CA - Scotiabank: The 6.4% Yield Is A Gift For Dividend Investors

2023-09-14 08:30:00 ET

Summary

- Bank of Nova Scotia is a quality high-yielding pick for patient investors due to its strong track record and steady revenue growth.

- BNS has a sizable footprint in emerging growth Latin American countries, contributing to diversification.

- Recent financial performance has shown signs of improvement, with increased revenue and a strengthened balance sheet.

It’s been a while since I last visited Bank of Nova Scotia ( BNS ) with a Buy rating back in February of this year. Like most stocks in this year’s volatile market, BNS has seen its ups and downs, and has fallen by 3.2% since my last piece, but the total return was flat thanks to dividends paid along the way. As shown below, BNS currently trades at the low end of its 52-week range and in this article, I discuss why BNS remains a quality high-yielding pick for patient investors.

{kind=link}

Why BNS?

Scotiabank has been around for over a century and is the third largest Canadian bank by assets. Like its Canadian peers, BNS is known for having its conservative lending practices, and this served shareholders well during trying times, including the Great Financial Crisis, when many U.S. banks were forced to suspend their dividends. BNS, on the other hand, hasn't missed a dividend payment since 1833 .

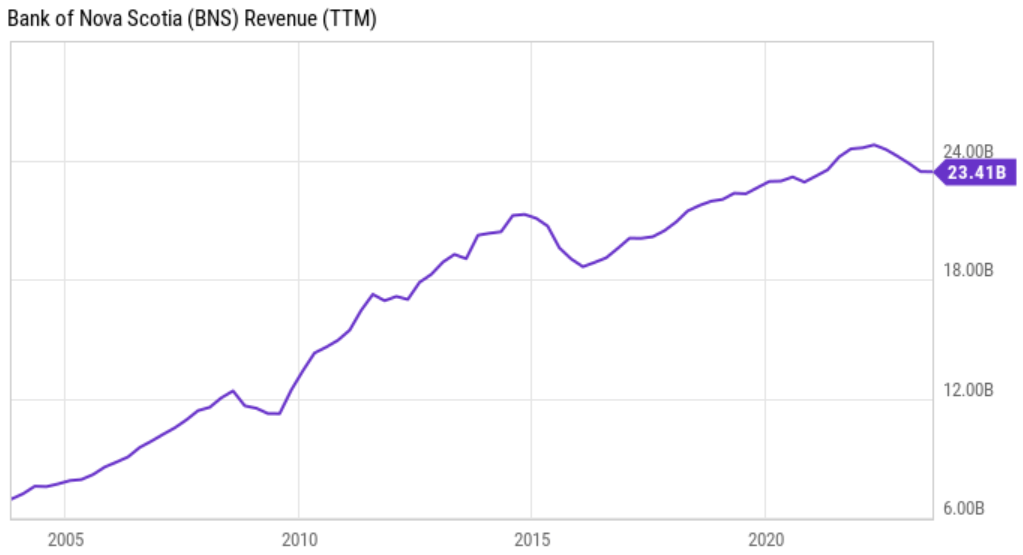

BNS is also the only Canadian bank to have a sizable footprint in emerging growth Latin American countries, where it gets nearly 40% of its total revenue. This combined with a strong presence in its home market has resulted in steady revenue growth over its history. As shown below, despite hiccups in 2008-2009 and 2016, BNS's revenue is up substantially over the past 20 years.

{kind=link}

Recent financial performance for BNS has been challenged by high inflation and interest rates, which has raised cost of funding and general economic uncertainty. However, it appears that BNS is climbing out of its trough. This is reflected by fiscal Q3 results, in which revenue is up 2% QoQ and 4% YoY. While diluted EPS was down by 18% YoY, it's showing signs of improvement as it was up by 2% QoQ, due to moderating expense growth (flat on a QoQ basis).

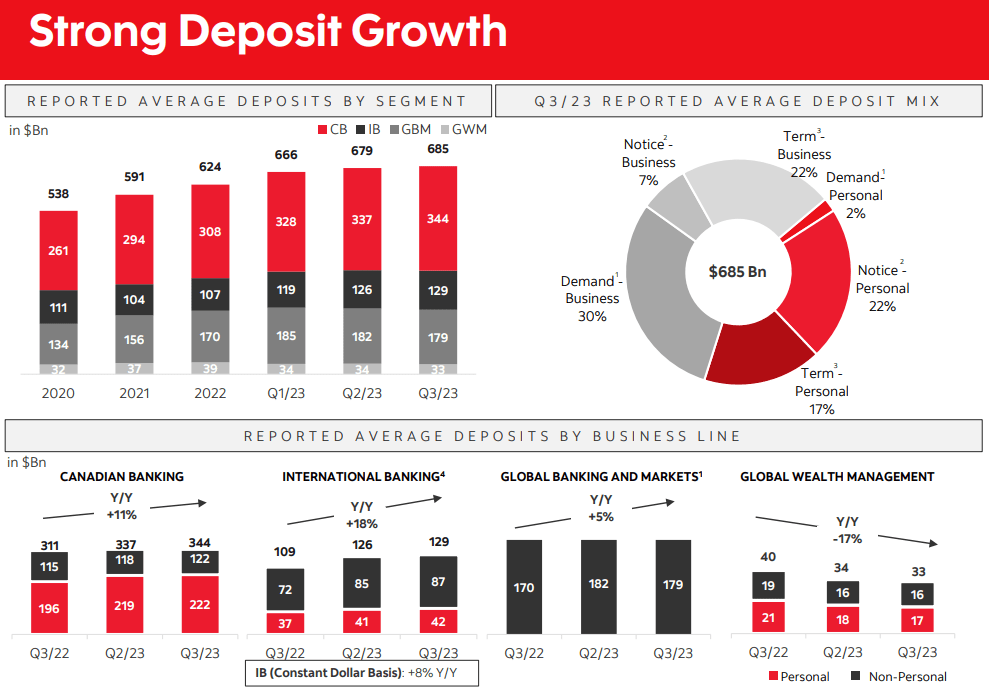

As shown below, BNS continues to attract a growing and diversified deposit base across geographies and customer segments, with total deposits landing at CAD $685 billion in the last reported quarter.

{kind=link}

BNS has also taken steps to strengthen its balance sheet, with its Tier 1 Capital ratio improving to 12.7% at the end of Q3. This is a notable 220 basis points higher than the 11.5% from when I last visited the stock in February, and it sits well above the 6% minimum requirement by Canadian banking regulators. Moreover, BNS continues to carry an A+ credit rating from S&P and has a high liquidity coverage ratio of 133%, up from 122% in the prior year period.

Concerns around BNS stem from moderating loan growth in its home market, as consumers are more cautious in the current environment and management noted that it's being more selective and deliberate in its approach towards new originations. With potential for a recession due to high interest rates, BNS may be subject to a higher loss rate. This is reflected by management raising the provision for credit losses, which negatively impacted earnings last quarter.

Nonetheless, BNS's international exposure may help to stem potential losses in any one market, as reflected by recent double-digit profit growth in the teens in Mexico, Caribbean, and Central America. BNS also remains a fundamentally efficient bank through contributions from digital assets such as Tangerine and from the higher margin wealth management business. This is reflected by BNS's Net Income Margin of 28%, sitting above the 26% financial sector median.

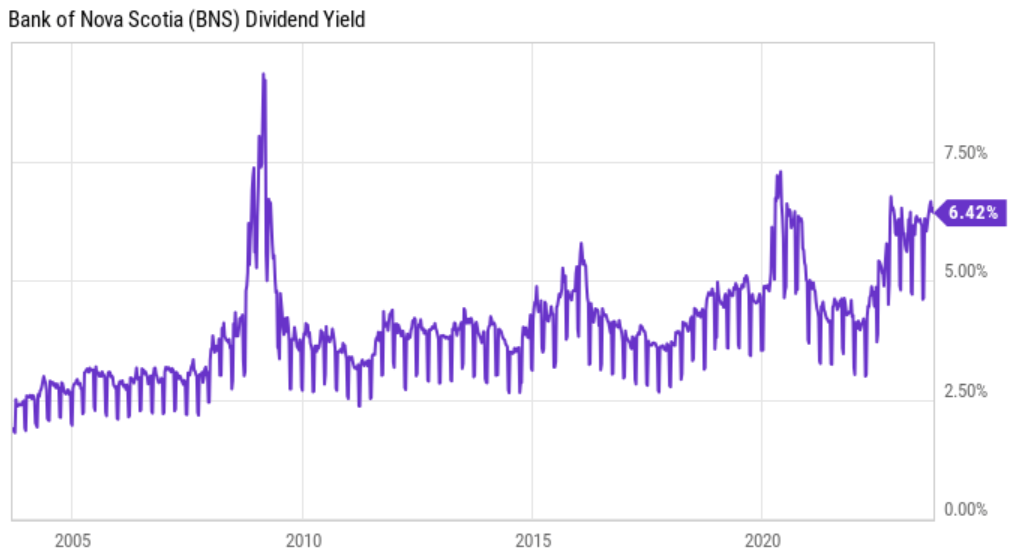

Meanwhile, BNS currently sports an appealing 6.4% dividend yield that's well-covered by a 58% payout ratio. As shown below, the yield currently sits at the high end of BNS's range over the past 20 years.

{kind=link}

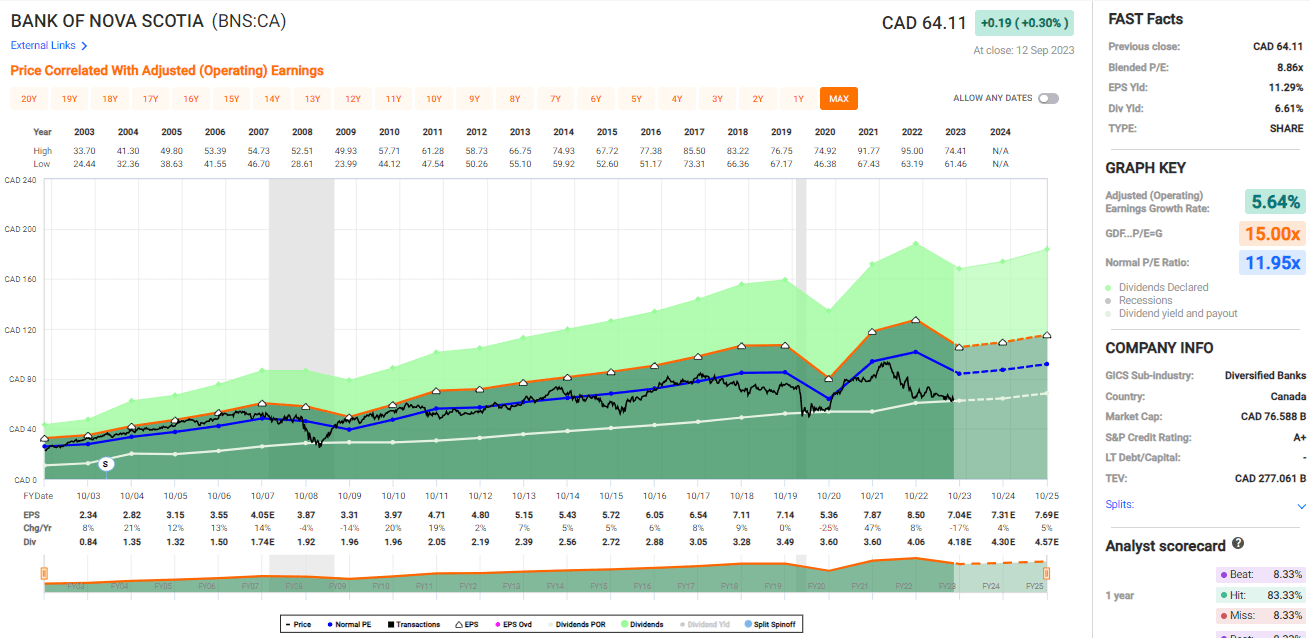

Lastly, I continue to find BNS appealing at the current price of $47.83 with a forward PE of 9.2, sitting well below its normal PE of 11.95, as shown below. The current valuation already bakes in the full-year 18% EPS decline this year, and analysts expect a resumption to growth over the next 2 years, with EPS estimated to growth annually between 5% and 11%.

{kind=link}

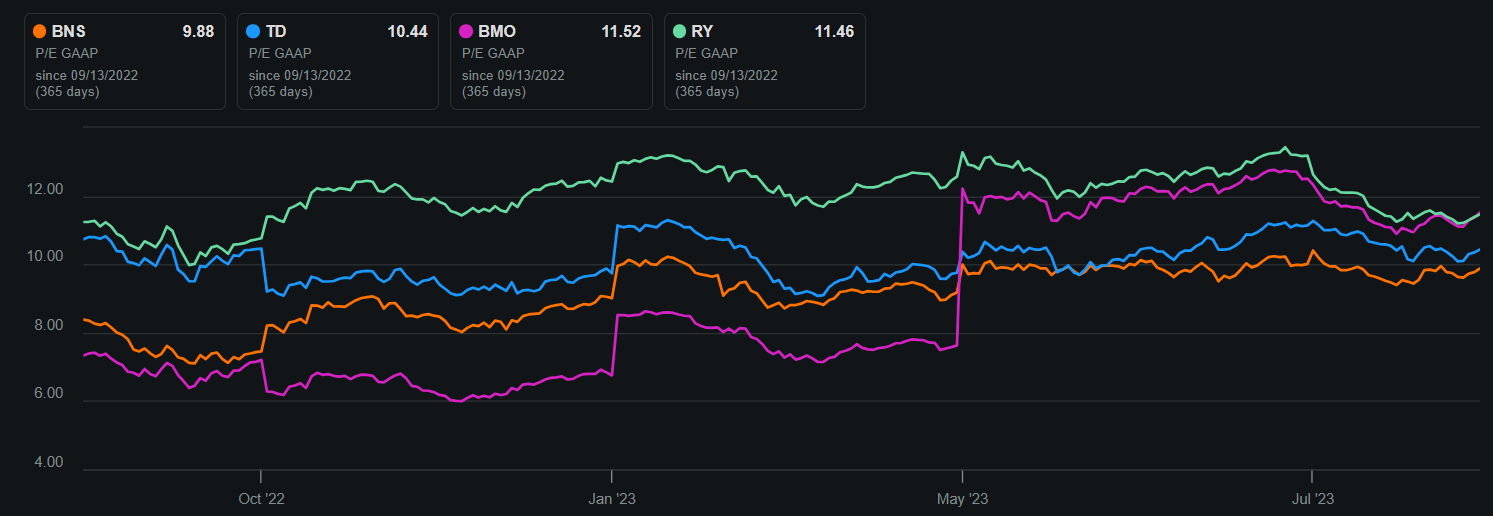

BNS also appears to be undervalued compared to its large peers, with a TTM PE of 9.9, compared to 10-12% for Toronto-Dominion Bank ( TD ), Bank of Montreal ( BMO ), and Royal Bank of Canada ( RY ), as shown below.

{kind=link}

Investor Takeaway

In conclusion, Bank of Nova Scotia stock remains a solid pick for those seeking yield from a quality Canadian banking giant. Its diversified presence across geographies has always been a plus, and is likely to help in mitigating potential losses due to economic headwinds in any one area. With an attractive dividend yield of 6.4% and trading at a forward PE of 9.2, BNS is an appealing pick for patient investors who are willing to pick up the stock during the down cycle before the economic picture improves.

For further details see:

Scotiabank: The 6.4% Yield Is A Gift For Dividend Investors