SLB - Schlumberger Is A Buy As Net Zero May Be Failing

2023-05-29 06:30:00 ET

Summary

- Schlumberger is a global energy equipment and service provider that recognizes the importance of fossil fuels and supports clean energy solutions.

- The company has shown strong performance, with a focus on digital solutions and international growth, and anticipates durable revenue growth in key markets.

- SLB is trading at an attractive valuation, and investors interested in equipment providers may consider buying shares below $40.

Introduction

It's time to talk about oil and gas infrastructure. And what better way to do that than by discussing one of the world's largest energy equipment and service providers Schlumberger ( SLB ) .

{kind=link}

This Texas-based giant with a market cap of more than $60 billion is currently trading 25% below its 52-week high, as the market has shifted its focus from value to growth stocks, incorporating elevated recession odds, which hurts companies like SLB.

While this isn't fun for existing shareholders, it's great news for investors looking to buy (more) SLB shares. While I usually prefer low-cost drillers instead of equipment producers, SLB is a great way to benefit from much-needed global investments in fossil fuels.

The company understands that net zero isn't happening the way it was designed to. The world needs fossil fuels, which we are currently finding out the hard way through elevated prices. I expect that to get much worse the moment economic demand bottoms.

Hence, it's time to take a closer look at the new and improved SLB.

SLB Knows Net-Zero Isn't Happening

This is the point where I need to clarify to new readers that I'm not against clean energy - far from it. While I have close to 20% oil exposure, I'm not a shill for fossil fuel companies and write content to somehow try to stop the trend towards clean energy.

No. I'm all for lower pollution, cleaner supply chains, less waste, etcetera. My point is that the energy transition is forced and technically just based on taxing fossil fuels to make expensive renewables more attractive. Not only do we not have enough materials to make net zero a reality, but we're also pressuring fossil fuels so much that investments in that area are underwhelming, causing a supply gap that caused oil and gas prices to fly the moment post-pandemic demand rebounded.

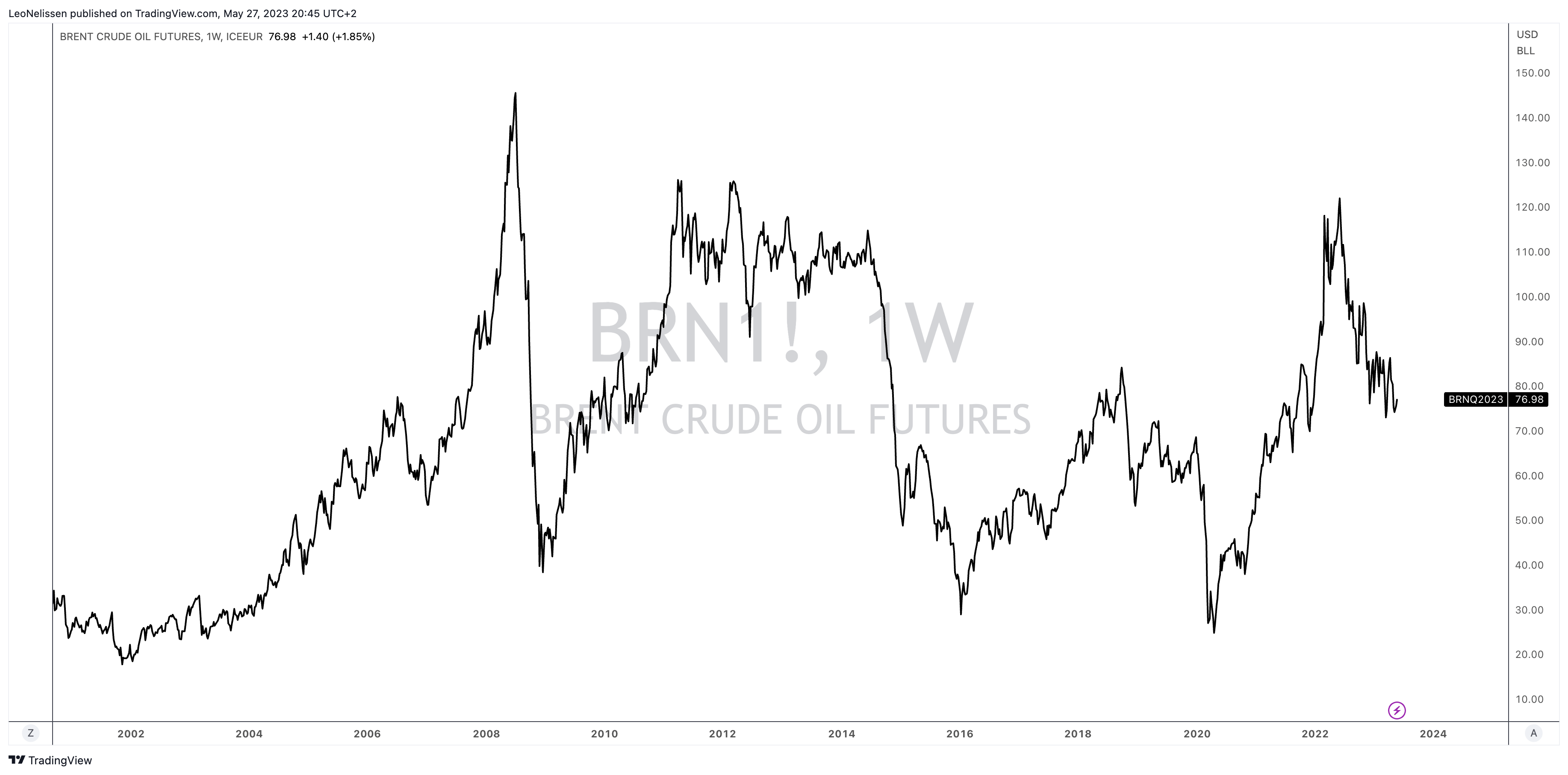

While oil prices are well below their highs, they are still elevated compared to prior cycles, as supply growth is in a very bad place - I discussed that in this article (among many others).

{kind=link}

One of Germany's leading newspapers, WELT , recently covered net-zero developments - using reports from the International Energy Agency, which is highly biased towards renewables.

The report revealed that global investors are now putting more money into solar energy than oil production. However, the numbers suggest that this does not necessarily translate into significant progress in climate protection.

According to the IEA report, investments in fossil fuels have increased by 15% since 2021, while investments in green energy have grown by 24%. The report states that for every $1 invested in fossil fuels, $1.7 is invested in clean technologies.

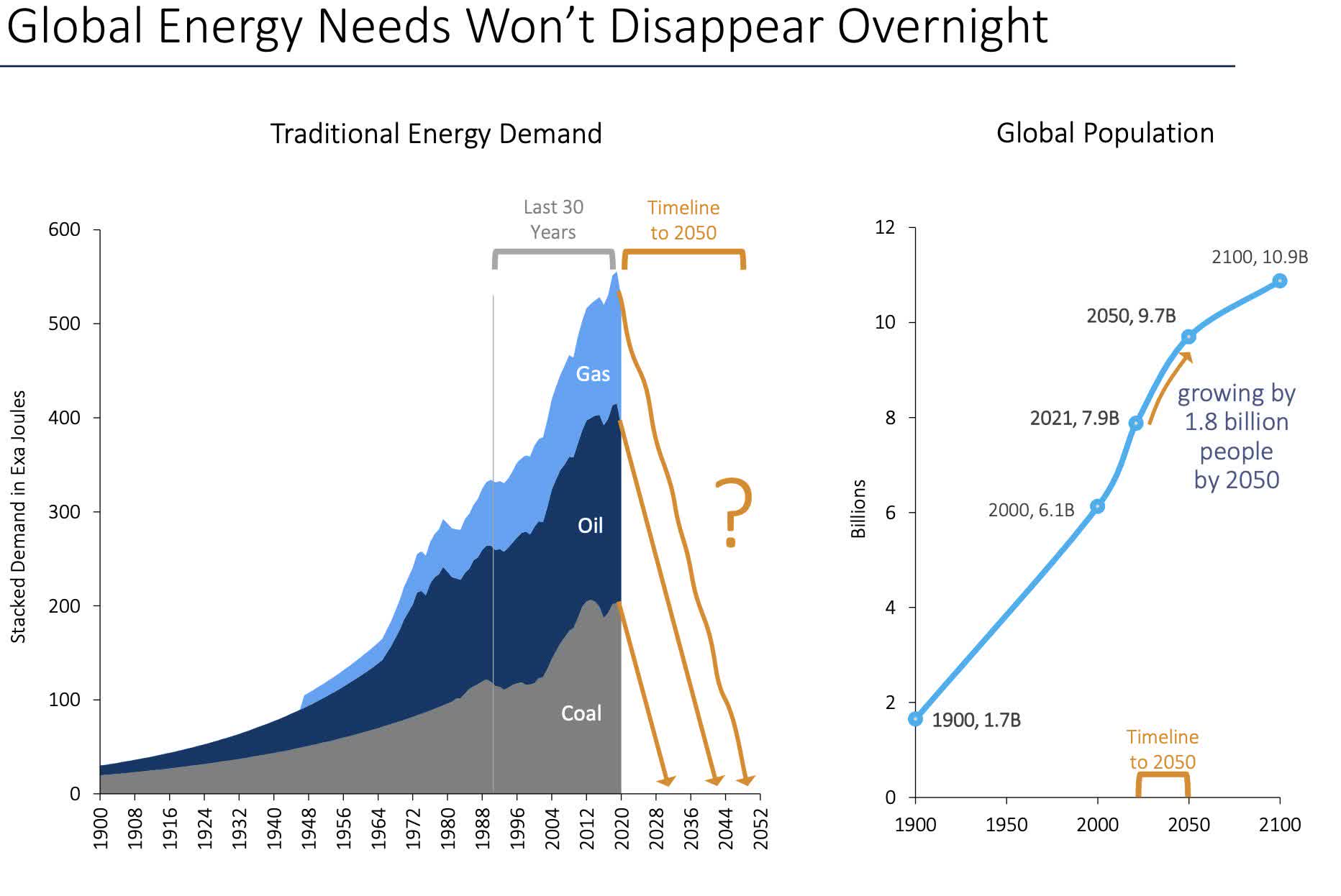

While investments in renewable energy are growing, investments in fossil fuel extraction continue, which is incompatible with the United Nations' goal of achieving net-zero greenhouse gas emissions by 2050. Expenditures for oil and gas production are expected to increase by 7% this year, reaching around $500 billion. This is roughly in line with pre-pandemic levels in 2019.

Enterprise Products Partners ( EPD ) highlighted the ridiculous 2050 goals, which essentially aim to erase more than 100 years of energy progress within thirty years - while the global population is still growing. There's no way renewables can decarbonize the global economy.

{kind=link}

Furthermore, investments in coal mining are also increasing globally by around 10% this year, surpassing pre-pandemic levels in 2019.

Again, I'm not against clean energy. I'm just against forcing a trend that cannot be forced - at least not without negative consequences.

With all of this in mind, Schlumberger - or SLB - recognized this and decided to incorporate it into its identity .

{kind=link}

Last year, the company changed its name to SLB to highlight its vision for a decarbonized energy future and reflect its transformation into a global technology company dedicated to driving energy innovation. T

Essentially, the company aims to strike a balance between energy affordability, security, and sustainability by promoting innovation and decarbonization in the oil and gas industry, as well as advancing clean energy solutions. SLB's new identity symbolizes its commitment to addressing current energy needs while leading the way in the energy transition.

I believe this is an incredibly corporate/fancy way of saying we'll keep doing what we're doing. We'll just rebrand it a bit. After all, the company's business remains focused on fossil fuel support:

{kind=link}

Again, given my view on energy, that makes sense for SLB and its shareholders.

SLB/Schlumberger Is Doing Very Well, Seeing More Upside

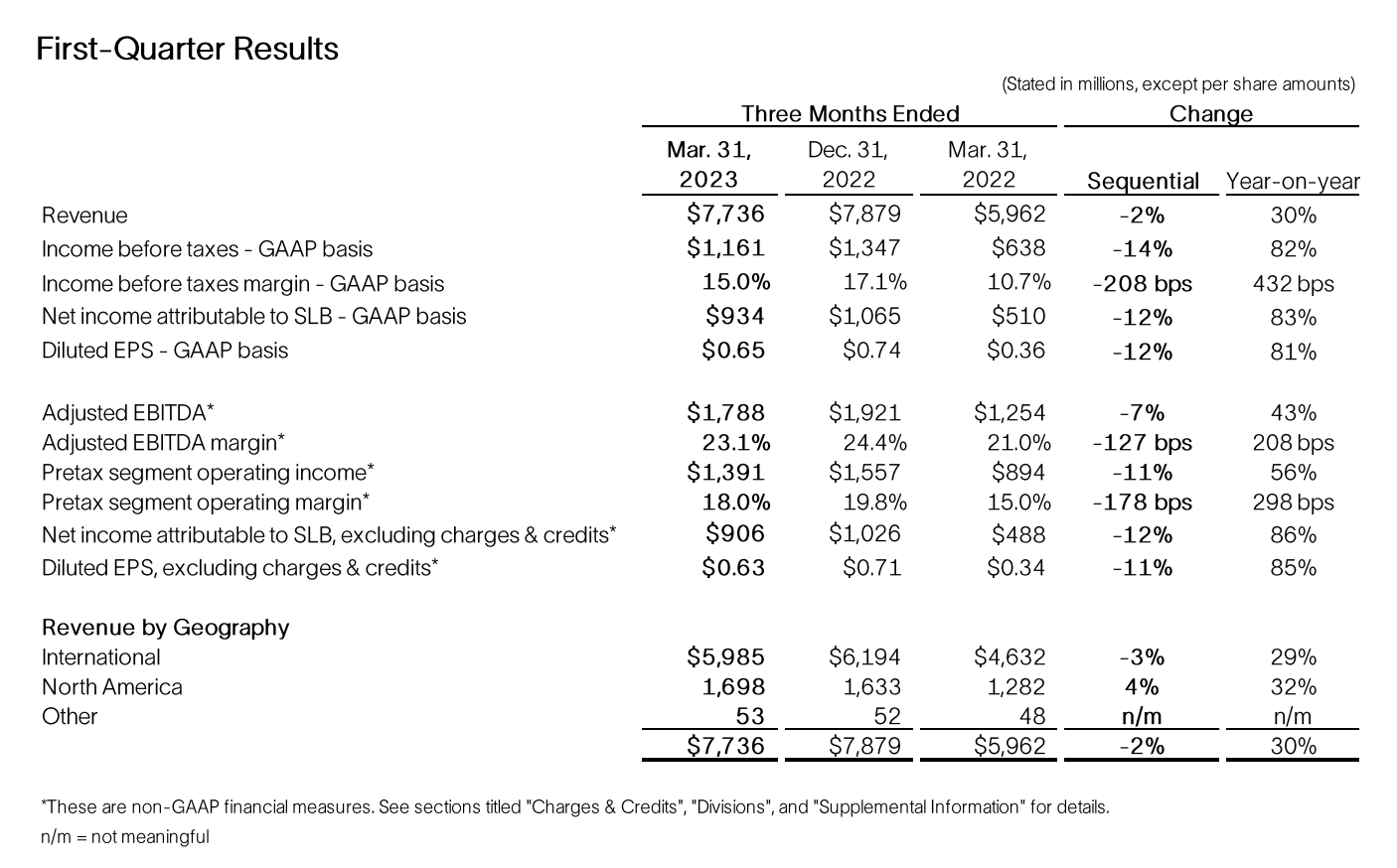

In the first quarter, SLB generated $7.7 billion in revenue, which beat estimates by$240 million. The year-on-year growth rate was 30%.

{kind=link}

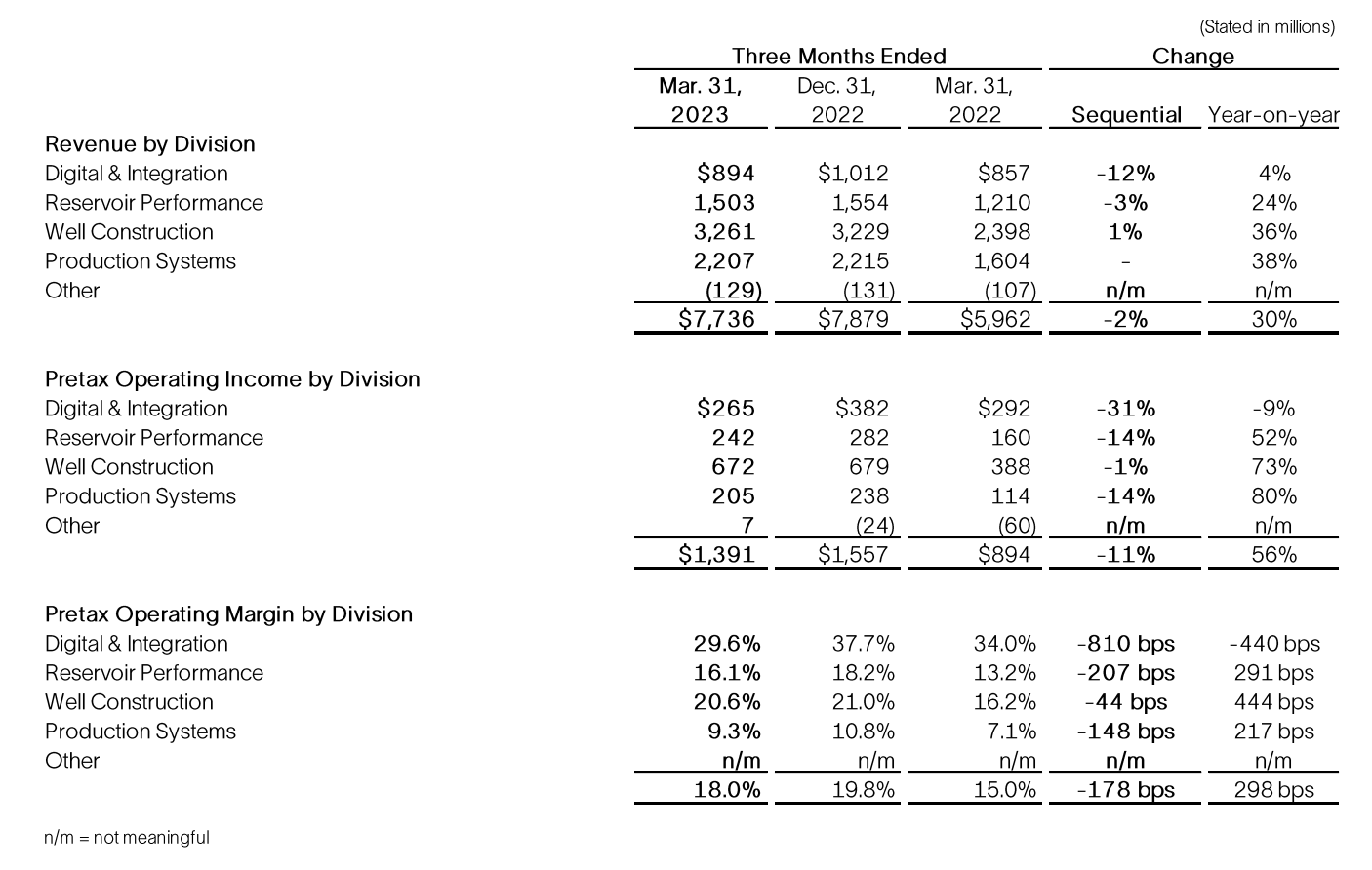

The Digital & Integration division's revenue decreased by 12% sequentially to $894 million, mainly due to lower APS project revenue and seasonally lower digital and exploration data licensing sales. Margins declined by eight percentage points to 30%.

However, strong digital growth, including a more than 50% increase in cloud and edge solutions, offset the decline in APS revenue. I expect cloud-based services to continue rapid growth in the years ahead. Also, margins are expected to improve in Q2 with the resolution of the pipeline issue in Ecuador and a sequential increase in digital sales.

The Reservoir Performance division reported a 3% sequential revenue decrease to $1.5 billion, primarily driven by seasonal activity reductions in Europe and Asia and lower revenue in Russia. Margins declined by 207 basis points to 16.1%. However, compared to the prior year, revenue grew by 24%, and margins increased by 291 basis points, fueled by strong international growth on land and offshore, which is essentially what we discussed in the first part of this article.

{kind=link}

The Well Construction division saw a 1% sequential increase in revenue to $3.3 billion, which came with a 44 basis points decrease in margins to 20.6%. On a year-on-year basis, revenue grew by 36%, while margins expanded by 444 basis points. The growth was caused by increased activity, higher pricing, and a favorable technology mix across all areas.

The production Systems division's revenue remained flat sequentially at $2.2 billion, with margins declining by 148 basis points to 9.3%.

This was influenced by seasonality and the activity mix in Europe and Asia. However, year-on-year revenue increased by 38%, and margins expanded by 217 basis points. Strong activity levels were observed in Europe, Latin America, and North America, while supply chain and logistics constraints continued to ease.

Especially the supply chain comment is important, as it could indicate that drilling becomes more affordable to some, which could increase margins for upstream drillers. That's something I will be looking for in the next earnings season.

With that said, the company is very upbeat about its future.

In its earnings call , the company highlighted that the Production Systems Division is a long-cycle lever of growth, expecting cumulative bookings of $10 billion to $12 billion in 2023.

The Middle East and offshore basins are key market areas for SLB, and the company anticipates durable revenue growth and a significant installed base for services in the coming years, which is also in line with what we discussed in the first half of this article.

Also, the Deepwater subsea market remains essential to SLB's growth opportunity, with the company strengthening its portfolio in that area.

Given how conservative SLB usually is, I believe that its focus on deepwater is a sign that the company is betting on sustained elevated oil prices.

CEO Le Peuch also mentions the sustained momentum and EBITDA margin growth expected in the subsea business. He believes that SLB is well-positioned to execute its returns-focused strategy, capitalize on international and offshore momentum, and expand margins.

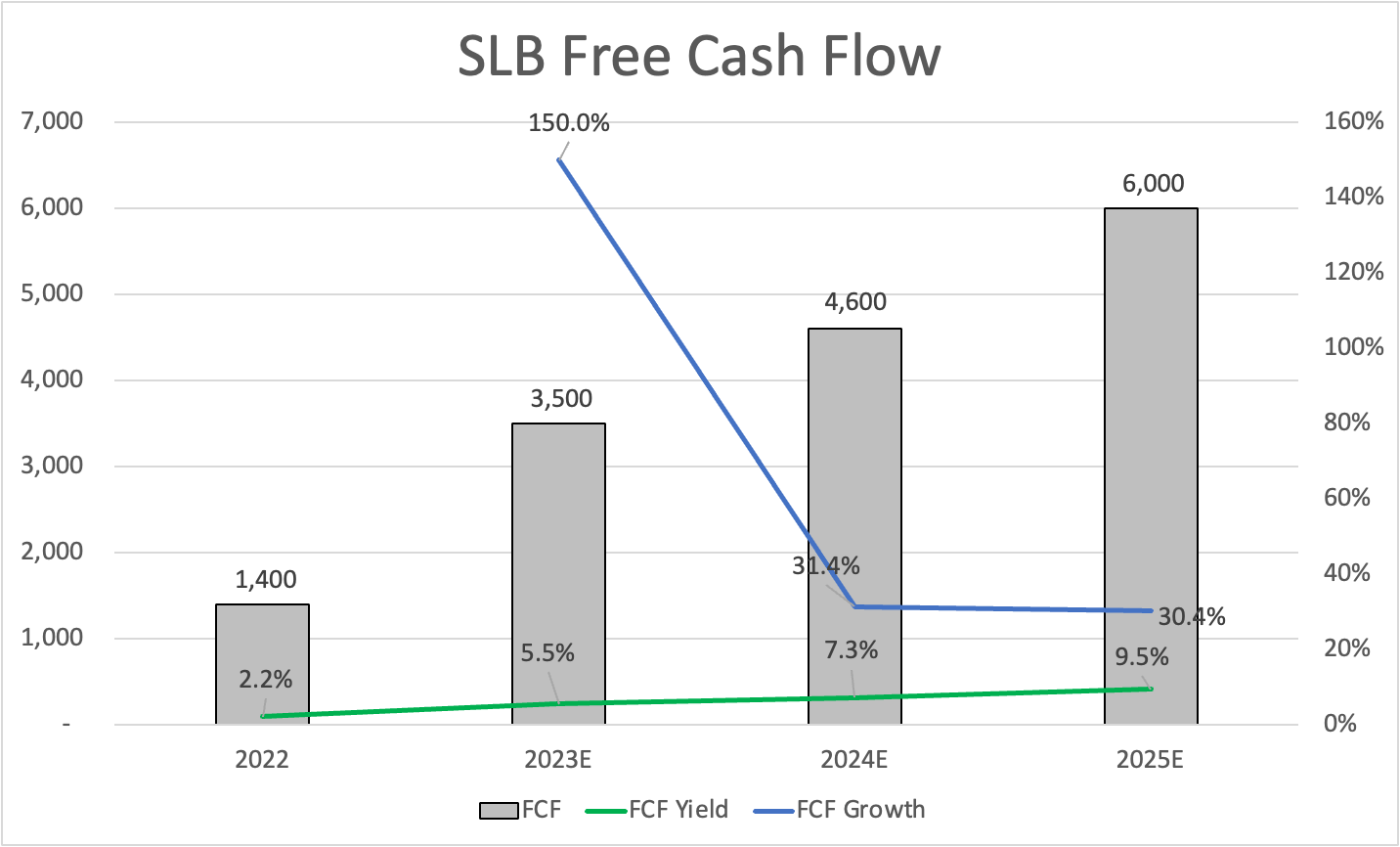

Analysts agree with SLB management. The company is expected to boost its free cash flow to $6 billion in 2025, which implies a free cash flow yield of 9.5% using the company's current $63.4 billion market cap.

{kind=link}

According to the company, the Middle East, international offshore basins, and gas projects are expected to comprise a significant portion of global upstream spending, while North America will benefit from a positive demand outlook and commodity pricing. I agree with these comments, especially with the demand side, which is likely to have a very strong impact on commodity pricing and project profitability. That's great for SLB, even if equipment growth rates are unlikely to go back to pre-pandemic levels (in my opinion). After all, most Western drillers aren't eager to boost output anymore.

Hence, the company highlighted the Middle East and offshore markets as anchors of supply growth, with unprecedented investment visibility and potential for growth.

Especially the offshore sector is projected to experience its highest growth in a decade, with significant activity in infill and tieback projects, large development projects, and exploration and appraisal activities.

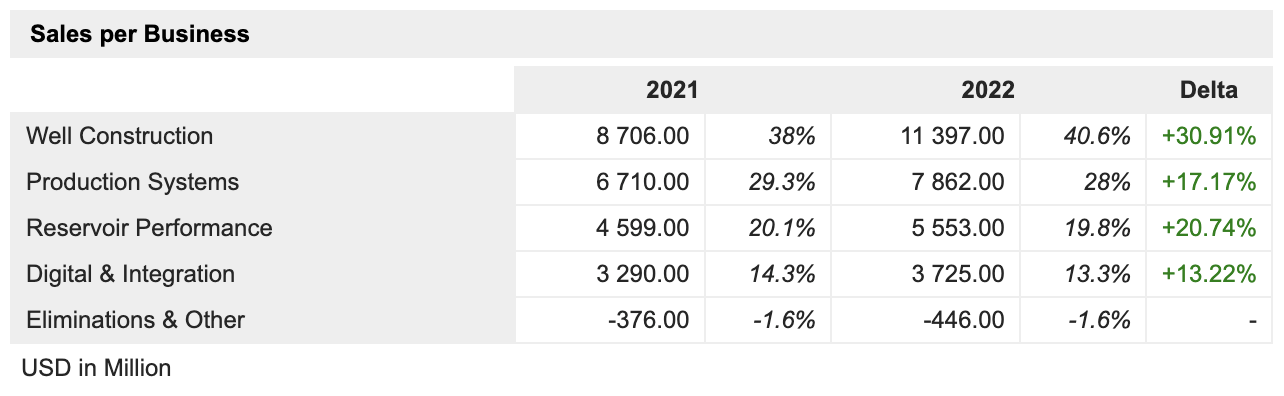

Hence, I believe that SLB is a more attractive investment than providers of onshore equipment in North America. In 2022, SLB generated just 16% of its revenues in the United States.

Valuation

SLB, which enjoys an A credit rating, is trading at roughly 8.9x 2023E EBITDA, which is based on its $63.4 billion market cap, $8.4 billion in expected net debt (1.0x EBITDA), and roughly $500 million in pension liabilities and minority interest.

I believe these valuations are attractive, even if estimates were to come down further due to economic headwinds.

SLB usually trades at 10x EBITDA, which makes sense given the company's ability to generate free cash flow.

So, conservatively speaking, I believe that SLB is at least 40% undervalued, which would put the current fair value at roughly $63, which is in line with current consensus estimates of $64.

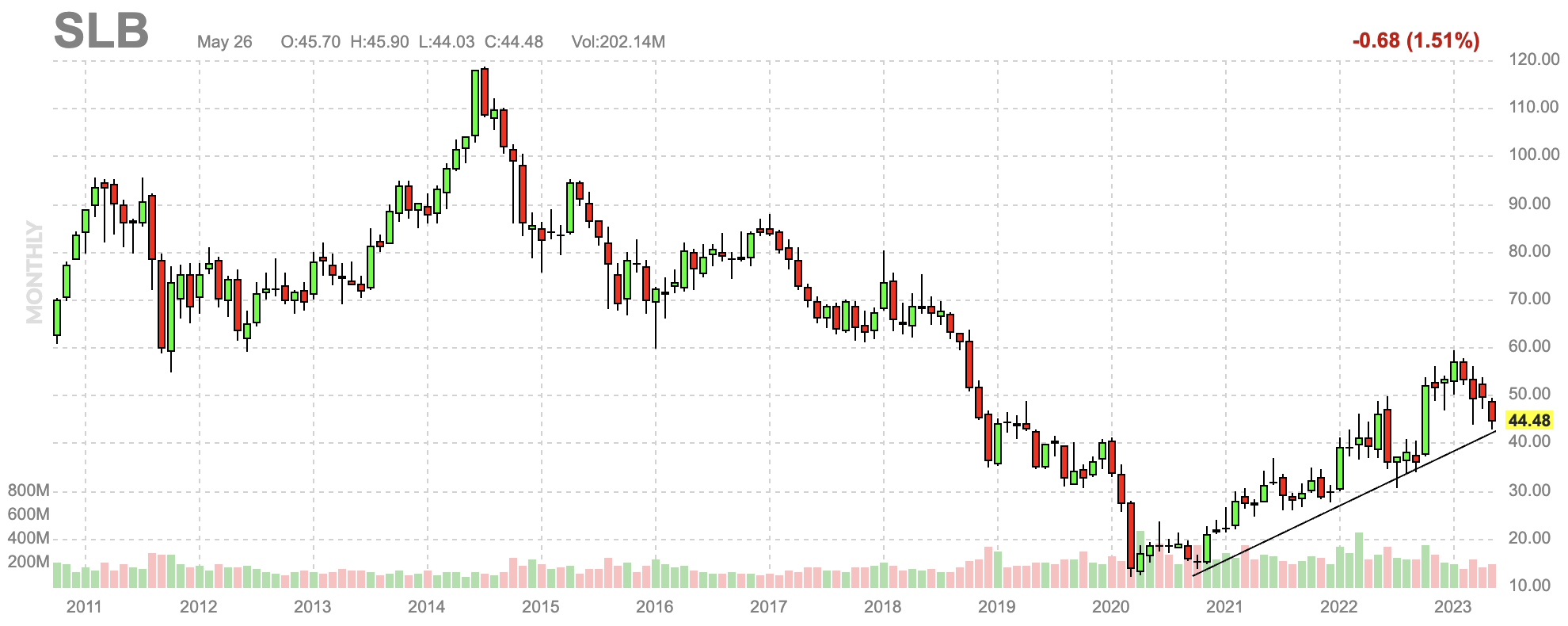

While SLB remains in a perfect uptrend, there's a risk the stock breaks down due to cyclical headwinds, which are the biggest risk to the long-term thesis - at least temporarily.

FINVIZ

Investors looking to buy equipment might enjoy buying SLB below $40. However, there's a high likelihood that investors get the chance to average down. We're not yet in a situation where oil is in an easy uptrend. I expect that to happen the moment economic growth expectations bottom.

At that point, we'll likely see a massive surge in oil equities.

Takeaway

SLB is a global energy equipment and service provider that recognizes the importance of fossil fuels in meeting current energy needs. While supporting clean energy, SLB understands that the energy transition cannot be forced without negative consequences.

Hence, the company aims to strike a balance between energy affordability, security, and sustainability, driving innovation and decarbonization in the oil and gas industry while advancing clean energy solutions.

SLB has shown strong performance, generating impressive revenue growth and beating estimates. With a focus on digital solutions and strong international growth, the company is well-positioned for future success.

It anticipates durable revenue growth in key markets such as the Middle East and offshore basins, as well as opportunities in the deepwater subsea sector.

SLB is trading at an attractive valuation. While there may be cyclical headwinds in the short term, long-term prospects for oil equities are promising.

Investors interested in equipment providers may consider buying SLB shares below $40, with the possibility of averaging down in the future.

For further details see:

Schlumberger Is A Buy As Net Zero May Be Failing