CA - Savaria: Decent Q2 2023 Results And Weak Sentiment Create Buying Opportunity

2023-08-30 22:10:16 ET

Summary

- The company’s revenues rose by 3.3% year on year in Q2 2023, despite the sale of its Norwegian business.

- Adjusted EBITDA came in at C$29 million ($21.3 million) which is strong considering there was a C$5 million ($3.7 million) negative impact from a new EPR system.

- With the market capitalization declining by over 8% since mid-July, I think this could be a good time to open a position.

Introduction

In April, I wrote an article on SA about Canadian mobility products maker Savaria (SIS:CA) (SISXF) in which I said that it should have strong organic revenue and income growth over the coming years thanks to the rapidly aging population in its main markets.

Well, Savaria posted its Q2 2023 financial results on August 9 and I think they were good as revenues rose by 3.3% year on year despite the sale of the Norwegian business while adjusted EBITDA came in at C$29 million ($21.3 million). Considering the market capitalization of the company has decreased by over 8% since the middle of July, I think that this could be a good time to open a position and it’s possible that I buy some shares over the coming days. Let’s review.

Overview of the Q2 2023 financial results

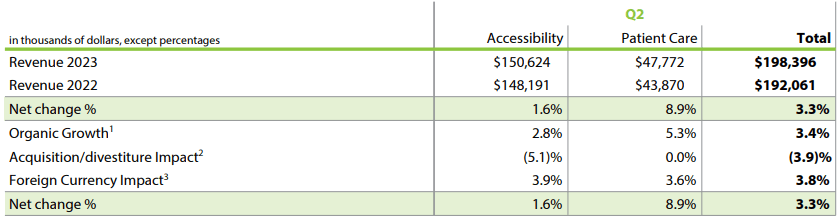

If you aren't familiar with Savaria or my earlier coverage, here's a brief description of the business. The company is involved in the manufacturing and installation of accessibility equipment such as wheelchair lifts and elevators, stairlifts, and accessible vehicles (accessibility segment); as well as ceiling lifts, medical beds, and pressure management products (patient care segment). It also provides wheelchair lowered-floor accessible conversions for minivans (included in the accessibility segment). Savaria currently has a total of 16 manufacturing facilities across North America, Europe, and China and employed 2,250 people as of August 9 (see page 5 here ). In March 2023, the company sold Norway-based Handicare AS which formed a major part of its Adapted Vehicles segment and was focused on commercial adaptations for emergency services eg police, and fire and rescue. In 2022, the adapted vehicles segment generated revenues of C$55.1 million ($40.5 million) and adjusted EBITDA of C$2.3 million ($1.7 million). Yet, it’s worth noting that not all of that came from Handicare AS and the remaining assets of the segment were integrated into the accessibility segment. Looking at the Q2 2023 financial results, we can see that the sale of Handicare AS had a negative impact of 3.9% on revenues but Savaria managed to book a decent revenue growth during the period thanks to good organic growth and favorable currency exchange rate changes.

{kind=link}

Organic growth was particularly strong in the patient care segment thanks to new contracts signed with healthcare facilities as well as price increases. Looking at the accessibility segment, revenues in North America grew by 12.1% to C$86.4 million ($63.6 million) but overall organic growth was negatively affected by lower production and delivery of stairlift products in Europe in April and May as a result of the implementation of a new ERP system. I expect organic growth in this segment to return to above 5% in Q3 2023.

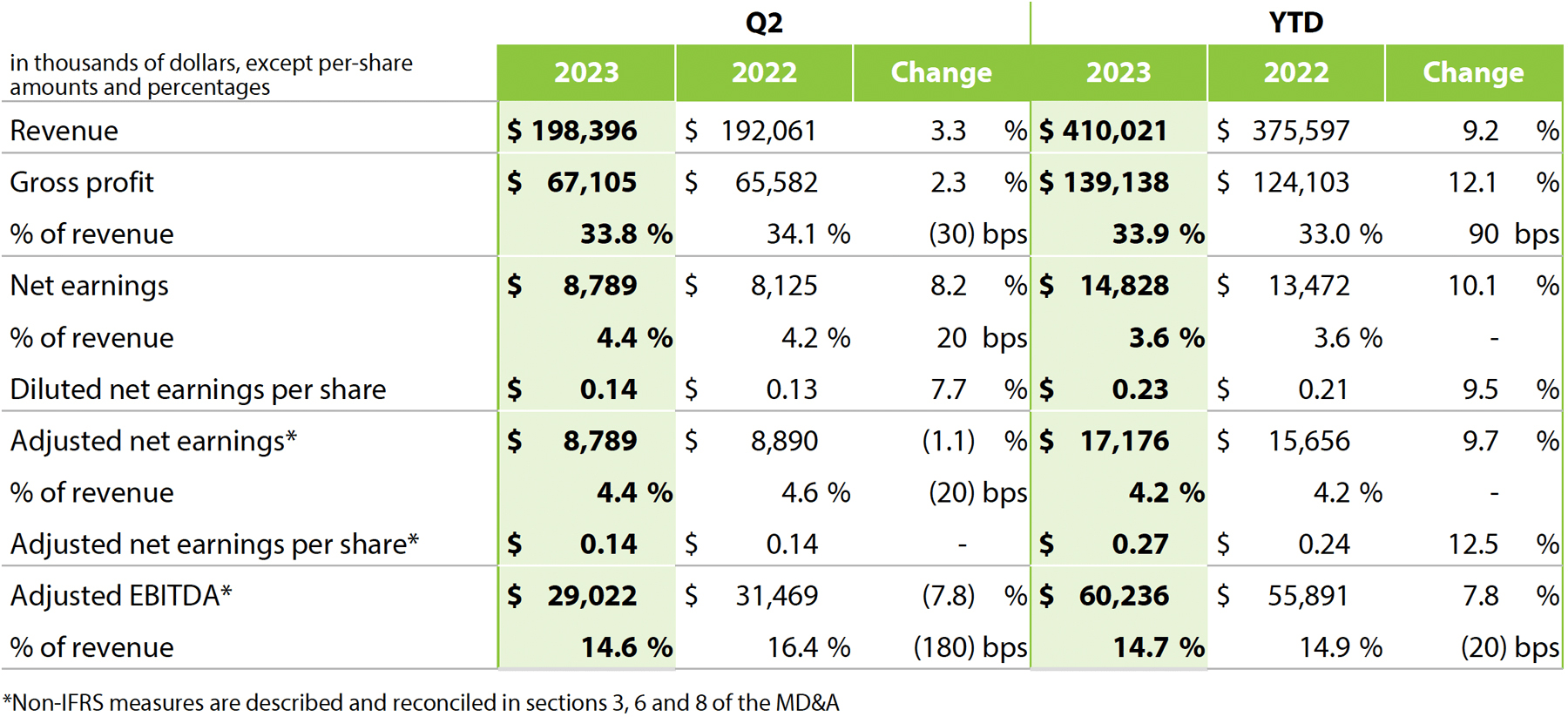

Looking at the income statement, adjusted EBITDA declined by 7.8% year on year as the adjusted EBITDA margin shrank by 180 bps to 14.6% but I consider this to be a strong result considering Savaria estimated that the implementation of a new ERP system decreased adjusted EBITDA about C$5 million ($3.7 million).

{kind=link}

Savaria also announced the launch of a company-wide initiative named Savaria One, the aim of which is to promote operational and sales excellence over the next 24 months. While there are no details available, I’m optimistic that this program could help the company boost its adjusted EBITDA margin to above 18% by 2025. In my view, the margins of the business should also improve in the coming quarters thanks to economies of scale, and I’m encouraged that Savaria mentioned in its press release for the Q2 2023 financial results that it seems on track to exceed its goal of C$1 billion ($735.7 million) in annual revenues by the end of 2025. At an adjusted EBITDA margin of 18%, this would put the adjusted EBITDA at above C$180 million ($132.4 million) which would be a significant improvement from the current C$124.6 million ($91.7 million) on a TTM basis.

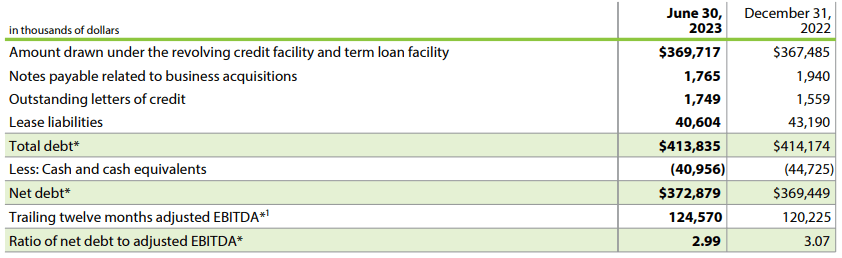

Looking at the balance sheet, net debt increased slightly compared to the end of 2022 and the main reason behind this was lower cash and cash equivalents in Europe. The net debt to adjusted EBITDA ratio remains at around 3x, which I consider to be a manageable level and I could see Savaria make one or two small acquisitions over the coming 12 months.

{kind=link}

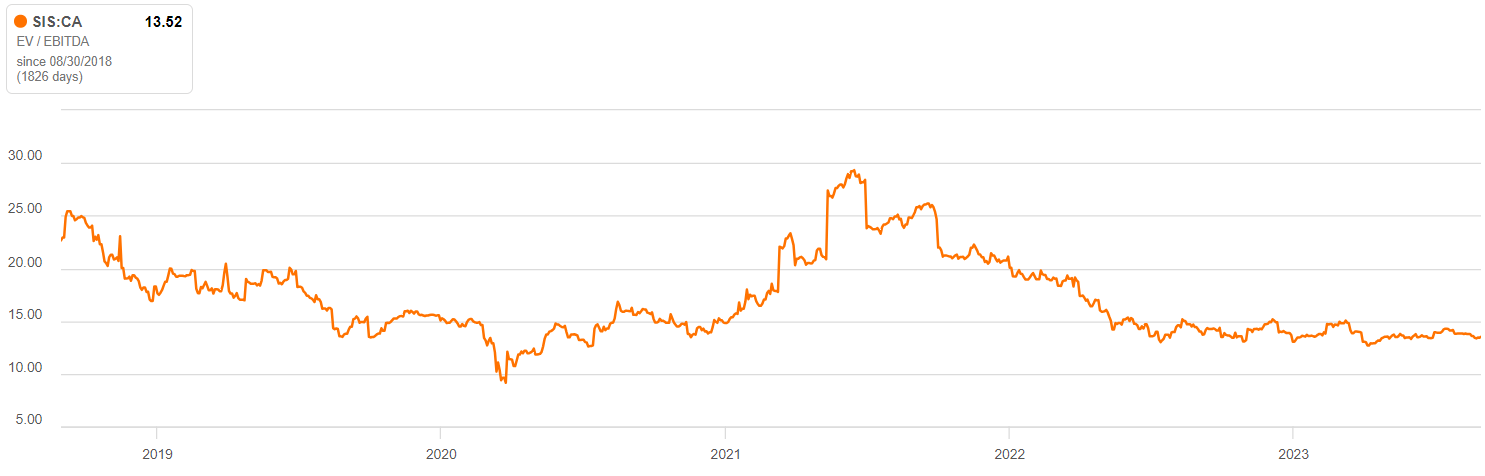

Turning our attention to the valuation, Savaria has an enterprise value (EV) of $1.41 billion as of the time of writing and is trading at an EV/EBITDA ratio of 13.5x on a TTM basis. The EV/adjusted EBITDA ratio, in turn, stands at 11.3x. While these levels might seem high at first glance, it’s worth noting that this is a stable business with decent organic growth that has been trading at above 15x EV/EBITDA over the past five years.

{kind=link}

Overall, I think that the Q2 2023 financial results were decent although it might not seem so from first glance due to lower adjusted EBITDA. In my view, the slide in the share price over the past six weeks has created a good opportunity to open a position here and I’m considering buying some shares over the coming days. In my view, the valuation of Savaria is likely to be back above 15x EV/EBITDA by the end of 2023. This level translates into C$18.35 ($13.50) per share or an upside potential of 14.9%.

Looking at the downside risks, I think that there are two major ones. First, it’s possible that sentiment remains depressed over the next few months due to the lower adjusted EBITDA in Q2 2023. Second, Savaria has made several large acquisitions in the past that were financed by capital increases - – C$38.4 million ($28.2 million) in 2017; C$57.3 million ($44.5 million) in 2018, and C$122 million ($95.7 million) in 2021. Another such transaction in the near future could lead to lower EPS in the short term.

Investor takeaway

In my view, Savaria booked decent financial results for Q2 2023, but it seems that the market is focusing on the lower adjusted EBITDA figure as the market capitalization has declined by more than 8% since the middle of July. The company is optimistic about its revenue growth over the coming quarters and I think that the adjusted EBITDA margin could surpass 18% by 2025. In my view, this is a good time to open a position and might pick up some shares over the coming days.

For further details see:

Savaria: Decent Q2 2023 Results And Weak Sentiment Create Buying Opportunity