SE - Sea Limited: Disastrous Earnings Create Huge Opportunity

2023-08-18 05:38:07 ET

Summary

- Sea Limited stock has tumbled due to lackluster growth and disappointing guidance.

- The company faces tough competition in the e-commerce segment, and its financial arm has seen a significant decline in growth.

- Despite the challenges, SE remains a dominant force in Southeast Asia and offers a compelling valuation for investors.

Thesis Summary

Sea Limited (SE) has seen its stock tumble 25% following earnings . Not only was growth lacklustre, but the lack of guidance was disappointing.

Sea faces stiff competition in the eCommerce segment, and growth in its financial arm has fallen off a cliff.

The company has greatly improved its cash flow, and it remains a dominant force in Southeast Asia. The odds are in their favour, but without much guidance, it remains to be seen how SE will perform moving forward.

After this sell-off, the company offers a very compelling valuation, and based on Technical analysis, I think we could be close to a long-term reversal.

I'm adding more here and would look to double down if we dropped into the $30 area.

Q2 Earnings: Not What We Expected

Sea has seen its share price plummet following the recent Q2 results. Let's not beat around the bush; here's the issue with SE's latest report:

{kind=link}

SE was one of the COVID darlings and was once trading at close to $300 a share. Back in 2021, SE was exploding. Its Digital Entertainment segment was booming, with Free Fire one of the most-played games in the world. E-commerce was also doing very well since lockdowns accelerated the adoption of online shopping. And to top things off, its Financial Services segment was growing in the triple digits.

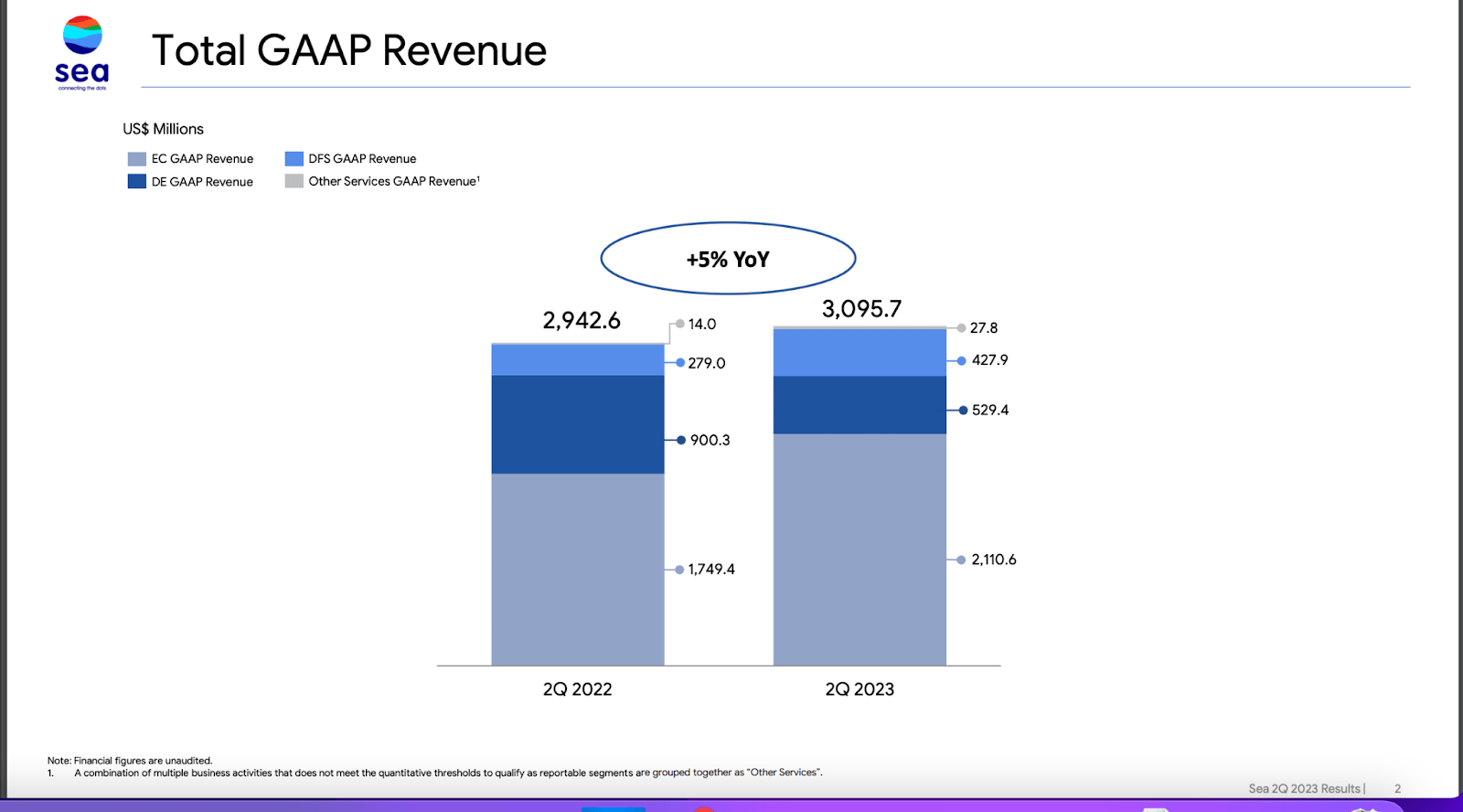

Fast-forward to Q2 of 2023 and what do we see? A meagre 5% YoY revenue growth and a share price of $40.

Clearly, a lot has changed. SE is no longer growing so fast, but it is also a lot cheaper, and this might be an opportunity to buy.

Let's dig into each segment to better understand what's going on:

{kind=link}

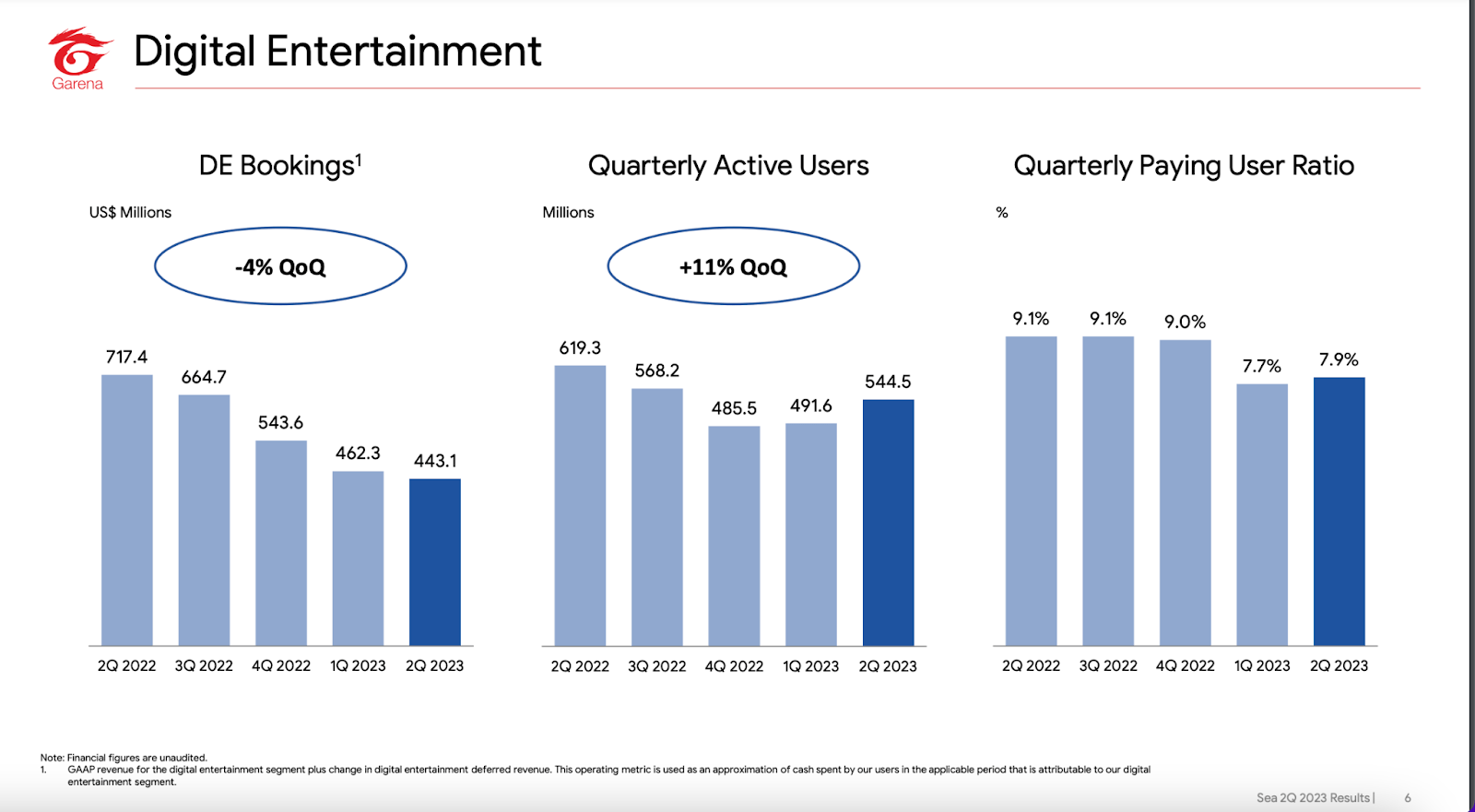

Starting with Digital Entertainment, we can see that Bookings have fallen by close to 40% since last year. However, we do see an interesting change in the trend in quarterly users. Can this be sustained? Is the worst over for Free Fire?

{kind=link}

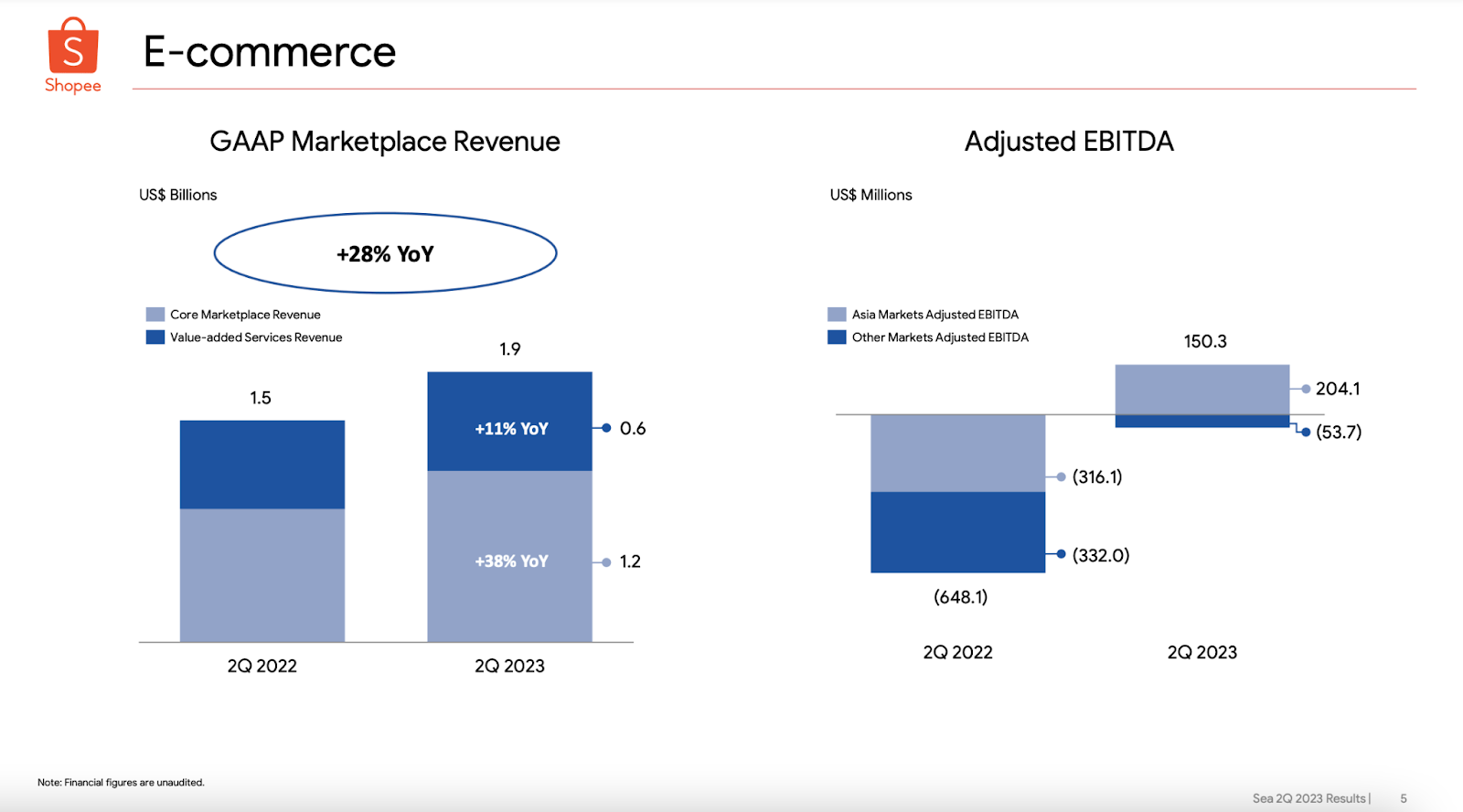

E-commerce has grown 29% YoY. We can see that most of the growth is coming from Core Marketplace Revenue. We can also see that, in terms of EBITDA, SE has achieved profitability in its more mature Asian market, and it is close to breaking even in its international endeavours.

{kind=link}

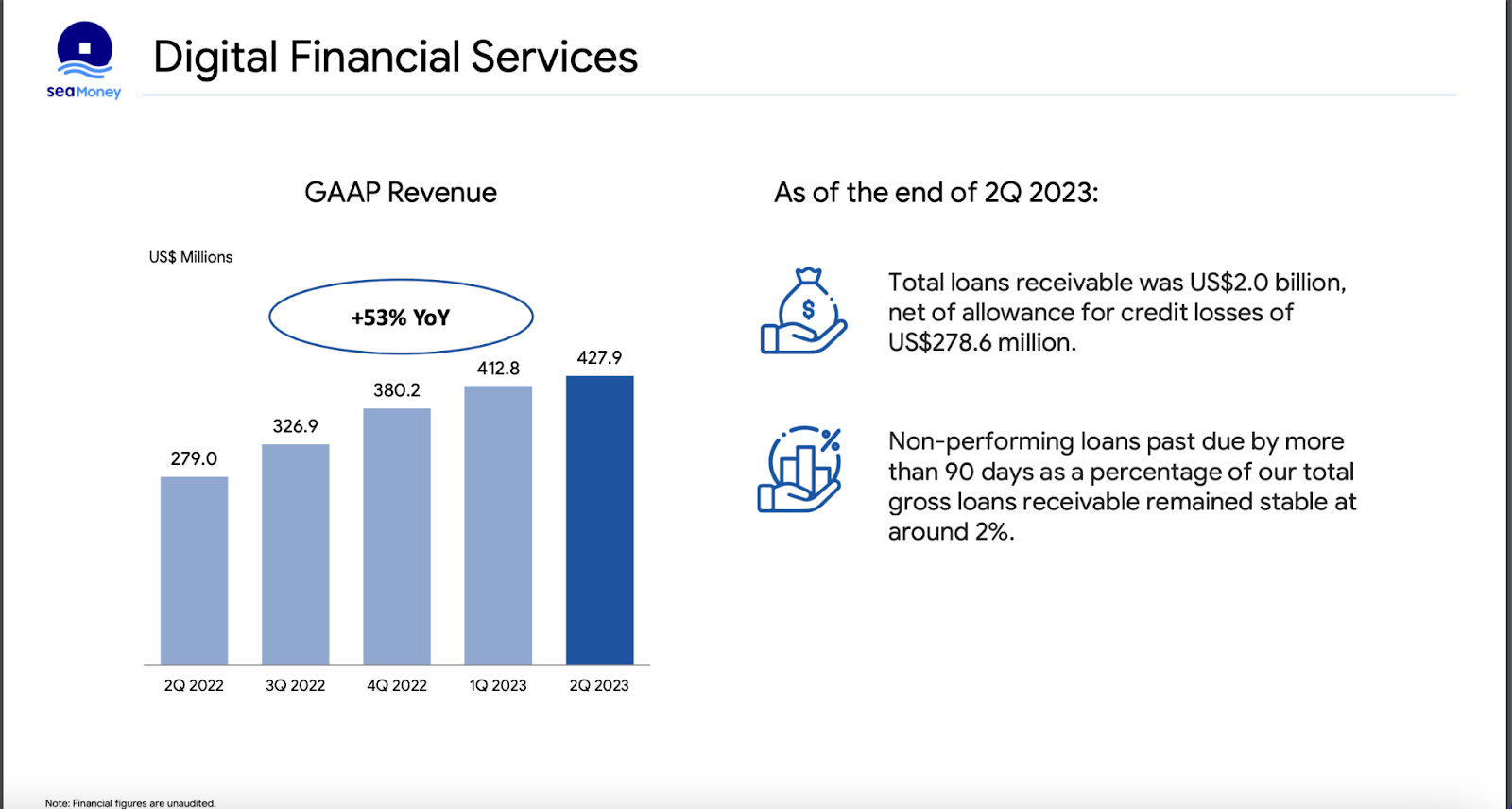

Lastly, Digital Financial Services has been the disappointing highlight of the quarter. YoY growth was 53%, but on a quarterly basis, this segment was nearly flat. The trend over the last five quarters, as we can see, has been clearly one of decreasing growth.

With that said, here's the silver lining:

{kind=link}

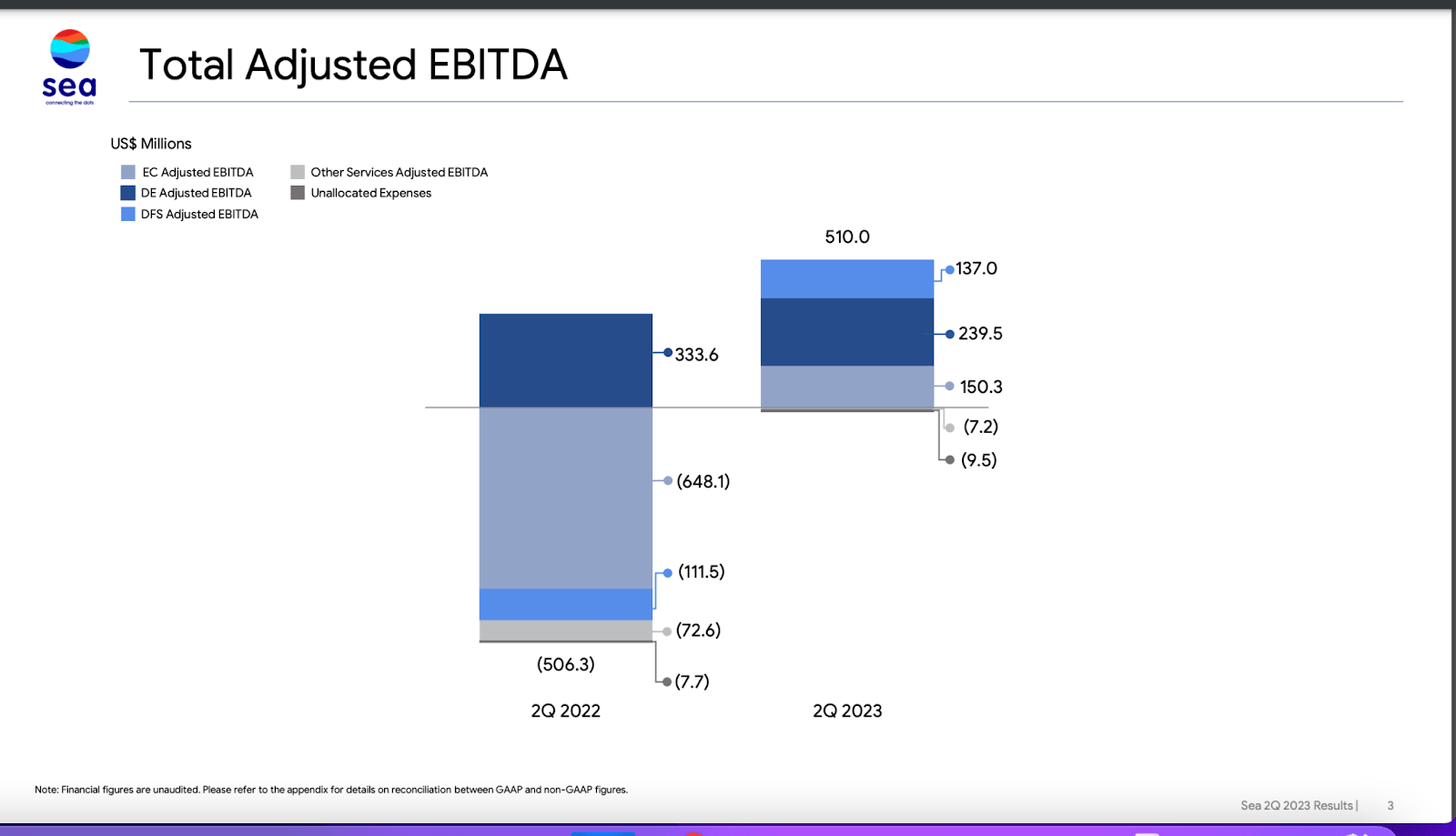

EBITDA is way positive now, with all of SE's segments reporting positive adjusted EBITDA. It is undeniable that SE has done a good job at keeping a lid on costs.

{kind=link}

Investors have been surprised by the latest earnings, understandably, but there's still a lot to like about SE, especially at this price.

The question is, what can we expect from SE moving forward? Has growth in DE peaked? Can Financial Services Growth re-accelerate? And what is the outlook on SE's e-commerce business as competition intensifies?

What To Expect Moving Forward

So what can we expect moving forward? Some answers can be found in the recent earnings call.

Given these positive developments and trends, we have started and will continue, to ramp up our investments in growing the e-commerce business across our markets. Such investments will have an impact on our bottom line and may result in losses for Shopee and our group as a whole in certain periods. However, this does not change our unwavering emphasis on self-sufficiency and improving cost efficiency as a key competitive moat.

Source: Forest Li, Earnings Call

Well, for those concerned about growth, SE's CEO has made it very clear that they are turning the growth engine back on. However, Li even mentions that this will have an impact on the bottom line, though self-sufficiency is key.

The way I see it, SE will invest as much as it can without jeopardizing its financial state, which seems like the right approach.

Now turning to games. So yes, as you pointed out, we are very happy to see positive trends on QAU, QPU, and -- as well as start to see signs -- positive signs for our Free Fire specifically on the booking number. But as we also shared earlier, we think this is a strong sign. On the other hand, we continue to monitor and observe the trends ongoing to see whether this is the beginning of a long-term stabilization."

Source: Forest Li, Earnings Call

When asked if we had turned a page in gaming, there was an encouraging trend, but management was not ready to draw any clear conclusions. It's also worth mentioning that "Undawn" recently launched, and the company also said it was too early to talk much about the data and that monetization was not a priority at this point.

In terms of the fintech business, we're pleased to see that it continues to produce strong cash flow and also a very strong year-on-year growth with a stable risk profile. And as we explained before, overall, we think at this stage, we try to maximize the synergies between our Shopee and SeaMoney ecosystem. And focus on building a strong platform with resilient and strong cash flow.

Source: Forest Li, Earnings Call

Again, the company was not very forthcoming with its predictions, which I guess is both good and bad. You don't want to make promises you can't keep. However, it is nice to see that the company is prioritizing "prudent" growth, especially in what has been a tough environment for lending.

All in all, I'd say the earnings call was not very insightful, so we'll have to draw some of our own conclusions in terms of the outlook for growth and profitability,

My 2 Cents

Starting with the eCommerce business, there's growth to be captured, no doubt. The Southeast Asia market is projected to grow at a 11.43% CAGR according to Statista:

Ecommerce growth (Statista)

In this region, Shopee controls 30%-50% of the traffic share, according to Similarweb , followed by Alibaba's ( BABA ) Lazada.

And watch out because there's another player in town, TikTok shops have taken the market by storm.

Seller app downloads (Apptopia)

TikTok is pouring huge amounts of money into this market and offering much more competitive rates than Shopee.

A CNBC check revealed that four-ply toilet paper from Nomieo was selling on TikTok at 5.80 Singapore dollars for twenty-seven rolls. In comparison, the same goods are selling at around SG$16.80 on Shopee.

Source: CNBC

Moving forward, there's only one-way Shopee can keep its throne, and that's improving its logistics network. We have seen some efforts in this regard, but I would like to see the company continue to do this more aggressively in the future.

When it comes to SeaMoney, again, there's a lot of growth left in the area. 70% of Southeast Asia is unbanked. But as mentioned in the earnings call, the growth in SeaMoney is dependent on Shopee.

Moving forward, I need to see the company make a commitment to focusing on growth in this area, instead of perhaps pursuing expansion abroad.

In terms of Garena, the gaming part of the company, there's not much to say. Popular games come and go, and Free Fire will never be what it was. I'm sceptical of the recovery in recent quarters.

But again, gaming is a huge segment, and the company has the potential to repeat this success. It has the know-how and the resources necessary.

And perhaps this is the most attractive thing at the moment:

CFO (koyfin)

SE is generating cash like never before, which puts it in a great position to finance growth cheaply.

Valuation

SE is definitely in a difficult position. Competition moving forward will be harsh. The good news is that with this latest price drop, SE is trading at a reasonable margin of safety.

{kind=link}

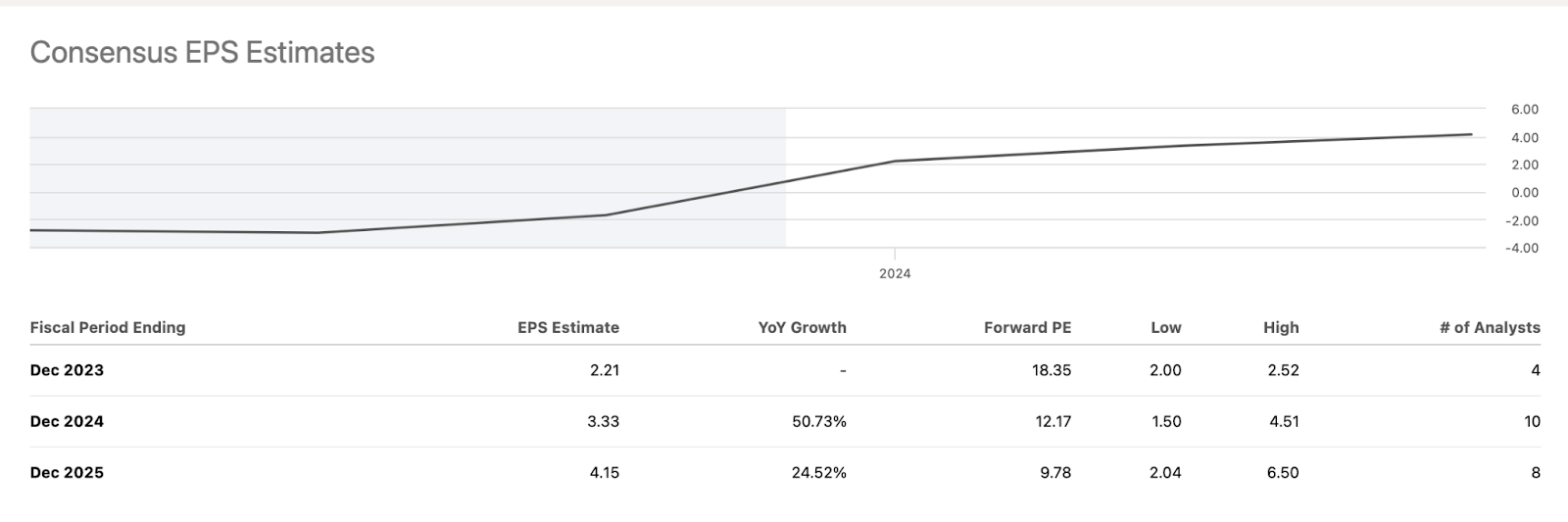

Analyst estimates on EPS suggest that SE is trading at under 10 times its 2025 earnings, which seems quite compelling.

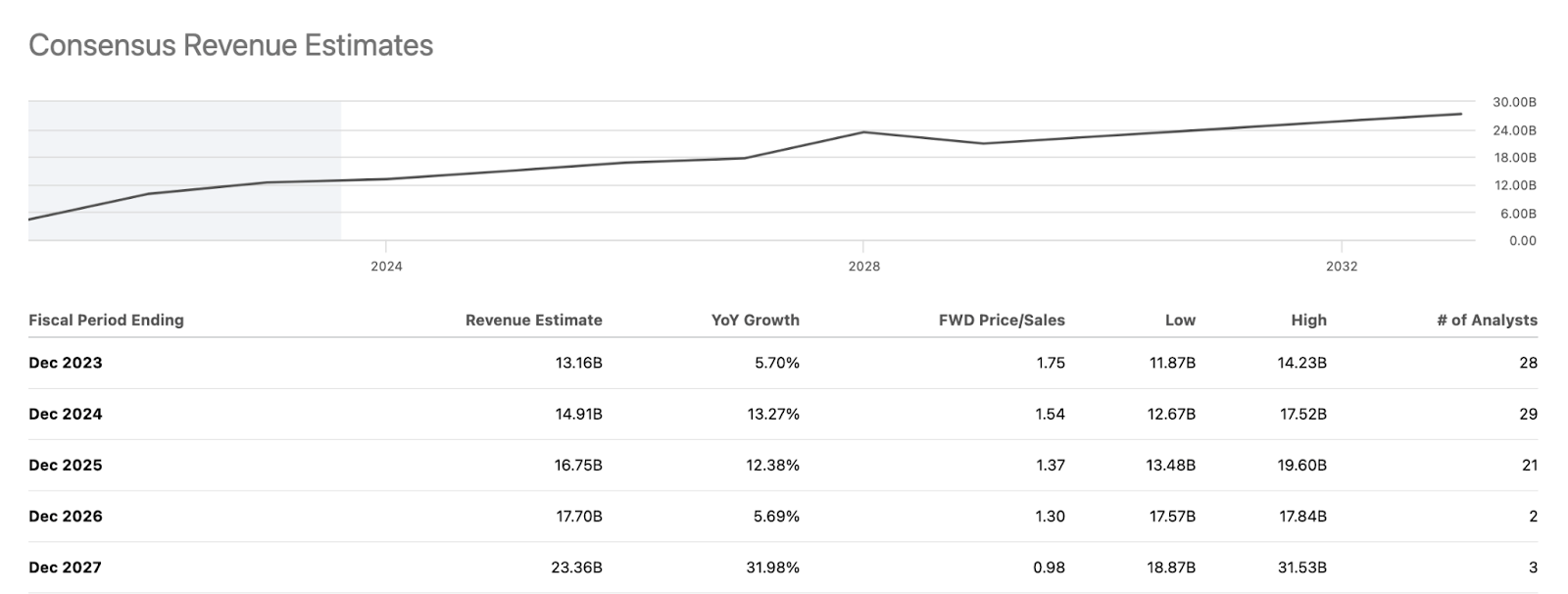

Furthermore, current revenue estimates are, in my opinion, quite conservative, leaving room for an upside surprise.

{kind=link}

Growth over the next 3 years would be around 10%, implying a 2025 forward P/S of 1.37

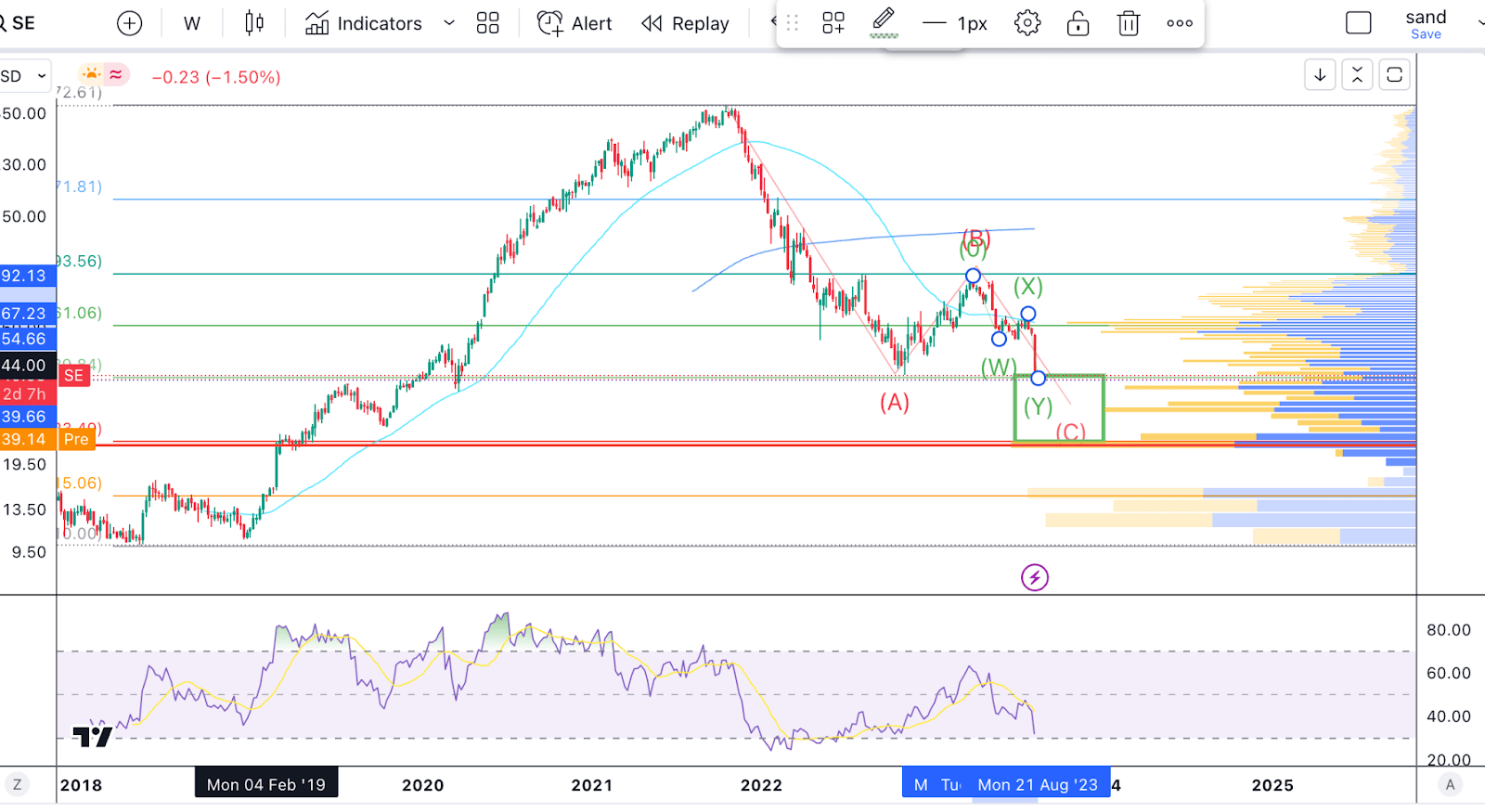

Now, let's move on to the TA.

{kind=link}

After a monster rally following its IPO, SE has now retraced a little over 61.8% from its all-time high. From an EW perspective, the bullish case is intact as long as we can hold above the 78.6% retracement.

For SE, this is around the $24 level. We can see in the graph that we also have strong support coming in from the Visible Range Volume Profile exactly at that level.

Furthermore, the RSI on the weekly is getting close to oversold, signalling a bottom could be close.

Ultimately, I'd be very surprised if SE reached the $24 level. Its valuation at that point would be incredibly compelling.

We also have some volume support coming in above $30 so this is where I'd add very aggressively, although I am already adding some more SE to my portfolio at these levels.

Takeaway

In conclusion, I won't deny that the quarterly results were disappointing. Personally, I was more disappointed with the lack of guidance. Hopefully, we will have clearer plans of what Shopee plans to do to remedy the situation by next quarter. Having said that, the company is in a strong financial position, has been growing cash flow and is now, after a 25% drop, very reasonably valued.

For further details see:

Sea Limited: Disastrous Earnings Create Huge Opportunity