SAP - SAP: Too Expensive To Consider (Ratings Downgrade)

2023-08-29 00:19:27 ET

Summary

- SAP has skyrocketed this year, including in August, when most other peers saw a correction.

- The company is experiencing a deceleration in cloud growth and recently cut its 2025 cloud revenue targets.

- The strengthening of the euro against the dollar is also causing reported revenue growth rates to decline.

- Now trading at a >20x FY24 P/E, SAP has become too expensive to invest in during a high-interest rate environment.

I'll admit it: even though I'm a dedicated tech investor and a long-term bull, I've been turning bearish on a lot of names recently. The reason is sheer prudence in the current high interest-rate environment. We have to ask ourselves: why invest in premium-valuation stocks when risk-free cash can yield 5%? I've dramatically tilted my allocation toward cash this year; a stock sitting in my portfolio must show compelling growth and sit at a reasonable valuation (the "GARP" trade!). It's not either-or; the company has to demonstrate both qualities.

I had been bullish on SAP ( SAP ) throughout most of the pandemic before turning neutral earlier this year. While I certainly did miss out on some gains as the stock rose >30% year to date (of note is the fact that SAP is one of very few software stocks to not see a material correction in the month of August), I don't regret my decision to turn cautious on this name.

With SAP now having clawed its way back to highs not seen since 2021, I am downgrading the stock to bearish , as I see more downside than upside in the stock at current levels.

Here are the core red flags that are driving my ratings downgrade:

- Cloud deceleration. SAP has admirably held onto its long-term cloud revenue targets (it is also one of the few companies to provide ambitious long-term forecasts) in the wake of macro uncertainty, but there can be no doubt that at its greater scale, SAP is facing revenue deceleration.

- Unknown impacts of AI on SAP's ERP systems. SAP certainly has AI embedded into its products; but historically as a legacy software vendor, the company has been late to major tech trends (its delayed conversion to cloud is one of the reasons why its cloud business is growing ~20% y/y today). As a technology, AI and automation has the capacity to rewrite the requirements and core value proposition of SAP's ERP and financial software systems. Meanwhile, among its competitors, Microsoft ( MSFT ) has OpenAI; Oracle ( ORCL ) has long applied machine learning in its new database products. It's unclear how SAP will manage to compete in this revised landscape.

- FX tailwinds are temporary. SAP's growth rates have started to decay as the dollar has reversed course and weakened against the euro, hurting SAP's reported revenue.

- Macro pressures. SAP implementations are typically complex projects that require dedicated teams and significant capital outlays. In the current macro environment where chief executives have delayed major capital projects, SAP's business momentum may suffer.

Valuation, in my view, remains the core reason to avoid SAP. Right now, Wall Street analysts are expecting SAP to generate $6.63 in pro forma EPS in FY24 (or 19% y/y earnings growth, supported by 9% y/y revenue growth: which implies significant margin leverage, on top of headwinds from having divested Qualtrics midway through this year). Even if we take consensus estimates at face value, SAP trades at a 20.9x FY24 P/E multiple, which is a premium valuation in a high-rate environment. Considering top-line growth is expected to slow to the single digits next year (something that rests heavily on where the euro settles against the dollar, by the way), SAP is not a gamble I'm willing to make.

The bottom line here: considering top-line deceleration and a valuation that has grown uncomfortably rich with the stock's latest upward drive, I'm recommending locking in gains and moving to the sidelines here until A) we see evidence of better top-line cloud results, or B) prices rationalize downward again and we see SAP return to a mid-teens P/E ratio against FY24 earnings.

Q2 download

It's worth noting that in spite of SAP's gains over the past several months, including the month of August when most tech stocks tumbled, the company saw material deceleration and a miss to Wall Street expectations when it reported Q2 results in late July. Take a look at the Q2 results below:

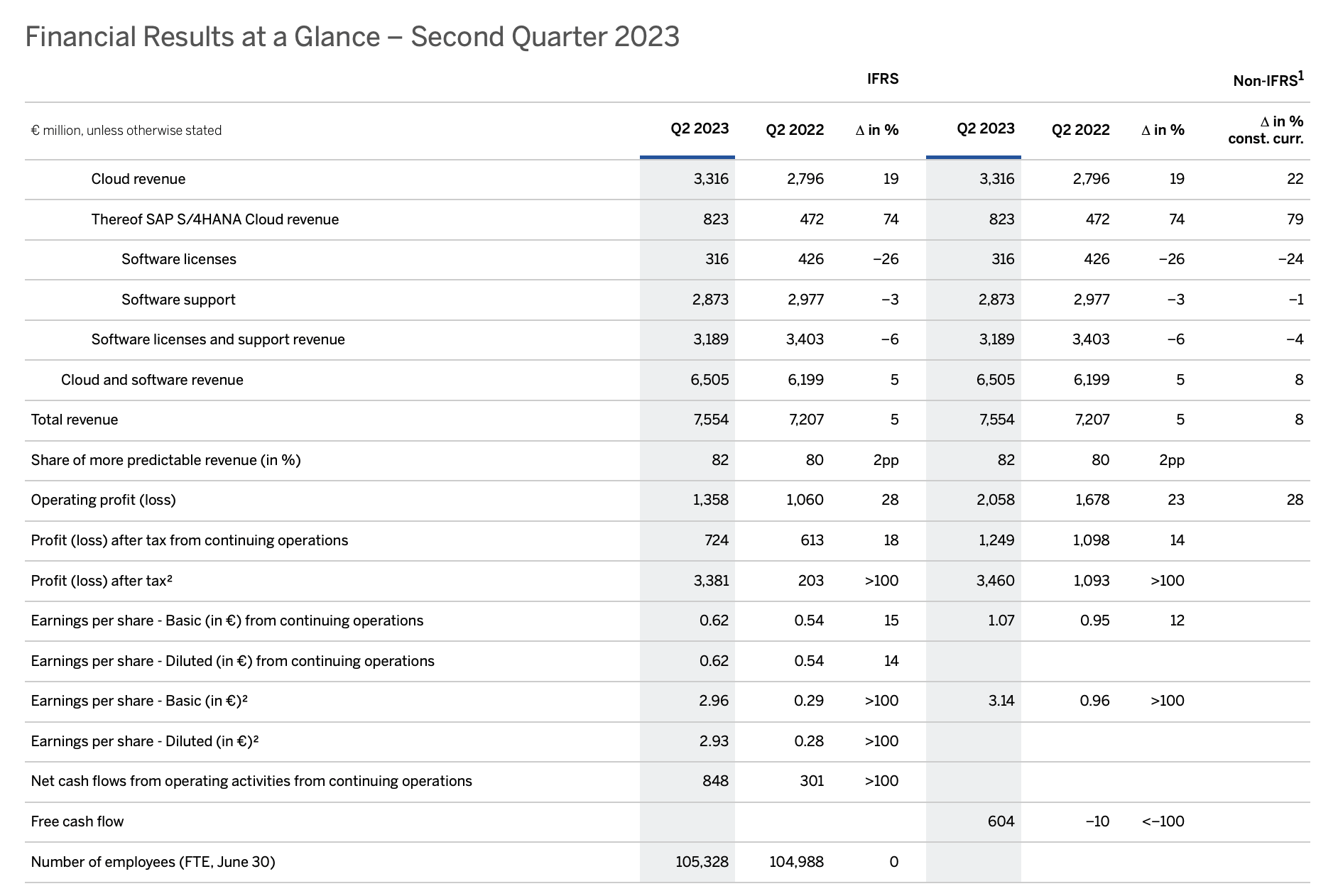

SAP Q2 results (SAP Q2 earnings release)

{kind=link}

SAP's revenue grew 5% y/y to ?7.55 billion, missing Wall Street's expectations of ~?7.65 billion (+6% y/y) and decelerating versus last quarter's 10% y/y growth rate. On a constant currency basis, growth would have been 8% y/y - indicating the impact of the dollar reversing course and weakening against the euro, negatively impacting SAP's revenue (whereas the dollar-euro strength had been a benefit to SAP's y/y revenue growth in the past several quarters). On a constant currency basis, however, performance still waned, as Q1's constant-currency revenue growth was 9% y/y.

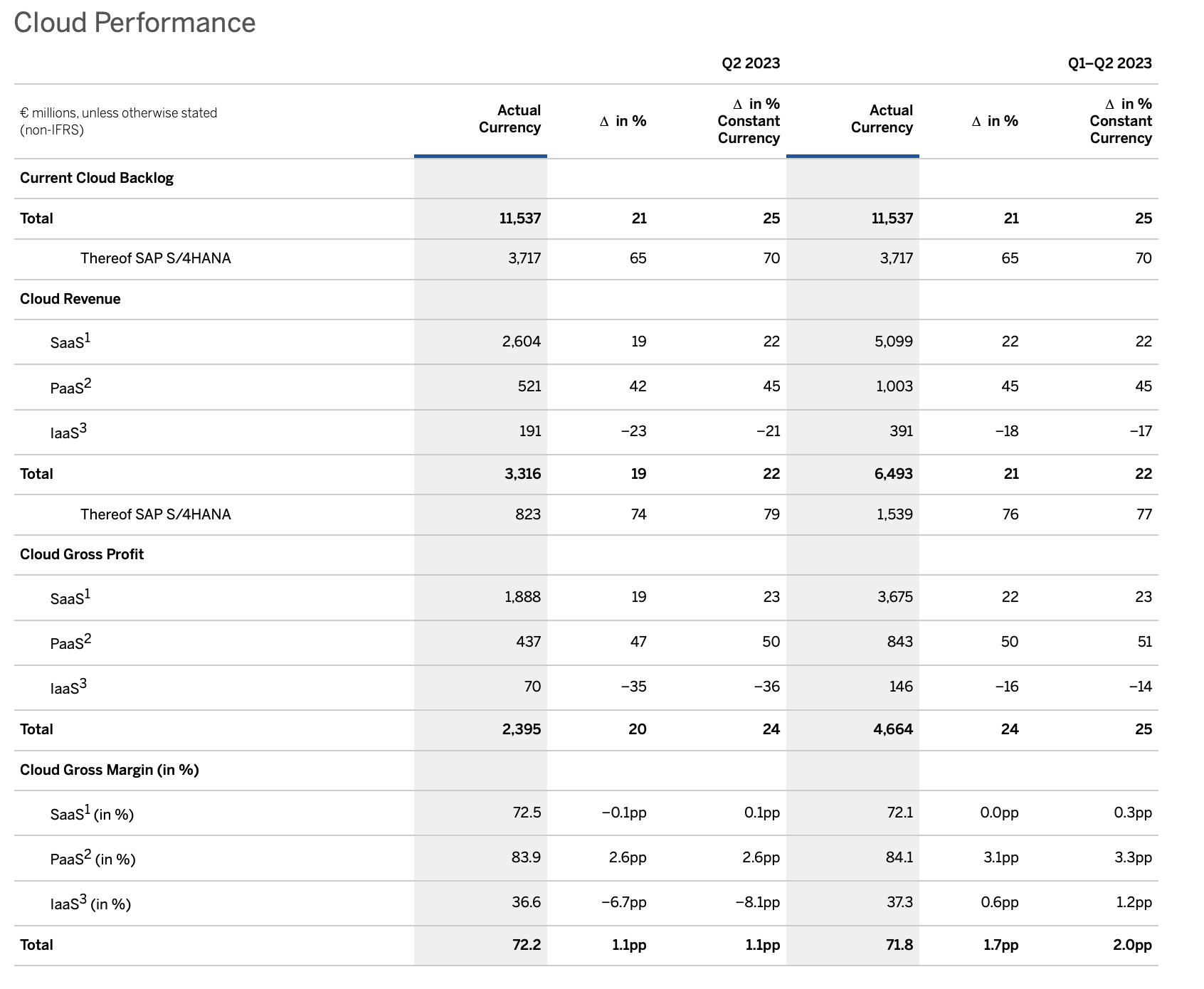

The chart below breaks down SAP's cloud revenue performance. Total cloud revenue grew 19% y/y to ?3.32 billion, or 22% y/y growth in constant-currency terms. This is consistent with 22% constant-currency growth in Q1; with growth primarily driven in the company's PaaS (platform-as-a-service) offerings, up 45% y/y at constant currency.

SAP cloud performance details (SAP Q2 earnings release)

{kind=link}

The company notes continued progress in its goal of capturing more mid-market customers. Per CEO Christian Klein's remarks on the Q2 earnings call :

Last quarter, we introduced the powerful new offering, GROW with SAP, designed for mid-market customers who are new to SAP and likely to be growing quickly as they build their businesses. GROW has quickly become popular just RISE with SAP, for which around half of the customers are net new to the SAP family. The momentum I've described with both RISE and GROW with SAP is underpinned by the SAP business technology platform. This is the foundation for integration and extensibility across our portfolio. We have reached an important milestone this quarter with over 20,000 live BTP cloud customers. This quarter, new wins included Visa, the world leader in digital payments; and Santander, the Spanish financial multinational who are using SAP business technology platform to revolutionize and streamline the banking experience. Increasing adoption of S/4HANA and the SAP business technology platform is also driving significant cross and upsell opportunities across our portfolio."

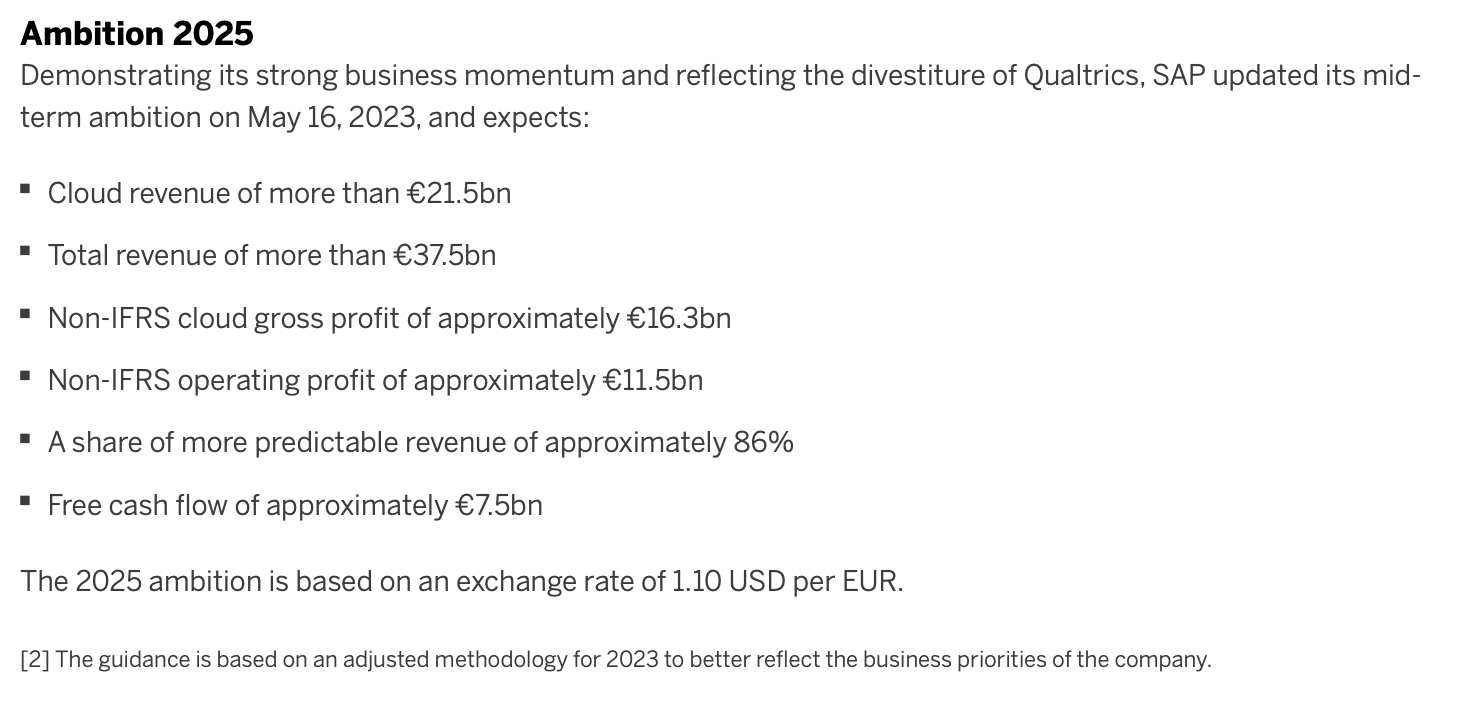

In spite of this, however, it's worth noting that SAP is slightly reducing its long-term (2025) cloud outlook.

SAP updated long-term forecast (SAP Q2 earnings release)

{kind=link}

As shown in the snapshot above, the company is now expecting cloud revenue of ?21.5 billion by 2025, versus a prior "Ambition 2025" plan of ?22.0 billion. It did, however, maintain its total 2025 pro forma operating profit expectation of ?11.5 billion, as well as its FCF expectations of ?7.5 billion.

Cloud gross margins bumped up by 110bps y/y, while pro forma EPS skyrocketed to ?2.93 - driven in part by the company's divestiture of Qualtrics this quarter. On the Q&A portion of the Q2 earnings call, in response to an analyst question on future M&A strategy, CFO Dominik Assam noted that with this divestiture the company has over ?4 billion in net cash, and that "we have a very strong balance sheet and are very much able to act."

Key takeaways

In my view, investors would be prudent to divest SAP and either reallocate that capital toward cash or toward more undervalued tech stocks (DocuSign ( DOCU ), Zuora ( ZUO ) and Alteryx ( AYX ) are among my favored plays at the moment).

For further details see:

SAP: Too Expensive To Consider (Ratings Downgrade)