SLB - Schlumberger: Rising Oil Prices Robust Growth And AI Coming Together

2023-09-29 12:05:28 ET

Summary

- Oil prices had a strong Q3, benefiting oilfield services companies like Schlumberger.

- Schlumberger is the world's largest provider of services and equipment for the energy industry.

- The company's digital business and AI presence are expected to drive higher margins and revenue growth.

- I outline key price levels to watch ahead of earnings in just a few weeks.

Oil prices had a tremendous Q3. The spot price of WTI was stuck in the mid-$60s back in July, but rapid changes across asset classes led investors to sell bonds and buy energy commodities. For oil specifically, limited supply and still-strong global demand resulted in both WTI and Brent notching 2023 highs, in the mid-$90s , by late September. Not surprisingly, oilfield services companies are among the beneficiaries.

I have a buy rating on Schlumberger Limited (SLB) given its growing free cash flow, offshore business momentum, rising oil prices, and AI presence. The chart is also encouraging.

Falling US Oil Supply Drives Up Prices Around the World

{kind=link}

According to Bank of America Global Research, SLB is the world's largest provider of services and equipment used in the drilling, evaluation, completion, production, and maintenance of oil and natural gas wells. It engages in the provision of technology for the energy industry worldwide. The company operates through four divisions: Digital & Integration, Reservoir Performance, Well Construction, and Production Systems.

The Houston-based $87 billion market cap Oil and Gas Equipment and Services industry company within the Energy sector trades at a near-market 22.3 trailing 12-month GAAP price-to-earnings ratio and pays a moderate 1.6% dividend yield. Ahead of earnings due out in just a few weeks, shares trade with a somewhat high 34% implied volatility percentage, and short interest is low at 1.5%.

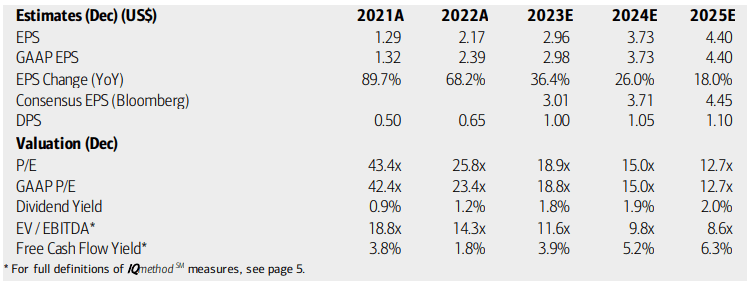

Back in July, SLB reported a modest earnings beat . $0.72 of operating EPS topped analysts' expectations by a penny, but revenue, up 20% from year-ago levels, came in light at $8.1 billion - a $110 million miss. Sequential EBITDA grew 10% and the $1.96 billion figure was 28% higher than the same quarter in 2022. Overall, Schlumberger's international and offshore segments continued to perform well, and the management team reaffirmed its earnings outlook. 2023 free cash flow could reach $3 billion, with $2 billion being returned to shareholders in the form of dividends and stock buybacks.

What's exciting about SLB is that its digital business could continue to drive margins higher - cloud computing, data analytics, and AI are all competitive advantages for the firm, and the management team expects Digital revenue to top $3 billion by 2025. And just recently, analysts at Morgan Stanley listed SLB as an energy firm that was actually specific when mentioning AI on its call (whereas many firms just said it in passing).

On valuation , analysts at BofA see earnings jumping 36% this year with continued strong EPS growth in the out year. By 2025, analysts expect operating per-share profits near the $4.50 mark, putting the hypothetical P/E ratio in the mid-teens should the stock price hover here. Dividends, meanwhile, are expected to rise at a steady clip, but the yield is much lower compared with many other Energy sector firms.

Still, free cash flow is robust and expected to rise. Considering that oil prices are much higher today compared with when the firm last reported earnings, I expect further positive EPS revisions and better FCF outlooks.

Schlumberger: Earnings, Valuation, Dividend, Free Cash Flow Outlooks

{kind=link}

SLB is not the cheapest Energy sector company you will come across, though. Its forward operating P/E is above both the industry average and even the S&P 500's. Still, if we assume 2025 EPS of $4.35 and apply a 20 multiple, then we are talking about an $87 stock looking to the end of next year.

But let's also consider the PEG ratio - normalized growth of 20% is unusual, and if we simply go with the sector median 1.9 PEG, then the P/E should be well above 30. Thus, I make the case that a high valuation is deserved given the 20%-plus bottom-line growth rate expectation.

SLB: More Expensive Than Its Industry, But High Growth

Seeking Alpha

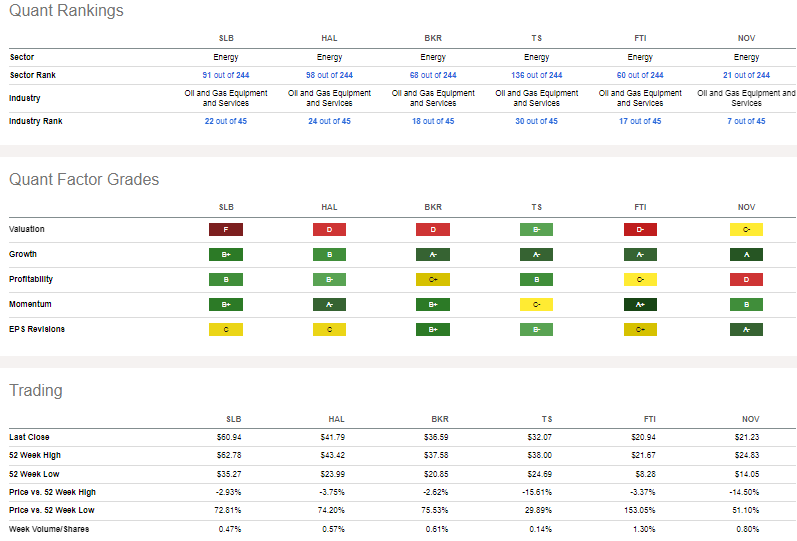

Compared to its peers , SLB features a high earnings multiple, but also a strong growth rating, Profitability is just about the best in its class while stock price momentum is solid. Given the mixed quarter reported in July, EPS revisions have been soft, but if the company can beat the street in a few weeks then I would expect much more sanguine profit outlooks given the recent rapid rise in domestic and international oil prices.

Competitor Analysis

{kind=link}

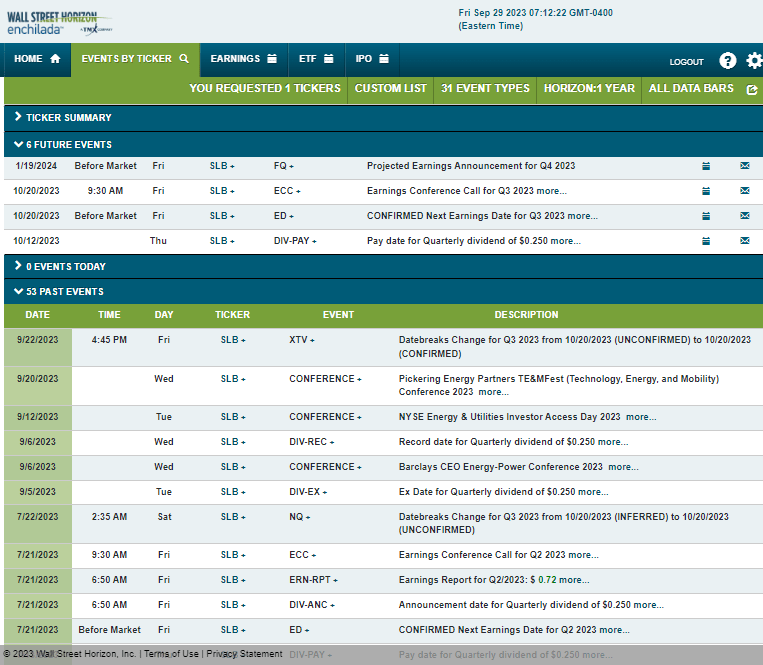

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q3 2023 earnings date of Friday, October 20 with a conference call immediately after the results hit the tape. You can listen live here . No other volatility catalysts are expected in the near term.

Corporate Event Risk Calendar

{kind=link}

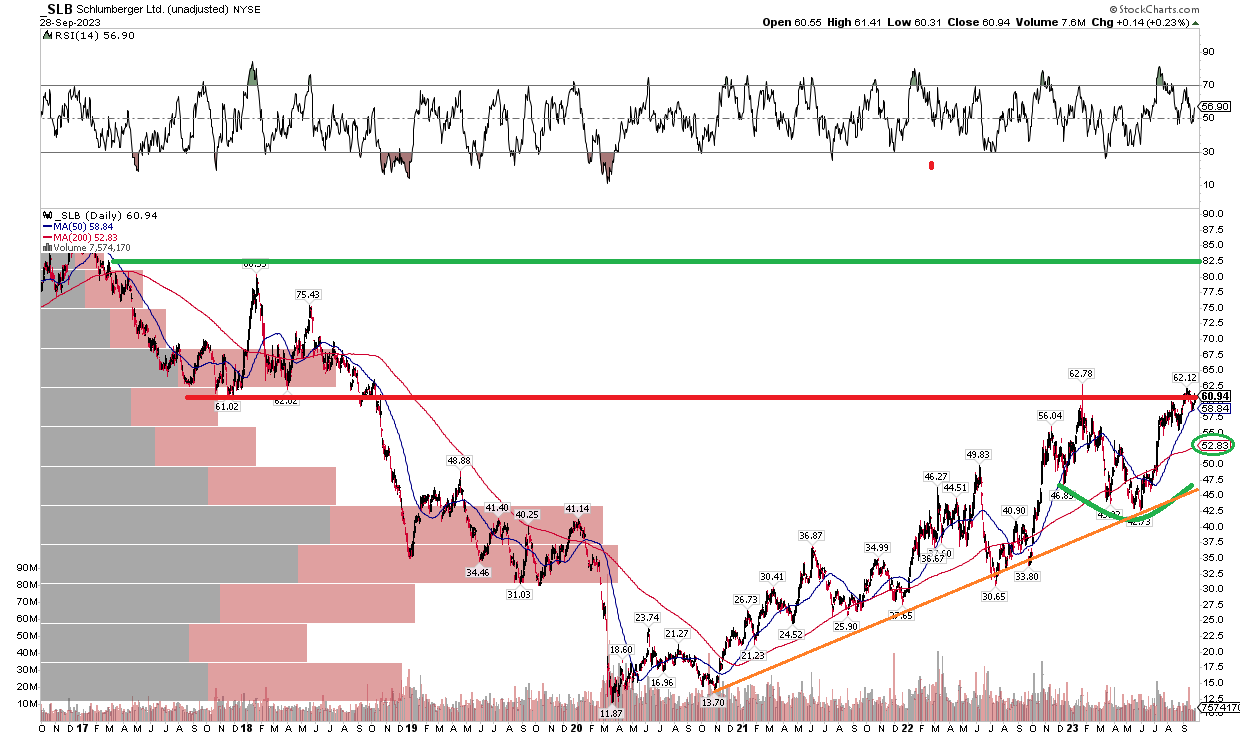

The Technical Take

Schlumberger's stock ran into resistance in the low $60s earlier this year and is once again pausing at this battleground between the bulls and the bears. Notice in the chart below that SLB is probing resistance, and it's natural for the stock to take a breather here. Bullish, though, is that this is the third try at rallying through that line which had been supported throughout the 2010s. A jump above the low $60s would portend a bullish measured move price objective to the upper $70s based on the height of a potential cup and handle, or rounded bottom, a pattern that has been ongoing for all of 2023.

Also, take a look at the long-term 200-day moving average. The trend indicator is positively sloped, asserting that the bulls are in control. Moreover, an uptrend support line off the November 2020 low (a successful retest of the March 2020 nadir), looks robust in my view. I see near-term support in the $54 to $55 zone - the July and August lows. Buying here with a stop under that range appears like a wise play ahead of earnings while long-term support is seen in a high volume by price area of $30 to $40.

Ultimately, I'd have eyes on the $80 spot for an upside target.

SLB: Shares Again Testing Resistance, Eyeing an $80 Target

{kind=link}

The Bottom Line

I am initiating buy coverage on Schlumberger for its positive growth prospects, unique industry presence, solid cash flow, and robust technicals.

For further details see:

Schlumberger: Rising Oil Prices, Robust Growth, And AI Coming Together