SE - Sea: I'm Buying While The Stock Keeps Falling

2023-11-21 06:30:12 ET

Summary

- Sea's stock has fallen by nearly 30% due to a slowdown in its gaming division, but the company's future in e-commerce and digital payments remains promising.

- The company's softer gaming revenue is offset by higher margins in the e-commerce division and cost discipline measures.

- Live streaming has helped the company to drive e-commerce bookings growth and secure market share gains.

- The company is also noting outsized performance in Brazil, demonstrating that Sea has a future beyond Asia.

A fresh bull market is well underway, with investors shrugging off the threat of inflation and cheering the end of rate hikes. Growth stocks are hot again, with very few exceptions - and among them is Sea (SE), the self-dubbed "Amazon of Southeast Asia."

This one-time market darling has seen its share price crater by nearly 30% this year, owing to one thing: a slowdown in its gaming division, which has been its cash cow for years as the company was ramping its e-commerce and digital financial services segments.

I last covered Sea in July , when the stock was trading closer to $55 per share. Since then, the stock has fallen by a fresh ~30%, driven by a poorly received third-quarter earnings print. And while I'm certainly not cheering the company's third-quarter results and the hole in my portfolio has been painful to bear, I'm renewing my bullish call on Sea and using the dip as a buying opportunity.

The headline reason here: I've always viewed gaming as more of a stopgap for Sea. It was important in the company's early days, yes - especially with how much cash Free Fire , the company's biggest hit, brought in during the pandemic when everybody was home and playing games. But Sea investors have all looked to the future for Sea's opportunity in e-commerce and digital payments when the company would become not just the Amazon of Southeast Asia, but its PayPal (PYPL) / Square (SQ) as well. And to me, that future is very much alive.

The other core reason I remain bullish on this name, despite the disappointing gaming results: the company's softer gaming revenue and profits are offset by higher margins in the e-commerce division, long a loss leader for the company, as well as corporate-level layoffs that have actually helped Sea increase its EBITDA performance during a difficult time.

Beyond the near-term drivers, here is a reminder of what I view to be the long-term bull case for Sea:

- Sea operates in the attractive "tiger economies" with secular multi-year growth tailwinds. Serving the fast-growing economies of Southeast Asia (Singapore, Indonesia, Philippines, Malaysia, etc.). Outside of its home country of Singapore, Sea benefits from rapidly modernizing infrastructure and a burgeoning middle class. It's not ludicrous to compare an investment in Sea to an early bet on Alibaba (BABA) and JD.com (JD) in China.

- Sea operates a conglomeration of attractive, profitable businesses. The company's gaming, e-commerce, and digital payments businesses serve a wide net of customers and are now each profitable in their own right - giving the company plenty of growth catalysts to capture more share in Southeast Asia. These subsidiaries, particularly the more nascent payments business, enjoy synergies and cross-sell opportunities with each other.

- Cost discipline. Unlike many other hyper-growth companies when backed into a corner, Sea has shown expense discipline this year in laying off ~10% of its headcount amid its gaming division slowdown.

- Incredibly well capitalized. Sea has more than $8 billion of cash and investments on its balance sheet (for sizing, that is approximately a year's worth of opex for the company) to continue investing in growth and potentially acquire new platforms.

The bottom line here: there's a lot to like about Sea in the long term, and with the stock under so much pressure this year, it's a good time to enter into this growth titan at an attractive price.

Q3 download

Like most do, we can start with the bad news in the gaming division first.

{kind=link}

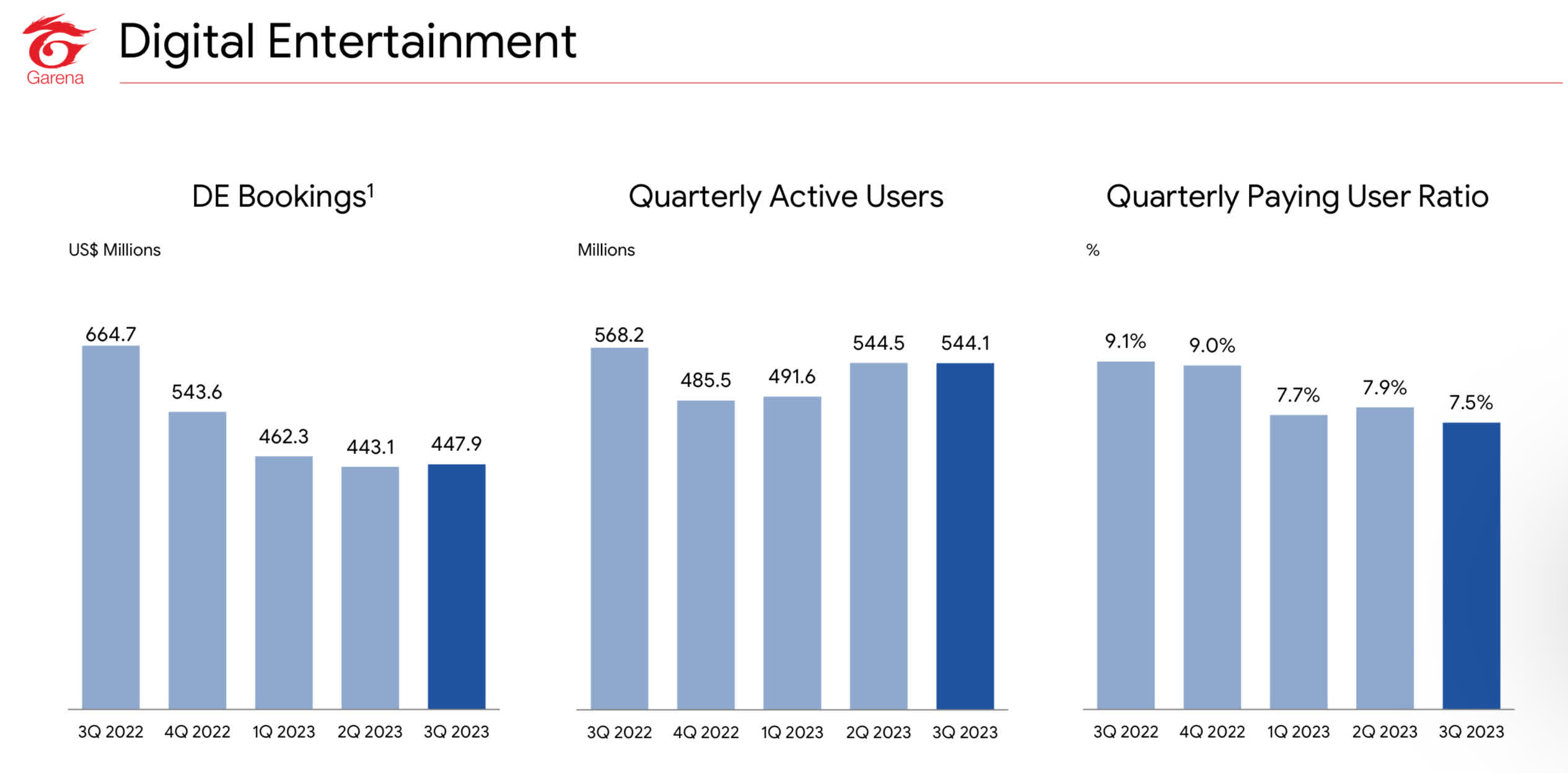

Quarterly active users saw a slight sequential dip to 544.1 million users, while the quarterly paid-user ratio fell sequentially as well to 7.5%. Total bookings in the division were slightly up versus Q2, but down -33% y/y to $447.9 million. Revenue for digital entertainment, similarly, was down -34% y/y to $592.2 million. As a reminder, for Sea, bookings in the gaming division represents when players purchased in-game items or subscriptions, whereas revenue represent the usage of those purchases.

Anecdotal commentary from the company's core gaming franchises pointed to stable user engagement (at least sequentially), with some pickup from non- Free Fire titles. Per Chief Corporate Officer Yanjung Wang's remarks on the Q3 earnings call:

We are happy to see that Free Fire maintains stable trends across both user and monetization metrics. Many of our initiatives around improving the user experience this year, such as reducing loading times, have shown continued success. We have also further deepened user engagement.

For example, we recently revamped Free Fire's guild system to enhance the social experience for our players. With all these efforts, we saw a higher revival of churned users and better user retention. Indeed, Free Fire was the most downloaded mobile game in the third quarter globally, according to Sensor Tower. We are also pleased to see healthy trends for our portfolio of published games. We added fresh, exciting content and enhanced the user experience for these games. New content on Arena of Valor received very positive user feedback, resulting in a new peak of quarterly active users for the game. Another of our published games, Call of Duty Mobile, achieved its highest quarterly bookings."

It's worth reminding ourselves that Free Fire was completely developed in-house. Sea has the technical know-how to develop hit games - and given time, it may produce another to reduce its reliance on its original golden goose.

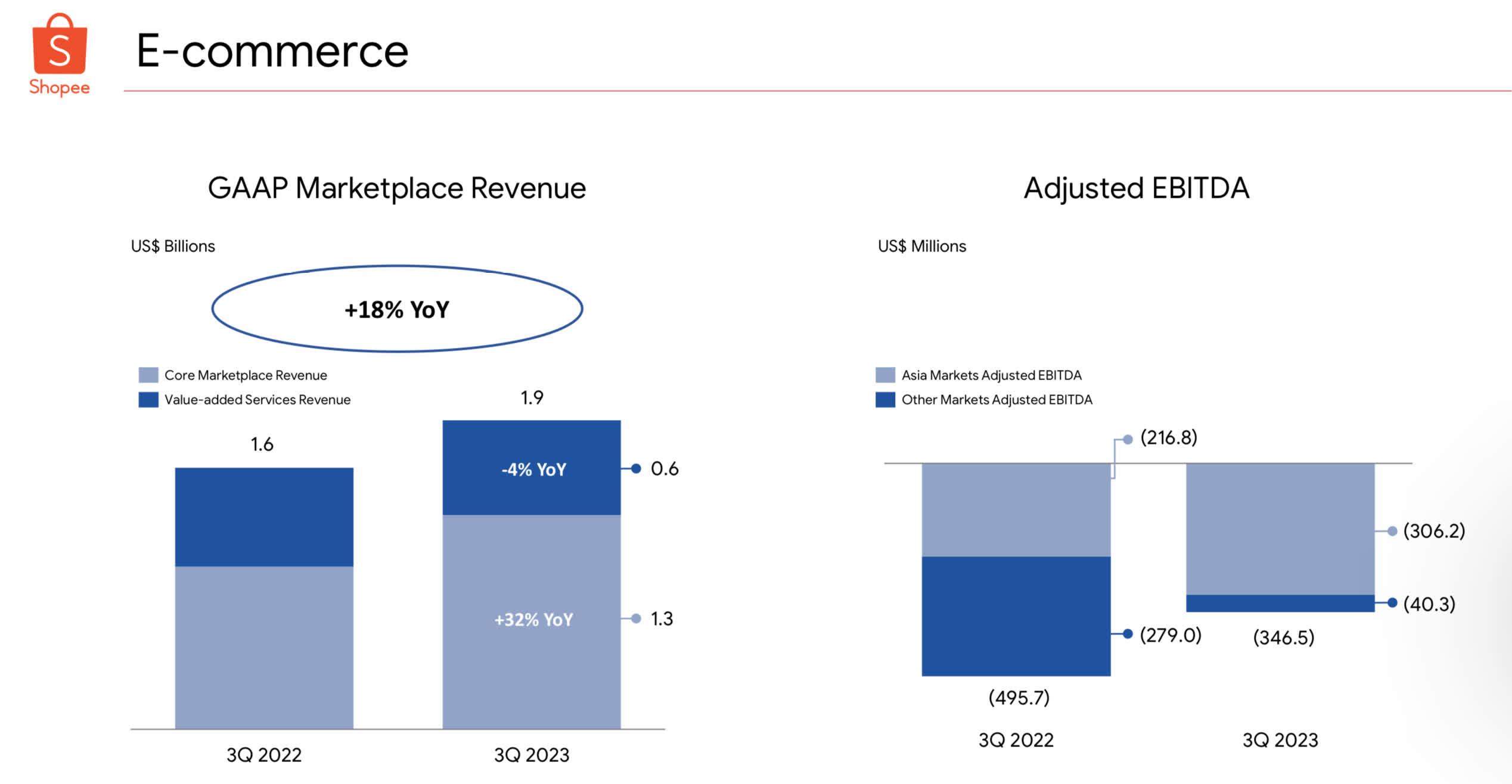

Results in the e-commerce division, meanwhile, were much more sanguine. Revenue grew 18% y/y, driven by a 5% y/y growth in GMV.

{kind=link}

The company believes that it gained market share in the quarter, and that share growth was driven in large part by the broad rollout of Shoppee Live - where product sellers do video demonstrations of their wares. Sea management noted that viewership hours on Shoppee Live in the month of October were triple that of June and that one in every five Shoppee users in Indonesia had used the feature.

Economies of scale have tremendously helped the e-commerce business scale, and the company notes that logistics costs per order are down -17% y/y. This has helped the company reduce its adjusted EBITDA losses to -$346.5 million, which is roughly one-third less than in the year-ago Q3. This was, in turn, driven by outperformance in Brazil - which gives us additional hope that Sea can be successful outside of Asia and in other hyper-growth economies as well.

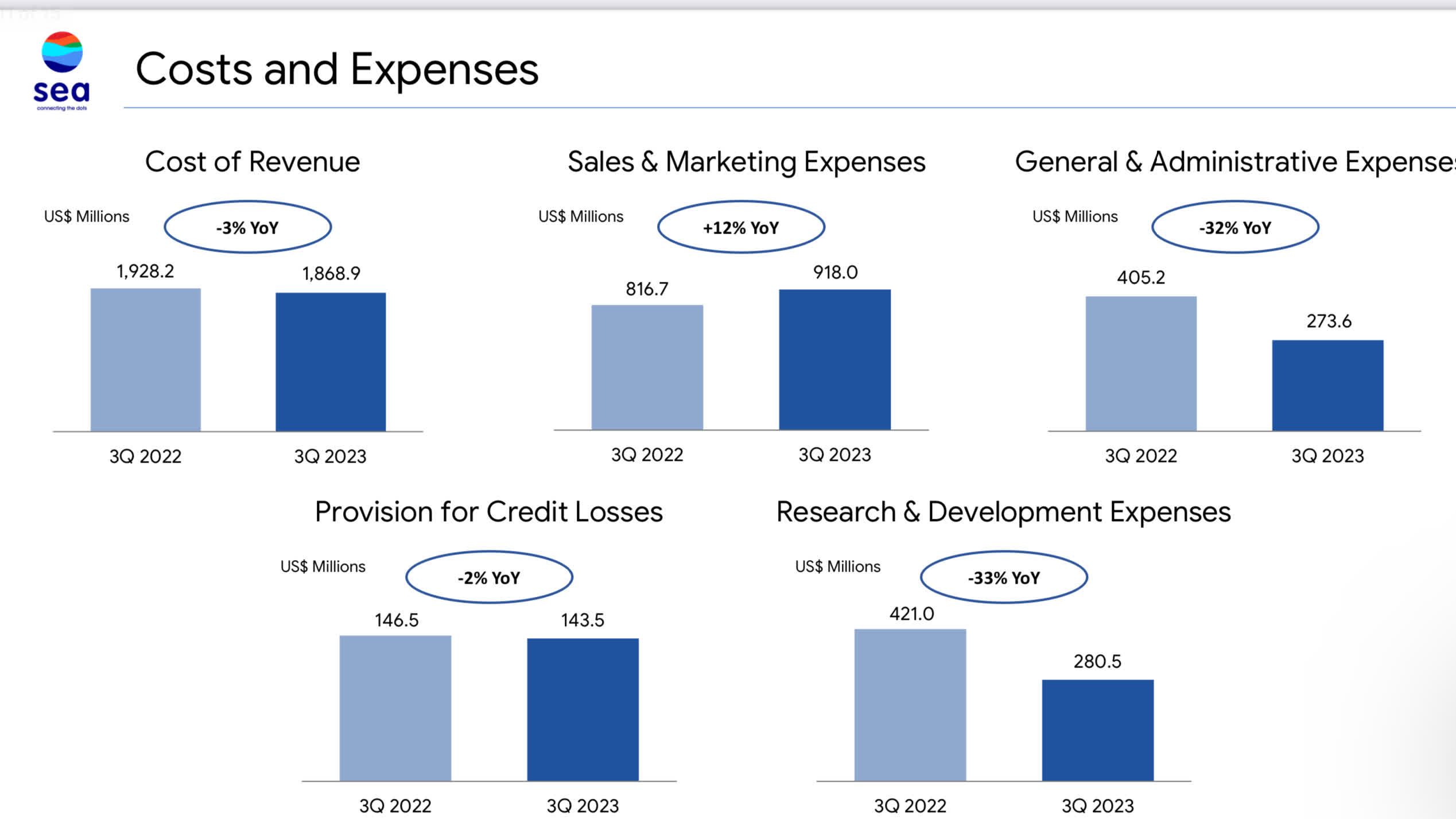

You can see as well in the chart below that Sea has made substantial cuts to general and administrative as well as R&D expenses, the result of layoffs that began in the tail end of 2022 that have shaved off ~10% of its headcount:

{kind=link}

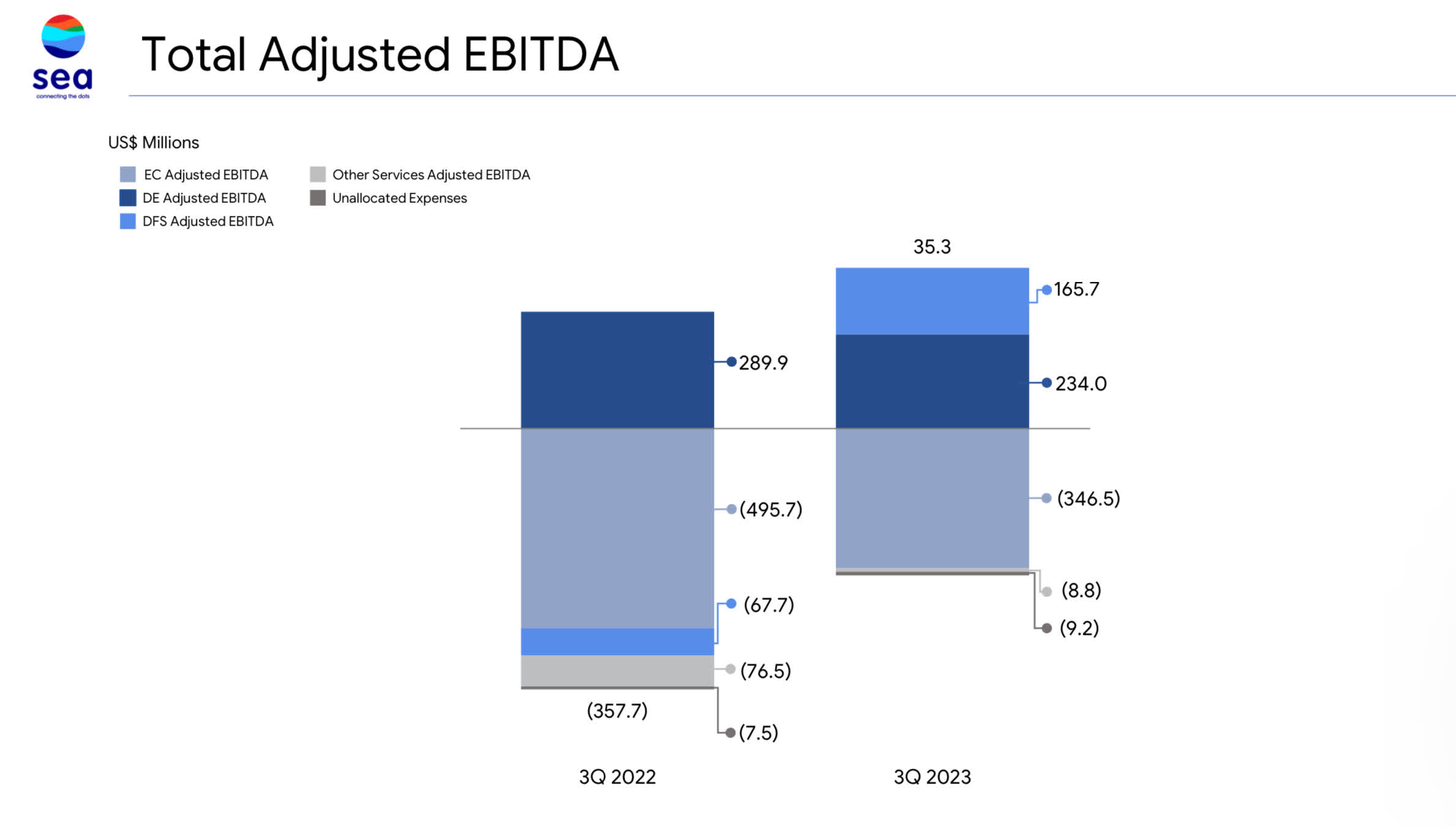

The combination of lower e-commerce losses and lower corporate overhead helped the company produce a positive adjusted EBITDA of $35.3 million, versus a -$357.7 million loss in the year-ago period:

{kind=link}

Key takeaways

In my view, I like the fact that Sea is finding ways to boost adjusted profitability even when its most profitable segment is faltering. While it's true that Sea has a lot to prove (reducing its reliance on Free Fire, improving e-commerce profitability in Asia, demonstrating growth in non-Asia markets), a lot of pessimism is baked into Sea's share price at sub-$40 and it's a great time to enter into this stock at a de-risked valuation.

For further details see:

Sea: I'm Buying While The Stock Keeps Falling