CA - Saputo: The C$2.1B EBITDA Guidance Has Been Delayed

2023-10-10 10:30:00 ET

Summary

- Saputo's EBITDA target of C$2.1B+ by the end of 2025 is no longer realistic, but the company remains committed to achieving it.

- The company's Q1 financial performance showed improvement, with increased gross profit and lower tax bill.

- Saputo is making progress but will likely have to delay its C$2.1B EBITDA target by a few years.

Introduction

Saputo ( SAPIF ) ( SAP:CA ) is one of the largest producers of dairy products in North America. The share price has been under pressure for several years now as Saputo's EBITDA has been sliding due to inflation issues. In my previous article on Saputo I referred to the company’s plans to generate in excess of C$2.1B in EBITDA by the end of 2025. As Saputo has now kicked off its FY 2024 (its financial years end in March), it’s time for a check-up on the company to see if that EBITDA target is still realistic.

The company’s website contains a lot of download-only links, but you can find all relevant information and documentation here .

The first quarter of the financial year started well

Saputo is one of the world’s largest companies in the dairy processing sector as it claims a top-10 spot worldwide while it's the largest cheese producer in Canada and the UK and a top-three cheese producer in the US.

{kind=link}

Saputo is a family company and throughout the years it has built a substantial portfolio of brand names. Some were organically created within the Saputo group, but the company also completed some M&A deals in the past few years which helped to expand the product offering.

{kind=link}

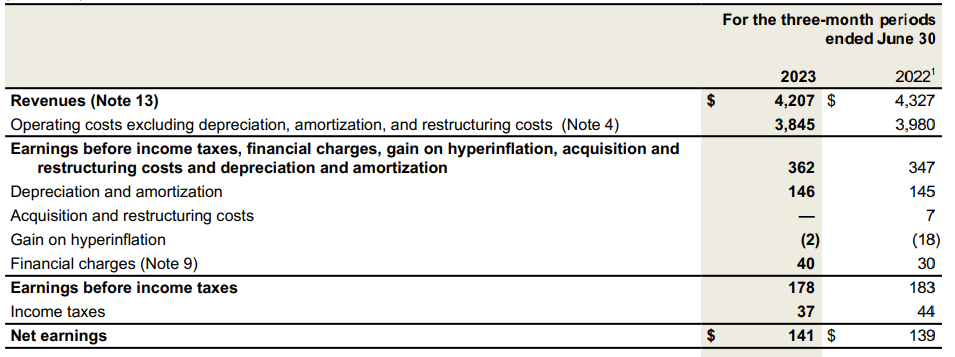

Saputo’s revenue decreased in the first quarter of the financial year (Q1 ended in June), but as you can see below, the margins actually improved as the gross profit increased by approximately 4% despite the 3% revenue decrease.

{kind=link}

Additionally, the total finance expense increase remained relatively limited but the lack of gains due to hyperinflationary circumstances (related to the activities in Argentina) is the sole reason why Saputo’s pre-tax income decreased by almost 3%. Excluding the impact of inflationary items, the pre-tax income would have been C$176M in the first quarter of this year compared to C$165M in Q1 FY 2023. So on an underlying basis, Saputo’s financial performance definitely improved.

And fortunately the total tax bill was slightly lower, resulting in a net income of C$141M for an EPS of C$0.33.

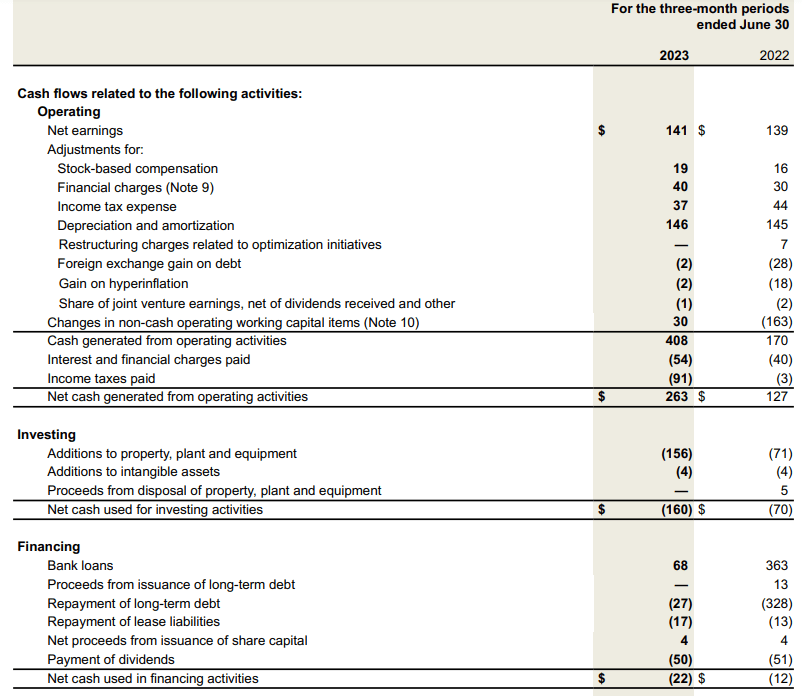

As you know by now, I’m also interested in the cash flow performance of a company, and that also is what I have been focusing on in Saputo’s case. The company reported a total operating cash flow of C$263M and this includes a C$30M contribution from working capital changes and excludes a C$17M lease payment. This means that on an adjusted basis, the operating cash flow was just C$216M. However, the cash flow statement below also shows a C$91M cash tax payment although only C$37M was due based on the Q1 income statement.

{kind=link}

This means the underlying operating cash flow was C$270M. And after deducting the C$160M in capex, the underlying free cash flow was C$110M. Lower than the net income, but that’s entirely related to Saputo’s capex program and timing: While the total depreciation and amortization expenses in the first quarter were just C$146M, the company spent C$177M on capex and lease payments and that C$31M difference explains pretty much the entire difference between the free cash flow result and the reported net income.

The free cash flow was just added to the balance sheet (of course after taking the C$50M in dividend payments into account) and the company ended June with C$376M in cash on the balance sheet. There was a total of C$725M in short-term debt and C$2.91B in long-term debt resulting in a total net debt of C$3.25B.

{kind=link}

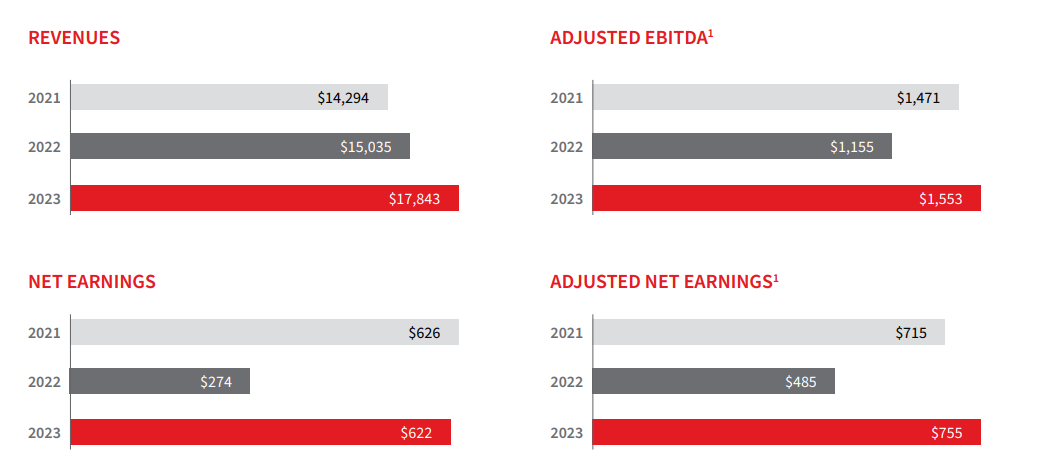

That’s rather high and it helps to explain why the company has been focusing on increasing its EBITDA. In FY 2023, for instance, Saputo’s total adjusted EBITDA was C$1.55B which means the pro forma debt ratio was just over two times the adjusted EBITDA.

But of course I'm very curious to see if the company remains on track to rapidly increase its EBITDA. In FY 2023, its EBITDA result was the highest in years and FY 2024 will hopefully be the year of confirmation.

{kind=link}

When Saputo announced its full-year results for 2023, it confirmed it expected to "deliver a year of strong adjusted EBITDA growth."

That’s nice to hear, but at the end of the first quarter, the company retracted its C$2.125B EBITDA target for FY 2025. But although the target date of 2025 was axed, Saputo remains committed to focus on that C$2.1B+ EBITDA target. From the Q1 conference call (the emphasis is mine):

Let me say this. The CAD 2.125 billion is still very, very much intact. We're confident in our plan. We're confident in our ability to be able to execute effectively on those projects, on those ideas and those initiatives that we set out for ourselves. So that's really not the issue.

And I would also say that, at the end of this quarter and going into Q3 and Q4, most of the heavy lifting on those projects will have been done. So we're extremely confident in our earnings power for the business. It's just the unpredictability of the elements relative to pricing, and relative to consumer sentiment that are creating a push out of our target date, but the target number remains unchanged. And our confidence in that is unchanged .

Investment thesis

Saputo isn’t the first but certainly also won’t be the last company that has to shelf ambitious growth plans. While the company keeps the mid-term EBITDA guidance of C$2.125B intact, it admits it's no longer realistic to expect this by the end of 2025. The company didn’t want to be pinned down with a new target to achieve the higher EBITDA, but we will likely have to measure the delay in years.

This means the company is not cheap based on the current financial performance but I do believe and expect the results will show continuous improvement. I currently have no position but I could be interested in a long position on weakness. That being said, I also don’t think there is any rush here.

For further details see:

Saputo: The C$2.1B EBITDA Guidance Has Been Delayed