SLB - Schlumberger: Double-Digit Earnings Growth As Energy Industry Expects Tailwinds In 2024

2024-01-05 12:12:45 ET

Summary

- Schlumberger is rated Buy. My bullish sentiment is shared by consensus from SA analysts and Wall Street.

- The company saw double-digit growth in the top & bottom lines, and equity growth driven by lower debt.

- Projections for the oil & gas industry remain positive going into 2024, which should favor this firm, a market leader in services for this sector.

Stock & Industry Snapshot

Today's research note goes behind the scenes of the oil and gas industry by covering a company that makes a lot of the magic in this industry happen.

That company? Houston's own Schlumberger ( SLB ) .

A few quick company facts are that it provides services like well construction, cloud-based digital solutions for the industry, geothermal energy projects, and more. For those readers less familiar with this company, think of it not in the same vein as an oil company such as Valero ( VLO ) or Exxon ( XOM ), but a services company supporting companies like those and helping make oil exploration possible.

From its profile page we know it trades on the NYSE and is in business since 1926, so a well-established company.

Recent sector performance from SA market data shows the energy sector showing triple-digit performance on a 3-year basis, although in the shorter-term it barely saw improvement of 3% or less. This is relevant since I believe an overall sector being bullish or bearish could have an impact on a stock within that sector.

energy sector market data (Seeking Alpha)

Scoring Matrix

We use a 9-point scoring method that looks at this stock holistically and assigns a total rating score, using a score matrix.

{kind=link}

Today's Rating

Based on the score total in the score matrix , this stock is getting a rating of buy.

Compared to the consensus rating on Seeking Alpha, I am agreeing with the consensus from SA analysts and Wall Street:

SLB - rating consensus (Seeking Alpha)

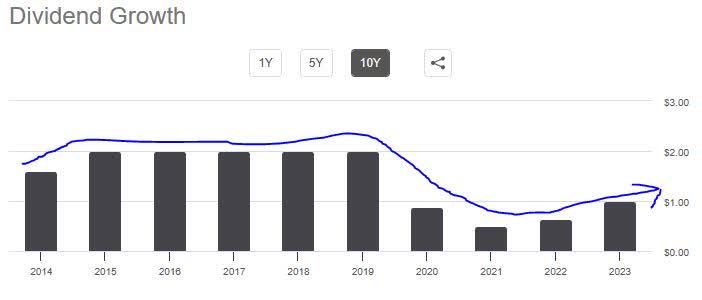

Dividend Income Growth

We will look at the 10-year dividend growth chart to spot any trends relevant to a dividend-income investor.

{kind=link}

In the chart above, I traced the trend, which shows the annual dividend hitting a plateau for many years and then dropping. If I had bought this stock in 2014, the annual dividend would have been $1.60, vs $1 in 2023, a 37% decline in a decade.

Looking at the payout history , we can see the quarterly payouts are steady but currently stuck at $0.25/share.

I think a positive tailwind to 2024 dividends could come from the fact that the company is profitable and has grown YoY earnings in the last reported quarter, and also has shown positive cash flow .

In this category, I would call this stock a hold , due to evidence showing lack of 10 year dividend growth since 2014, but also having steady quarterly payments and higher potential for further dividend hikes in 2024 if their positive earnings and cashflow continues.

Dividend Yield vs Peers

Next, let's talk about the dividend yield . Using the yield comparison tool from Seeking Alpha, I am comparing the yield of this stock vs 3 peers in the energy sector.

{kind=link}

For this peer group, in addition to Schlumberger I also picked energy-sector services companies like Halliburton ( HAL ), Oceaneering ( OII ), and Baker Hughes ( BKR ).

Of this group, my stock was 2nd place with a yield of 1.90%, while Baker-Hughes led the pack with a yield of 2.30%.

Considering the overall sector average is closer to 3.60%, I must admit that Schlumberger is hitting the lower end of that range and not too impressive with a yield less than 2%.

If I were adding some energy-sector stocks to my portfolio and focused on dividend yield, I would consider Sunoco ( SUN ) at a yield of 5.79% .

In this category, I would give Schlumberger a hold.

Revenue Growth

What we can see from the income statement is that top-line revenue growth jumped to $8.3B in the quarter ending September, vs $7.47B in Sept 2022, an 11% YoY growth.

With the next earnings results just two weeks away on Jan. 19th, the question is whether revenue growth is expected to be sustainable going into 2024?

From the sentiment I gathered in their Q3 earnings comments, it appears that this firm is anticipating a tailwind in 2024 for its business, which is globally diversified.

Here is what CEO Olivier LePeuch had to say:

Looking ahead, we believe the market fundamentals remain very compelling for our business. The oil and gas industry continues to benefit from a multiyear growth cycle that shifted to the international and offshore markets where we are the clear leader.

In the fourth quarter, we expect continued sequential revenue growth driven by year-end sales in Digital & Integration and seasonal product and equipment sales in Production Systems. In addition, the fourth quarter will reflect the results of the OneSubsea joint venture.

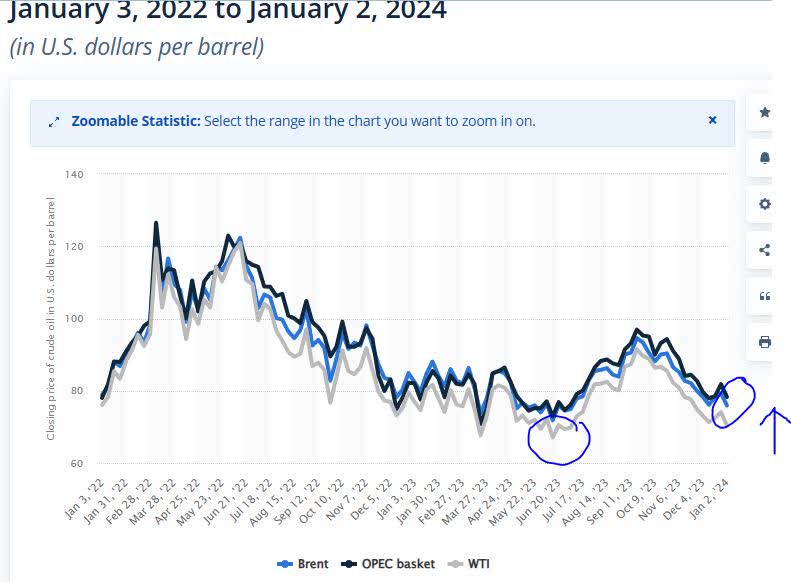

In this category, I would call this stock a buy, on the basis of double-digit YoY revenue growth as well as future positive growth sentiment from the company, but also according to Statista data it appears oil prices have recovered somewhat from a summer slump, though not quite at the levels they were in spring 2022. I believe higher oil prices could lead to energy companies spending more on services and exploration, rather than cutting back.

{kind=link}

Earnings Growth

Also, from income statement data , we can paint an earnings picture for this firm.

What it tells us is that earnings jumped to $1.12B in Q3, vs $907MM in Sept 2022, a +23% YoY growth.

We already mentioned the company's positive growth outlook going forward, but now let's mention something about costs.

We can see that interest expense growth remained roughly low on a YoY basis and not significant, and total operating expenses jumped a bit.

Also notable to mention is significant margins lately. According to remarks by CFO Stephane Biguet:

Margins expanded 147 basis points to 13.5% representing the highest margin since we began reporting results for the division. This expansion was primarily driven by higher sales of completions, artificial lift and surface production systems as well as pricing improvements.

Based on this double-digit earnings growth which I expect to be sustainable going forward as the evidence of global growth for this business points to it, I will be calling this stock a buy in this category.

Equity Positive Growth

Now, to mention something about the company's equity growth, let's refer to the balance sheet .

What we can see is that total equity (book value) grew to a stunning $19.7B in Sept 2023, vs $17.5B in Sept 2022, a YoY growth of 12.5%.

A positive mention I want to highlight is declining long-term debt. It went down to $11.38B in Q3 vs $12.45B in Sept 2022, an 8.5% decline in debt.

At the same time, the company is cash-rich with $2.4B in cash and equivalents.

My sentiment is positive in this category, fueled by the CFO's remarks indicating cash flow strength leading to lower debt:

As a result of our strong cash flow performance, our net debt reduced sequentially $731MM to $9.4B. Our net debt to trailing 12-month EBITDA leverage ratio of 1.2 is at its lowest level since 2015.

I think the evidence points to this stock being a buy in this category of equity.

Share Price vs Moving Average

When considering the stock is trading below its 200-day moving average (as of this article writing) and also the other data I discussed which shows double-digit growth in earnings, revenue, and equity, I think this can be called a value opportunity at the current price range and I will call it a buy .

Valuation: Price-to-Earnings

From valuation data , I am looking at the GAAP-based forward P/E ratio as a key valuation metric to compare the gap between price to earnings. Right now, the multiple is 17.69x earnings, which is 65% above the sector average that hovers closer to 11x earnings.

I think what could be driving this elevated price multiple is the recovery in share price, which is trading around the moving average now. So, the driver is price .

However, at the same time, earnings grew by double-digits on a YoY basis and currently have a positive outlook from the company.

On the surface, a 17.6x price multiple may appear justified given that earnings grew 23% YoY, however consider that I am also comparing peers and looking to pick one out of the bunch with the best valuation.

If you consider that its peer Halliburton is also trading around its 200-day SMA now, and also achieved +30% YoY earnings growth but has a forward P/E multiple of just 12.18x, and it is a much more justified valuation and one I would pick.

In this category, then, I think that Schlumberger is more of a hold at this valuation, than a buy or sell.

Valuation: Price-to-Book Value

Turning again to valuation data , now let's look at the forward P/B ratio.

Again, we see an elevated multiple of 3.66x book value. This is 122% vs the sector average that hovers around 1.65x book value.

I think, again, what is driving this is the rise in the share price.

We also discussed the double-digit equity growth of this firm already as well.

Again, I am compelled to call this a hold at this price multiple since equity rose along with the share price, but I think a 3.6x multiple is somewhat too high to call a buy right now. Consider that its peer Baker Hughes has a price to book valuation of just 2.26, and also has seen YoY equity growth, so that would appear to be a better buy in terms of this specific metric.

Risk Analysis

It has come down to the wire in deciding whether this stock is a buy or a hold, and the deciding factor appears to be this quick risk analysis I will do.

The potential downside risk I think could come from oil prices impacting investment and spending by the energy sector. We already looked at the oil price chart from Statista and know the industry took a hit in the pandemic period when demand dropped, then later went up again, and now the question is what happens in 2024.

In another article covering Delta Air Lines ( DAL ) I argued that travel demand will be on the rise, benefiting airlines but by extension also the oil industry that fuels them.

More importantly, I want to point your attention to a late-December article in Reuters . The piece highlights the energy industry's multi-billion-dollar deal making spree in 2023.

Also, according to the article:

Three-quarters of energy executives polled in December by the Federal Reserve Bank of Dallas expected more oil deals worth $50 billion or more to pop up in the next two years.

Further, a news article 5 days ago in Investopedia pointed to the general sentiment that oil will go higher in 2024.

According to the story:

Most public- and private-sector forecasts point to higher global oil prices in 2024.

Even against the backdrop of continued concerns about a potential recession, BofA (Bank of America) sees much more potential for oil prices to surge unexpectedly than to fall.

"While downside [price] risk remains limited, upside risks to oil prices could come from Middle East tensions, U.S. sanctions enforcement, and potential Fed rate cuts," BofA said.

So my outlook is that the evidence supports a buy rating on this stock, in the category of risk.

Quick Summary

To summarize, I am going bullish on this stock and giving it a buy , based on the holistic picture and evidence overall.

It is a company with double-digit revenue, earnings, and equity growth along with declining debt and strong future global growth projections.

It is not much of a dividend play, with a poor history of dividend growth, and a below average yield at less than 2%.

My portfolio strategy on this one would be to buy in the current price range and hold until it climbs about 10 to 15% above its 200-day SMA, which I think can be achieved in 2024 if both oil prices rise and its own earnings continue to outperform.

For further details see:

Schlumberger: Double-Digit Earnings Growth, As Energy Industry Expects Tailwinds In 2024