SE - Sea Limited: Pressure Points Everywhere

2023-12-26 03:43:51 ET

Summary

- Sea Ltd's fundamentals have been pressured by loss of customer engagement in digital entertainment and intensifying competition in online retailing.

- Looking to 2024, I don't see Sea Ltd.'s business momentum shifting sufficiently positive to justify a bullish sentiment pivot.

- Meanwhile, I argue that Sea Ltd.'s one-year forward earnings multiple of approximately 28x won't attract share price support coming from bargain hunters.

- According to my valuation estimate anchored on a residual earnings model, SE stock's fair value may suggest almost 30% downside. "Sell".

Sea Ltd. (SE) holds a dominant positions in quite a few sectors across South East Asia, notably in e-commerce (Shopee), gaming (Garena) and digital lending/ banking (Sea money). However, the company's fundamentals have lately been pressured from loss of customer engagement in digital entertainment, intensifying pressure in online retailing, as well as macro headwinds.

Looking to 2024, I don't see Sea Ltd.'s business momentum shifting sufficiently positive to justify a bullish sentiment pivot. Meanwhile, I argue that Sea Ltd.'s one-year forward earnings multiple of approximately 28x won't attract share price support coming from bargain hunters. In fact, according to my valuation estimate anchored on a residual earnings model, SE stock's fair value may suggest almost 30% downside. "Sell".

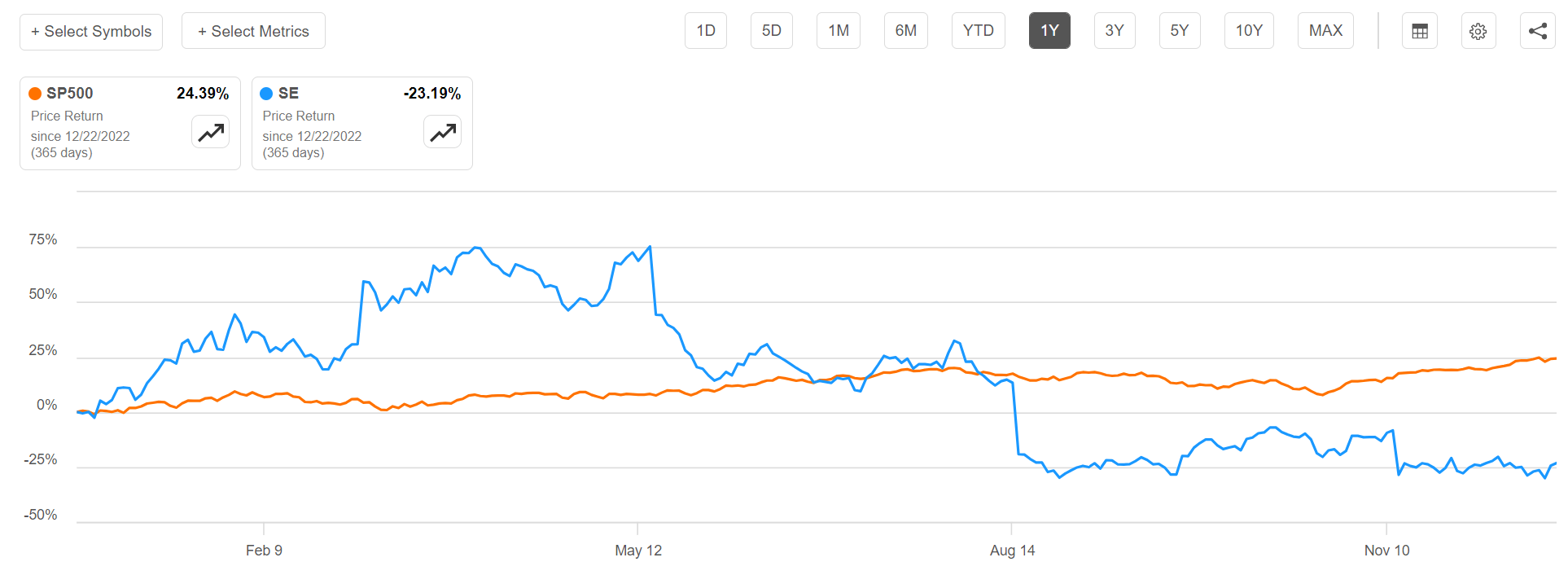

For context, Sea stock performance has lagged behind the broader equities market year-to-date. Since the beginning of the year, SE shares are down about 23%, compared to a gain of approximately 24% for the S&P 500 (SP500).

{kind=link}

Not A High-Growth Story Anymore ...

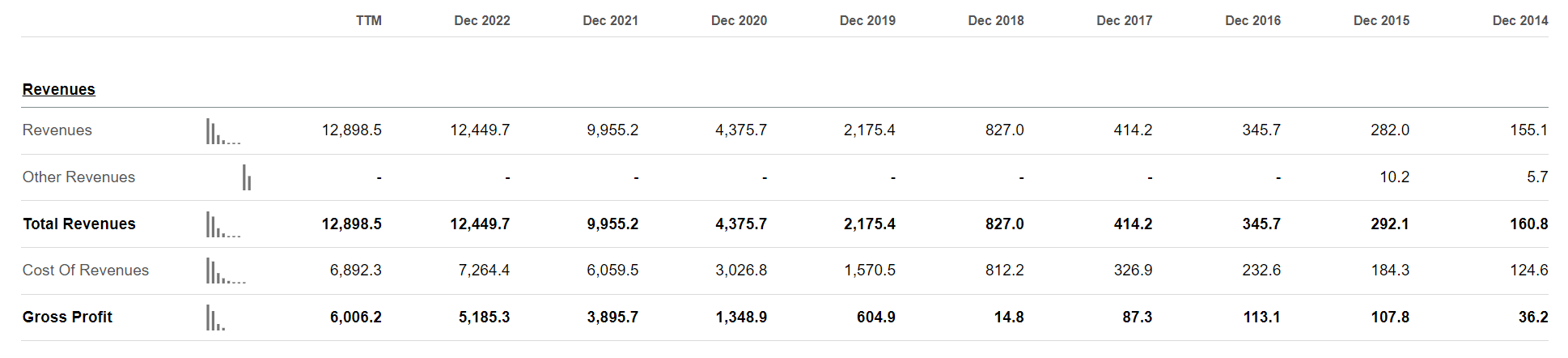

The Sea Ltd. equity story has for a long time offered investors the opportunity to participate in the growth potential provided by one of the world's most promising regions: South East Asia. On that note, I point out that Sea Ltd.'s topline has expanded from $155 million in 2014 to $12,449 million in 2022, a compounded annual growth of approximately 73%. Over the same period, gross profit jumped from $36 million to $6,006 million.

{kind=link}

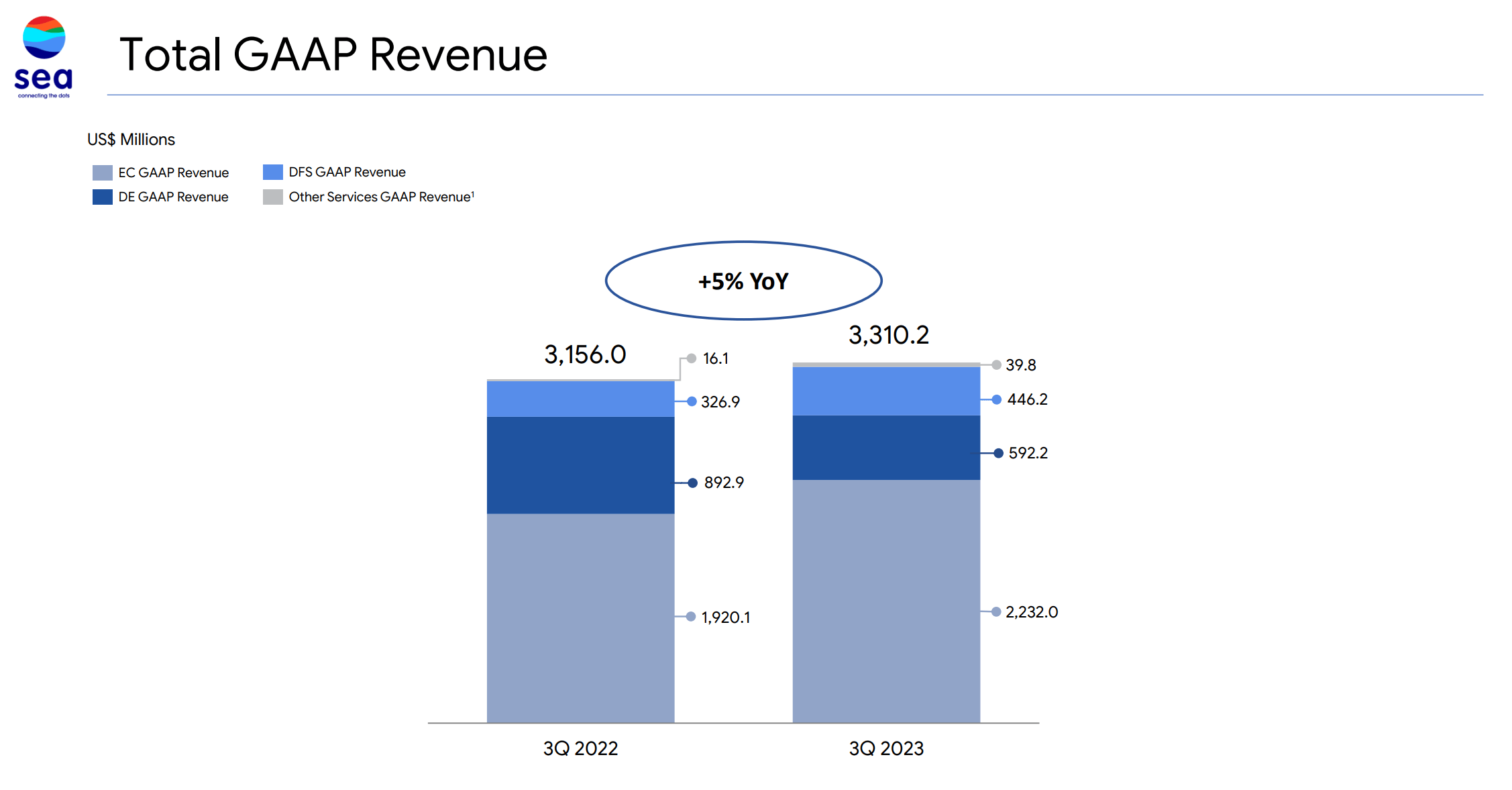

However, Sea Ltd.'s growth slowed sharply in 2023: In fact, in the September quarter the revenue growth fell to about 5% YoY. This growth is now notably below the expansion rate of U.S. tech companies such as Microsoft (MSFT), Google (GOOG) and Amazon (AMZN).

Sea Limited - Q3 2023 reporting

{kind=link}

Admittedly, it may be true that some deceleration in YoY growth may be due to macro pressure, citing globally elevated interest rates and sluggish economic activity in China. Nevertheless, there should also be a structural element embedded in the loss of momentum, as incremental e-commerce penetration uplift in ASEAN countries is now benchmarked against an elevated base.

... While The Wait For E-commerce Profitability Gets Longer

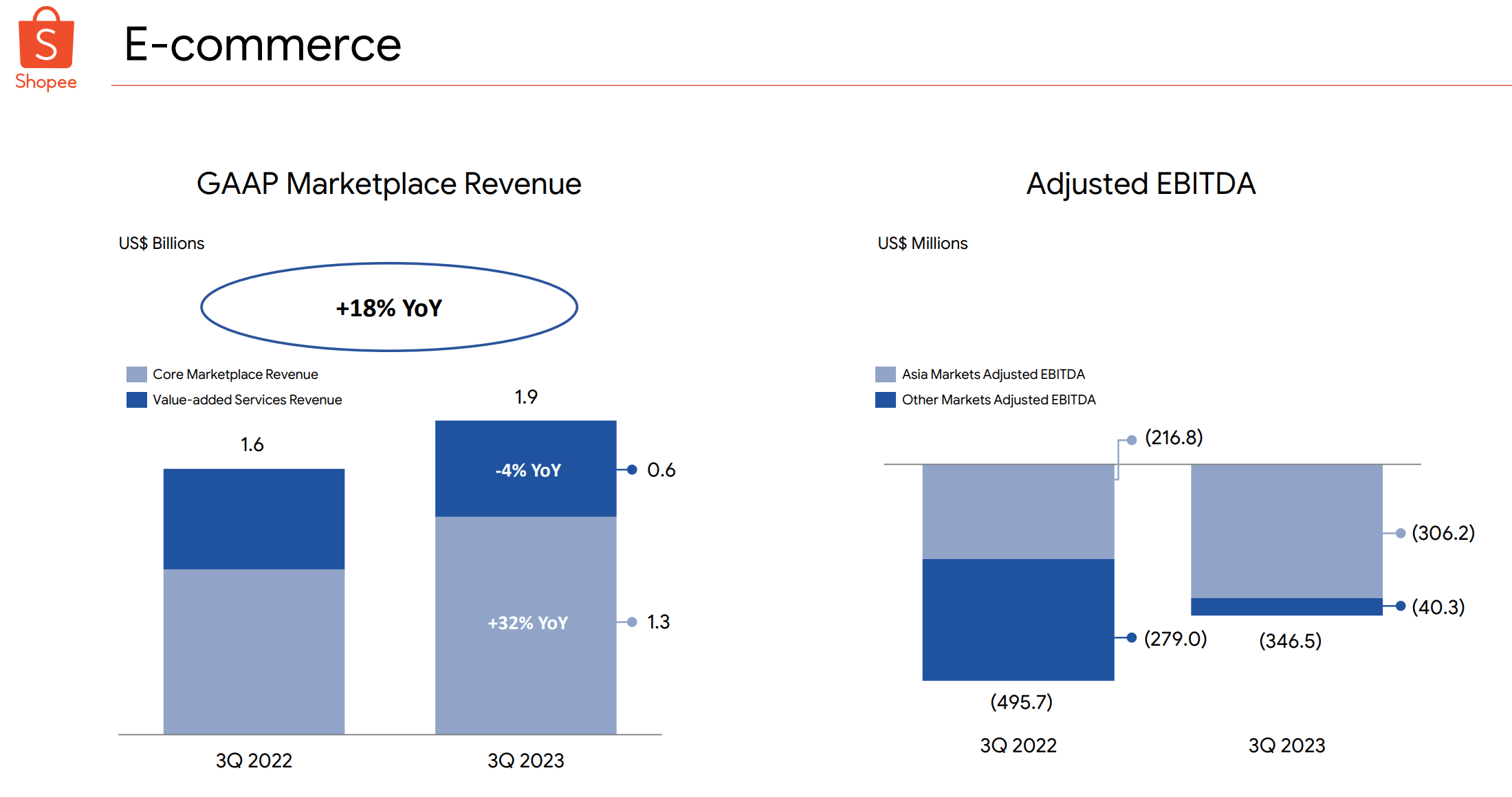

About two thirds of Sea Ltd.'s topline relates to the company's e-commerce business, Shopee. And given the relative importance of this segment, it is quite concerning to note that the segment has historically failed to write positive EBITDA. In fact, in Q3 2023 alone Shopee accumulated close to $350 million of operating losses. In that context, investors should note that Shopee's spending on sales and marketing doubled QoQ for the three months ending September, while the growth in Gross Merchandise Volume didn't match the increased investments.

Sea Limited - Q3 2023 reporting

{kind=link}

While Shopee struggled to generate net positive operating income as of latest Q3, the likelihood of breaking even on profitability in the next few quarters trends lower and lower as competition for ASEAN e-commerce customers intensifies: Less than two weeks ago, Alibaba ( BABA ) increased its investment in Lazada, a direct competitor of Sea Ltd.'s Shopee, by injecting an additional $634 million. This marks Alibaba's third investment this year, totaling over $1.8 billion in Lazada. Meanwhile, Sea Ltd.'s Shopee is also facing competition from TikTok, who invested $1.5 billion investment in a joint venture with Indonesia's GoTo Group. If the deal is approved by Indonesian regulators, TikTok will hold a 75% share in Tokopedia, an ownership share that brings material equity commitment into the competitive landscape for the South East Asian e-commerce market.

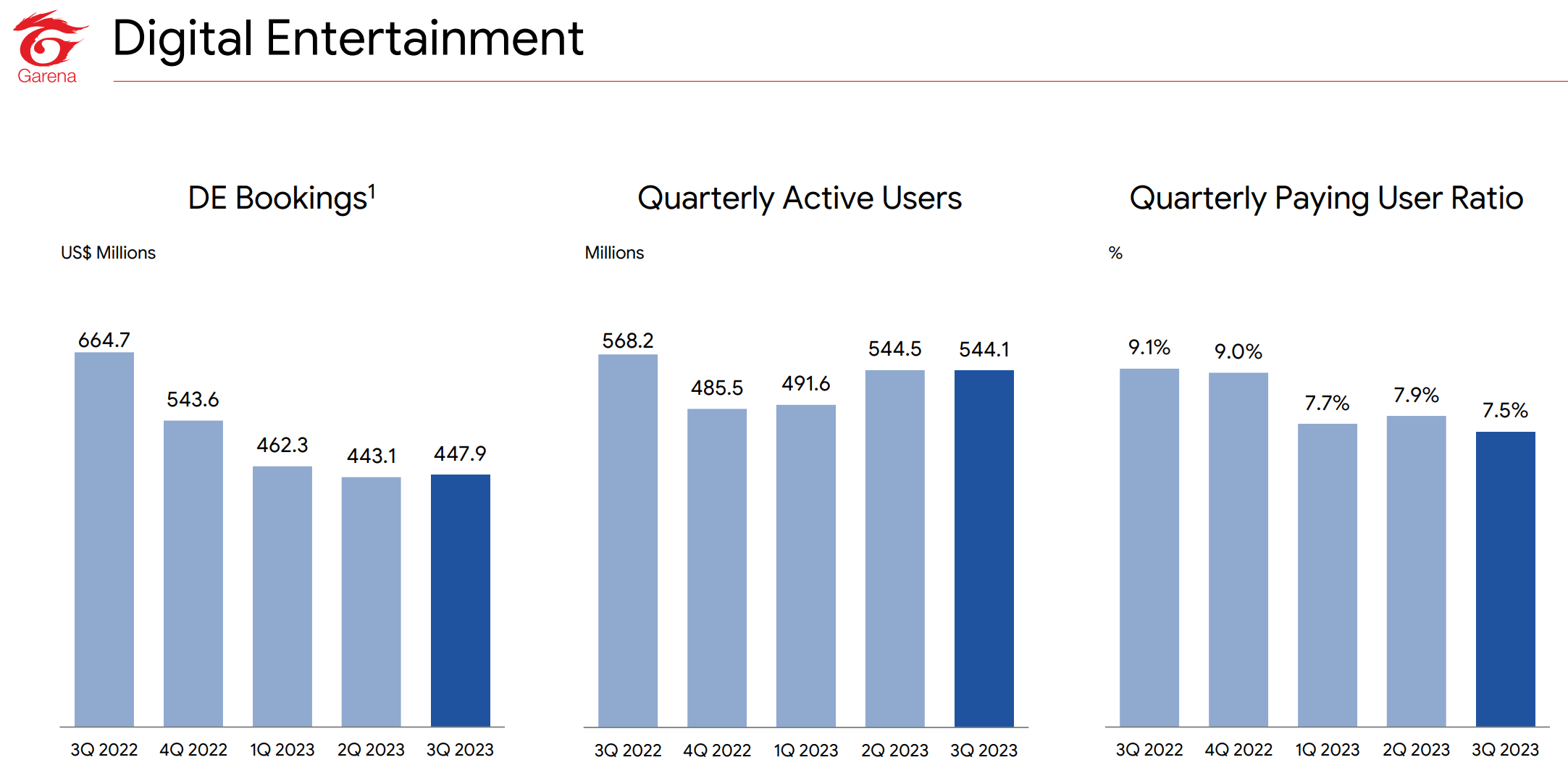

Making things worse for Sea Ltd. still, the company is also facing fading customer engagement in the company's Digital Entertainment business (Garena). Although this segment accounts for slightly less than 20% of topline as of Q3, Garena generated the lion share of operating income -- generating $234 million of EBITDA in the September quarter. That said, I point out that Sea Ltd.'s Digital Entertainment business has suffered strong negative momentum multiple quarters in a row, with bookings trending down from $664 million in Q3 2022 to $448 million in Q3 2023 (-32% YoY). Again, the fading momentum may be partly explained by a structural element; specifically, Sea Ltd.'s Garena has failed to create a blockbuster game comparable to Free Fire, a mobile game that was released more than 5 years ago, in 2017, and may be slowly losing its appeal.

Sea Limited - Q3 2023 reporting

{kind=link}

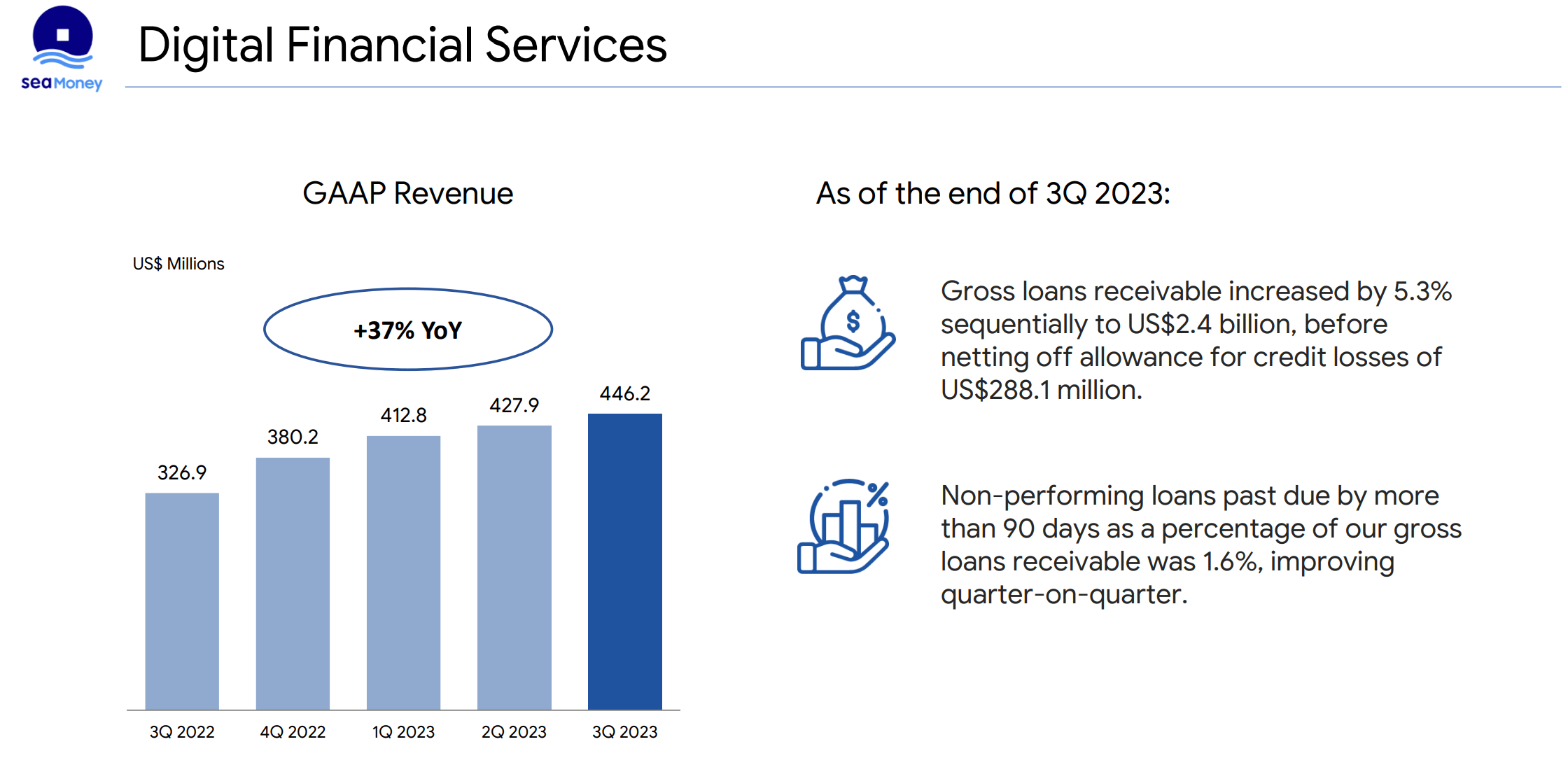

The best business traction for Sea Ltd's segments is seen in the company's Digital Financial Services arm, a segment that has shown a consistent high-growth pattern over the past few quarters. However, banking is a notoriously difficult business to penetrate due to stringent regulations and compliance requirements, as well as competitive pressure from both established (e.g., HSBC, DBS) and emerging market players (e.g., Grab). Moreover, Sea Ltd.'s financial services business is the smallest segment of the group's operating units and good momentum here may not be sufficient to offset pressure in the other units.

Sea Limited - Q3 2023 reporting

{kind=link}

Valuation: Set TP At $27/Share

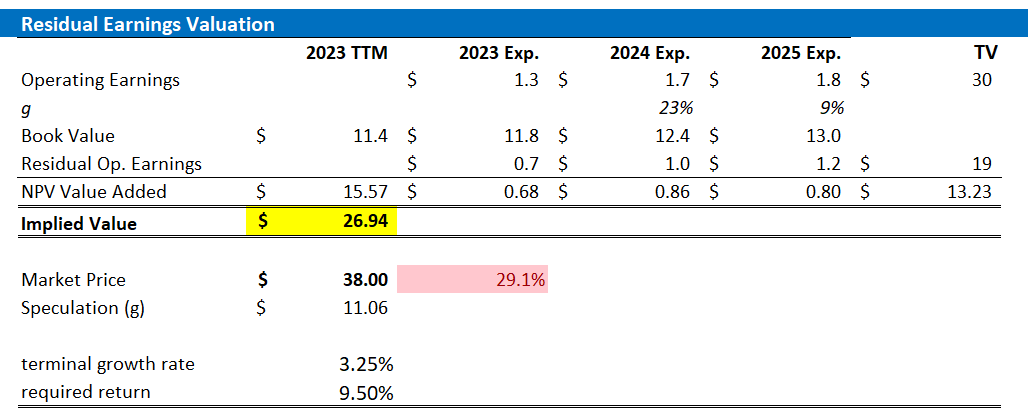

To value Sea Ltd. stock, I suggest using a residual earnings model, which anchors on the idea that a valuation should equal a business' discounted future earnings after capital charge. As per the CFA Institute :

Conceptually, residual income is net income less a charge (deduction) for common shareholders' opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company's capital.

With regard to my Sea Ltd. stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal till 2026. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor on Sea Ltd.'s cost of equity at 9.5%, which is approximately in line with the CAPM framework.

- For the terminal growth rate after 2025, I apply 3.25%, which is about 50-75 basis points above the estimated nominal global GDP growth. The growth premium should reflect the elevated growth potential of the ASEAN region.

Given the above assumptions, I calculate a base-case target price for SE stock equal to $26.94/share.

Analyst Consensus; Company Financials; Author's Calculations

{kind=link}

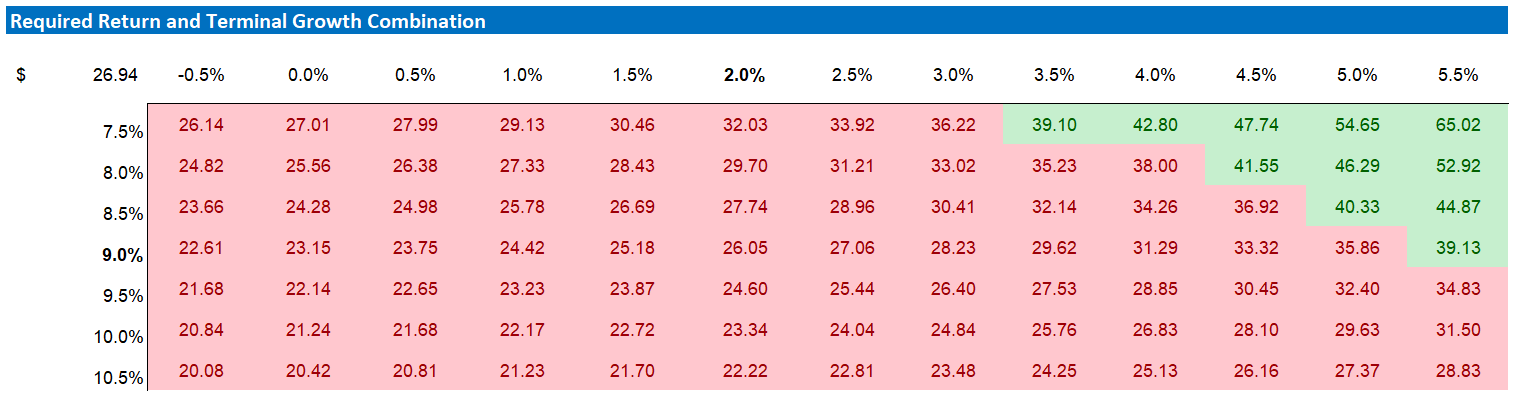

As I argued that my estimates for growth and equity charges may be conservative, I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I've included a sensitivity table to test different scenarios and assumptions. See below.

Analyst Consensus; Company Financials; Author's Calculations

{kind=link}

Upside Risk To The Thesis

In my opinion, faster than expected EBITDA expansion in the e-commerce segment would be the major upside catalyst for SE's share price. On that note, I view the (currently farfetched) possibility of fading competition and consolidation in the ASEAN e-commerce sector as the likely key driving factor for this. Moreover, I point out that an expanding topline in Sea Ltd's game-centric segment Garena would likely be highly accretive for the group's operating income. But to stimulate a turnaround in momentum, Garena would likely need to hit it big with a new blockbuster game.

Investor Takeaway

Sea Ltd. faces challenges as its core fundamentals feel the strain from reduced customer engagement in digital entertainment and escalating competition in the online retail sector. In that context, there are currently no clear indications that suggest a significant shift in Sea Ltd.'s business trajectory that would warrant a shift towards bullish sentiment. Based on my valuation using a residual earnings model, it appears that SE stock might imply a downside of nearly 30%. My recommendation: "Sell."

For further details see:

Sea Limited: Pressure Points Everywhere