SLB - Schlumberger Limited: A Bet On Carbon Capture Capabilities

2023-05-30 05:18:52 ET

Summary

- Schlumberger Limited is well-positioned to capitalize on the growing carbon capture market, with strategic partnerships and a strong presence in the industry.

- The company's well construction division is driving revenue growth, while its digital and integration segment holds potential for future expansion.

- Despite concerns over high debt levels, Schlumberger's financials remain relatively stable, and the company offers a solid dividend yield of 2.25%.

Editor's note: Seeking Alpha is proud to welcome Wealth Analytics as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Schlumberger Limited (SLB) is an exciting opportunity to gain exposure to the growing market of carbon capture. The company is making plenty of moves to establish itself as the company regarding these CCUS projects. The balance sheet is decent and fears of high debt should go away as the company gets back on track with their cash flows once again. Being a part of the incentives to boost our dependence on renewables and decrease emissions is something I think most investors should look towards. With a solid company like SLB they offer that opportunity and is therefore a buy for me.

Investment Rundown

Schlumberger Limited operates in the oil and gas industry. Leveraging its deep expertise and cutting-edge technology, Schlumberger provides a diverse array of innovative solutions and services to cater to its client's needs.

End Markets (Investor Presentation)

{kind=link}

SLB has made the right moves to grow its revenues efficiently and is diverting efforts to capture the carbon opportunity. Partnering up with a major company like Linde plc ( LIN ) will translate into a tailwind for the company. The trend points to more off-shore activity and that creates an opportunity for SLB to grow revenues further, which they have done so far, noting a 30% YoY top-line growth in the last report . Investors are able to gather a lot of value from starting a position here, the dividend yield of 2.25% paired with a solid earnings growth outlook makes for an excellent investment case.

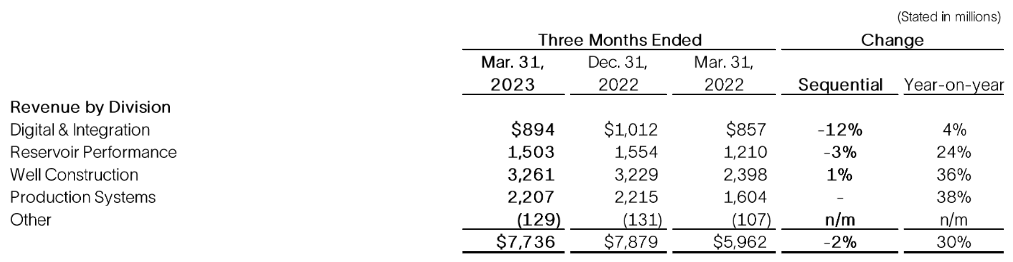

Company Segments

Looking at the company is made up of 4 different divisions with the well-construction one making up the largest portion of the revenues, nearing 50% of it. It's further reassuring to see this part of the company also growing almost the fastest, at 36% YoY.

Earnings Highlights (Q1 Report)

{kind=link}

The well construction division provides an extensive array of services, encompassing well planning, drilling fluids, drilling tools and technologies, wellbore placement, and well integrity solutions. Schlumberger leverages state-of-the-art drilling techniques, advanced drilling fluids, and cutting-edge drilling tools to assist clients in optimizing drilling performance, mitigating drilling risks, and safeguarding the integrity of the wellbore.

Company Market (Investor Presentation)

{kind=link}

Looking at the most profitable part of the company, however, there is some concern to be had. The digital & integration division saw a decline in the operating margins on a YoY basis, while all the other divisions saw an increase. The company is however showcasing that this part of the business will be able to play a vital role in some markets as they help streamline the process and I would also bet it's a rather scalable part of their business too. The CEO Olivier Le Peuch remained confident about the outlook however, "We continue to see positive pricing as our performance differentiates, technology adoption increases, contract terms are adjusted to offset inflation, and service capacity continues to tighten in key international markets". This makes me confident that SLB will be able to efficiently grow this part of the business as the trend is showcasing a higher demand for such solutions. This would also help bring up the overall margins of the company and grow operating cash flows even higher than the $330 million that was generated in the first quarter.

Markets They Are In

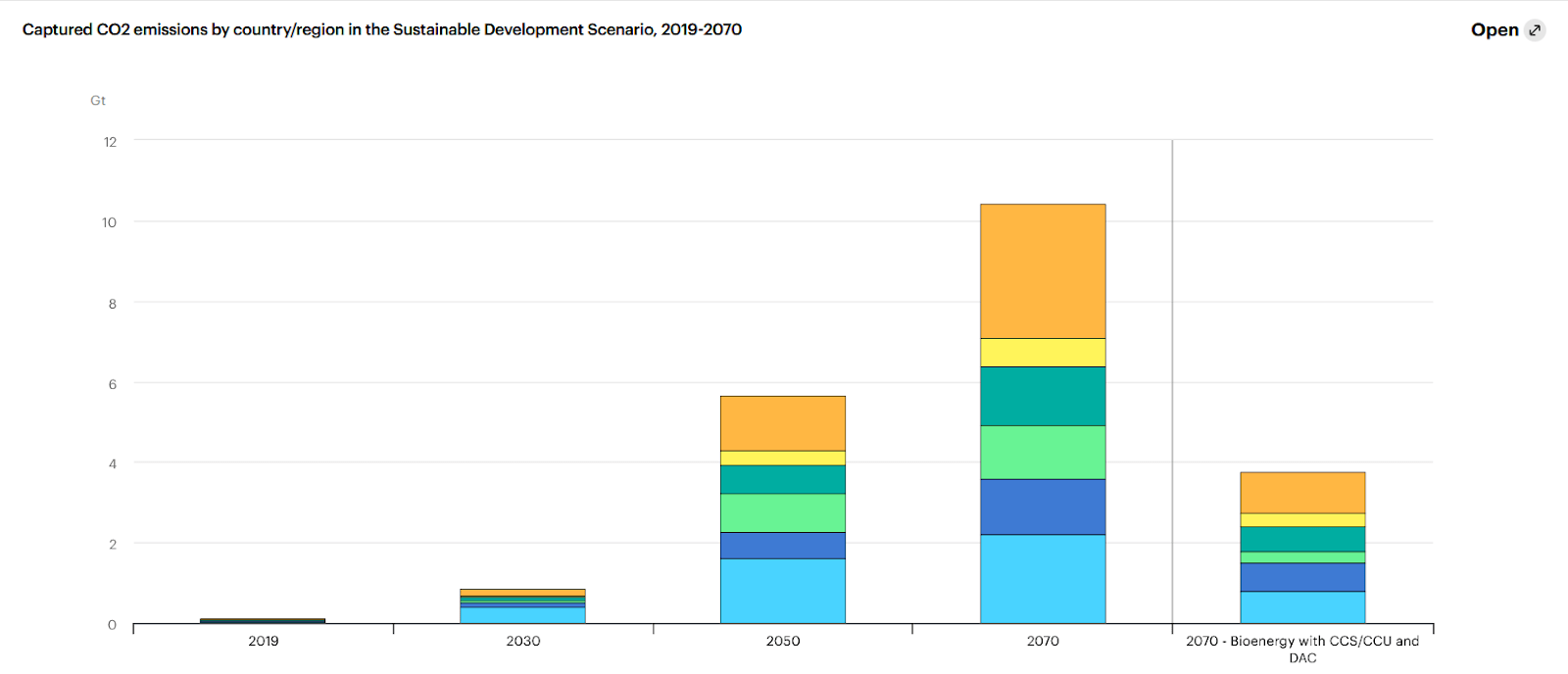

SLB acting as a solutions provider in the oil and gas industry is pushing more and more into the decarbonization part. With the partnership with Linde, they aim to make companies more interested in reducing their carbon footprint. With that said, the market for CCUS is estimated to grow rapidly over the coming years. In 2021 it was valued at under $2 billion, but by 2028 it will be over $10 billion according to a report by GlobeNewswire .

With the moves SLB is already making, they are essentially taking the driver's seat in this market and becoming a leader already. The biggest market for these CCUS projects is still in the US, where about 60% of the global carbon capturing is happening according to IEA . With new policy incentives and social pressure more and more companies are looking to reduce their carbon footprint and that of course creates demand for the services SLB provides.

{kind=link}

Looking at the big picture, we are only at the very start of this carbon capture market opportunity. By 2070 it will have grown immensely from where we are now. Being in a company that is already establishing itself as a market leader will be of great benefit in the long term in my view. In 2021 there were 100 new projects announced regarding CCUS, and SLB has so far been able to be a part of 100 different projects themselves. Going forward it will be key to watch the development of the New Energy segment of the company. Regarding the partnerships, it seems the growth here will be seen in the Digital segment of the business. So far being the most profitable part of the business, but not yet the fastest growing. The coming years and the seeming resurgence of CCUS projects should hopefully put more growth here in my view. Other than that, the remaining divisions in the company are likely to continue experiencing demand as the oil services market is expected to see a 6.6% CAGR from now until 2027.

Financials

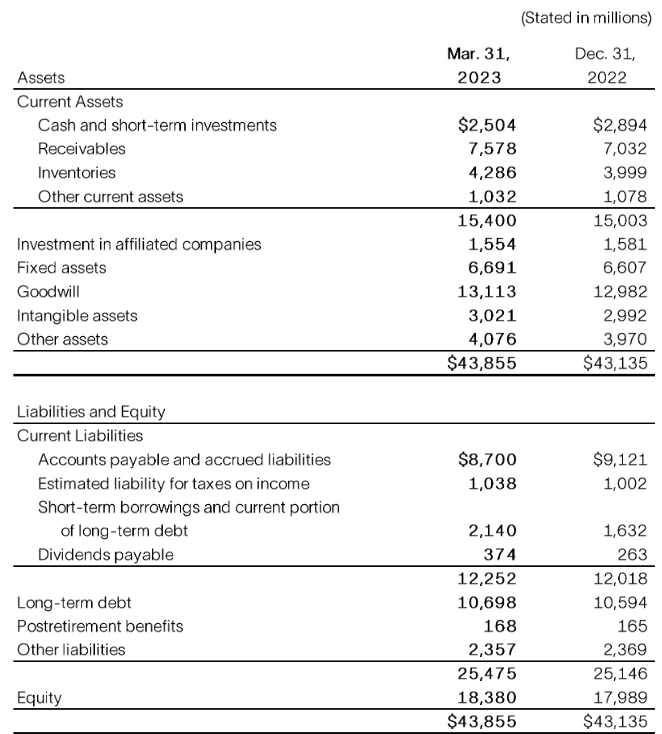

Looking at the financials of the company they seem to be in a relatively strong position still. The cash flows have seen a drastic decline over the last few years but remain positive at least. Going from close to $3 billion in 2019 to under $300 million in 2022. The company still has enough cash at hand to pay down all the short-term borrowings and the current portion of the long-term debts at least. But it would leave them with just $400 million left, however.

Company Balance Sheet (Q1 Earnings Report)

{kind=link}

Looking ahead however the cash flow for the company is expected to continue to rise as the first quarter is usually a buildup to the coming quarters according to the company. This will of course be a vital point to look at in the coming reports. If there isn't the development we'd like to see, then the current valuation could in my opinion be too rich and call for a compression.

The net debt/EBITDA ratio for the company is however sitting at around 1.67 right now which isn't alarmingly high. Going forward though I don't want to see a higher debt level for the company. Over $10 billion is already quite high, especially when the cash flows are nowhere near what they used to be. Until there is development there I can't see a positive effect of increasing debt, other than just causing concerns for investors.

Industry Comparison

Company Comparisons (Author's calculation)

Looking at the chart above I don't think SLB comes off as the clear choice. Both Halliburton Company ( HAL ) and Baker Hughes Company ( BKR ) will very likely gain from similar trends that SLB is experiencing. Growth in the oil service market is estimated to be decent at a 6.6% CAGR until 2027 as mentioned before. That should be visible in all these companies' top lines in my opinion given the market share each of them hold. With SLB however I see them offer a better and broader exposure to the CCUS projects and the potential market for them. With that said, they already have a solid EBITDA margin compared to the other and I still see them having plenty of upside growing this. SLB also seems to be the one company here who can sustain the growth the longest. Paying a 14x forward earnings premium for a company like SLB which has gather the largest market share and is set up the best to deal with these CCUS projects is fair to me. If the P/E would be around the 10x mark, then I would find SLB incredibly undervalued, but a 14x still makes it a buy in my view. Especially with the estimated EPS growth of 37% YoY. With close to the best dividend yield for SLB out of these the bonuses add up.

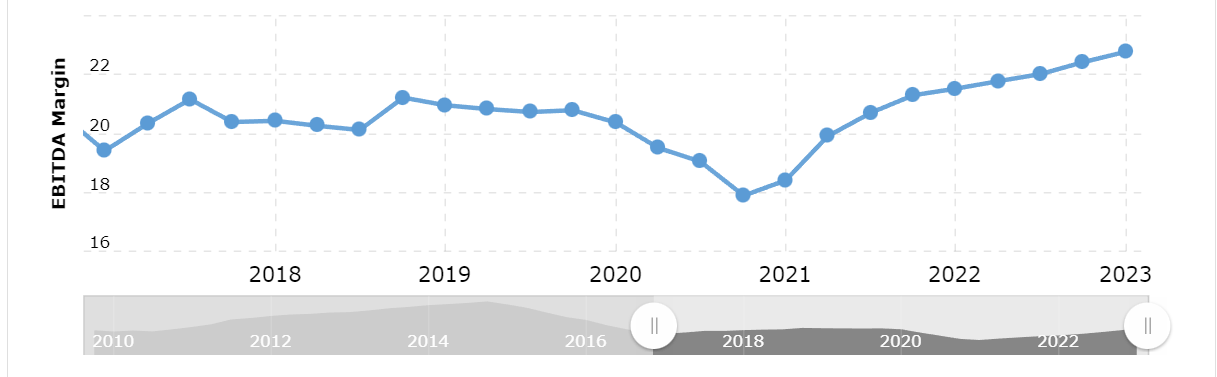

SLB EBITDA Margin (Macrotrends)

{kind=link}

Where perhaps SLB comes ahead is the so far strategic and vital partnerships they are establishing, but also the strength they are showcasing in growing out their margins. As seen above, the moves the company has made from 2021 and onwards are paying off. Most notably as well is the lack of margin drops that happened to companies in the oil and gas industry as a result of lower commodity prices. The resilience of SLB and their business model is clearly shown here. All the companies mentioned before are likely going to gain from the increase in CCUS but as we are so short into the market it's hard to see which ones will be the winners and dominate it. For a diversified portfolio, all of these companies could be included. But on an individual level for SLB, I am rating them a buy, but there are positives about the other ones that SLB doesn't have. The lower valuation and stability of a company like HAL makes sense for someone who wishes to not have as much volatility. BKR seems more like the growth option of the three, with estimates suggesting they will double their EPS by 2027, from 2023 levels. With that said though, where SLB is setting themselves apart is the market share and the long history of being involved in these CCUS projects. They have built up a strong reputation with them, something I don't see the other companies matching right now.

Risks

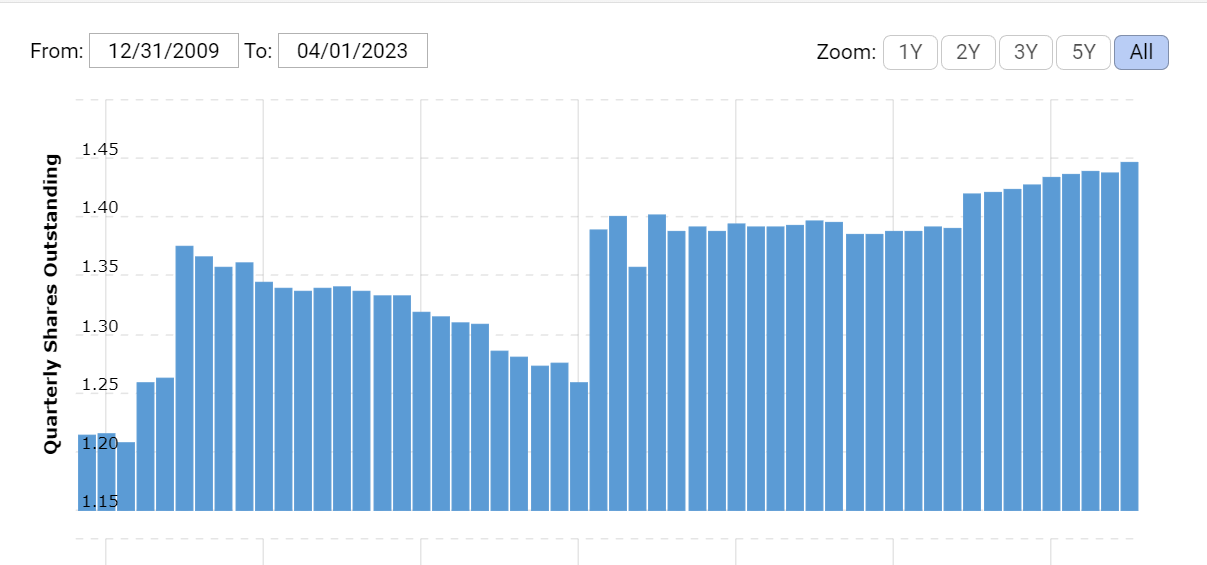

Perhaps the most concerning risk I see with SLB right now is the negative history of diluting shares. Increasing nearly 4% in the last 5 years is not a major cause for concern, but as the CCUS projects develop, they could turn out to not be as profitable as once thought to scale. That could hurt the margins for SLB and cause for an increase of the dilution rate.

Shares Outstanding (Macrotrends)

{kind=link}

Besides that, the company holds around $1.5 billion in cash which is not enough to pay off at least 30% of the long-term debts. That is a factor I like to look at. If the company is taking on more debt, and at a faster rate than they are building up cash that can make the buy case here turn into a sell case instead. I want to gain exposure to these trends and markets, but not at the cost of being invested in an overleveraged company. Right now however, I do not see enough concerns that would warrant a sell for SLB.

Final Words

I think that SLB is an interesting company to do research about right now. They are at the brink of the beginning of a major market opportunity like carbon capture. Some suggest we need to have 120x higher capabilities of capturing carbon if we want to meet our climate goals. Where SLB comes in the picture is as a service provider that partners up with companies to help them lower their emissions. The company is outside of this however growing revenues at a steady and strong rate YoY as the trend for off-shore is increasing, which is currently boosting revenues in the well construction division. With a higher P/E than the sector, I still see the potential of an investment into SLB given the market position they are taking in the CCUS projects and the decent dividend they have established so far.

For further details see:

Schlumberger Limited: A Bet On Carbon Capture Capabilities