trajectory in the short to medium term. However, SandRidge Energy ( SD ) is likely to successfully navigate this turbulent market environment due to its opportunistic hedges and rapid oil production growth.

SandRidge significantly increased its capital budget in mid 2022 to invest in incremental oil production, and now its oil production has already inflected. As its oil production grows, SandRidge’s cash flow is becoming less sensitive to lower gas prices while offering more torque to higher oil and natural gas liquids pricing.

Additionally, SandRidge’s management opportunistically hedged a portion of its gas production, offering downside protection in a low-gas price environment as oil production grows and free cash flow is generated. Despite this oil production growth and a large, growing net cash position, SandRidge has continued to trade in-line with gas-weighted peers, offering a compelling opportunity here.

SandRidge Q4 2022 Forecast

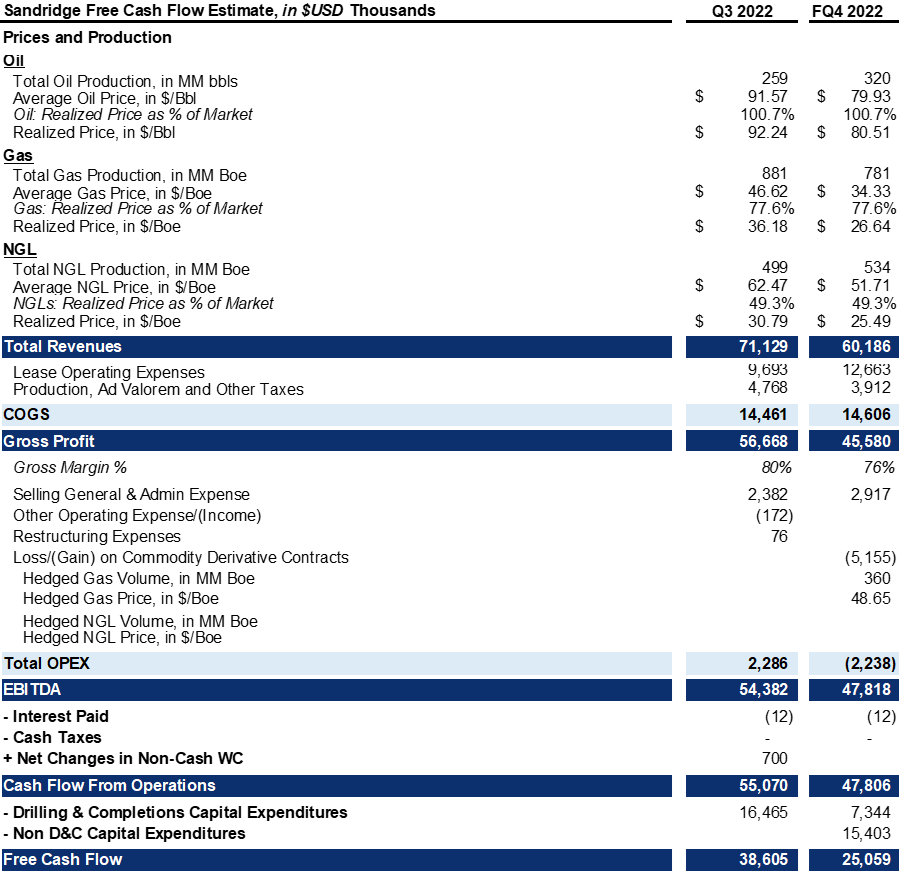

It is helpful to review SandRidge’s Q3 2022 cash flow and likely Q4 cash flow based on prevailing commodity prices. Below an estimate of SandRidge’s Q4 cash flow based on commodity prices at the time, and management production and cost guidance:

{kind=link}

As can be seen above, SandRidge may see a modest decline in cash flow from operations ((CFO)) despite significantly lower oil & gas prices and higher cost guidance. Free cash flow ((FCF)) is projected to decline materially due to higher capital expenditures, discussed in detail below.

The decline in revenues due to lower market prices is likely to be partially offset by SandRidge’s natural gas hedges. These covered roughly half of SandRidge’s forecasted Q4 production at a favorable price above $8/MMBtu, while the prevailing market price is around $2.4/MMBtu at the time of writing. And with hedges rolling off in March 2023, these may continue to offer SD stock significant downside protection if gas prices remain low in Q1 2023.

SandRidge’s management has a successful hedging track record. SandRidge was previously unhedged while gas prices were on the rise, and subsequently hedged roughly half of the company’s natural gas production when prices were near their peak. This certainly helps on SandRidge’s path of net cash builds and oil production growth.

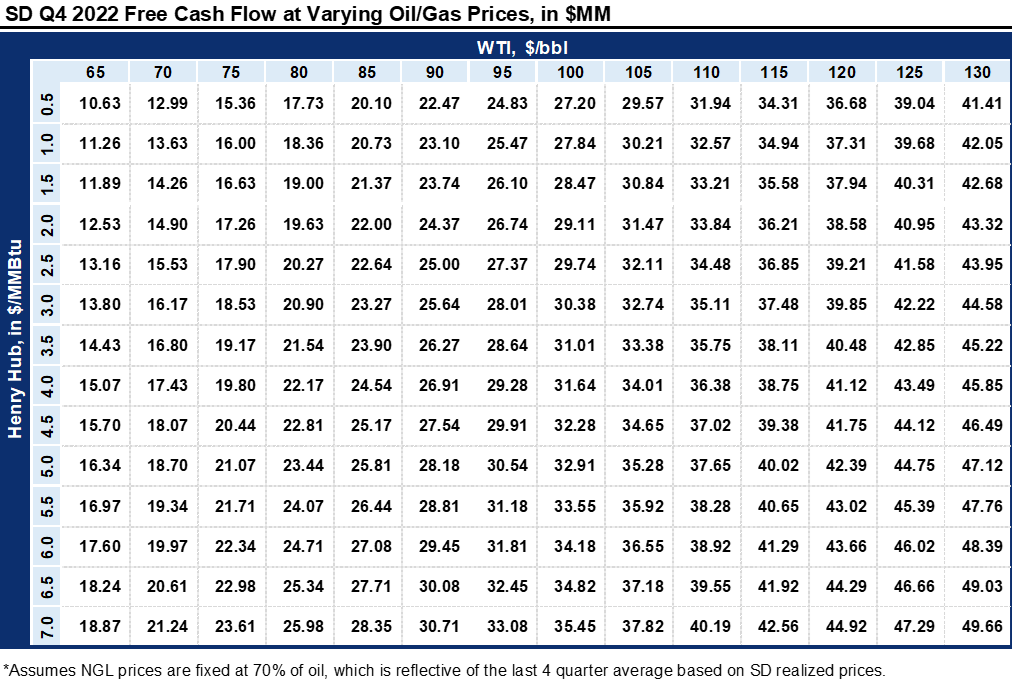

With its current hedges, SandRidge continues to offer significant torque to higher oil and gas prices. We sensitized our estimate of SandRidge’s Q4 FCF to a range of oil and gas prices, to illustrate what could happen to cash flow in subsequent quarters in future quarters:

{kind=link}

Oil Production Growth

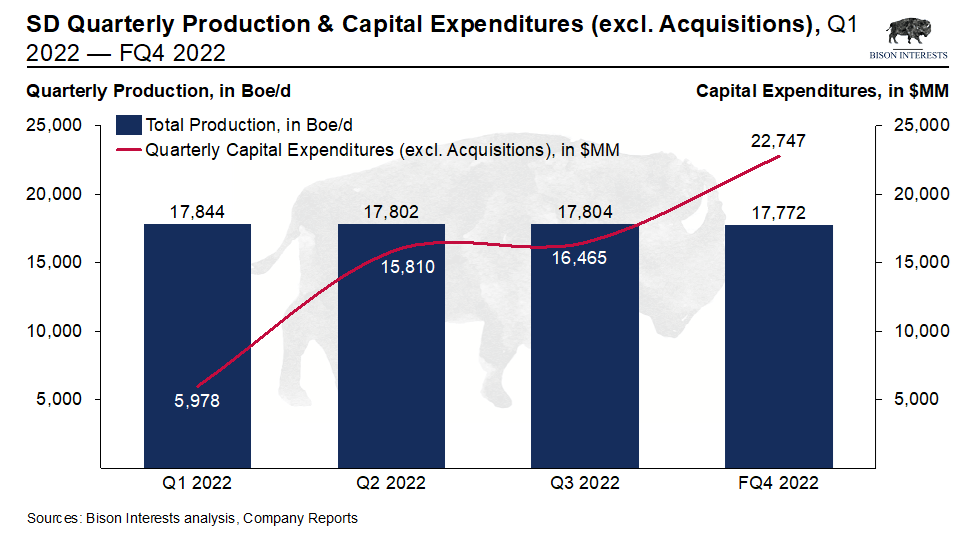

SandRidge’s overall production including natural gas, natural gas liquids and oil, has in aggregate been flat over the last year, while its capital expenditures have increased materially:

{kind=link}

At the surface level, this could be concerning for some investors. However, a closer look reveals that even though overall production remains flat, SandRidge’s oil production has been inflecting:

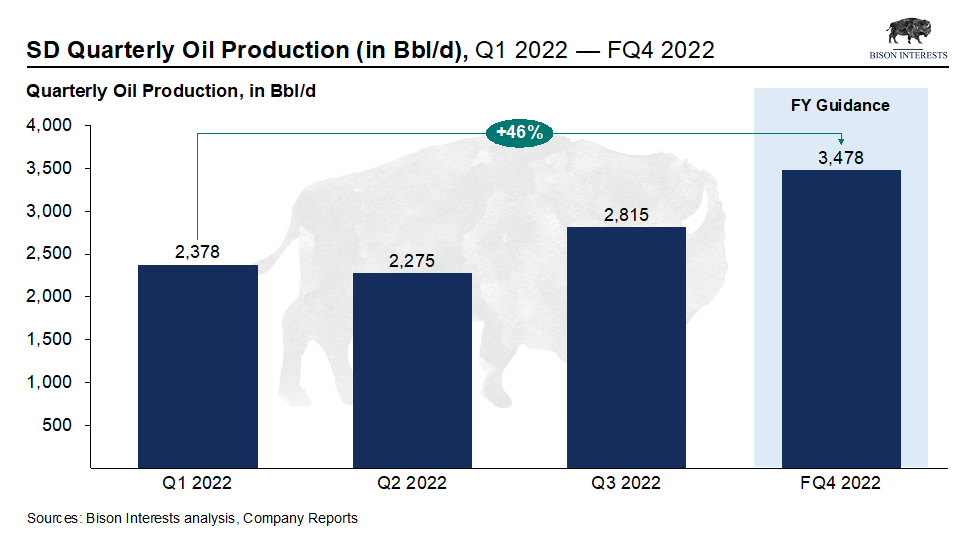

{kind=link}

In early Q3 2022, SandRidge increased its capital expenditure guidance to $56-70MM from $41-50MM, as it announced it was drilling 3 additional oil wells, re-activating and optimizing other wells that were previously shut in and completing artificial lift conversions. These wells were drilled and brought on production successfully, benefiting SandRidge with a 24% increase in oil production in Q3, as can be seen above. And SandRidge’s oil production is expected to increase another ?24% in Q4, as per management’s full year production guidance.

It is noteworthy that SandRidge has been using its capital budget to increase oil production, which in the current commodity price environment is its highest margin product. Its overall margin profile is rapidly improving, while many are fixated on its flat overall production and higher capex. This high margin growth substantially increases the value of SandRidge’s future production, particularly when considering the compelling macroeconomic setup for oil, which may result in higher prices.

Growing Cash Balance and NOLs

With a ?$570MM market cap at the time of writing, we estimate SandRidge is trading at a ?20% FCF yield on equity, using our Q4 estimate 2022 YTD FCF. Additionally, SandRidge had accumulated over $1.5B in net operating losses, which will continue to shield it from tax liabilities in successive quarters. These are increasingly valuable in the context of the risk of windfall profits taxes on oil and gas producers.

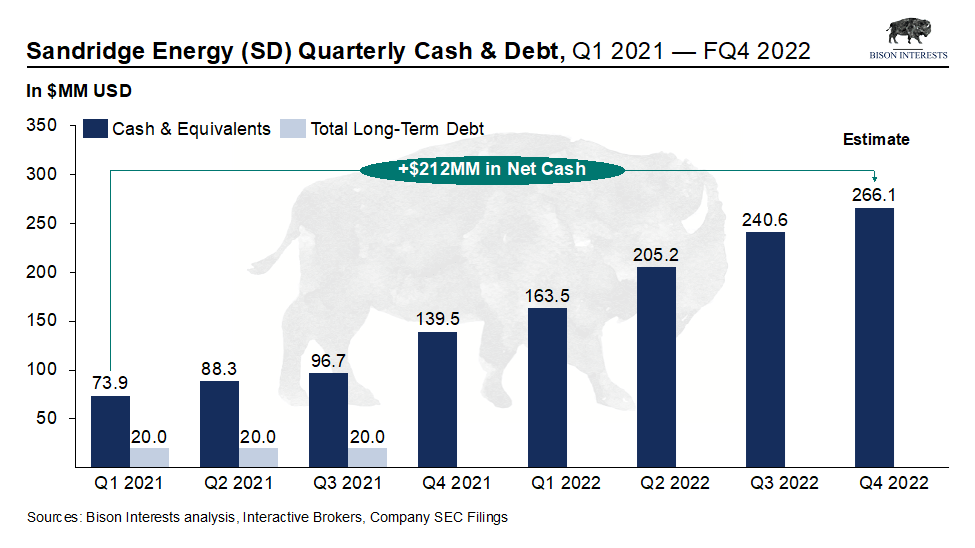

Even with significantly higher capital expenditures, it looks like SandRidge had ?$7.2 per share in net cash (and no debt) at the end of Q4 2022. With a share price of ?$15.5 at the time of writing, SandRidge has almost half of its market cap in net cash! This offers SandRidge flexibility to acquire assets if the opportunity arises, or to use its cash balance to buy back shares or pay dividends:

{kind=link}

Compelling Opportunity:

In the current environment, SandRidge is one of the few publicly traded oil and gas producers offering both downside protection to lower gas prices, and oil & gas price upside as it invests in increasing oil production. In the current oil & gas price environments, this may lead to higher-than-expected cash flow even if its overall production remains flat, despite common misconceptions likely lingering from bankruptcy in 2016.

And despite a likely decline in FCF due to lower commodity prices and higher Capex, SandRidge’s FCF yield and oil production growth remains high. Having generated significant cash flow and been debt-free for several quarters now, SandRidge has the flexibility to either return capital to shareholders or buy assets to grow production, while offering unusual downside protection from its large net cash balance and hedges.

For further details see:

SandRidge Energy: Oil Production Growth Offers Upside With Hedged Natural Gas Downside