ET - SCD: Add Diversification To Your Portfolio With This High-Yielding Fund At A Discount

2023-12-21 11:47:19 ET

Summary

- LMP Capital and Income Fund offers a high yield of 9.94% and exposure to common stocks, making it appealing to income-focused investors.

- The fund's performance has been reasonable, with a 5.98% return since the previous article was published.

- The fund's portfolio includes master limited partnerships and high-yielding dividend-paying stocks, providing diversification and potential for high income.

- The fund has generally outperformed the S&P 500 Index in terms of total returns, so investors do not have to sacrifice upside potential to get income.

- This fund appears to be fully covering its distributions and trades at an enormous discount.

The LMP Capital and Income Fund ( SCD ) is a closed-end fund that income-focused investors may find appealing, as it provides a very high yield to its shareholders without forcing them to abandon the upside potential of investing in common stock. After all, as of the time of writing, the S&P 500 Index ( SP500 ) only yields 1.40% so it is virtually impossible to obtain a reasonably attractive level of income by investing in common stock. That yield only results in $14,000 annually from a $1 million investment and it seems highly unlikely that anyone who has managed to amass a portfolio of that size would be satisfied with such a scant level of annual income. The LMP Capital and Income Fund is able to do much better, as it currently boasts a 9.94% yield and also has common stock exposure.

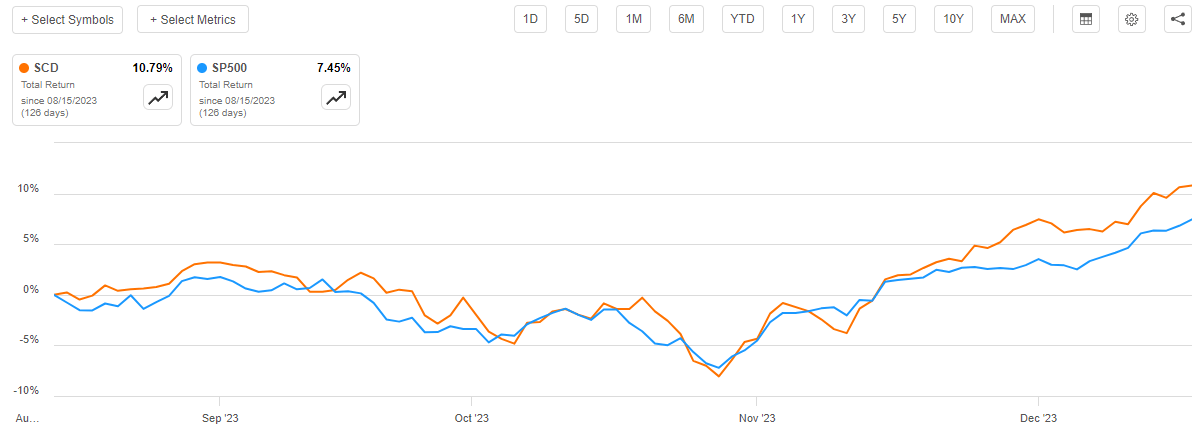

As regular readers may remember, we last discussed the LMP Capital and Income Fund in the middle of August of this year. That was, obviously, a very different market environment to the one that we are currently in. In the middle of August, the market was gradually adjusting to the idea that the Federal Reserve might actually be serious about its "higher for longer" narrative and was selling off many common stocks as well as bonds as investors rotated into shorter-duration assets such as energy. That is very different from today, as today's market very much resembles the bubble environment that existed when the Federal Reserve cut interest rates to zero in response to the pandemic lockdowns and the government's need for enormous amounts of newly printed money. We can probably expect that the shift in market mentality would have an impact on the performance of this fund. That is certainly the case, as shares of the LMP Capital and Income Fund are up 5.98% since the date that my previous article was published. That is not nearly as good as the 7.45% return that the S&P 500 Index delivered over the same period, but it is still a very reasonable return for a four-month period:

{kind=link}

This does not tell the whole story, however, because the LMP Capital and Income Fund is a closed-end fund and not an exchange-traded fund or something similar. As such, the fund typically delivers a much greater proportion of its overall returns to the shareholders via distributions. It does not rely solely on share price appreciation. As such, we need to include the distributions that the fund paid out in any discussion of its overall performance. When we do that, we see that the fund's shareholders received a 10.79% total return over the past four months. That was substantially better than the total return provided by the S&P 500 Index over the same period:

{kind=link}

This certainly speaks well to the quality of the fund's assets and management. Naturally, though, we will want to investigate it further to see if this performance was a fluke or if it is something that can be sustained in the long term.

About The Fund

According to the fund's website , the LMP Capital and Income Fund has the primary objective of providing its investors with a very high level of total return. However, as is the case with many closed-end funds, it is expected that much of this return will be delivered to the shareholders in the form of current income. That is not a bad or inappropriate objective for this fund given the assets that it invests in. The website specifically states that the LMP Capital and Income Fund invests its assets in a combination of fixed-income securities and common equities:

{kind=link}

For the most part, any fund that invests in common equities should have total return as an objective. This is because common equities are by their very nature total return vehicles. As I explained in my previous article on this fund:

Common equity is generally considered to be a total return vehicle, so the fund's objective certainly makes a great deal of sense. After all, we typically buy common stock because we want to receive an income from the dividends that it pays out as well as benefit from capital gains as the issuing company grows and prospers.

The fund does invest in fixed-income securities such as preferred stock and bonds as well, which are generally considered to be income vehicles. After all, neither bonds nor preferred stock delivers net capital gains over their lifetimes. However, this does not change the overall thesis here as income is a component of total return. Thus, this is a blended fund that aims to provide as high a return as reasonably possible without confining itself to solely investing in common stocks or fixed-income securities. The fund then pays out the majority of its investment profits to the shareholders in the form of distributions. This is a very similar strategy to the one employed by most blended closed-end funds.

In my last article on this fund, we saw that the LMP Capital and Income Fund was very heavily weighted towards common equities. It has increased that weight significantly since the date that the previous article was published. As we can see here, 97.17% of the fund's assets are currently invested in common stocks:

CEF Connect

The last time that we discussed this fund, 90.97% of the fund's assets were invested in common stock. Thus, the common stock position increased substantially over the past few months. However, the fund's allocation to preferred stock did not really change (it increased slightly from 2.16% to 2.75% of total assets). The big change here is that the fund spent a lot of its cash, probably on acquiring stocks. We could credit this to the recent rally, but that seems to be rather unlikely. The chart above is dated October 31, 2023, which was just when the recent market strength started. Thus, it seems likely that the fund spent its cash acquiring stocks back in August or September, which means that the fund actually managed to catch the bottom. That is very shrewd market timing if indeed it was the reason for the shift in the asset allocation that we see here. That undoubtedly worked out to be a great move on behalf of the fund's shareholders.

In the description of the fund's strategy above, we see that it claims to focus its efforts on investing in master-limited partnerships, real estate investment trusts, and similar entities that have long been considered to have very high yields. This makes sense, considering that the fund has stated that it is going to try and earn a high percentage of its total investment returns from income-producing assets. This is generally what we see when we look at the largest positions in the fund's portfolio, although it is far from perfect in this regard. Here are the largest positions in this fund today:

{kind=link}

Here are the yields on these companies:

| Company |

| Current Yield |

| Microsoft Corp. ( MSFT ) |

| 0.80% |

| Energy Transfer ( ET ) |

| 9.01% |

| Enterprise Products Partners ( EPD ) |

| 7.61% |

| Apple Inc. ( AAPL ) |

| 0.49% |

| The Blackstone Group ( BX ) |

| 2.59% |

| Sunoco LP ( SUN ) |

| 5.77% |

| Broadcom ( AVGO ) |

| 1.84% |

| ONEOK ( OKE ) |

| 5.53% |

| Apollo Global Management ( APO ) |

| 1.82% |

| Plains GP Holdings ( PAGP ) |

| 6.80% |

This is certainly a more income-focused portfolio than we see most equity closed-end funds possessing. After all, with the exception of Microsoft and Apple, all of the companies here have a higher current yield than the S&P 500 Index. We also do not see excessive exposure to the "Magnificent 7" technology stocks, except for Microsoft and Apple. These stocks tend to possess incredibly low yields and very high valuations, which has the effect of dragging down the overall yield of the S&P 500 Index as well as any fund that they are included in.

Another major thing that I noticed here is that several of these companies are ones that we do not often see among the largest positions in most closed-end funds. That is something that could be very appealing to investors who are seeking to improve the diversification of their portfolio. In the comments on some of my articles on common equity closed-end funds, I have seen a few people complain about how every fund seems to have the same ten positions. Thus, even if an investor has several different funds in their portfolios, they have very limited diversification because every fund is invested in exactly the same thing. This one has some different assets, so it can help investors reduce their overall risks.

There have been relatively few changes to the fund's largest positions since the last time that we discussed it. Indeed, the only changes of note are that Magellan Midstream Partners and Merck ( MRK ) were removed from the largest positions list. In their place, we have ONEOK and Apollo. The removal of Magellan Midstream Partners was inevitable because that company was acquired by ONEOK back in September. Thus, that change to the positions list may simply be this fund holding the shares that it received in that transaction. Otherwise, the weightings of a few of these companies have changed but otherwise the names are the same so the changes that we see here could be caused simply by one stock outperforming another in the market. As such, it is not necessarily a sign that the fund is actively engaging in a great deal of trading to change its positions.

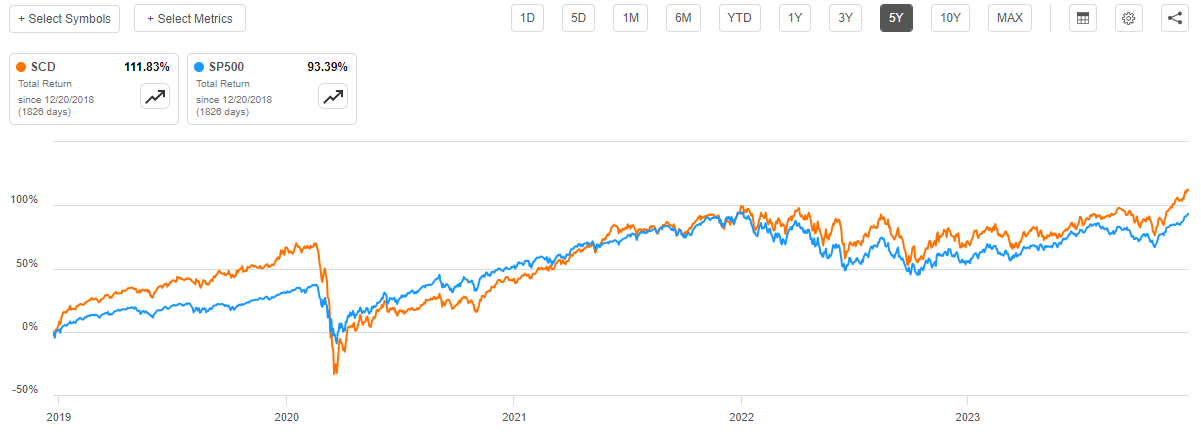

In fact, the LMP Capital and Income Fund only has a 16.00% annual turnover, which is very low for a closed-end equity fund. As I have pointed out in a variety of previous articles, a high level of trading serves as a drag on a fund's performance because it costs money to trade stocks and other assets. This is one reason why actively managed funds typically underperform comparable indices. However, this does not really appear to be the case with this fund, as its total returns have been substantially better than the S&P 500 Index over the past five years:

{kind=link}

This is partly due to the high distribution that this fund pays out, as that boosts the total return somewhat, but it needs to obtain the money that it pays out through investment activities in order to be sustainable. After all, no fund can sustain an indefinitely declining net asset value per share. Thus, we can conclude that this fund's trading activity and expenses do not appear to be negatively impacting its performance. This is yet another thing that investors should be able to appreciate about this fund.

Leverage

As is the case with most closed-end funds, the LMP Capital and Income Fund employs leverage as a means of boosting its effective yield and total return well beyond that of any of the underlying assets. I explained how this works in my previous article on this fund:

In short, the fund borrows money and uses that borrowed money to purchase stocks, partnership units, and other income-producing assets. As long as the purchased securities deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is not as effective today with rates at 6% as it was three years ago when the fund could borrow money for basically nothing. This is because the difference between the returns that the fund can get on the purchased assets and the amount that it has to pay on the borrowed money is not as great as it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason.

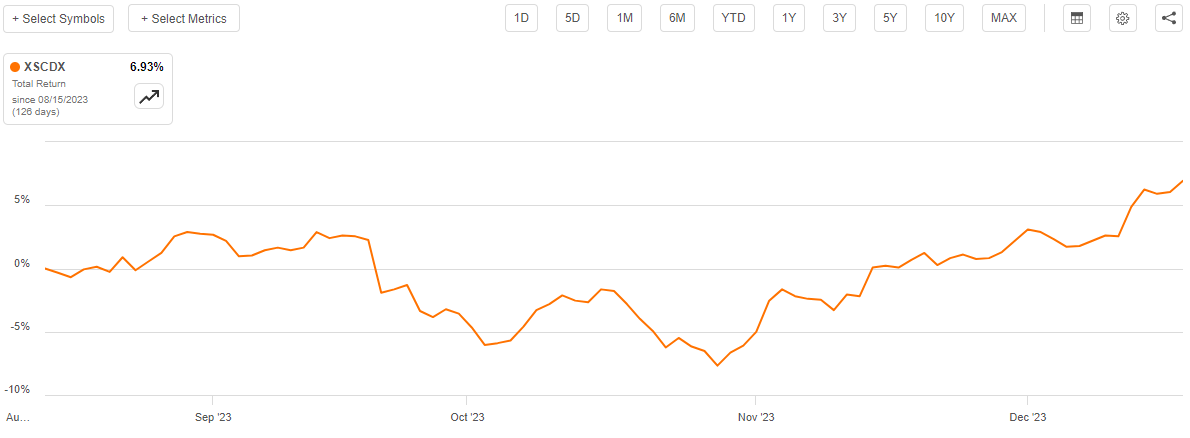

As of the time of writing, the LMP Capital and Income Fund has leveraged assets comprising 18.59% of its portfolio. This is considerably lower than the 19.41% leverage that the fund had the last time that we discussed it. This is easily explainable by the fact that the fund's net asset value per share is up 6.93% since the time of our last discussion:

{kind=link}

Thus, as long as the fund's leverage remained static, it would end up representing a smaller percentage of the portfolio simply because the value of the portfolio is higher. This is exactly what we see here.

The fund's leverage is nothing to worry about, as it is quite a bit less than many other closed-end funds possess. As such, it represents a fairly reasonable balance between risk and reward.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the LMP Capital and Income Fund is to provide its investors with a very high level of total return. However, it expects a significant portion of that total return to be in the form of income provided to both the fund and its investors. This is evident in the fact that the fund invests in a number of master limited partnerships and high-yielding dividend-paying stocks. The fund pools the dividends and distributions that it receives from the assets in its portfolio and combines them with any capital gains that it manages to realize through the trading of appreciated common stocks. Then it pays out the money that it receives through these activities to its investors, net of its own expenses. When we consider the capital gains that are typically provided by common stocks and the fact that many of the things in this portfolio have very high yields (such as the master limited partnerships), we can expect that the fund's shares will also boast a very high yield.

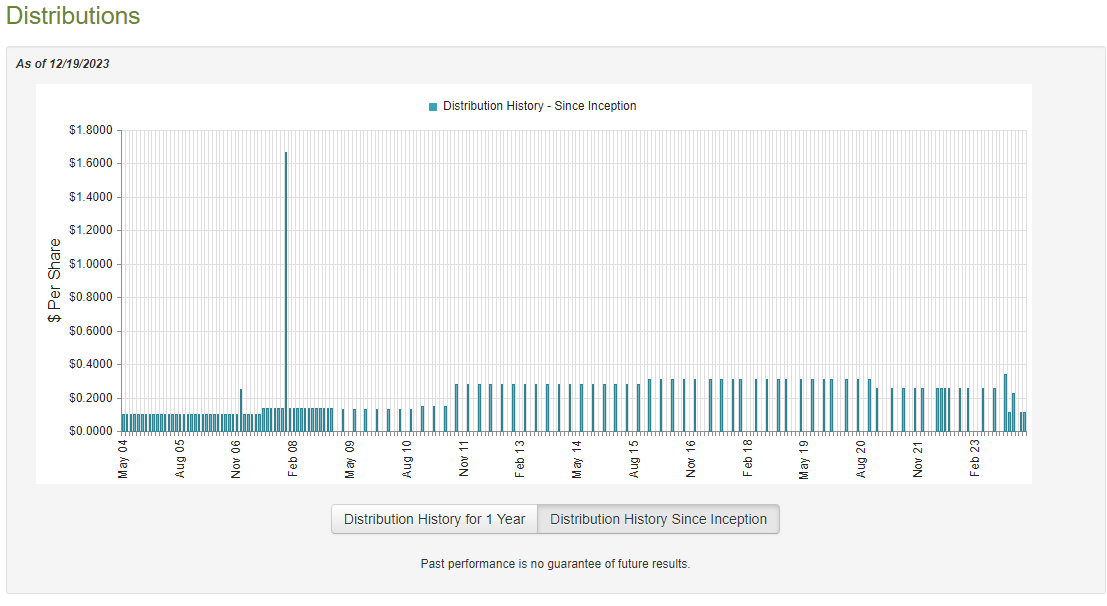

That is indeed the case, as the LMP Capital and Income Fund pays out a monthly distribution of $0.1130 per share, which gives it a 9.94% distribution yield at the current price. That is certainly competitive with other closed-end funds that are available in the market. In fact, it is higher than many equity closed-end funds manage to provide. Unfortunately, the fund has not always been particularly consistent with respect to its distributions. As we can see here, the fund's payout has varied significantly from period to period:

{kind=link}

We can see that the fund has changed its distribution both positively and negatively several times over its history. This is something that may reduce the fund's appeal in the minds of those investors who are seeking a safe and consistent source of income to use to pay their bills or finance their lifestyles. However, it is not necessarily unusual for a fund to do this, as distributions sometimes depend on the returns that the fund actually manages to generate. After all, we do not want a fund to be paying out more than it can actually afford and destroying its net asset value. That is not a sustainable scenario over the long term.

However, as I have pointed out numerous times in the past, a fund's distribution history is not always the most important thing for us to consider. After all, anyone who purchases the fund's shares today will receive the current distribution at the current yield. This buyer will not be affected by any actions that the fund has had to take in the past. As such, the most important thing for our purposes today is how well the fund is able to sustain its current distribution.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, this report will not include any information about the fund's performance over the past six months. That is very disappointing because the excluded period includes both a very weak market during which asset prices declined overall and a rebound in that market that saw stocks and bonds shoot up and bond yields fall. This report will not provide us with any information about how well the fund managed to perform in that environment. We will unfortunately have to wait until the fund releases its full-year report to have that information, and this report will probably not be released for a few more months.

During the six-month period, the LMP Capital and Income Fund received $3,184,563 in dividends along with $56,964 in interest from the assets in its portfolio. We subtract out the money that the fund had to pay in foreign withholding taxes, which gives it a total investment income of $3,219,340 during the period. The fund paid its expenses out of this amount, which left it with $101,715 available for shareholders. As might be expected, that was nowhere close to enough to cover the distributions that the fund paid out to its shareholders over the period. The fund's distributions totaled $8,995,284 over the course of the six-month period. At first glance, this could be concerning as the fund did not have sufficient net investment income to cover the distributions that it made to its investors over the period.

However, there are other methods through which the fund can obtain the money that it needs to cover its distributions. For example, it receives distributions from the master limited partnerships that are contained in its portfolio. It might also be able to realize some capital gains when the securities in the portfolio appreciate. Realized capital gains and distributions from master limited partnerships are not considered to be investment income for accounting or tax purposes, but they obviously represent money coming into the fund that can be distributed to the investments. Unfortunately, the fund generally failed at this task during the reporting period. It did manage to realize $3,597,530 in net capital gains but this was fully offset by $5,700,223 net unrealized losses. Overall, the fund's net assets declined by $14,262,026 after accounting for all inflows and outflows during the period. While some of that decline in net assets was due to the fund repurchasing $3,265,764 of its own shares, it still failed to cover its distributions out of its investment profits.

This is a continuation of the fund's failure to fully cover its distributions during the preceding full-year period. Over the full-year period that ended on November 30, 2022, the fund's net assets declined by $25,231,815 after accounting for all inflows and outflows. Thus, the fund failed to fully cover its distributions over the trailing eighteen-month period. That suggests that the fund may be struggling to cover its distributions.

Fortunately, it does appear that this situation is improving. As we can see here, the fund's net asset value per share is up 14.21% year-to-date:

{kind=link}

This strongly suggests that the fund has been able to pay out all of its distributions this year and still has a great deal of money left over. It was able to accomplish that task solely out of its investment profits. This suggests that the fund can probably sustain its current distributions if it is able to maintain the performance that it has seen this year. While that will generally require a bull market, historically bull markets are more common than bear markets so overall the fund's distribution may be okay. We probably do not have to worry about a distribution cut unless we get a prolonged bear market in the near future.

Valuation

As of December 19, 2023 (the most recent date for which data is currently available), the LMP Capital and Income Fund has a net asset value of $15.59 per share but the shares currently trade for $13.49 each. This gives the fund's shares a 13.47% discount on net asset value at the current price. That is a much larger discount than the 11.68% discount that the shares have had on average over the past year. As such, the current price could represent a very good entry point for anyone who wants to add this fund to their portfolio.

Conclusion

In conclusion, the LMP Capital and Income Fund appears to be a reasonable way for investors to generate a high level of income without sacrificing the upside potential that is possible with common stock. The fund's 9.94% yield certainly proves to be sufficient to satisfy any income-focused investor, and its performance so far this year has been relatively decent. Indeed, it is hard to believe that this fund trades for as large of a discount as it currently possesses. It is certainly true that the fund's financial performance during the most recently reported eighteen-month period was less than stellar, but the net asset value has improved year-to-date, so it appears that it is covering all of its distributions. When we consider that the fund's portfolio is a bit more varied than ordinary equity closed-end funds, we can make a great case for purchasing this fund today.

For further details see:

SCD: Add Diversification To Your Portfolio With This High-Yielding Fund At A Discount