SE - Sea Limited: Pandemic Bottom Is Here - Speculative Buy For The Patient

2023-08-18 14:00:56 ET

Summary

- SE's performance has been more than decent in our opinion, thanks to the improved cash monetization and expanded EBITDA margins.

- However, it is apparent that Mr. Market is expecting a lot more, with bullish support still missing, triggering the drastic decline in its stock prices after both FQ1'23 and FQ2'23.

- The Asian Development Bank still expects the Southeast Asia region's inflation to be elevated through 2025 as well, dampening SE's prospects in the intermediate term.

- Investors may want to temper their expectations for now, since the stock may remain volatile moving forward.

The SE Investment Thesis Is Only For The Patient - Bullish Support Has Yet To Materialize

We previously covered Sea Limited ( SE ) in June 2023, rating the stock as a Buy thanks to the drastic plunge after its FQ1'23 earnings call. However, we had also cautioned investors that the stock might remain volatile, attributed to the elevated short interest and the reversal of its cost optimization efforts in FQ4'22.

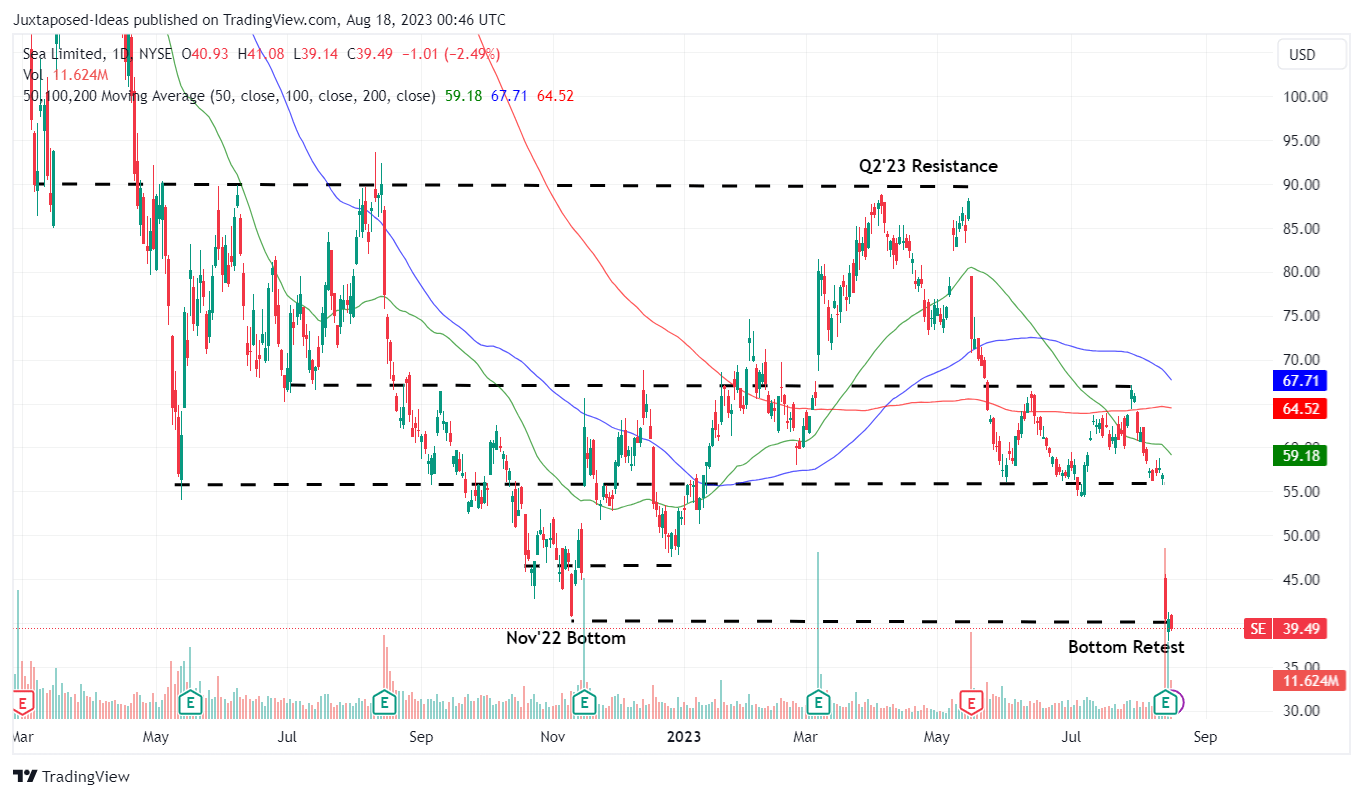

With the stock further moderated to its fair value after the recent FQ2'23 earnings call, we believe that the risk reward ratio is highly attractive here, especially given the improved margin of safety to our long-term price target of $89.37.

SE 1Y Stock Price

{kind=link}

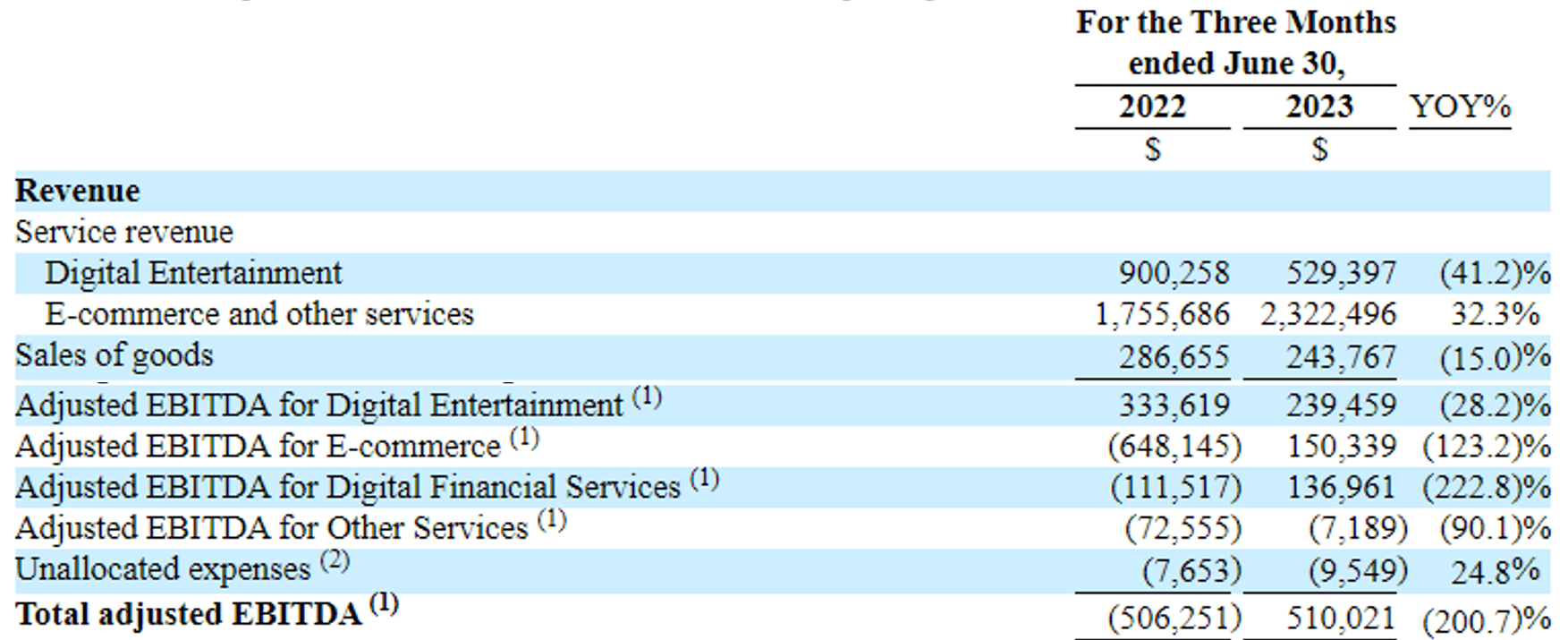

For now, the SE stock has dramatically lost over -30% of its value after the mixed FQ2'23 earnings call , despite the impressive profitability beat. The e-commerce company reported revenues of $3.09B (+1.6% QoQ/ +5.2% YoY) and GAAP EPS of $0.54 (+260% QoQ/ +132.3% YoY).

If we are to look closer, it is apparent that its adj operating expenses have remained stable QoQ at $1.01B (-38% YoY) excluding provision for bad debts, with an overall operating margin of 9.2% (+2 points QoQ/ +31.6 YoY) in the latest quarter.

It appears that SE has intensified its short-term investments to $2.17B (+329.6% QoQ/ +68.9% YoY), contributing to the temporal boost of its profitability with an interest income of $107.6M in the latest quarter, naturally explaining the acceleration of its EPS in FQ2'23.

On the one hand, we are encouraged by the management strategic choice to finally take advantage of the elevated interest rate environment and the robust balance sheet with $5.69B of cash (-13.5% QoQ/ -26.8% YoY).

On the other hand, it appears that the company has reached its steady state operating cadence, drastically expanded by +53% compared to the previous FQ4'22 expenses of $663.1M, though moderated by -41.2% from FQ3'22 expenses of $1.72B.

Assuming so, SE investors must brace for impact indeed, since it is unlikely that things may improve in the near term, attributed to its mixed performance thus far.

SE's Performance By Segment

{kind=link}

For example, SE reported declining Digital Entertainment revenues of $529.39M ( -1.9% QoQ / -41.1% YoY) and decelerating E-commerce and other services revenues of $2.32B (+3.1% QoQ/ +32.5% YoY) in FQ2'23.

This suggests that the Southeast Asian region continues to face tightened discretionary spending, despite the MoM decline in Singapore's June 2023 CPI to 4.5% (-0.6 points MoM/ inline YoY).

Then again, SE's profit margins have also improved drastically, with Digital Entertainment adj EBITDA margin of 45.2% (+2.6 points QoQ/ +8.2 YoY) and E-commerce and other services adj EBITDA margin of 12% (-0.5 points QoQ/ +59.4 YoY).

With an overall adj EBITDA margin of 16.4% (-0.2 point QoQ/ +33.9 YoY) in the latest quarter, we believe the drastic correction in its stock prices have been unwarranted indeed.

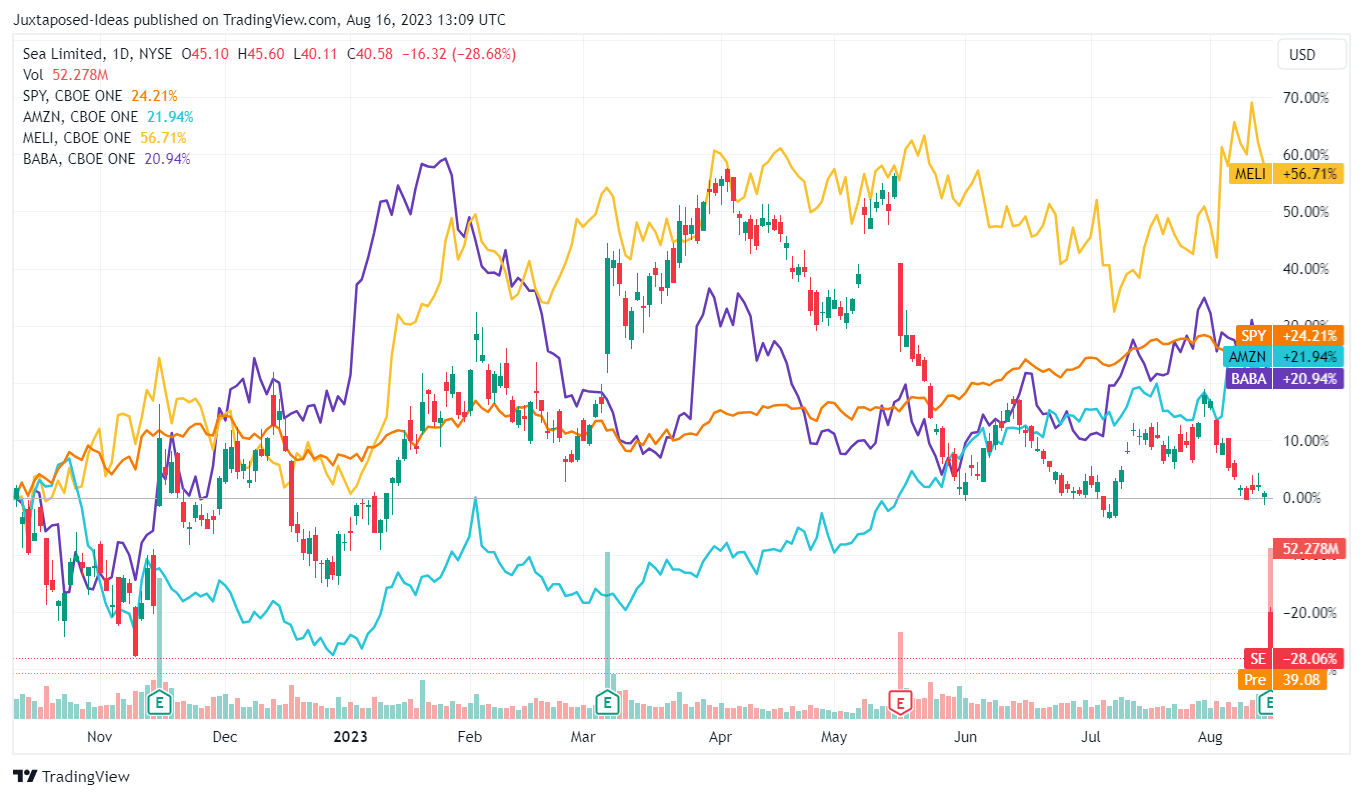

SE Stock Performance Compared To Peers

{kind=link}

This development has unfortunately implied that the SE stock has minimal bullish support, with investors preferring to sell first and think later for two of its recent earnings call.

This is despite the notable improvement in the overall market sentiments since the October 2022 bottom, with many of its e-commerce peers already recording massive stock recoveries.

As a result, SE investors that are looking for quick recoveries must also temper their expectations, with its prospects remaining mixed in the intermediate term.

For example, the Asian Development Bank still expect the Southeast Asia region's inflation to be elevated through 2024 at 3.2%, compared to the pre-pandemic levels of 2.3% . With things likely to normalize only by 2025, we may SE's recovery dampened for a few more quarters, in our opinion.

Shopee Market Share In Southeast Asia

The Financial Times

In addition, while SE may boast the largest market share of 48.1% in 2022 , the company has also warned of a possible impact of intensified marketing costs on its bottom line, due to the intensified competition offered by TikTok ( BDNCE ) and Lazada ( BABA ).

Therefore, we may see its profitability underwhelm from henceforth, potentially impacting its stock valuations and prices at the same time. Investors take note.

So, Is SE Stock A Buy , Sell, or Hold?

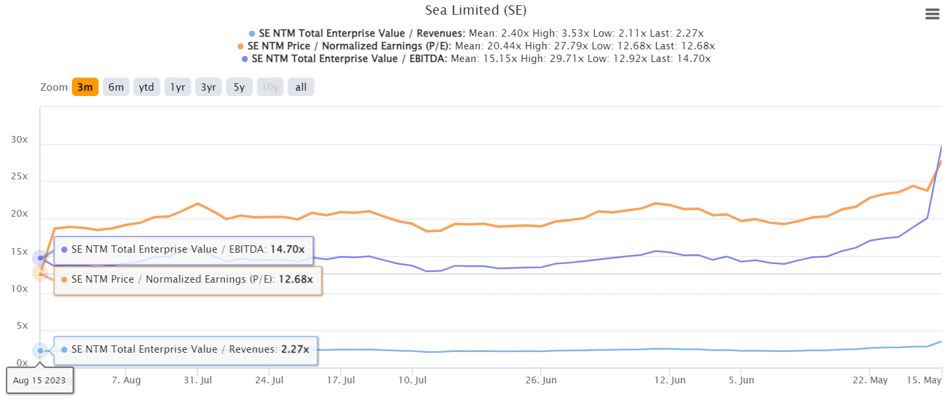

SE 3M EV/Revenue, EV/ EBITDA, and P/E Valuations

{kind=link}

Then again, while SE may not boast a similar operational scale as Amazon ( AMZN ), MercadoLibre ( MELI ), and BABA's Lazada, we suppose the recent sell-off has contributed to the much-needed moderation in its valuations.

For now, SE trades at NTM EV/ Revenues of 2.27x, NTM EV/ EBITDA of 14.70x, and NTM P/E of 12.68x, down from its inflated 1Y mean of -2.47x/ 117.32x/ -7.19x and nearer to its peers' mean of 2.51x/ 14.47x/ 32.76x, respectively.

In our opinion, these valuations are interestingly nearer to its current fair value of $38.66, based on its NTM EV/ EBITDA and annualized FQ2'23 EBITDA per share $2.63.

These levels also offer an improved upside potential to our long-term price target of $89.37, based on its NTM EV/ EBITDA and the market analysts' FY2025 EBITDA per share projection of $6.08.

As a result of the attractive risk reward ratio, we are cautiously optimistic that this bottom may hold. Investors may consider adding the SE stock here, based on its previous March 2020 support levels.

For further details see:

Sea Limited: Pandemic Bottom Is Here - Speculative Buy For The Patient