SE - Sea Limited Defending Its Turf

2023-12-01 23:12:43 ET

Summary

- Sea Limited's share price dropped by 20% after the release of its 3Q23 results, mainly due to concerns over Shopee's increased sales and marketing spending.

- Garena's user base declined slightly in 3Q23, but average revenue per user increased. Operating profit and margin improved.

- SeaMoney's revenue and margin continued to grow, but at a slower rate. The company disclosed its credit portfolio for the first time.

- I have my short-to-medium concerns, and will continue to stay on the sideline.

Investment Thesis

After Sea Limited’s (SE) 3Q23 results were revealed, the share price slipped by about 20%. The market was caught off guard by Shopee's escalated sales and marketing (“S&M”) expenses, going from 3 consecutive profitable quarters to losing money. Whereas for Garena, there was not much update aside from the modest decline in user base. SeaMoney, its most profitable segment, continues to outperform with growth in revenues, earnings, and margin expansion. Overall, the results were acceptable, and the dip in share price was rightfully so.

While we have witnessed management's swift execution in transforming into the largest e-commerce platform in Southeast Asia, and their successful navigation through the challenging macro-environment, I currently harbor reservations regarding Shopee’s sales efficiency, Garena’s inability to expand its user base, and SeaMoney's current deceleration in growth, despite its outperformance during the quarter. Until there are noticeable improvements, I will remain on the sidelines.

I maintain my hold rating due to my short to medium term concerns. Do also check out my previous coverage of the company’s 2Q23 results, and if you like what you read so far, I would appreciate a follow.

Digital Entertainment (“DE”)

Digital Entertainment’s Top-Line & Operational Metrics

{kind=link}

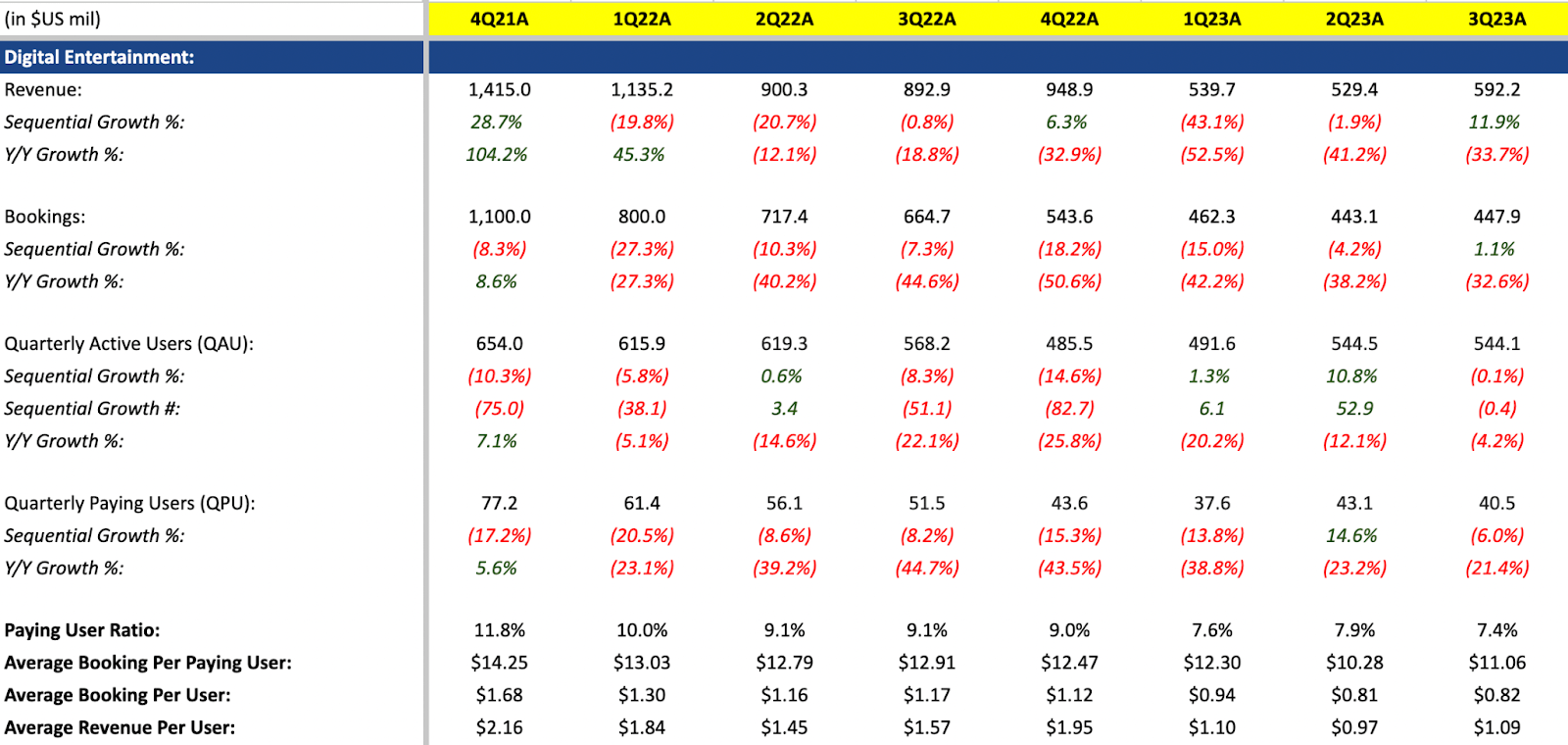

Just 2 quarters after reporting a recovery in both metrics in 2Q23, Garena's quarterly active users (“QAU”) and quarterly paying users (“QPU”) fell 0.1% and 6% QoQ, respectively, in 3Q23. The reopening of the schools caused the drop. The drop in QAU, however, has been mitigated by a rise in average revenue per user (“ARPU”) – increasing from $0.97 in 2Q23 to $1.09 in 3Q23. Bookings, made up of current revenue and change in deferred revenue, did improve modestly at 1% QoQ, suggesting a slight recovery in spending by its users.

Digital Entertainment’s Profitability

{kind=link}

Operating profit has improved as it grew 16.6% sequentially from $296.5 million in 2Q23 to $345.8 million in 3Q23 as a result of reducing operating expenses (“OpEx”), and operating margin expanded from 56% to 58.4% in 3Q23.

Both revenues and margins are likely to be more stable and less volatile in 4Q23 and FY24 beyond, which is in contrast to previous years, where comparisons were challenging due to the high growth driven by the impact of COVID-19.

E-commerce (Shopee)

SE’s E-commerce Financials SE’s E-commerce Operating Metrics

{kind=link}

{kind=link}

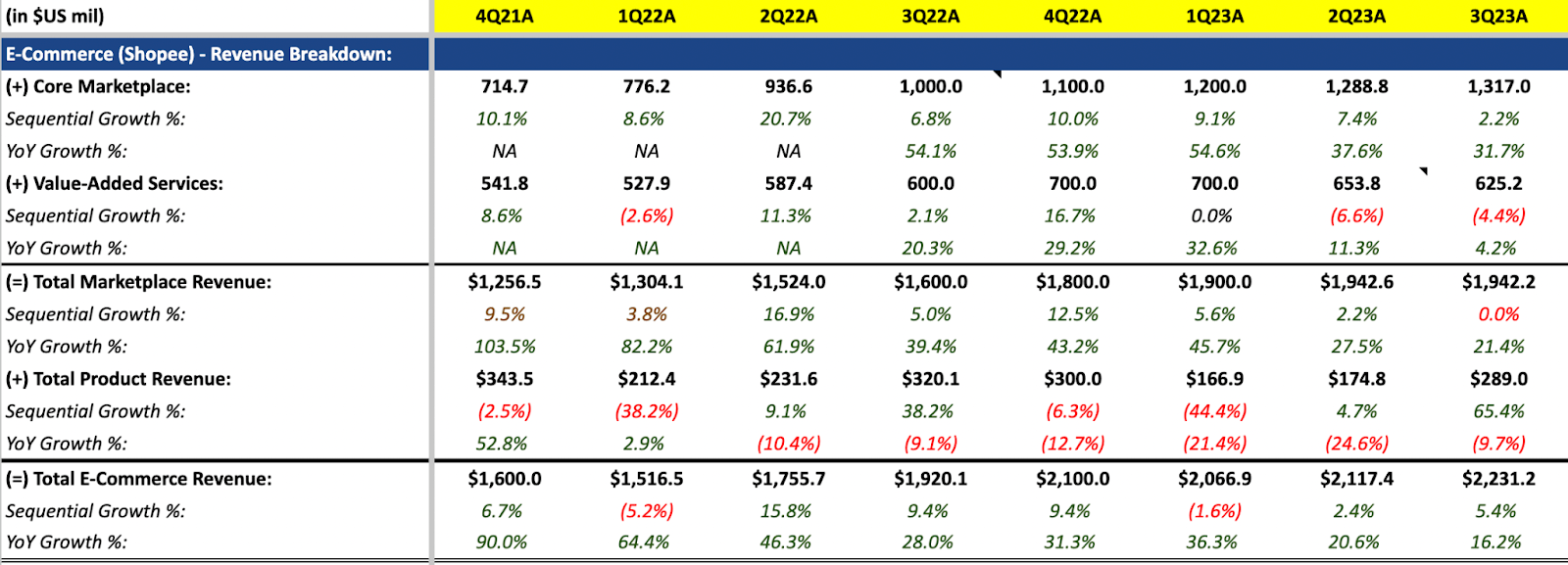

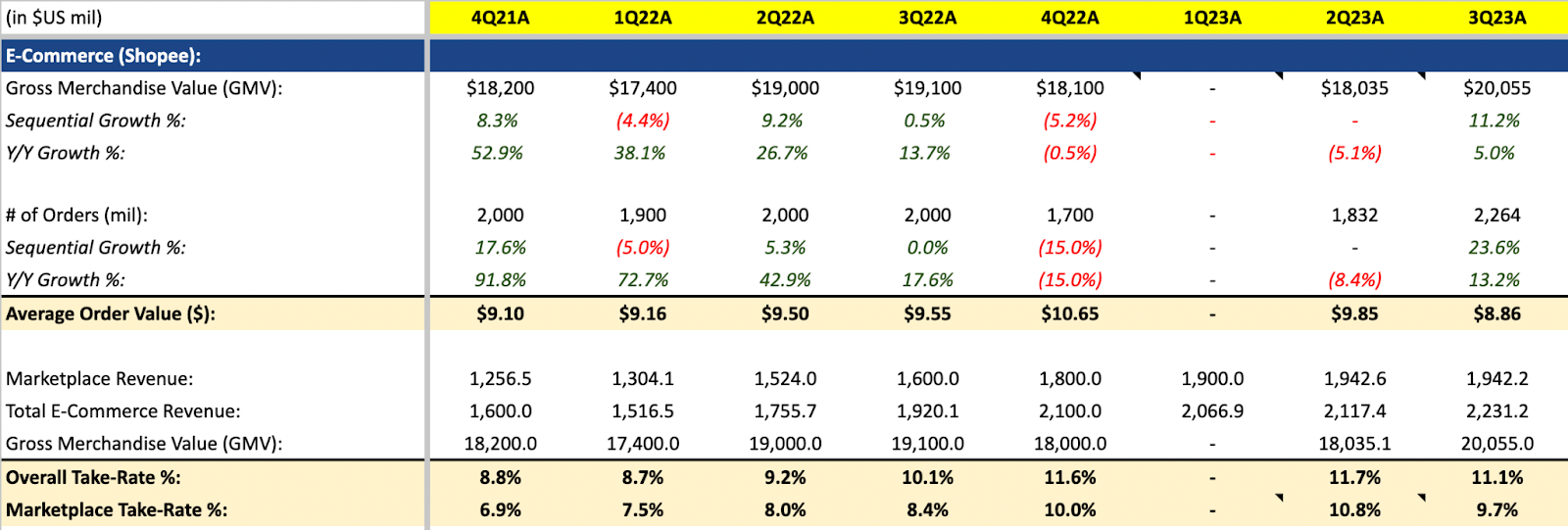

During the quarter, management reinstated the reporting of GMV and gross orders figures after two quarters of not doing so. While this move implies confidence in future growth, I found the reversal somewhat perplexing, as it created unnecessary confusion among investors and generated market noise. GMV and gross orders grew 11.2% and 23.6% quarterly, respectively, indicating a resumption in growth after pivoting to reinvestment mode last quarter. Investing in Shopee Live, the company's live-streaming platform, was emphasized heavily in the 2Q23 and 3Q23 earnings calls, which helped fuel the growth in GMV and gross orders. Furthermore, management highlighted the improving unit economics of Shopee Live.

Total marketplace revenue, consisting of core marketplace revenue and value-added services (“VAS”) revenue, declined slightly from $1,942.6 million in 2Q23 to $1,942.2 million in 3Q23. This is partially caused by increasing shipping subsidies and reduced logistic costs as VAS revenue fell 4.4% QoQ to $625.5 million. As a result, marketplace take-rate (i.e. Total Marketplace Revenue / GMV) fell from 10.8% in 2Q23 to 9.7% in 3Q23, and average order value (i.e. number of orders / GMV) also fell from $9.85 in 2Q23 to $8.86 in 3Q23.

E-commerce Sales and Marketing Expenses E-commerce Profitability

{kind=link}

{kind=link}

The observed growth is predominantly due to the substantial surge in S&M expenses, nearly doubling from $432 million in 2Q23 to $861.5 million in 3Q23. The main concern is whether these efforts have translated to top-line growth as revenue only grew at a mere 2.2% QoQ, which is lackluster to me. You might also be wondering – shouldn’t the TikTok ban in Indonesia benefit Shopee? As the ban only took effect on 3rd October 2023 , the impact may not be fully realized until the subsequent quarter. It is important to exercise caution as the threat from TikTok has not completely dissipated, and there's the possibility of their return to the market. Additionally, Lazada, a subsidiary of Alibaba (BABA), has also been ramping up S&M spending, which can be personally felt on the ground. Due to the rise in S&M expenses, the operating margin declined to -19.2% during the quarter.

Digital Financial Services ((DFS))

Digital Finance Service Revenue Digital Finance Service Profitability

{kind=link}

{kind=link}

DFS revenue grew 4.3% QoQ to $446.2 million, and growth has been slowly declining noticeably. Loan receivables expanded from $2 billion in 2Q23 to $2.4 billion in 3Q23. For the first time, management has disclosed its total credit portfolio of $2.9 billion, of which $1.4 billion are Shopee Pay Later Loan and $1.5 million are cash loans to Shopee buyers and sellers. For those unaware of how the credit business works, check out my detailed coverage of SeaMoney.

Operating profit increased 24.4% QoQ to $150.5 million, and margin expanded from 28.3% in 2Q23 to 33.7% in 3Q23, driven by top-line growth (by credit business) coupled with lower overall OpEx. A notable consideration during the earnings call is management's acknowledgment of a more cautious approach to growing the credit business in light of current economic conditions. Depending on the impact on credit quality, there could be a negative impact on both revenue and profitability.

Overview of Balance Sheet & Cash Flow Statement

Cash and cash equivalents, restricted cash, and short-term investments amounted to $7.4 billion as of 3Q23, an increase from $7.1 billion in 2Q23. The debt-to-equity ratio has steadily declined from 0.85 in 3Q22 to 0.52 in 3Q23 and has remained relatively stable from 0.53 in 2Q23. Operating cash flow (“OCF”) came in at $599.8 million, marking the fourth consecutive quarter of positive OCF. All of these highlight the company’s strong balance sheet.

Valuation

Sea Limited FY24 Valuation

Digital Entertainment: Projected QAU is set to reach 2,151 million, accompanied by an ARPU of $0.97, yielding a revenue of $2,086 million. Expecting an EBIT margin of 54.0%, the operating profit will reach $1,126 million. However, considering the heavy reliance on a single-game – Free Fire, the potential risk of insufficient contribution from new game launches, and a relatively modest growth rate, applying an EV/EBIT multiple of 8x results in an estimated enterprise value of $9,014 million.

E-commerce: GMV is projected to come in at about $85.40 billion – a growth acceleration from FY23. With a marketplace take rate of 9.5%, the expected marketplace revenue is $8.11 billion. Adding a product expected revenue of $874 million, FY24 revenue totals up to $8.99 billion. Considering the weak 3Q23 revenue growth, and uncertainty over the degree of reinvestments on future profitability, a revised EV/Sales multiple of 1x (from 1.2x previously) generates an enterprise value of $8.99 billion.

Digital Finance Revenue: The projected revenue for FY24 is expected to reach $2,177 million, yielding an estimated EBIT of $577 million with a margin of 26.5%. This projection accounts for the likelihood that the achieved margin in 3Q23 may not be sustained. Considering the declining growth rate, a revised EV/EBIT multiple of 13x (previously 15x) is applied, resulting in an enterprise value of $7,502 million.

Summing up: Factoring in net cash and the number of shares outstanding, the calculated equity per share stands at $49.46, representing a potential upside of 36% from the current share price.

Risks

Some of the key risks, while not exhaustive, include:

-

Digital Entertainment: Concern around the stabilization of QAU and QPU, lack of a recovery in user base

-

E-commerce: Higher-than-anticipated S&M expenses leading to reduced profitability, sustained weak top-line growth despite increased investments, heightened competition, and a potential dip in consumer spending due to inflation.

-

Digital Finance Services: Impact of higher-than-expected credit losses on revenue and profitability, and a reduction in profitability due to increased operating expenses.

Conclusion

We have seen how Shopee has proactively doubled down on reinvestments to bolster market share in a highly competitive market and aggressively grow the livestreaming business, given that it has nowhere to retreat but to defend its only turf. While I do have my concerns over its weak top-line growth and margins, I maintain the perspective that Shopee stands as the unrivaled leader in the region and remains poised to secure the lion's share of the market. While Garena QAU has exhibited stability, my concerns arise from the lack of a clear trend indicating a recovery in user base growth. SeaMoney reported healthy (albeit declining) growth rates and expanding margins, although I have my reservations about the 3Q23 margin being sustained.

In light of these uncertainties, I maintain a hold rating, despite recognizing the potential upside observed in my valuation.

For further details see:

Sea Limited Defending Its Turf