SE - Sea Limited: No Love

2023-12-27 15:39:06 ET

Summary

- Sea's growth story is far from over.

- Profitability turned negative in Q3 - this was intentional.

- Analyst estimates are too low.

- Sea is trading at its cheapest valuation multiple ever.

- Investors loved it at $300. Shouldn't they love it even more at $40?

Introduction

Sea Limited ( SE ) is a Singaporean-based tech conglomerate that operates three high-quality companies in three secular markets:

- Garena - a global game developer and publisher of mobile and PC games including Free Fire, Arena of Valor, and Call of Duty Mobile.

- Shopee - the leading e-commerce platform in Southeast Asia, Taiwan, and Brazil.

- SeaMoney - a fast-growing digital financial services provider in Southeast Asia. These services include ShopeePay, SeaBank, and SeaInsure.

The company was one of the most intriguing growth stories in the early days of the pandemic. However, growth has slowed significantly over the last few quarters, so much so that it led to one of the most devastating crashes in the growth stock universe.

The funny thing is that investors were buying the stock aggressively back when the stock was trading at nosebleed valuations.

Investors loved it at $300. Shouldn't they love it even more at $40?

Well, that's not the case as the stock continues to struggle while the broader markets rally off to new highs.

That said, following its spectacular decline of about 90%, I make the investment case that it pays to be a contrarian today - I believe the risk to reward for Sea stock is heavily skewed to the upside.

Growth

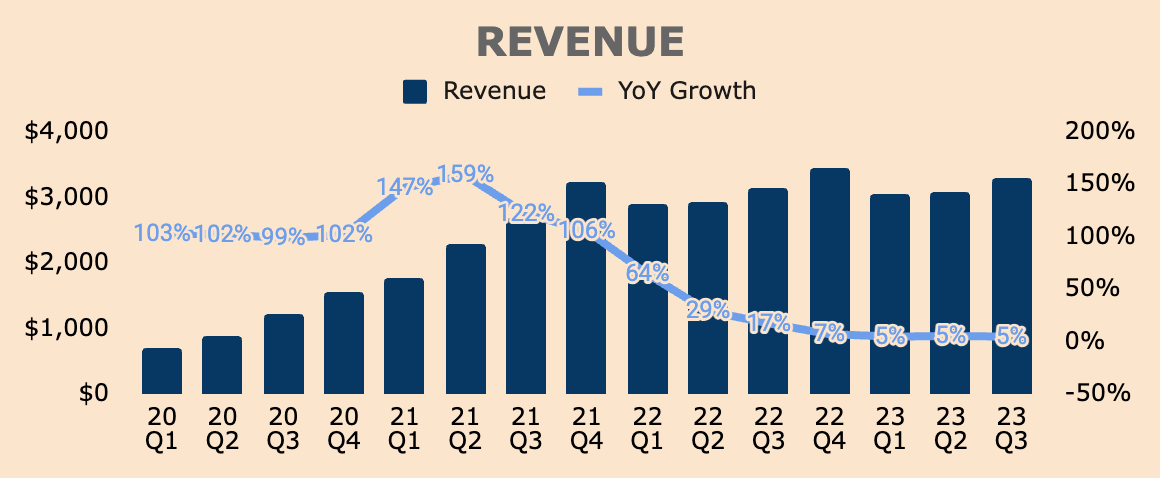

Looking at its topline, Q3 Total Revenue was $3.3B, up by a mere 5% YoY. While this beat analyst estimates by $90M, or 3%, Sea's growth has gone through a significant slowdown over the last few quarters, from its glory days of triple-digit growth in 2020 and 2021, to just mid-single-digit growth as of recently.

Years of growth have been pulled forward due to the pandemic, which consequently led to the company facing very tough YoY comps in the last couple of years, thus the steep deceleration in growth.

Now you see why shares of Sea are down so much.

{kind=link}

Let's take a look at the performance of each of Sea's business units.

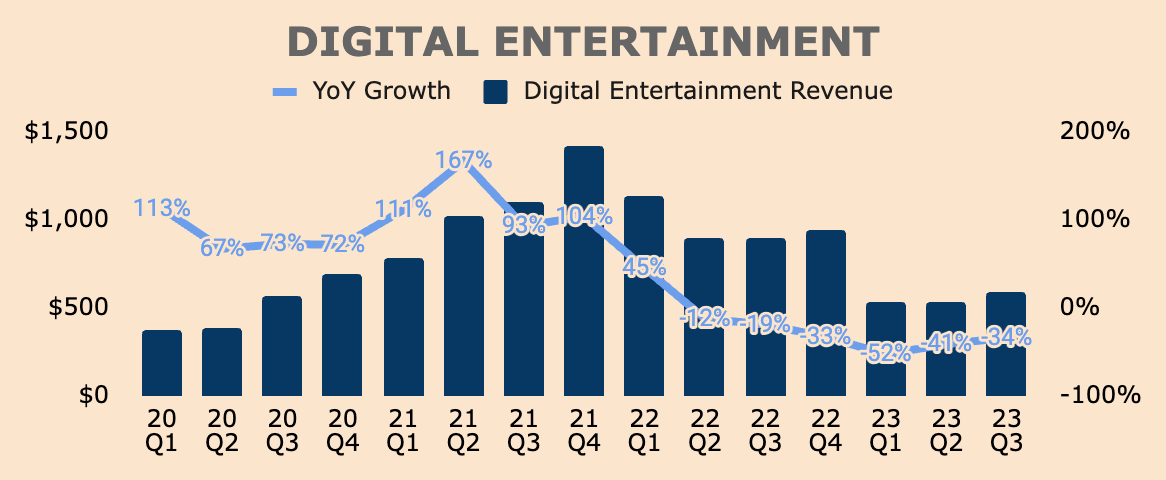

Looking at the gaming division first, Q3 Digital Entertainment Revenue was $592M. While this is up 12% QoQ, it is down 34% YoY and still far from its highs of $1.4B in Q4 of 2021. Nevertheless, it is still encouraging to see some signs of recovery in the business.

{kind=link}

The drop in Revenue was due to the moderation in user engagement, lower monetization, as well as the Free Fire ban in India starting in early 2022.

- Q3 Bookings were down 33% YoY to $448M.

- As you can see below, Q3 Quarterly Active Users were down 4% YoY and flat QoQ at 544M, due to global economies reopening.

- More importantly, Q3 Quarterly Paying Users were down even more, decreasing by 21% YoY to 41M.

- As a result, the Paying User Ratio dropped to new lows of just 7.4%, reflecting lower monetization rates within Garena.

As it relates to the Digital Entertainment business, QPUs is the most important metric to track. We saw a decent recovery in the metric in Q2 but it dipped again in Q3. On a positive note, QPUs remains higher than Q1's low of 38M - hopefully, that is indeed the low and that Garena continues to add more QPUs in the following quarters. That way, Garena can return to growth mode, after nearly two years of decline.

Author's Analysis

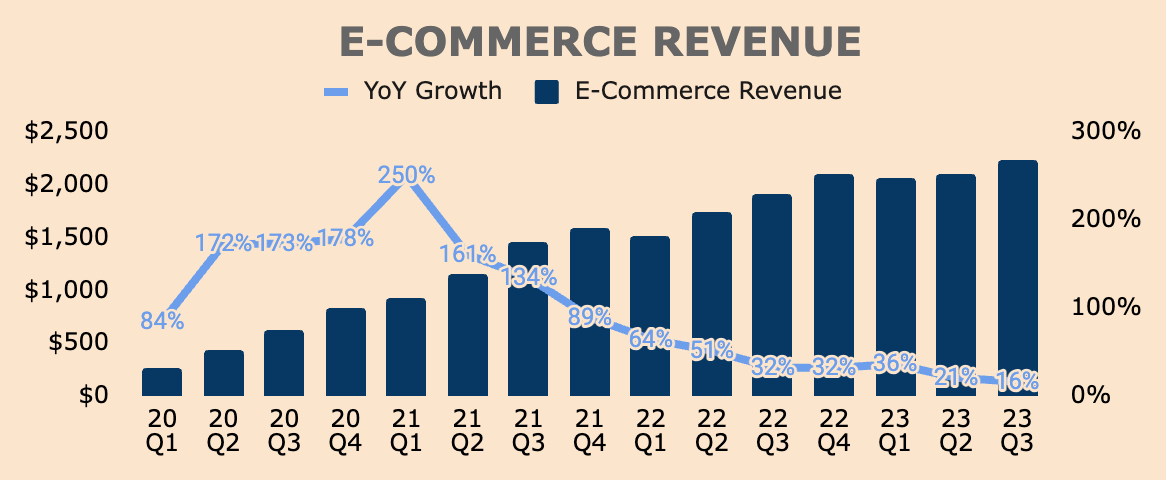

Turning to Shopee, Q3 E-Commerce Revenue grew 16% YoY to $2.2B, an all-time high for the company. This includes:

- Core Marketplace Revenue of $1.3B, up 32% YoY.

- Value-added Services Revenue of $0.6B, down 4% YoY.

Similar to Garena, Shopee's growth has also slowed down materially, although it stayed positive, unlike the gaming division.

{kind=link}

Growth was bolstered by a 5% YoY increase in GMV to $20.1B and a 13% YoY increase in Gross Orders to 2.2B.

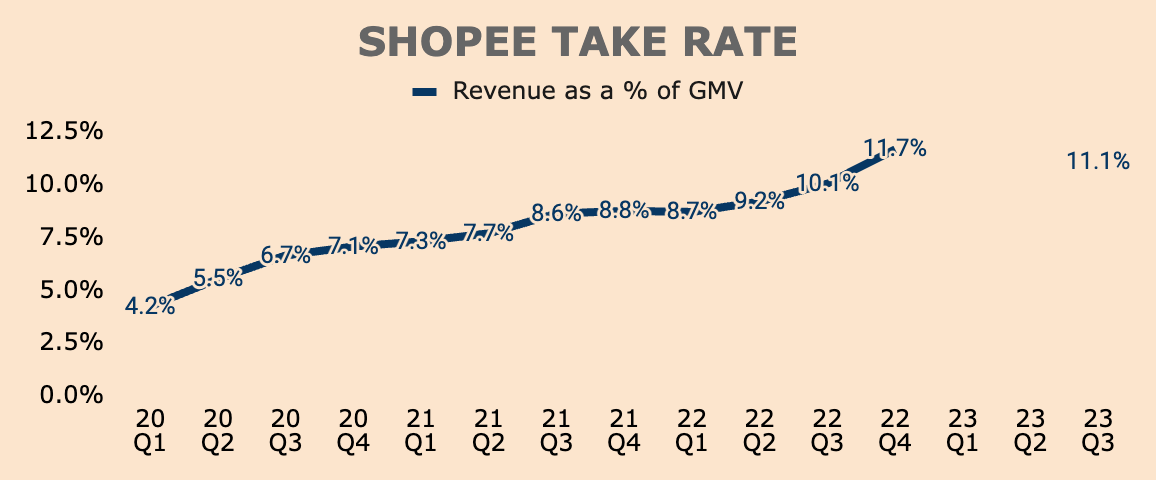

As you may have noticed, E-Commerce Revenue grew faster than GMV, primarily due to Shopee's improved Take Rate - or Revenue divided GMV - which reflects Shopee's increasing ability to monetize its platform.

As you can see, Q3 Take Rate was about 11.1%, which is about 100 basis points higher YoY. However, that figure is not as high as Q4's 11.7%, which could possibly mean lower fees for sellers and/or higher discounts for buyers, in an attempt to stimulate stronger growth.

(Note: Take Rates in Q1 and Q2 are left blank as Sea did not disclose GMV figures in both periods).

{kind=link}

Regardless, management is seeing strong engagement within the Shopee platform, particularly with Shopee Live as the company pushes into e-commerce live streaming. For instance:

- In Indonesia, 20% of daily active users watched live streaming in October. At the same time, the number of average daily streamers, hours streamed, and daily stream sessions all grew by more than three times in October, as compared to June.

- In Southeast Asia, orders on live streaming already accounted for more than 10% of total order volume in October.

With that in mind, Shopee Live should continue to be a key growth driver for Shopee as the company invests in more collaborations with content creators and live-streaming sellers.

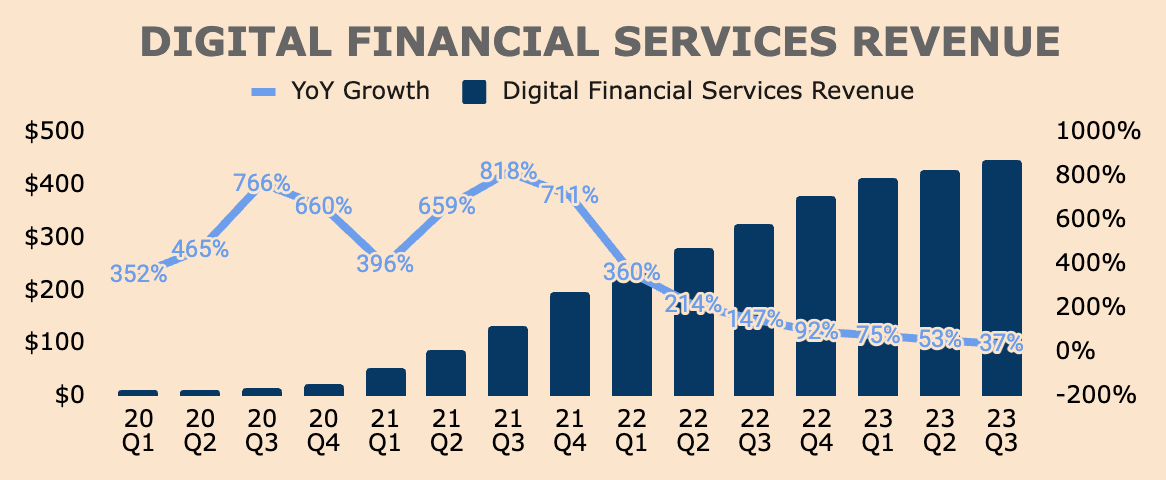

Moving on, SeaMoney continues to grow faster than the overall company. In Q3, Digital Financial Services Revenue grew by 37% YoY to $446M, a record high for the company. This was mainly due to its growing credit business, with its total credit portfolio expanding by 5% QoQ to $2.9B.

{kind=link}

All in all, Shopee and SeaMoney continue to grow rapidly, although not as fast as they did a couple of years ago, and this is reasonable given the larger size of each of these businesses.

On the other hand, Garena is the clear laggard, dragging the entire business down to subpar growth. Because of Garena, the growth profile of Sea does not look impressive at all.

As the saying goes, one bad apple spoils the bunch .

Consequently, the growth slowdown gave investors a major shock. And disappointingly, they are quick to conclude that Sea's growth story is over.

Rest assured, I believe Sea could return to strong growth mode in the next few quarters due to relatively easier YoY comps in 2024, the relaunch of Free Fire in India , as well as continued momentum with SeaMoney.

Profitability

While growth has been lackluster, profitability is on the right trajectory.

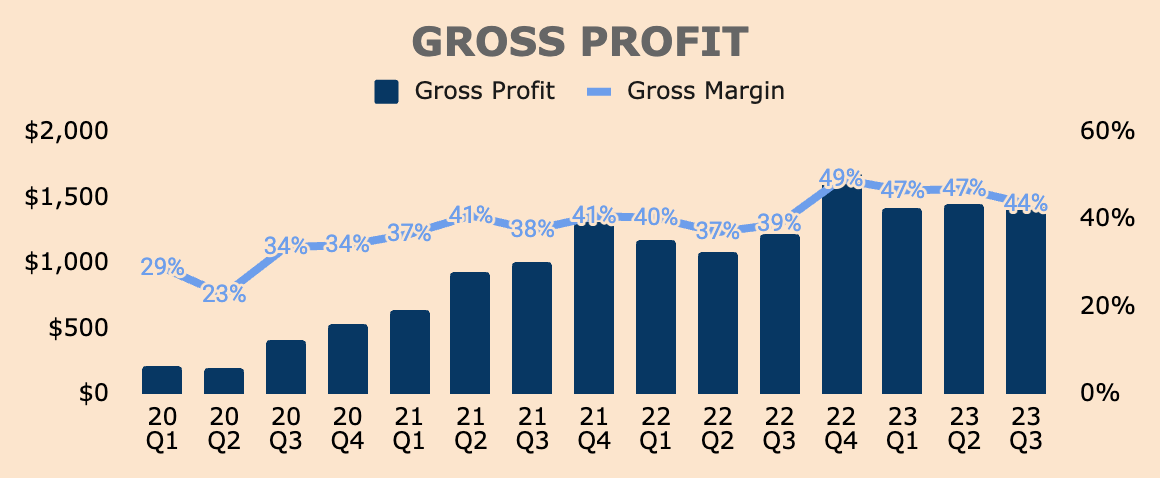

In Q3, Gross Profit was $1.4B, up by 17% YoY, despite Revenue growing by only 5% YoY. As a result, Gross Margin expanded from 39% last year to 44% in Q3, primarily due to increased monetization and greater cost efficiencies in Shopee and SeaMoney.

Although Gross Margin has trended down over the last few quarters, the long-term trend is still up, and that demonstrates economies of scale within the business.

{kind=link}

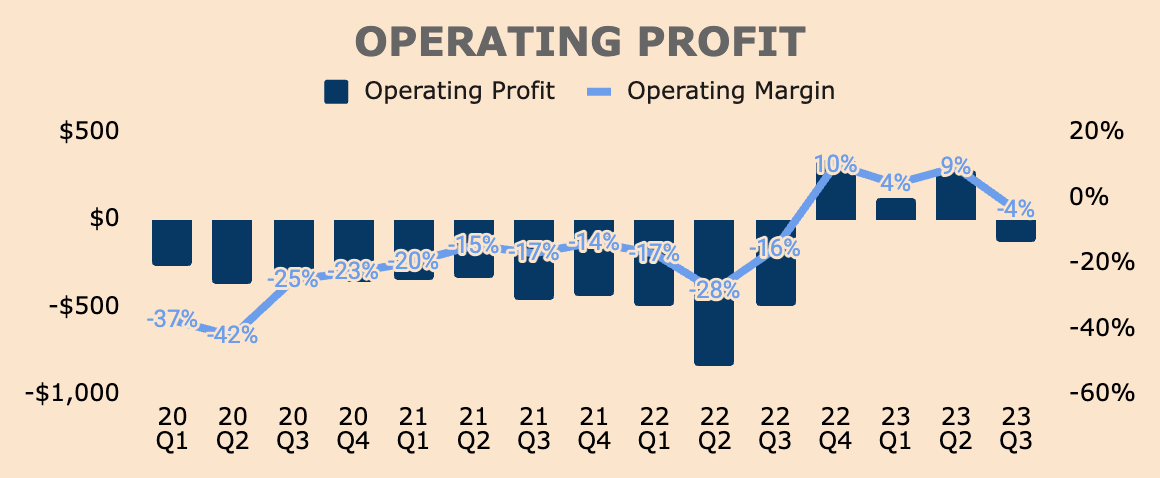

Moving down the income statement, Q3 Operating Profit was $(128)M, which is a (4)% Margin. As you can see, Operating Margin flipped to negative again after three consecutive quarters of operating profitability.

{kind=link}

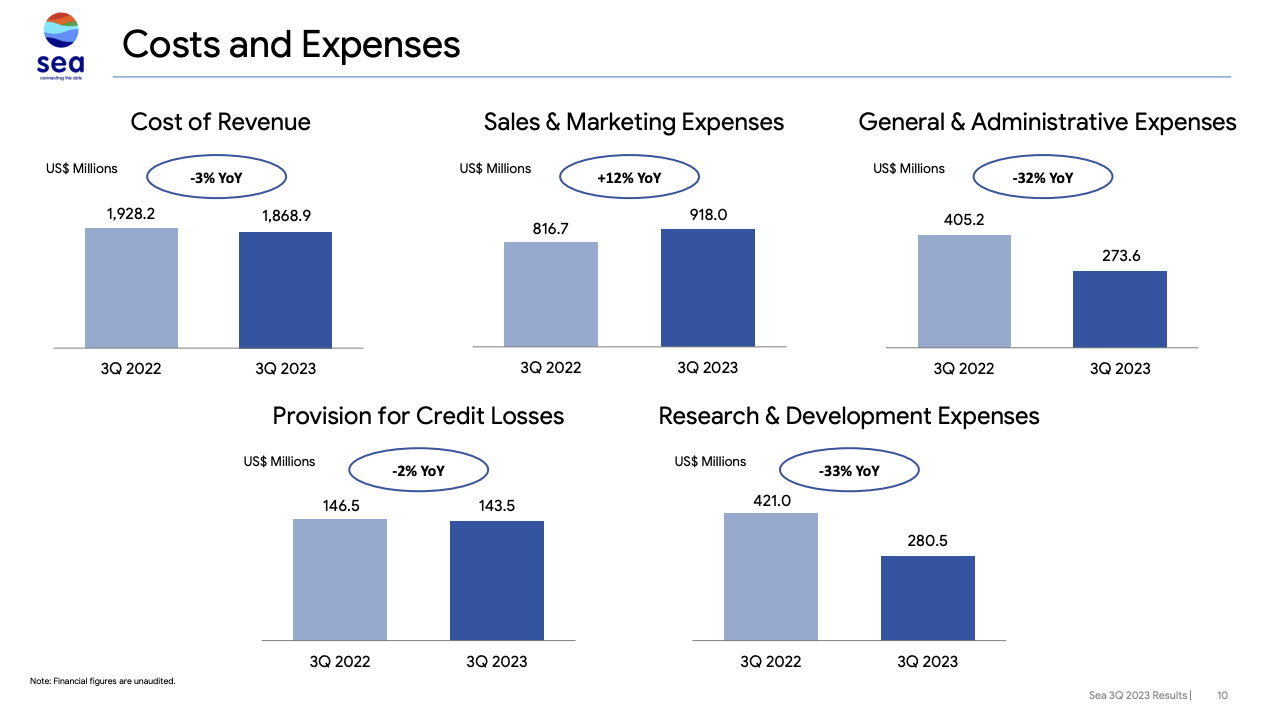

Sea has been focusing on optimizing operating expenses and achieving higher cost efficiencies throughout most of 2022 and the first half of 2023. However, it seems that Sea is finally ramping up spending once again.

It looks like all the cost savings from other areas of the business were used for Sales and Marketing Expenses, which increased 12% YoY, or 86% QoQ, to $918M. Not surprisingly, over 90% of it was allocated to Shopee, which saw Sales and Marketing Expenses rising by 50% YoY to $862M.

Sea Limited FY2023 Q3 Earnings Presentation

{kind=link}

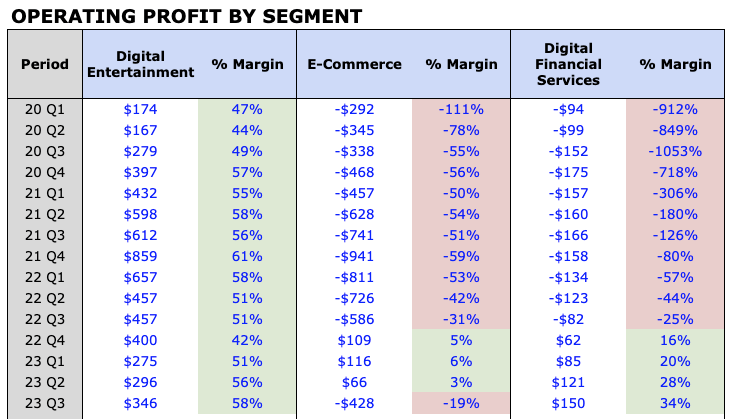

If we look at Operating Profit by segment, we can see that the E-Commerce segment turned unprofitable once again, burning $(428)M in Q3, representing an Operating Margin of (19)%. Despite the huge swing to the downside, the losses from the E-Commerce segment are covered by the other two higher-margin segments, which saw Operating Margins improving YoY and QoQ.

{kind=link}

It's safe to assume that with improved profitability in Garena and SeaMoney, management is turning more aggressive in terms of capturing market share and growing GMV for Shopee.

A few years ago, this strategy would not have been sustainable. But today, Sea is self-sufficient enough to exploit Shopee's growth potential.

What's more, Shopee in Brazil is inching closer to profitability, with Contribution Margin Loss Per Order improving 91% YoY to $0.10 in Q3. Eventually, this should put less burden on Shopee's operating profitability.

In addition, SeaMoney should also enjoy better unit economics over time as the segment scales - 40%+ Operating Margin looks possible given the momentum.

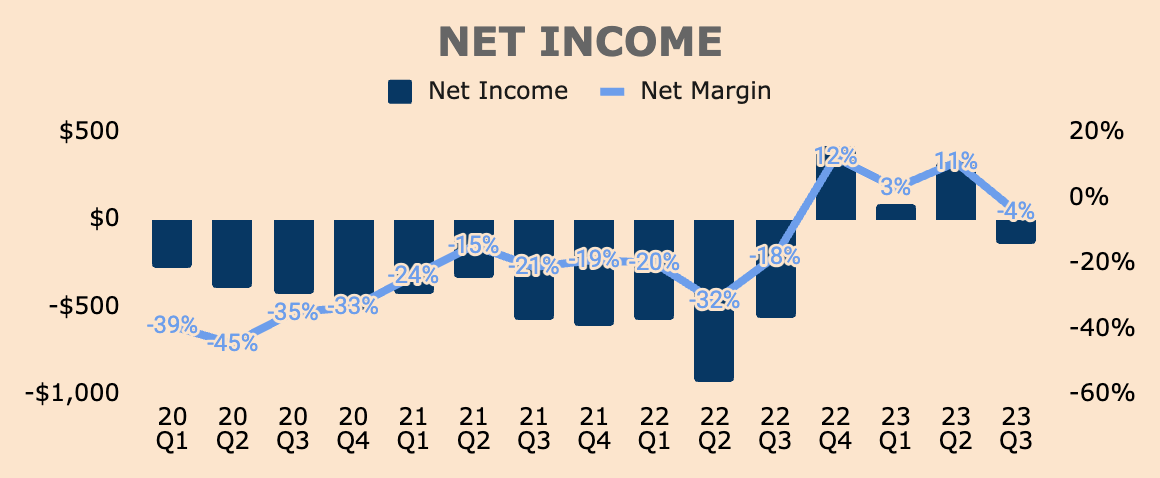

In Q3, Net Income was $(144)M, which is a (4)% Margin. Net Margin turned negative in Q3, again, due to elevated marketing spend. I expect this to continue as Q4 marks the holiday season, so don't be surprised if Net Margins remain negative.

{kind=link}

That said, Sea should return to GAAP Net Income profitability as the company scales further - I expect this to happen sooner rather than later.

Previously, Sea operated a growth-at-all-costs strategy, stacking loss after loss in pursuit of upsized growth. However, Sea has pivoted to one that balances growth and profitability, which led to margin expansion.

Be that as it may, the profitability narrative turned negative in Q3.

Fortunately, this was intentional - after some time of disciplined cost controls, management is now focusing on increasing market share and strengthening market leadership.

Sea, being in a fundamentally stronger position, is now ready to ramp up spending to stimulate growth.

The question remains as to whether Sea can sustain growth and improve profitability in the long run - not just for a few quarters. That is the ultimate test of a truly scalable business model.

Health

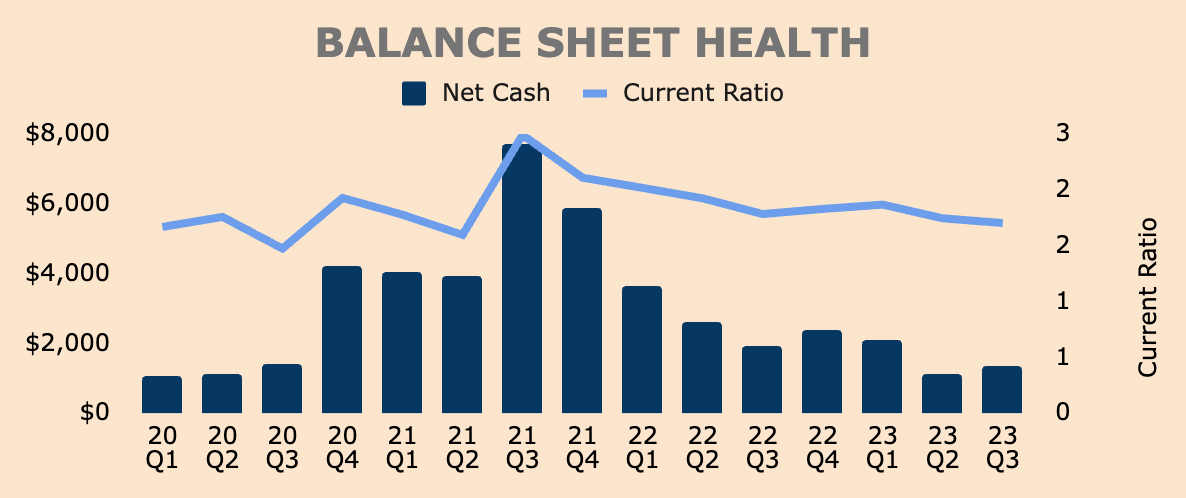

Turning to the balance sheet, Sea has $6.0B of Cash and Short-term Investments with $4.6B of Total Debt, placing its Net Cash position at $1.4B.

As you can see, Net Cash has fallen substantially over the past two years as Sea has pretty much stopped raising capital in the equity and debt markets -as mentioned earlier, the company aims to be self-sufficient and not rely on external funding.

That said, we should see Net Cash build up over time as management focuses on profitable growth.

{kind=link}

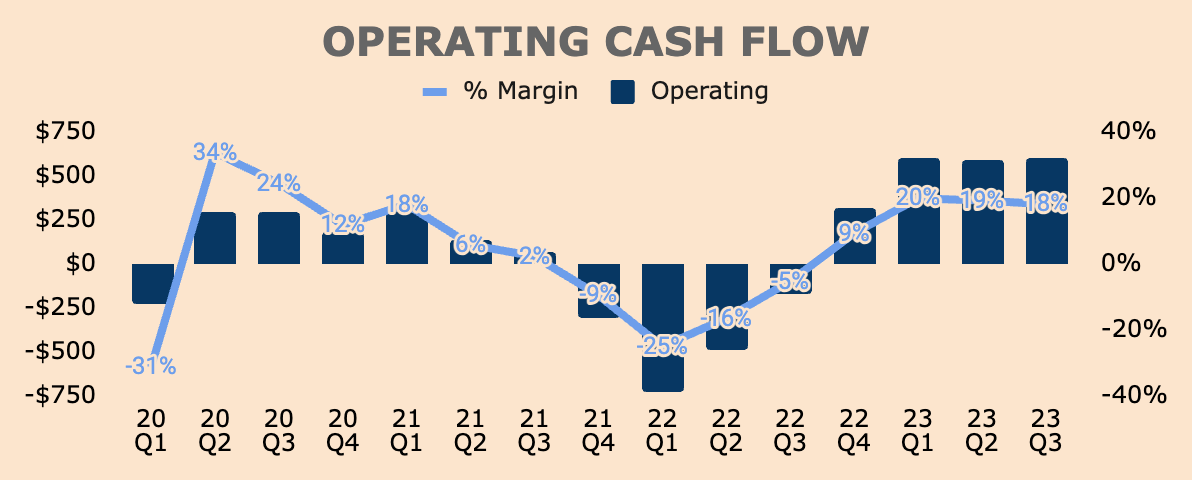

In terms of cash generation, Sea had an Operating Cash Flow of about $600M in Q3, which represents an OCF Margin of 18%. In the first nine months, OCF improved from $(1.4)B to $1.8B, which is remarkable given that the cost-cutting initiatives started only a year ago. This goes to show that Sea is capable of managing its capital efficiently.

{kind=link}

With positive cash flow generation in place, Sea is in a good financial position to reinvest and reaccelerate growth, which is what the company aims to do moving forward.

In this current period, we will prioritize investing in the business to increase our market share and further strengthen our market leadership. We now have scale, a deep understanding of our markets, and strong localized execution across diverse geographies. This gives us a wide competitive moat, and we intend to grow it further. Our move to self-sufficiency and profitability in the past quarters has significantly improved both our cash reserves and operational efficiency and we see a very good opportunity to build our e-commerce content ecosystem efficiently especially in live streaming.

Outlook

Management did not give any guidance. I think part of the reason why the stock sold off so much is that management failed to give guidance, which is just another way of saying: 1) "We don't have good visibility in our current operating environment" or 2) "Our forecast is so bad that we're better off not giving guidance".

Whatever it is, I would love to see better communication from management moving forward, and hopefully, they'll do that in their Q4 earnings release. This should boost investor confidence.

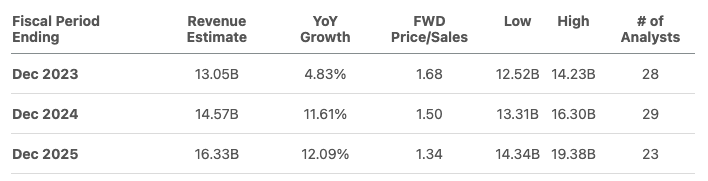

That said, analysts expect Q4 Revenue of $3.5B, which is only a 2% growth YoY. This also means that they expect Revenue to decelerate from Q3's growth of 5%.

During the earnings call , management made it clear that they "will continue to invest in the holiday shopping season, which we believe is a good time to acquire users, gain market share, and strengthen our content ecosystem".

In other words, we should continue to see elevated marketing spend and this should lead to higher-than-expected Revenue growth in Q4.

Regardless, Sea should enter 2024 with relatively easier comps, which is why analysts expect growth to reaccelerate to 12%, on top of 2023's growth of just 5%.

{kind=link}

In other news, Shopee remains the third most downloaded shopping app worldwide, which should support growth in future quarters.

Data.ai

More excitingly, two of Garena's mobile games - Black Clover M and Free Fire - are the top three most downloaded games worldwide in the last 30 days. Including the relaunch of Free Fire in India, these should drive sequential growth for Sea's Digital Entertainment segment.

Data.ai

With this in mind, I believe Q4 analyst estimates are too low. I believe Sea's market leadership, Shopee's return to growth spending, and Garena's rebound, should all drive better-than-expected growth numbers in Q4, which should set the stock up for a strong 2024.

Valuation

From a historical standpoint, Sea is trading at its cheapest valuation ever.

As you can see, Sea is trading at just 1.5x EV to Revenue, far below its peak of 31.8x. A return to its 5-year average multiple of 11.1x would result in a 700%+ appreciation in share price.

Sure, the lower multiple is justified given the company's slowing growth rate. However, Sea is now a much larger, more profitable, and competitively stronger company than it was two years ago.

It's funny how the same investors who were happy to buy the stock back when it traded at $300+ with a Revenue multiple of more than 30x, are now quick to dismiss the stock despite trading at a 90% discount to its all-time highs.

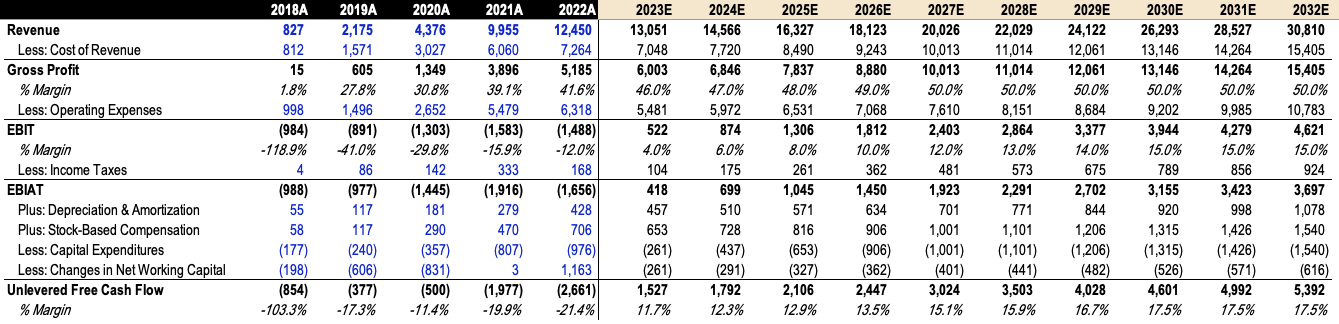

My DCF model also shows how undervalued the stock is. Below, you can see my key assumptions:

{kind=link}

For Revenue growth, I followed analyst estimates for the first three years and slowly dropped growth rates over time. By 2032, I expect $30.8B in revenue for Sea.

I also expect Sea to achieve economies of scale through the years, thus leading to margin expansion. By 2032, I expect a stable Free Cash Flow Margin profile of just 17.5%. As a reference, MercadoLibre ( MELI ), which has a very similar business model to Sea, has an FCF Margin of 23.6% in 2022, so my long-term FCF Margin for Sea is actually very conservative.

{kind=link}

Using a discount rate of 10% and a perpetual growth rate of 2.5%, I arrive at an intrinsic value per share of ~$83 for Sea stock, which is more than double the current price of $39. It is also much higher than the average analyst price target of $56.

Below, I've also included my bear and bull cases.

As you can see, even assuming a lower FCF Margin and perpetual growth rate, Sea still trades at a considerable discount.

Author's Analysis

In short, I believe Sea stock is significantly undervalued.

But I guess a lot of investors think otherwise, as we've seen with the continual decline in the share price.

Let me remind you. Sea has:

- Some of the most valuable and successful mobile game assets in the world.

- The most dominant e-commerce platform in Southeast Asia (and possibly Brazil soon).

- A fast-growing fintech giant in the making.

Now, at $40 a share, Sea stock seems to be left dead in the water with sentiment at an all-time low - it pays to be a contrarian today.

In my eyes, Sea is trading at deep value territory and any slight positive catalyst could launch the stock price higher with relative ease.

Risks

Competition is the biggest bear argument against Sea. Many investors fear the company is losing market share to competition, thus slowing Sea's growth. This includes names such as Lazada ( BABA ), Tokopedia, and Mercado Libre.

Most recently, TikTok joined forces with Indonesia's GoTo, which owns Gojek and Tokopedia. The social media company invested over $1.5B in GoTo, including $840M to acquire a 75% stake in Tokopedia.

The deal enabled TikTok to resume its shopping app service in Indonesia, following Indonesia's ban on e-commerce transactions directly on social media platforms.

Under the agreement, TikTok Shop will be combined with Tokopedia, essentially allowing TikTok to bypass the ban by redirecting shoppers to Tokopedia, where they will complete their purchases.

This was a huge development as there are a lot of synergies:

- TikTok - the biggest social media platform in Indonesia.

- Tokopedia - an e-commerce powerhouse in Indonesia.

- Gojek - has an extensive logistics network and the most popular mobile wallet in Indonesia, GoPay.

It made sense why shares of Sea plummeted following this news.

But one part of the deal really got my attention: TikTok acquiring 75% of Tokopedia for $840M.

That implies a valuation of about $1.1B.

Just three years ago, Google ( GOOG ) invested in Tokopedia at a valuation of $7.5B.

To see that big of a valuation drop and to see GoTo selling Indonesia's jewel to a foreign company at less than $1B, seems fishy to me. GoTo might be in a bad financial position to pull off that kind of move.

And this could actually be bullish for Sea.

In addition, if the deal doesn't fall through ( expected to close in Q1 of 2024 ), Sea could enjoy market share gains which should be a major catalyst for the stock.

If it does go through, Sea stock may be pressured for some time as sentiment turns sour again.

Thesis

Sea is at an inflection point.

More specifically, the company is gearing up for profitable growth as it abandons the grow-at-all-costs mentality.

While growth has been lackluster lately, Sea still has a long growth runway due to secular trends in the mobile gaming, e-commerce, and fintech industries.

That is why management is sacrificing short-term profitability for long-term market share gains and leadership, which should generate strong returns for shareholders in the long run.

Investors loved it at $300, back when the stock was trading at nonsensical valuations.

Today, investors can pick up shares of Sea at a 90% discount, despite being a fundamentally stronger company overall. What's more, growth is set to reaccelerate in 2024 and analysts have set a low bar on Sea as well.

Yet, it receives no love.

I think that's just irrational market behavior - in this kind of situation, it pays to be a contrarian.

For further details see:

Sea Limited: No Love