ET - SCD: Not A Bad Income CEF If It Can Sustain The 10.58% Distribution Yield

2023-08-15 18:33:28 ET

Summary

- The average American is facing high inflation, causing a strain on household finances and forcing people to find ways to boost their incomes.

- Investors can consider closed-end funds, like the LMP Capital and Income Fund, to earn a high level of income from their assets.

- The fund focuses on generating income through a portfolio of common equity, fixed-income securities, and master limited partnerships, offering a current yield of 10.58%.

- The fund failed to cover its distribution in the most recent period despite the market rebound year-to-date, which is very concerning.

- The valuation is quite attractive right now and the fund could be a good investment if it can sustain the distribution.

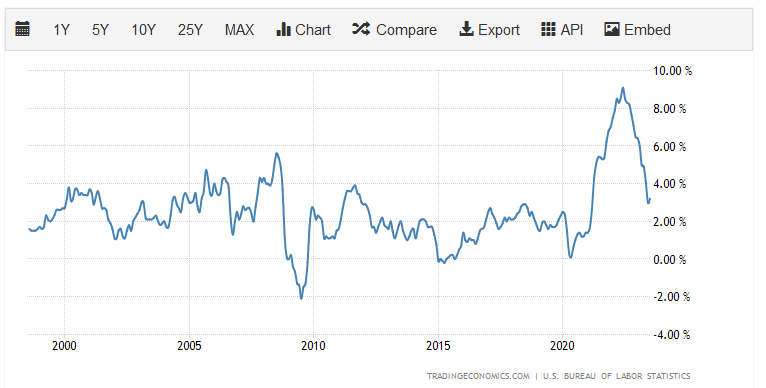

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high inflation that has been increasing the cost of living over the past two years. This is clearly evidenced by the consumer price index, which claims to measure the price of a basket of goods that is regularly purchased by the average American consumer. This chart shows the year-over-year change in this index during every month over the past twenty-five years:

{kind=link}

As we can clearly see, the consumer price index began to increase at a much more rapid rate than usual shortly following the COVID-19 pandemic and the economic shutdowns that accompanied it. The reason for this is that the Federal government implemented a number of policies that were ostensibly intended to keep the economy afloat during a period of time in which we were all forced to stay at home and away from most businesses. The Federal Reserve printed money to fund the wave of government spending, which increased the money supply by 40% during the period. Once everything started to reopen, people spent this money and because the actual productive capacity of the economy did not increase by anywhere close to 40%, it caused prices to surge.

The big problem with this is that real wages did not increase nearly as rapidly as prices did, which strained the finances of many households. This was particularly bad because approximately 64% of Americans live paycheck-to-paycheck and do not have the savings required to maintain their lifestyles when their real wages decline. As many of the price increases have been centered around food and energy, which are necessities, the higher prices cannot simply be avoided by eschewing luxuries. This has forced many people to resort to desperate measures such as dumpster diving, pawning possessions, or taking on second jobs simply to make ends meet. In short, people are desperate to boost their incomes in order to maintain their lifestyles.

As investors, we are certainly not immune to this. After all, we need food for sustenance and energy to heat our homes and businesses just like anyone else. However, we do have other methods that we can employ to obtain the extra income that we need to maintain our desired standard of living that do not rely on resorting to desperate measures. After all, we have the ability to put our money to work for us to earn an income. One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income. These funds are unfortunately not very well followed in the financial media and many investment advisors are unfamiliar with them so it can be difficult to obtain the information that we would really like to have to make an informed investment decision. That is a shame, because these funds offer a few advantages over ordinary open-ended and exchange-traded funds. In particular, these funds are capable of employing certain strategies that have the effect of boosting their effective yields well beyond that of any of the assets in the underlying portfolio.

In this article, we will discuss the LMP Capital and Income Fund Inc ( SCD ), which is one fund that investors can use to earn a high level of income from their assets. This is immediately apparent in the fact that this fund yields 10.58% as of the time of writing, which is substantially higher than nearly everything else in the market. It is certainly more than enough to turn the eye of any income-focused investor. Let us investigate and see if this fund could be a good addition to your portfolios today.

About The Fund

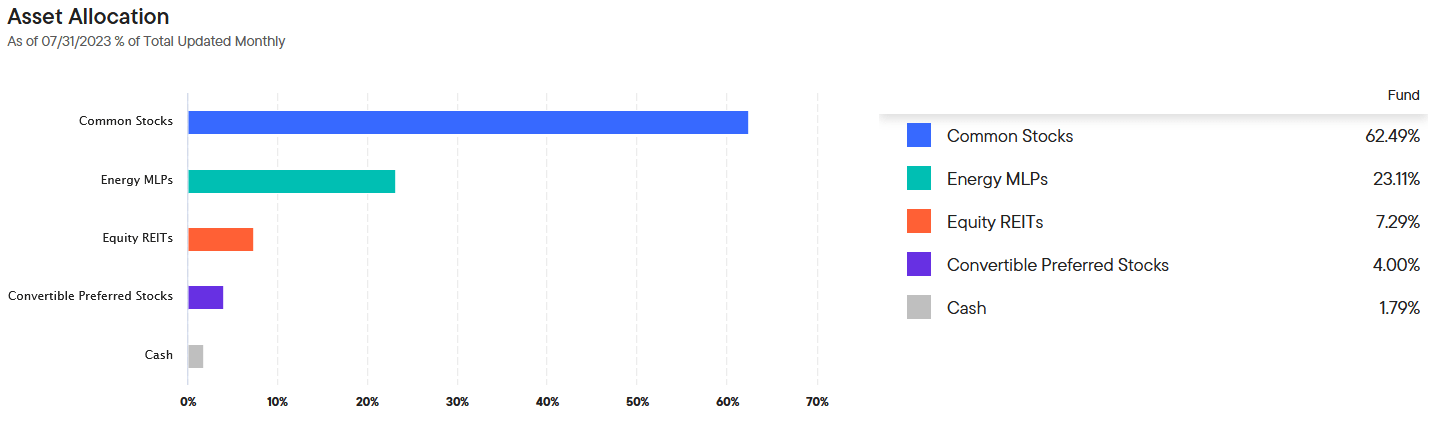

According to the fund’s webpage , the LMP Capital and Income Fund has the objective of providing its investors with a high level of total return. That is not particularly surprising as the name of the fund implies that it invests in both common equity and fixed-income securities. A look at the portfolio appears to confirm this, as 90.97% of its assets are currently invested in common equity, with much smaller allocations to cash and preferred stock:

CEF Connect

Common equity is generally considered to be a total return vehicle so the fund’s objective certainly makes a great deal of sense. After all, we typically buy common stock because we want to receive an income from the dividends that it pays out as well as benefit from capital gains as the issuing company grows and prospers. The preferred stock in the portfolio will deliver its returns primarily in the form of dividends paid to the investors so will primarily provide a certain amount of income to the fund. That does not change the fund’s claim that it is focusing on total return, as income is a component of total return. In fact, this fund specifically states that it is attempting to earn the majority of its total return in the form of income:

{kind=link}

The fact that this fund is prioritizing income in favor of capital gains tells us that the portfolio is almost certainly going to look very different from the S&P 500 Index ( SPY ). After all, the S&P 500 Index only yields 1.46% at its current level so its credentials as an income investment are pretty terrible. Indeed, one could simply put their money into a money market fund or a high-yield savings account and earn more income than the S&P 500 Index will deliver. The above overview of the fund hints at this as it specifically states that the fund will invest in master limited partnerships, real estate investment trusts, fixed-income securities, and common stocks. Curiously, the only one of these categories that will usually beat a money market fund is master limited partnerships.

The iShares U.S. Real Estate ETF ( IYR ) only yields 2.95% and even the Bloomberg U.S. Aggregate Bond Index ( AGG ) only yields 2.96% at the current price. Indeed, ten-year Treasuries are actually yielding less than the 5% that can be obtained with most money market funds. The Alerian MLP Index ( AMLP ) yields 8.17% right now so it is the only one of these that really has good income credentials right now.

The universe of common stocks is much larger than real estate investment trusts or master limited partnerships. As might be expected, the LMP Capital and Income Fund has a much higher proportion of its assets invested in common stocks than either partnerships or real estate trusts:

{kind=link}

While common stocks as a whole do not have particularly attractive yields, there are certain common stocks that have reasonably high yields. For example, Verizon ( VZ ) currently yields 7.78% and AT&T ( T ) is quite comparable to that. With that said, there have been a few analysts publishing reports here at Seeking Alpha over the past few months on some of these high-yielding stocks suggesting that their yields may not be sustainable. Even so, it does illustrate the point that while common stocks as a whole are not particularly attractive income vehicles, there are some individual common stocks that may be.

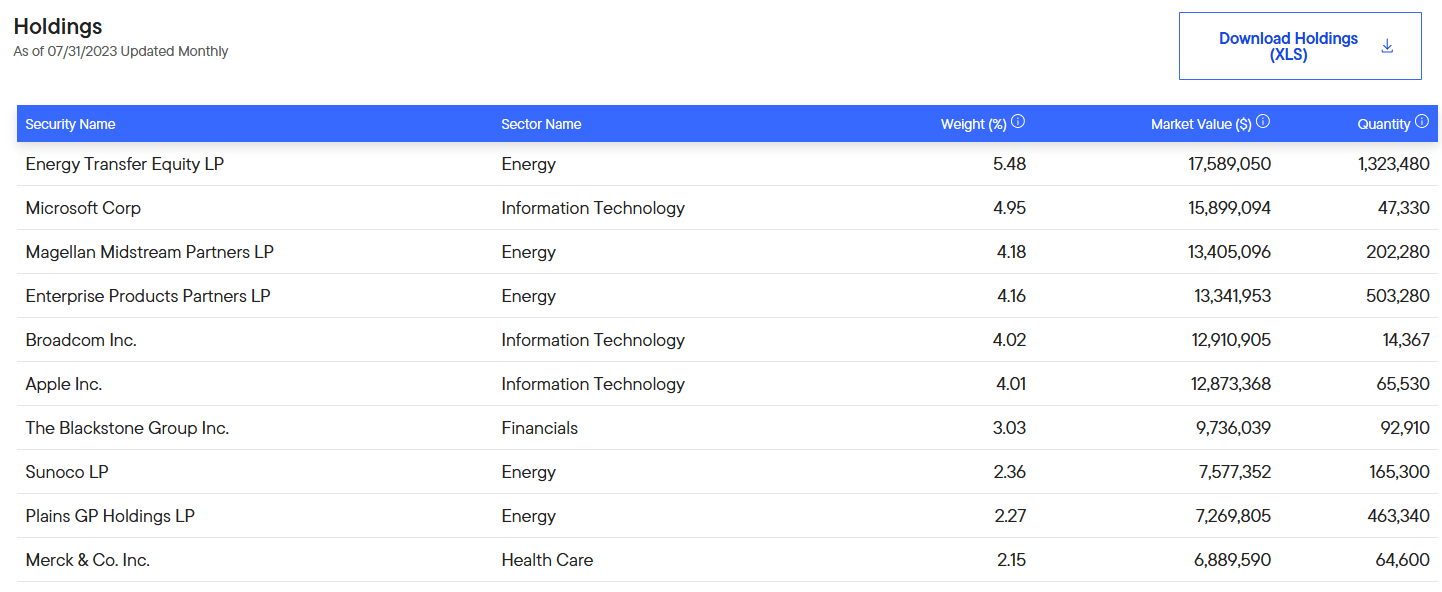

A look at this fund’s actual portfolio implies that its statement about targeting its portfolio toward the generation of income may be hyperbole. Here are the largest positions in the fund’s portfolio:

{kind=link}

Here are the dividend yields of these companies:

| Company |

| Type |

| Current Yield |

| Energy Transfer ( ET ) |

| Master Limited Partnership |

| 9.75% |

| Microsoft ( MSFT ) |

| Common Stock |

| 0.84% |

| Magellan Midstream Partners ( MMP ) |

| Master Limited Partnership |

| 6.37% |

| Enterprise Products Partners ( EPD ) |

| Master Limited Partnership |

| 7.47% |

| Broadcom ( AVGO ) |

| Common Stock |

| 2.15% |

| Apple ( AAPL ) |

| Common Stock |

| 0.53% |

| The Blackstone Group ( BX ) |

| Common Stock |

| 3.49% |

| Sunoco ( SUN ) |

| Master Limited Partnership |

| 7.54% |

| Plains GP Holdings ( PAGP ) |

| Master Limited Partnership |

| 6.41% |

| Merck & Co ( MRK ) |

| Common Stock |

| 2.68% |

As we can clearly see, the only assets in the fund’s ten largest positions that are better for income than a money market fund are all master limited partnerships. With that said, the fund may be able to essentially convert a common stock into an income vehicle for its investors by selling a small amount of its position. For example, if Apple appreciates 10% in a year, the fund could sell 10% of its position in order to leave the actual size of the position the same and still effectively end up with the same result as a stock that stays flat and pays a 10% dividend.

A look at the fund’s entire portfolio (downloadable from the webpage) reveals that the majority of the portfolio is invested in dividend-paying common stocks. This is a very different situation from many other common stock funds that include non-dividend-paying companies like Alphabet ( GOOG ), Meta Platforms ( META ), or Tesla ( TSLA ) among their top positions. This could be a good thing for those investors that are seeking to reduce their concentration risk. Concentration risk refers to the tendency of funds to invest their assets in the same stocks. For the most part, this includes all of the mega-cap technology stocks, Tesla, UnitedHealth Group ( UNH ), and a few of the other high market-cap companies that have been responsible for a substantial portion of the S&P 500 Index’s performance in recent years. This situation can result in an investor that is holding multiple funds believing that they have a diversified portfolio. However, this is not the case because all of the funds are holding the same stocks. The fact that this fund is holding different stocks thus allows it to improve the overall diversity of your portfolio, as well as fit in well with other funds without the problem of increasing your concentration risk.

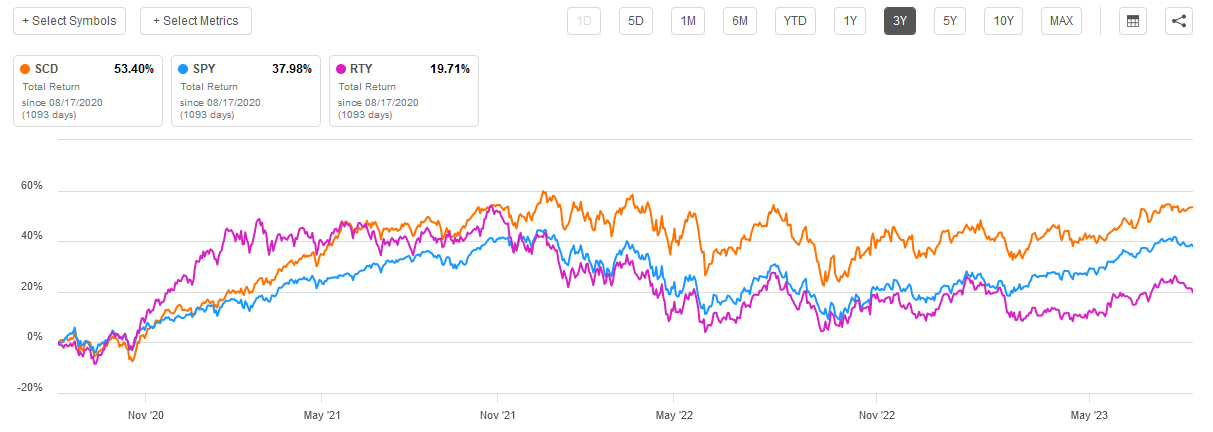

The fact that the fund’s portfolio has been avoiding some (but not all) of the high-flying technology stocks has not really hurt its performance. In fact, the fund managed to outperform the S&P 500 Index over the past three years:

{kind=link}

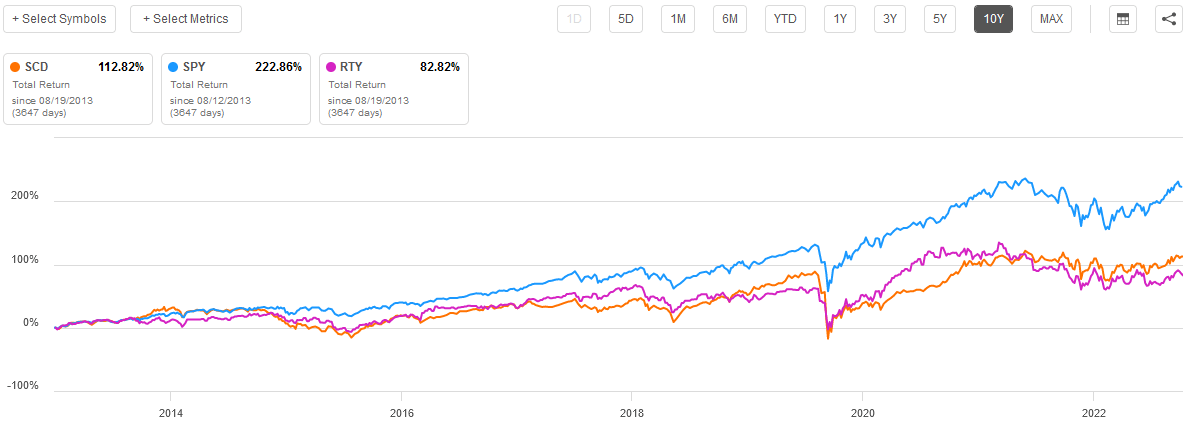

We also see that the LMP Capital and Income Fund managed to outperform the Russell 2000 Index ( RTY ) as well. Unfortunately, this outperformance has not extended over longer periods. The S&P 500 Index outperformed this fund over both the five-year and ten-year periods when measured on a total return basis. The S&P 500 Index also managed to beat it over the past twelve months. However, this fund has pretty convincingly trounced the Russell 2000 Index over pretty much any period that you want to measure. For example, the difference is quite pronounced over the past ten years:

{kind=link}

As numerous other analysts have pointed out before, the past decade has been one of the most interesting in history as ultra-low interest rates drove money into long-duration stocks as well as non-dividend-paying entities. It was previously something of a market truism that small-cap stocks outperform large-cap stocks over a long period. Thus, we would normally expect to see the Russell 2000 outperform the S&P 500 Index, but this was clearly not the case over the past decade. Unfortunately, that same market attention to huge non-dividend-paying companies resulted in the LMP Capital and Income Fund underperforming the S&P 500 Index over the period, although it did manage to beat the small-cap index. It is worth noting though that the above total return figures assume that all dividends and distributions paid out by the three assets are reinvested. It is a safe bet that anyone that is purchasing this fund for income is not going to reinvest all of the distributions. As such, most investors will probably see a lower total return from this fund than the above charts imply, but much larger amounts of cash income that can be spent on bills, luxuries, or whatever else you want.

Leverage

In the introduction to this article, I stated that closed-end funds like the LMP Capital and Income Fund have the ability to employ certain strategies that have the effect of boosting their yields well beyond that of any of the underlying assets in the portfolio, or indeed pretty much anything else in the market. One of these strategies is the use of leverage. In short, the fund borrows money and uses that borrowed money to purchase stocks, partnership units, and other income-producing assets. As long as the purchased securities deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to note though that this strategy is not as effective today with rates at 6% as it was eighteen months when the fund could borrow money for basically nothing. This is because the difference between the returns that the fund can get on the purchased assets and the amount that it has to pay on the borrowed money is not as great as it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason. Fortunately, this fund meets this criterion. As of the time of writing, the fund’s leveraged assets comprise 19.41% of its total portfolio. Thus, this fund appears to be striking a reasonable balance between risk and reward.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the LMP Capital and Income Fund is to provide its investors with a high level of total return with an emphasis on the generation of income. In order to achieve this, the fund invests in a combination of real estate investment trusts, master limited partnerships, preferred stock, and ordinary dividend-paying common stocks. While only the master limited partnerships boast a respectable yield, the fund can convert the other assets here to income by selling appreciated stocks. It then aims to pay out nearly all of its net investment income and returns to the shareholders. When we consider that the fund is employing a layer of leverage to boost its returns beyond those earned by the assets in the portfolio, we can assume that this fund would boast a reasonably high yield itself.

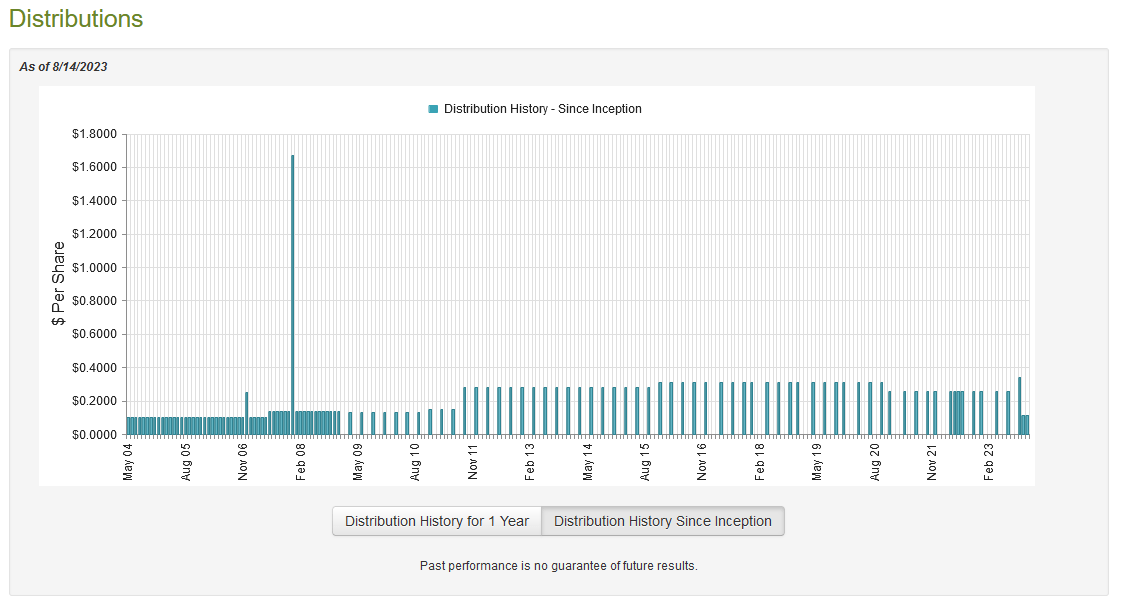

That is certainly the case as the fund currently pays a quarterly distribution of $0.34 per share ($1.36 per share annually), which gives it a 10.58% yield at the current price. Please note that the fund will be switching to a monthly payment schedule, with a monthly distribution of $0.1130 per share ($1.356 per share annually) beginning in November. Unfortunately, the fund has not been particularly consistent with respect to its distribution over the years. In fact, it has varied quite a bit:

{kind=link}

This is likely to reduce the fund’s appeal somewhat in the eyes of those investors that are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, many funds vary their distributions over time to correspond to the market returns that they are able to generate. The fund will naturally have to change its distribution to ensure that it is not paying out more than it is actually able to earn from its portfolio. After all, doing that would deplete its assets and make it ever more difficult to earn the returns that are necessary to sustain its distribution.

As I have pointed out in numerous previous articles though, a fund’s history is not necessarily the most important thing for anyone buying the fund today. After all, a new buyer will receive the current distribution at the current yield regardless of the fund’s past. In fact, someone buying today will be pretty much completely unaffected by the fund’s distribution history. The most important thing is how well it can sustain the payment going forward. Let us analyze its ability to do that.

Fortunately, we do have a very recent document that we can consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is one of the most recent reports that we currently have available for any closed-end fund, which is nice simply for its recency. The market has also generally been much better year-to-date than it was last year, so the fund may have had an opportunity to earn some respectable gains. That will, of course, be reflected in this report.

During the six-month period, the LMP Capital and Income Fund received $3,184,563 in dividends and $56,964 in interest from the assets in its portfolio. After we net out the money that the fund had to pay in foreign withholding taxes, it had a total investment income of $3,219,340 over the period. It paid its expenses out of this amount, which left it with $101,715 available for shareholders. Obviously, that is not enough to cover any distributions, but the fund still paid out $8,995,284 during the period. At first glance, this is likely to be concerning as the fund did not have sufficient net investment income to cover its distributions.

However, a fund like this does have other methods through which it can obtain the money that it needs to cover the distributions. For example, it might have been able to generate capital gains that can be paid out to the investors. In addition, this fund receives some money from the master limited partnerships in its portfolio that is not included in net investment income.

Unfortunately, the fund generally failed here. It reported net realized gains of $3,597,530 but this was offset by $5,700,223 net unrealized losses during the period. Overall, the fund’s assets declined by $14,262,026 after accounting for all inflows and outflows during the period. This is a clear sign that the fund failed to cover its distributions over the period. It is curious, then, that it just recently increased the distribution, as it is not going to be able to sustain that unless its financial performance improved. This is possible, but it is difficult to believe that the fund managed to earn more money through investment returns in the past two months than it did in the full six-month period that included much of the market rebound. We will want to keep a sharp eye on this fund’s finances.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the LMP Capital and Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them for less than the net asset value. This is because such a scenario implies that we are obtaining the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of August 14, 2023 (the most recent date for which data is available as of the time of writing), the LMP Capital and Income Fund has a net asset value of $14.78 per share but the shares only trade for $12.86 each. This gives the fund’s shares a 12.99% discount on net asset value at the current price. That is a very reasonable price to pay for the fund, although it is not as good as the 15.27% discount that the shares have had on average over the past month.

Conclusion

In conclusion, the LMP Capital and Income Fund appears to be a very reasonable way for an investor to earn a very high yield from their portfolios today. The fund boasts a double-digit yield and a distribution that has just increased, but it is uncertain whether or not it can actually sustain the new payout. The fund almost appears to be trying to boost its share price through any means necessary. The portfolio does offer a nice mix of assets that are different from other funds, so it can add a certain amount of diversity to a portfolio. The current valuation is also quite attractive. Overall, there are certainly a lot worse funds out there, we just need to watch and make sure that this one can actually sustain that distribution.

For further details see:

SCD: Not A Bad Income CEF If It Can Sustain The 10.58% Distribution Yield