SAN - Santander: A Bank With Still-Existing Upside

Summary

- Many of the financial companies I've been positive about for the past few years have gone firmly into overvalued territory. This includes European banks.

- One of the exceptions to this pattern is Santander, a Spanish bank I've been writing about a few times over the past few years.

- While Santander is no longer troughing, and while I'm already up quite a bit on my position, the bank is still a "Buy" for 2023. Here is why.

Dear readers/followers,

It's been about a year since my last update on Santander ( SAN ). While I have been writing only about an article a year on the bank, I've stayed continually positive and slowly added to my position. As of yet, the bank has not reached levels I would consider valid for any sort of rotation or trim. This means that I'm very happy to hold an undervalued, quality financial institution at a low cost/price, and wait for it either to normalize or to keep harvesting attractive dividends.

There's no doubt that Banco Santander isn't as safe as, say, Allianz ( ALIZY ) or other European Financial institutions, but this does not equate to this bank not being investable.

Let's go into the 2023 thesis for Santander.

Santander - Why the bank remains a "Buy" here

Southern-European banks, whether they be Spanish or Italian, have never been of much appeal in some investors' minds, especially international ones. The associated geopolitical uncertainties and scandals have done its part to scare many people away from investing in them. I would definitely say that you don't want to invest in any bank or company here, but Santander is somewhat different.

It has a market-leading or close to a market-leading position in every single legacy market it works in. It's on the top list here for loans in not only Spain and Portugal, but Italy, Poland, the UK, and the LATAM area, and also has branches and exposures to Germany and Scandinavia.

While some of you might think that Santander stock must have suffered greatly during the financial crisis, this was actually not the case. Santander went through 2008-2012 with below-average earnings volatility. It has superb diversification and strong risk culture. Therefore, ironically, Santander actually did significantly better than banks who initially were viewed as being able to handle a crisis, but in the end, weren't.

I became positive about banks like this and companies from Southern Europe quite early. They're somewhat more volatile and fickle investments than you might be used to - but the returns they can grant you if invested at the right time, are nothing short of amazing. The one difference to Scandinavian banks, which I consider to be higher in quality and in safety, is that Santander targets CET-1 of around 11-12%, while most Scandi banks never go below 15%. But this is not uncommon on an international level, so I won't fault Santander for going by those numbers and targets.

From a revenue segmentation perspective, Santander is a retail-reliant bank. We have 4Q22/FY22 results, and they were excellent.

Why?

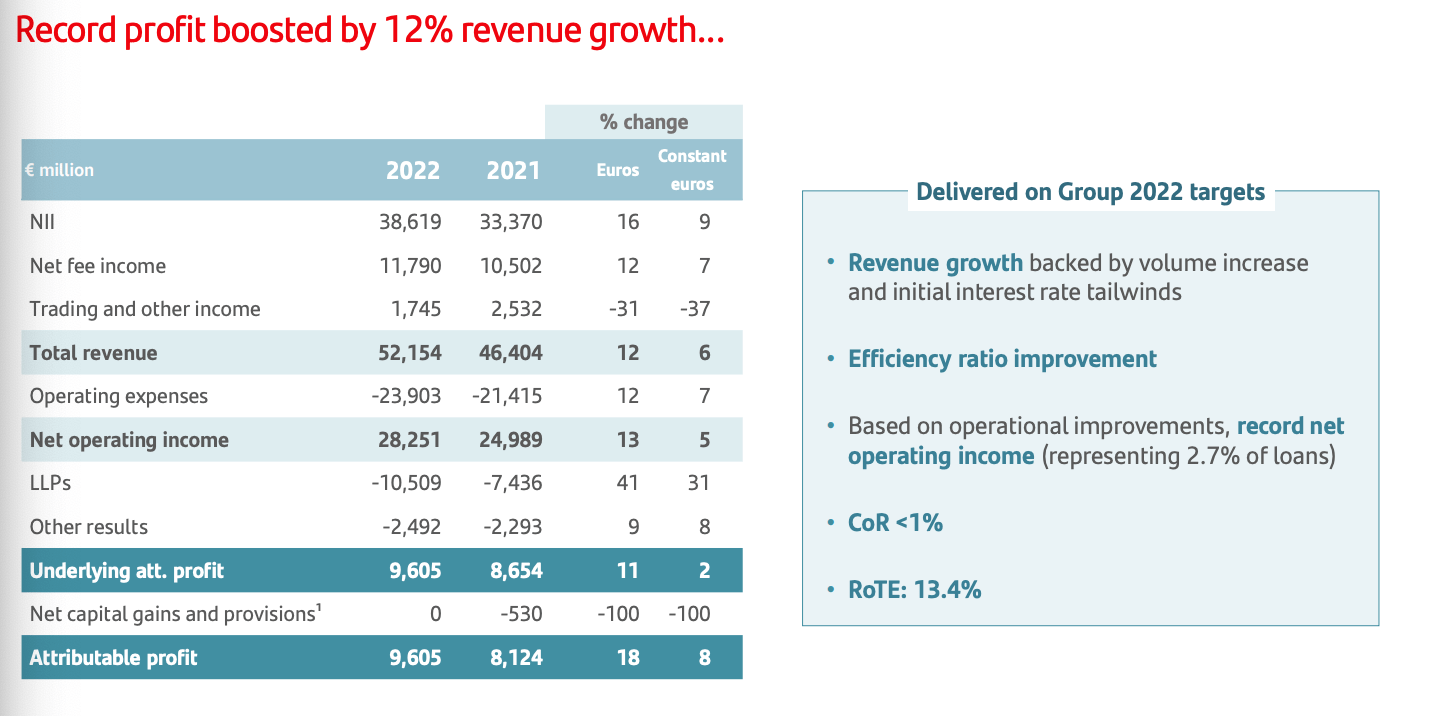

Because Santander delivered record profits during 2022, with a record €2.3B in 4Q22. The bank's 2022 was a year of increased profitability, shareholder value, and returns which saw EPS grow by 23%. That's a feat not achieved by many companies, even finance ones, during this last fiscal. The company further solidified its already-excellent balance sheet and delivered revenue growth year-over-year of 12%. That's amazing when considering the macro environment. Attributable profit for the full year was close to €10B.

{kind=link}

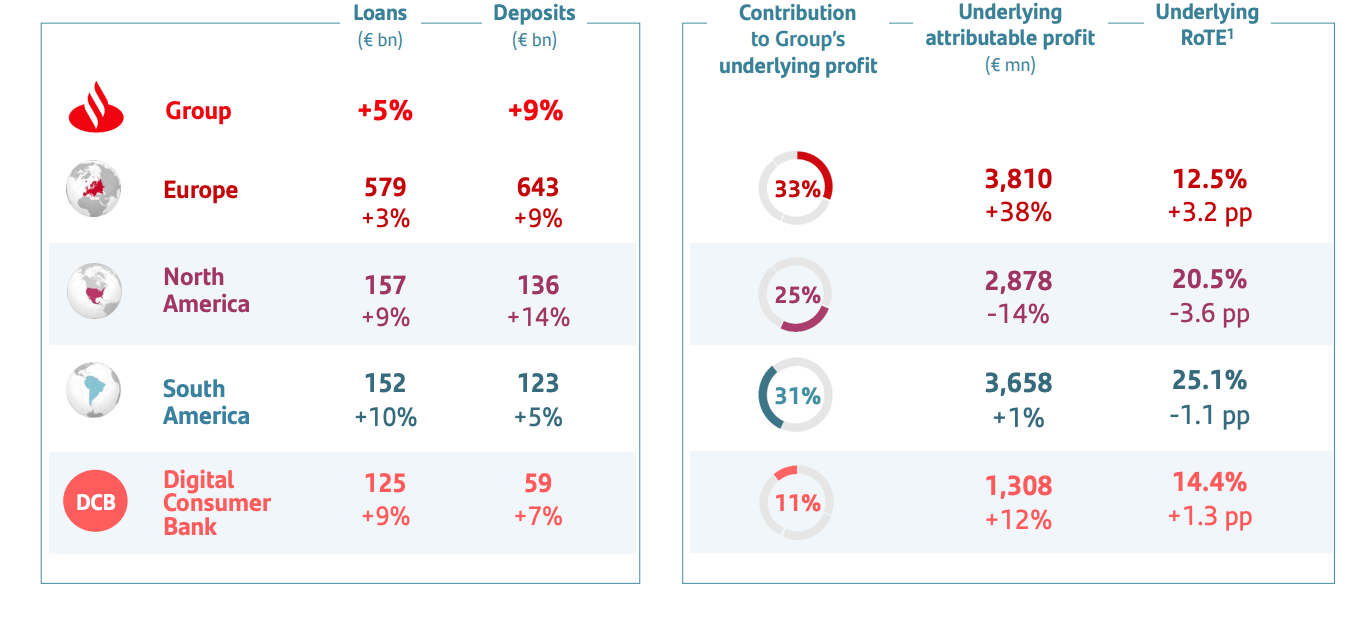

The company has taken an offensive approach to green financing and ESG, leading it to be the #2 global leader in renewable financing, and over €5B in financing exposure to EVs alone. Here's a high-level overview of the development for Santander in terms of regions - and you can see, those developments are nothing short of amazing.

{kind=link}

All business regions are contributing to growth here. Underlying reasons for growth are a combination of volume and interest rate/macro trends. The higher interest rates are in particular benefitting UK, Poland, and LATAM, but not yet fully reflected in many other areas, which mean that more positive is to come. However, both NII and NIM numbers are up, with deposits growing by almost 10%. People are also trusting more of their money to Santander in terms of private banking, with net new money of almost €12B in the private banking segment.

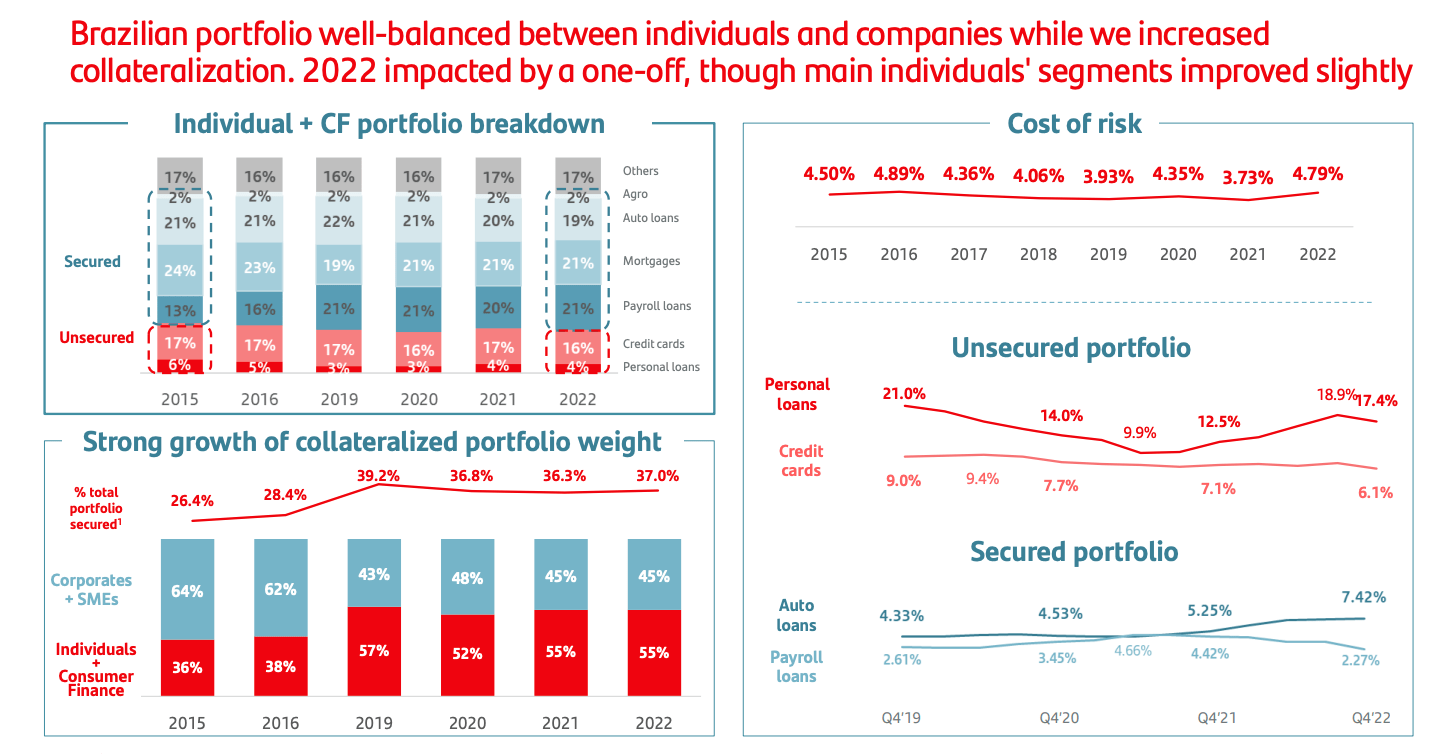

The bank's NPLs are somewhat higher than your typical NA or local European bank, due to the company's risk profile. We're at 3.08% as of December. That's still not worried as such, especially since it's down 8 basis points. 65% of the company's loan portfolio is investment-grade and secured, and 90% of the loans have LTVs of below 80%. There is currently about €100b worth of loans that are either in stage 2 or 3.

Santander has always had a somewhat higher risk profile to other banks - this is part of why some people tend to avoid it.

Me, I don't mind risk - I just want to know how it is being managed. Brazil is a good example of this. Banking and doing this sort of thing in Brazil is always associated with a higher risk cost, but Santander seems to have found a decent balance here, and a way to make a good profit without being too exposed to any one outsized type of risk.

{kind=link}

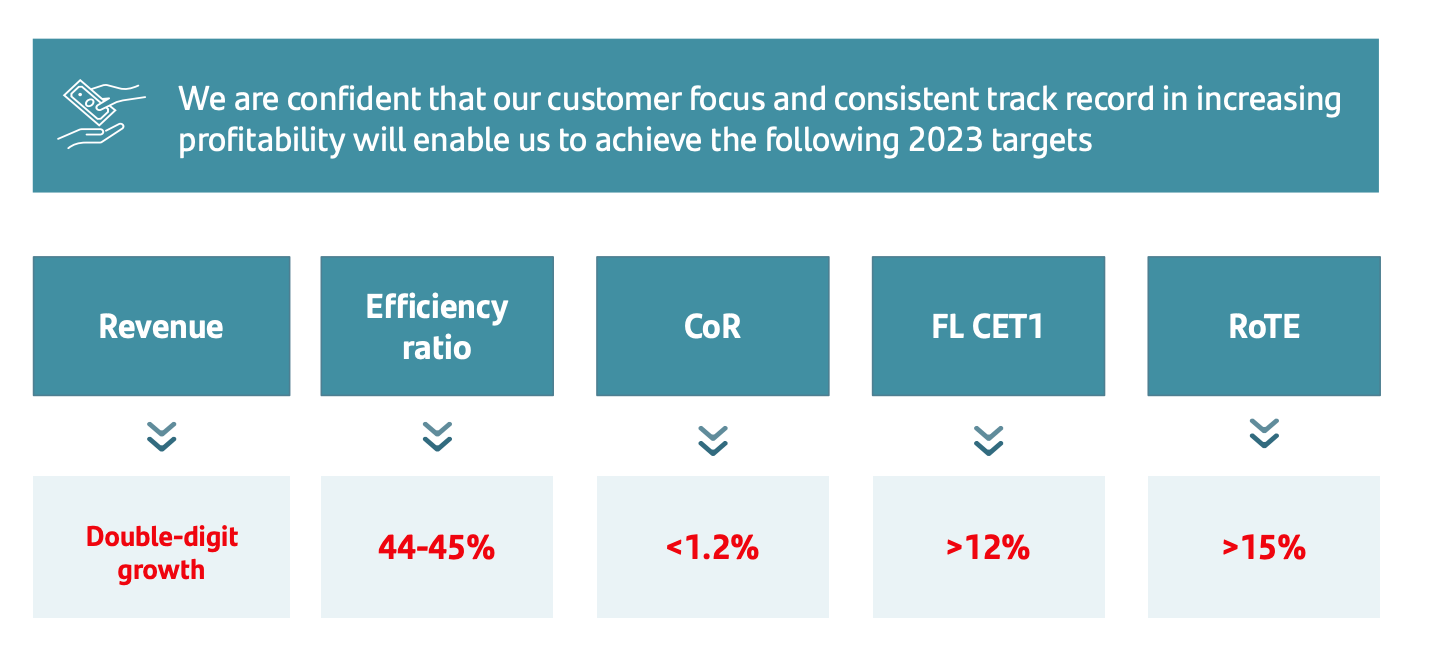

Santander delivered on every one of its 2022 targets. The company's customer base increased by 7 million in 2022 alone, and it's the top-3 bank in terms of NPS in 8 markets across the world. Santander has managed to go above 12% CET-1 while delivering the sub-1% CoR target, while achieving double-digit growth in revenues, RoTE of 13.4%, and a 23% increase in earnings. This resulted in a 16% increase in the suggested dividend from Santander.

What's more, the company believes and targets the same type of positive trend for 2023 as well.

{kind=link}

Given where the interest rates across the world are going, as well as other overall global trends, I do not see a reason why this wouldn't be the case for Santander in 2023, unless we see a marked turnaround.

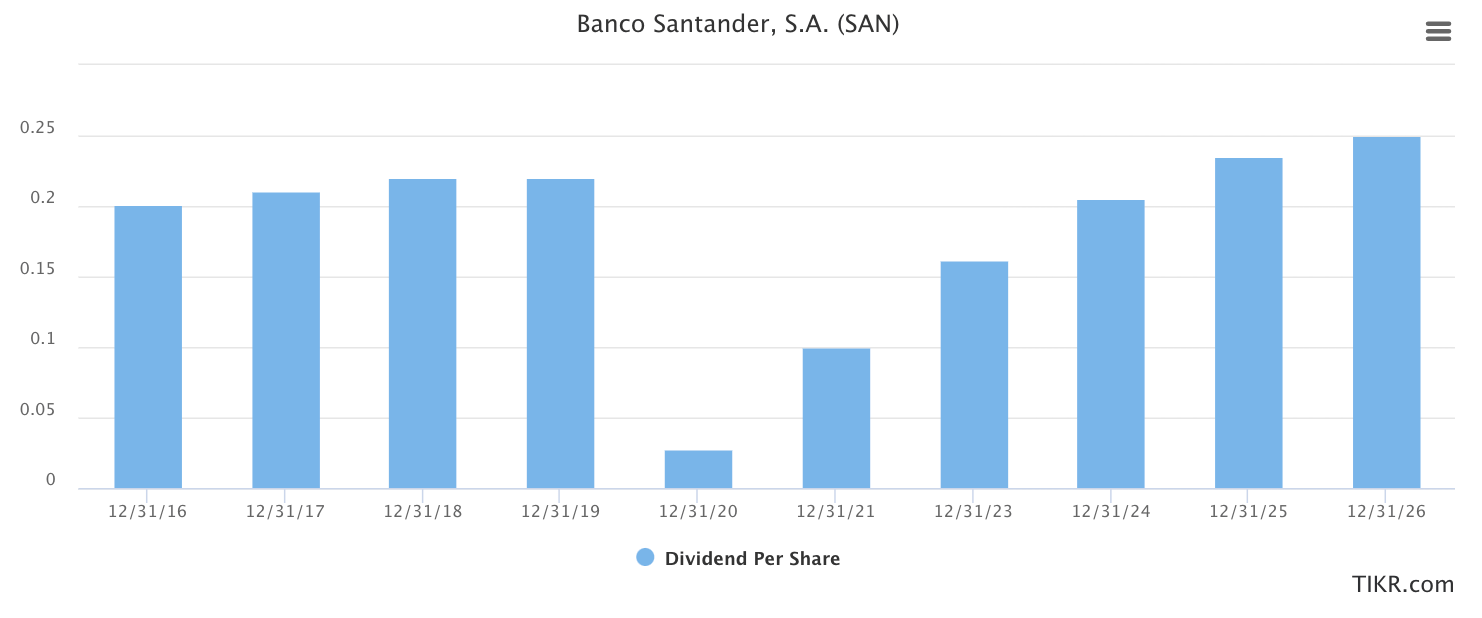

The company did right-size the dividend during COVID, but the dividend is coming back up to its normal levels. That means at this time, you're still buying the company cheap, but also not getting perhaps the full amount of dividend that you'll be able to expect later on once the bank goes further into the expected normalization.

{kind=link}

Getting profit from an investment like Santander is a multi-year venture, but once that profit materializes in full, it's my experience that it will not only outperform local markets, but international ones by far - all you need is the foresight and conviction to hold onto quality in the face of seeming danger. That's what I've been doing with Santander - albeit not as much as I perhaps should have had in terms of overall allocation.

With 2022 results in, and 2023 guidance given, and I'm saying that the bank is doing well and will likely continue to do well, here is my current valuation discussion for Santander.

Santander - The valuation for 2023

Santander has previously traded at some incredible discounts to peers due to its history of reducing the dividend, and I've given Santander upside targets of 50-100% before. I said in my earlier article that the company's earnings, even during COVID, vastly outperform any cut dividend the company has suggested. I also said that it's extremely unlikely that we'll see less than €0.15, which turned out to be exactly right.

However, some valuation concerns can be said to remain at this time, looking at the business.

From a NAV/SOTP valuation, we need to take the value of its major listed subsidiaries - which fluctuates wildly. Intrinsic value captures no more than a 2-3 year projection from current numbers, which due to the current environment, comes at a relatively high level of uncertainty. There still aren't that many bank majors with the sort of emerging market exposure that Santander has either, which really limits the peers we can fairly look at or consider here. My peer comps for Santander are HSBC ( HSBC ), BBVA ( BBVA ), and Standard Chartered ( SCBFY ) - and those aren't, as I see it, as good as Santander.

When I last wrote about Santander, it traded close to the nominal share price it does now. I specified that on a considered share price of €5/share, again very conservative, the conservative upside for Santander from around €3/share is well over 40%+.

This is still a realistic upside - it's not outlandish or in any way exuberant. It's based on normalization - no more.

Since last year, analysts have become far more positive on SAN. The company is followed by 20 of them, and they look at Santander having a clear upside to an average share PT of €4.30. We also see 15 of those 20 analysts at a "Buy" or equivalent target here, from a range of €3.01 low and €5.82 high. I believe this, still, fairly well captures the sort of upside we can see in Santander at this particular time.

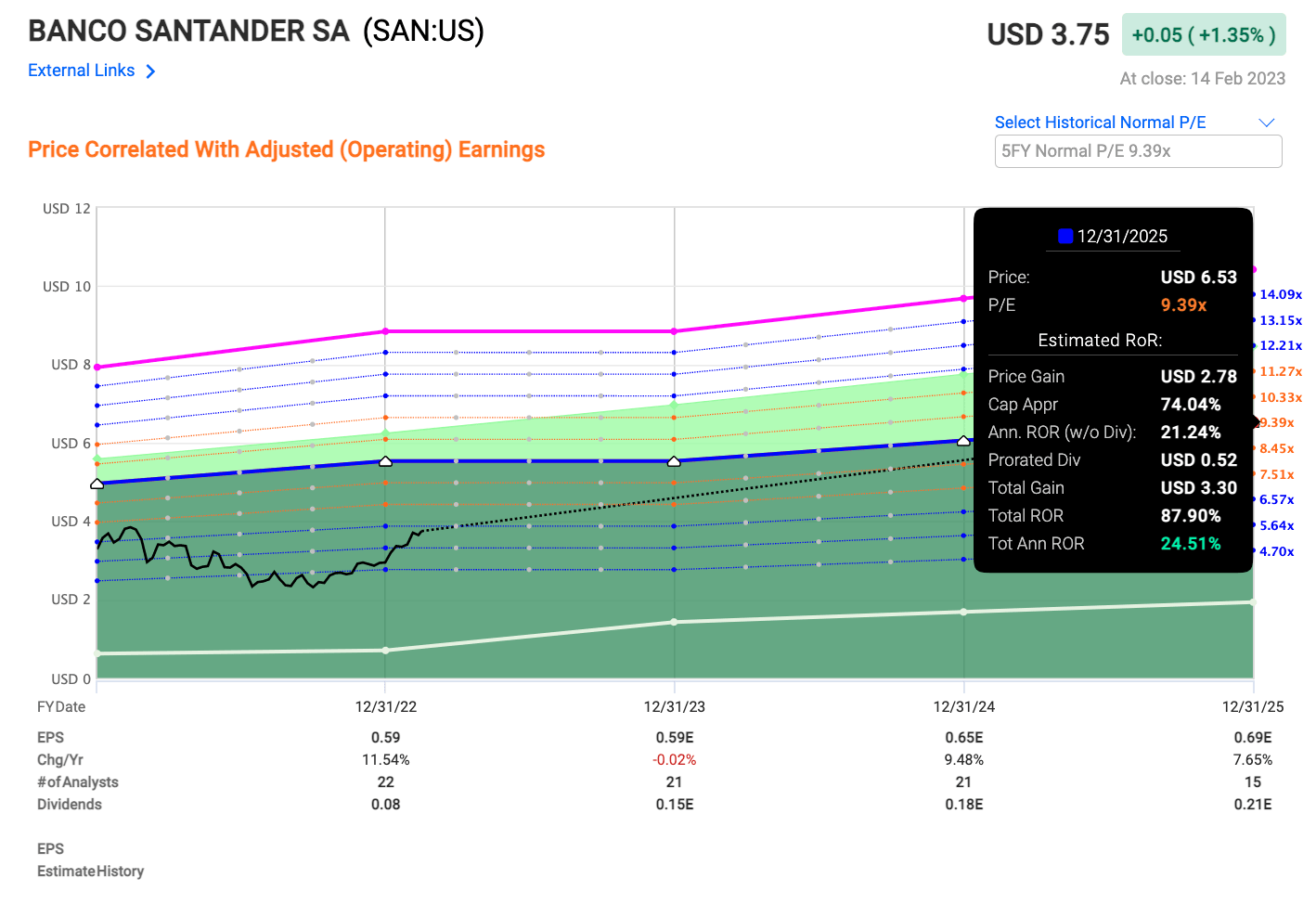

Remember, Santander is an A+ rated bank. This is not some local bank with bad credit - it's a global bank with one of the top ratings there is. And it has a conservative upside, even for the SAN ADR, of 24.51% per year, or close to 88% in total.

{kind=link}

So, that's the overall upside I see for the company here. I continue to argue that Santander is quite a long-term investment, and those that go into it should not be looking at this as a short-term play.

But then again, very few investments I make can be characterized as "short term" in terms of their targets. If a company does reach the stated trim level before my expectations, I won't hesitate to carve at it like a steak - but overall, I've held most of my portfolio positions for years, and some of them going on 8 years at this point (though in 2 cases, such long holding levels have been mistakes).

I argue that part of a solid investment strategy involves trimming and rebalancing profitable positions at overvaluation.

This is something I've become more vocal about in the last 1-2 years, and I will continue to include this in my strategy.

Santander, however, is far from that point - it's still a "Buy", and an undervalued one at that.

Here is my current Santander thesis for 2023.

Thesis

- Santander is one of the better banks found in the Southern European area and geography. It has significant emerging market exposure, which gives it a heightened risk profile in context to other banks - but it's also immensely qualitative, as evidenced by how it has survived previous downturns.

- I consider Santander a "Buy" at cheap valuations, and I believe this bank can deliver significant upside over time - and that now is one of those times.

- I give Santander a PT of $4/share and give it a "Buy".

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I consider the company fulfilling all of my criteria - it's attractive here.

For further details see:

Santander: A Bank With Still-Existing Upside