SE - Sea Limited: Q2 Earnings Not As Bad As It Looks A Buying Opportunity

2023-08-22 02:18:07 ET

Summary

- Sea Limited stock dropped by almost 29% following the release of its 2Q23 earnings report.

- The drop was caused by poor results from Garena and concerns about the impact of efforts to reaccelerate growth on Shopee's bottom line.

- Despite the drop, SE presents a buying opportunity at a cheaper price.

Recap

Following the release of the 2Q23 earnings report, Sea Limited's stock ( SE ) dropped by almost 29%. The current stock, now at $39/share, is trading around its 52-week low and COVID low. This was caused by two main reasons: 1) beaten-down Garena's results and 2) the plan to 'reaccelerate' growth, an effort that possibly leads Shopee's bottom line to take a hit. Read our previous coverage here.

Revenue grew only 5% (Y/Y) in 2Q23 due to disappointing results from Garena and the recent strategic pivot that have led the market view on the stock pessimistically. Yet, we believe the latest drop presents an opportunity to buy at a much cheaper price. Here is why.

SE quarterly earnings results (Company, Vektor Research)

The Gaming Business Suffered, but the Decline Softened

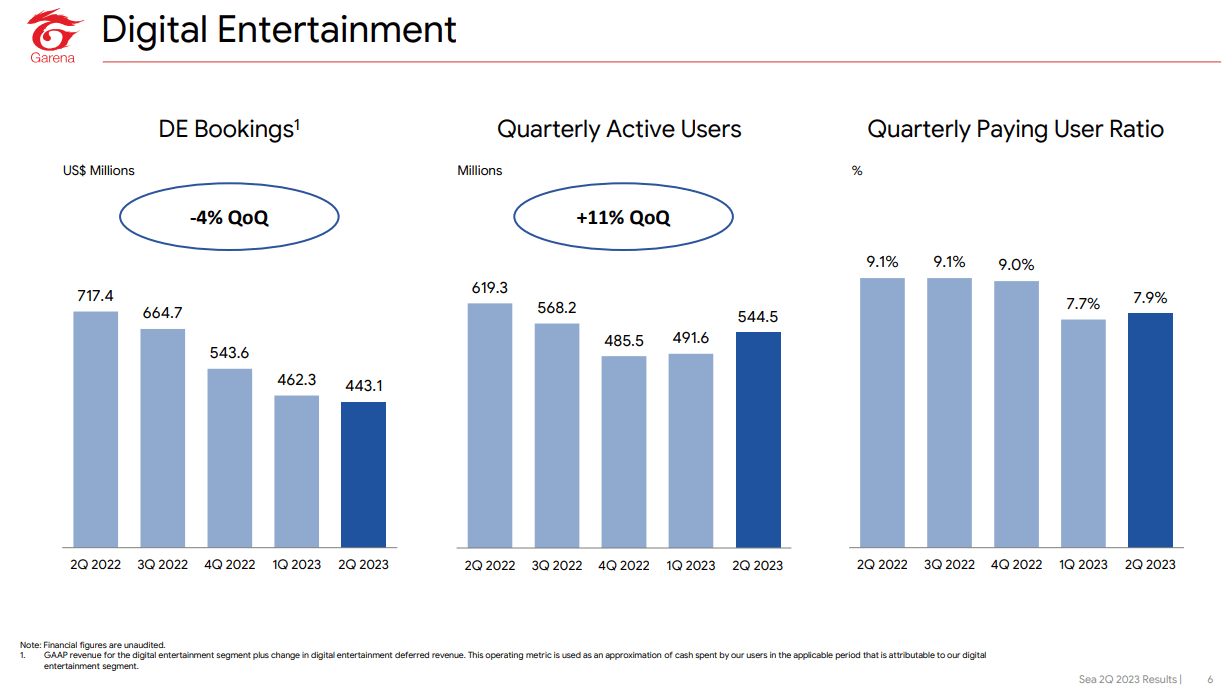

Revenue from digital entertainment business dropped 41% (Y/Y), dragging down the group top-line growth to 2% (Q/Q) and 5% (Y/Y). Bookings were down 38% (Y/Y). However, if we look at the numbers more closely, Garena's revenue appears normalizing at a 2% (Q/Q) decline.

Digital Entertainment revenue (Company, Vektor Research)

Additionally, bookings were down 15% (Q/Q) in 1Q23, and in 2Q23, it was only a 4% (Q/Q) decline. Meanwhile, quarterly active users (QAU) were up 11% (Q/Q), and paying users improved to 7.9% of total QAU. The management also noted that Free Fire's bookings went up quarter-on-quarter for the first time in the last seven quarters, and as a result, drove Garena's EBITDA margin as Free Fire has higher margins.

Garena operational metrics (Company) Garena's margins (Vektor Research)

{kind=link}

How about Sea Limited's cash flows? Isn't Garena a cash-cow business? Despite soft Garena's results, the company still generated almost $600 million operating cash flow during the quarter, roughly flattish quarter-on-quarter but significantly better than last year, during which the company was losing money. According to our calculation, post share-based compensation free cash flow was $384 million in 2Q23, which implies an FCF margin of 12% vs. 10% in 1Q23.

Sea's post-SBC FCF ($ million) (Company)

When asked whether "the worst is over for Free Fire," the management was seemingly unsure whether "this is the beginning of a long-term stabilization." Yet, despite uncertainties, further decline will have smaller impact on the group as a whole. A year ago, Garena made up of 31% of Sea's revenue. Now, it is 17%.

Pivoting from Profitability to Growth

On the e-commerce side, revenue was up 21% (Y/Y), but quarter-on-quarter growth was only 2%, although gross order grew more than 10% (Q/Q). Core marketplace revenue, which includes transaction-based fees and advertising revenue, increased 38% (Y/Y), and it grew 7% (Q/Q) thanks to "improved monetization."

However, the market still punished the stock due to the company's strategy to pivot from sustaining its profitability to investing in growth. First, the company is ramping up the shipping subsidies program, which in turn, impacted value-added service revenue, which declined 7% (Q/Q). Second, content-based e-commerce remains the key focus as it has generated the much-desired growth. The management said during the 2Q23 earnings call :

Indeed, during July's [7.7] live streaming focused campaign in Indonesia, we recorded a 12x growth in transaction volume and a 10x increase in the number of buyers during the campaign, as compared to a normal day. For the [8.8] shopping campaign, around one quarter of our Indonesian buyers watched live streams on Shopee Live and made close to 5 million orders in a single day. In fact, Shopee has already become the leading live streaming e-commerce platform in Indonesia based on a report by Populix.

But we believe this partly resulted in increased sales & marketing expenses: expenses were 21% of revenue in 2Q23, up from 16% in 1Q23, but still lower than 39% in 2Q22. E-commerce's EBIT margin shrank to 3% from 5% to 6% in the previous quarters.

S&M expenses as a % of revenue (Vektor Research)

Worse, the management said these initiatives could impact Shopee's bottom line and turn the business into a loss again. Please note that what drove the stock price recently was the fact that Shopee turned profitable for the first time. So, what are the reasons behind this strategic change? Here is what the management said:

I think also looking at the financial position we have achieved and the resources we have, overall, we think we are in a much stronger position and a much stronger footing now to refocus on growth.

And more importantly, we also see new opportunities for growth, in particularly relating to live streaming as well as e-commerce related to -- with video content.

Our take is that besides how quickly Sea can turn profitable, the other reason is that Sea is defending its market share from TikTok. Through its survey on consumers in Thailand, the Philippines, and Indonesia, Cube Asia found that 51% of consumers spending on TikTok spent less on Shopee. Our view is that because TikTok's consumer segmentation is closer to Shopee than to, for example, Tokopedia. In the recent earnings call, CEO of Tokopedia said :

I also would like to mention that there are two types of E-commerce. The first one is traditional E-commerce with search-based product discovery. The second one is E-commerce focusing on content-based business utilizing live streaming to drive transactions, especially in the area of impulsive transactions. So far, we have been focusing a lot on our core strength and capabilities in traditional commerce.

As things stand, TikTok is still giving out free delivery promotions, per our writing. But we have written these in our previous articles:

Our view is that while the industry is more rational, things could change quickly as new players enter the market with aggressive promotions and discounts. Existing players are likely to walk the same path to protect market share at the expense of possibly margin erosions, in our view.

Our take is that aggressive moves from TikTok are likely to force established e-commerce players, including Shopee, to do more promotions and discounts to defend market share.

But at some point in the future, players should be cutting back subsidies and pursuing profitability, as we have seen previously. So, how quickly can Sea turn profitable once again? First, we need to look at how the company did it. As cited in the 4Q22 earnings call transcript :

We exited the markets, we downsized operations, we walked through all these initiatives to decide which is core, which is less core, what we need to prioritize and what we need to deprioritize.

GAAP sales and marketing expenses improved by 34% quarter-on-quarter and 55% year-on-year driven by more targeted investments across shipping incentives and brand marketing. There were also sequential improvements in R&D and G&A expenses

So, Sea Limited not only downsized its workforces to achieve profitability but also de-prioritized non core-markets, as well as cut back incentives and sales and marketing expenses. And now it is pursuing growth through free shipping subsidies, a strategy that, in our view, is much easier to pivot from compared to the other two options.

On the other hand, despite the threat of competition, Shopee still holds the biggest market share in Southeast Asia. According to data by Similarweb, Shopee held 30% to 50% of traffic share, with the second place going to Lazada with 10% to 30% in the last three months, as cited in CNBC on May 2023.

Furthermore, Snapcart's survey on 1,000 respondents in Indonesia earlier this year revealed that Shopee led in four different categories: Brand Use Most Often (61%), Top of Mind (70%), Transaction Volume Market Share (51%), and Transaction Value Market Share (46%), as cited in Marketeers . Perhaps the more interesting part is that 71% of respondents picked free shipment as a key consideration for buying online during the Holy Month of Ramadan, and 62% of respondents agreed that Shopee offered the best free shipping promotion.

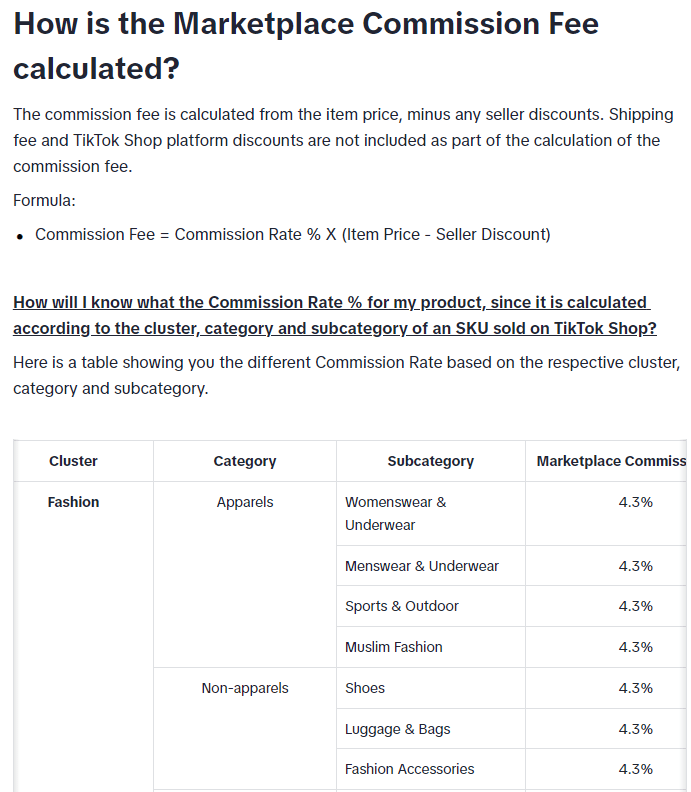

Yet, TikTok is not only giving out free delivery service, but also adjusting its marketplace fees for sellers. As of June 2023, the maximum rate is 4.3% of a product's selling price after discount, based on category. Previously, it was 1% plus a flat fee, which would be substantial for cheaper products. For Shopee sellers , total maximum fee is 10% if they participate in all programs (free shipping, cashback, and Star programs). But they could keep it as low as 4% for a regular administrations fee.

TikTok Commission Fee (TikTok)

{kind=link}

We acknowledge that the threat of competition remains the biggest risk in investing in e-commerce, especially in a low barriers to entry landscape. Nevertheless, as mentioned before, at some point they will revert to pursuing profitability. Aggressively giving out subsidies will put pressure on the bottom-line, and continuously increasing the take rate is not sustainable.

Yet, the important point is to reduce costs per customer served, and this always has been Sea's long-term focus. For instance, the company recently added 600 collection points in Singapore to provide consumers with more delivery options, as well as installed lockers at 150 convenience stores in Taiwan.

Additionally, contribution margin loss per order in Brazil narrowed to $0.24, improved from a loss of $0.34 in 1Q23 and significantly better than a $1.42 loss last year. Sea has invested in distribution and sorting centers, as well as expanded first and last mile hubs.

…we have been highly focused on reducing our ecosystem's cost to serve and improving the user experience for both our buyers and sellers. During the second quarter we made important progress on both fronts. In the quarter, we further improved the efficiency of our logistics operations and expanded our network and capabilities across our markets.

Looking ahead, as we reaccelerate investments in growth, our strategic focus to build cost leadership and continually improve user experience remains key to our long-term success.

Lastly, digital financial service reported a top-line growth rate of 53% (Y/Y) and 4% (Q/Q), as the company is looking to expand its product offerings and further integrate SeaMoney with Shopee. We believe that our thesis is still playing out: the proliferation of e-wallet adoption and large underbanked and unbanked population will drive Sea's fintech growth. Non-performing loans remained at 2% of gross loans receivable.

Valuation

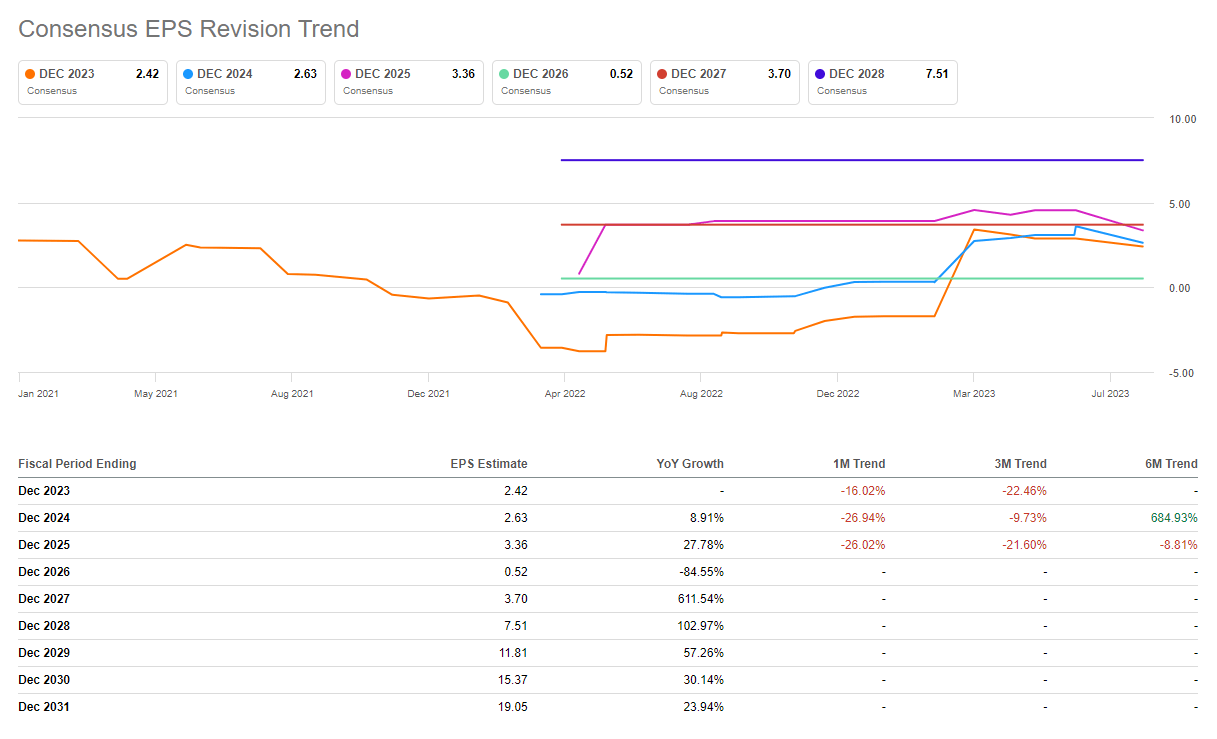

After shares plunged to their 52-week low and COVID low, Sea Limited's stock is now trading at 16x of its forward P/E and less than 2x of its forward sales. The market is more conservative on earnings outlook as a result of the strategic pivot.

Consensus EPS revision (Seeking Alpha)

{kind=link}

But what is the growth outlook? E-commerce in Southeast Asia and Latin America markets is still under-penetrated, as research from McKinsey and data from Statista suggest. In Indonesia, GOTO's management (Tokopedia's parent company) spoke during the recent earnings call:

If we look at the penetration of E-commerce in Indonesia compared to China, we are only half of the rate of the penetration. And in terms of frequency, we are one-third off what Chinese consumers are consuming today. So the market is still wide open.

With increased competition from TikTok, we believe that the company's "investment" in free shipping subsidies is to protect market share. Despite that, the company still holds the biggest market share in the Southeast Asia market, maintains profitability at the group level (9% EBIT margin in 2Q23), and generates positive free cash flow.

The tepid 5% top-line growth was overshadowed by soft Garena's results and higher shipping subsidies that reduced the value-added service revenue. Continuing investment in logistics remain the long-term priority for the company despite the recent strategic pivot. Our fair value estimate is $88/share (128% upside). Therefore, we maintain our bullish view on Sea.

For further details see:

Sea Limited: Q2 Earnings, Not As Bad As It Looks, A Buying Opportunity