SAP - SAP: Great Q3 That Boosts Confidence In Cloud Performance

2023-10-25 04:36:49 ET

Summary

- SAP's robust performance in 3Q23, driven by cloud, license, and maintenance revenues, reflects its resilience and growth potential.

- SAP's cloud business shows significant momentum, with substantial growth in S/4 HANA cloud revenue and Cloud and Business Technology Platform (BTP) offerings.

- SAP is strong business in a deteriorating macroeconomic environment due to its mission-critical enterprise software, idiosyncratic product cycle, and a net cash balance sheet.

Summary

This post is to provide my thoughts on SAP ( SAP ) business and stock. I believe SAP is an attractive business, especially in today’s uncertain macro environment as it offers several defensive traits that investors like. Firstly, SAP offers a mission critical function to businesses (database and enterprise resource planning management, which is like the backbone for all department functions). Secondly, the SAP balance sheet is strong at net cash position, which means there is no liquidity risk. Thirdly, the business has very high recurring revenue that provides stability in volatile times. Based on outlook, I am recommending a buy rating.

Investment thesis

For 3Q23 quarter, SAP reported revenue of EUR7.74 billion, driven by both cloud revenue of EUR3.5 billion, License revenue of EUR335 million, and Maintenance revenue of €2.9 billion. The strong performance drove EBIT to €2.3 billion and EPS of $2.99.

I expect SAP to continue its growth momentum due to the strong traction in cloud performance. For reference, CCB growth momentum continued despite toughening macro environment with 25% organic growth in 3Q23, which I expect to continue at similar levels in 4Q23. In the earnings call yesterday, management highlighted continued momentum in S/4 HANA as evidenced in both S/4 HANA cloud revenue and CCB growth of 66% on an organic basis. Respectively, cloud revenue grew 77% while CCB grew 66%. Both of these performance are significant indicators of underlying demand as they grew on top of a huge growth comp last year (cloud revenue grew 81% last year while CCB grew 90% last year). Furthermore, management highlighted strong traction in driving the RISE and GROW offerings, which in turn result in net new customers as well as an installed base maintenance conversion of >2x. Notably, both large and mid-sized customers are continuing to leverage SAP’s generative AI capabilities providing further S/4 HANA CCB on these multi-year programs. These factors, in my opinion, will be able to offset the mixed macro driven softness in the transactional business over the near-term and more importantly, provide visibility into the sustainability of cloud growth in FY23 and over the medium-term.

I think one of the key debates is how SAP can maintain CCB growth at 25% over the coming quarters. Specifically, the lower end of the FY23 cloud revenue growth guidance implies an acceleration in 4Q23 from 3Q23. My belief is that there is no issue in meeting this acceleration as the it is well supported by S/4 HANA momentum along with traction in BTP. Moreover, management has noted that they have signed multi-year deals into past which I expect to contribute to CCB as they ramp. Although I would note that it is incredibly hard to model the impact of these multi-year deals are they are not reported separately. This might cause some volatility in the near-term as there would be various expectations in the market (by investors).

All in all, following a strong 3Q23 performance, I expect revenue to continue growing at this pace and margins to expand as management’s mid-term targets imply ~31% FY25 adjusted EBIT margins which requires 340bps margin expansion over the next 2 years. There should be no issues for SAP to expand margin as planned given that the rate of expansion today is on track (2Q23 expanded margins by 176bps vs FY22. 176 * 2 = 352 bps). Also, as cloud becomes a larger mix of the revenue base, it would drive margin expansion as well.

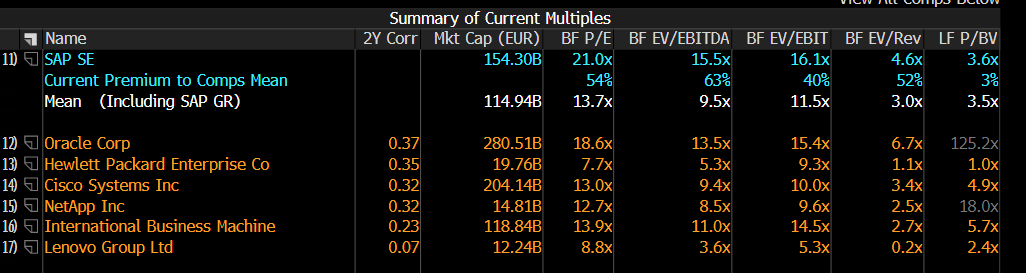

Valuation

Own calculation

I believe the fair value for SAP based on my model is EUR159. My model assumptions are that SAP will continue to grow as guided for FY23 and 10% for FY24 and FY25, driven by the strong cloud momentum. Accordingly, as cloud revenue becomes a larger mix of the pie, margins should expand accordingly. I used management FY25 margin guide as a benchmark for my FY25 adjusted earnings margin (increasing by ~200bps per year, slightly more than the 170bps due to financial leverage). Based on my assessment on SAP business, I expect it to continue trading at a premium vs peers given its lower debt profile, expanding margins narrative, higher growth profile (vs peers at high-single digits).

{kind=link}

Risk

SAP faces the risk of macroeconomic conditions being more challenging than anticipated. This includes potential disruptions such as supply chain issues, wage inflation, rising interest rates, and fluctuations in economic growth. These factors have the potential to influence corporate IT budgets and, consequently, have a direct impact on SAP's sales opportunities. Conversely, improved macroeconomic conditions may facilitate accelerated adoption of SAP's products, potentially leading to faster revenue growth than currently projected.

Another significant risk involves the pace of the transition to cloud-based revenues. This shift in revenue composition could occur either faster or slower than expected, consequently affecting the timing of revenue recognition. This variability may also influence the achievement of gross and operating margin targets. SAP needs to remain vigilant to these uncertainties as they may impact financial performance and strategic planning.

Conclusion

In conclusion, SAP's impressive 3Q23 performance underscores its resilience and growth potential, driven by robust cloud, license, and maintenance revenues. Notably, SAP's cloud business exhibits significant momentum, with substantial growth in S/4 HANA cloud revenue and Cloud and Business Technology Platform offerings. In a challenging macroeconomic environment, SAP stands out due to its mission-critical enterprise software, strong balance sheet with a net cash position, and high recurring revenue, providing stability in volatile times. This performance, along with a clear growth strategy, instills confidence in SAP's outlook. While challenges exist, including the pace of cloud revenue transition and macroeconomic risks, SAP's strong performance and strategic positioning make it an attractive investment target.

For further details see:

SAP: Great Q3 That Boosts Confidence In Cloud Performance