SE - Sea Limited: Q3 2023 Earnings Shopee's Return To Loss But Still A Buy

2023-11-21 03:20:59 ET

Summary

- Sea Limited's stock experienced a significant drop following the 3Q23 earnings release. But we still believe the stock is a buy.

- Garena, Sea's gaming division, saw a year-on-year decline in revenue but finally showed growth in average bookings per user. The relaunch of Free Fire India was postponed.

- Shopee returned to a loss-making business. But this move is required to gain market share, especially as TikTok Shop was banned in Indonesia. In addition, unit economics in Brazil improved.

- SeaMoney delivered a robust 37% top-line growth, while maintaining its credit quality. The NPL ratio more than 90 days improved to 1.6% from 2%.

- Forward P/E is 15x based on 2025F earnings. Risks include massive spending on S&M continuing to 4Q23 and TikTok Shop to re-enter the e-commerce space.

Recap

After our previous publication on Sea Limited ( SE ), the stock went up and briefly reached $47 per share. This surge was mainly due to the closure of one of its toughest competitors, TikTok Shop, in Indonesia. Previously, the stock was beaten down because the company shifted its strategy from profitability to growth, but we view that this move is required to defend its market share. Yet, the market was once again disappointed by the 3Q23 earnings release, punishing the stock over 22% in a single day. However, we maintain our view that the stock is a buy at the current price.

SE earnings summary (Company, Vektor Research)

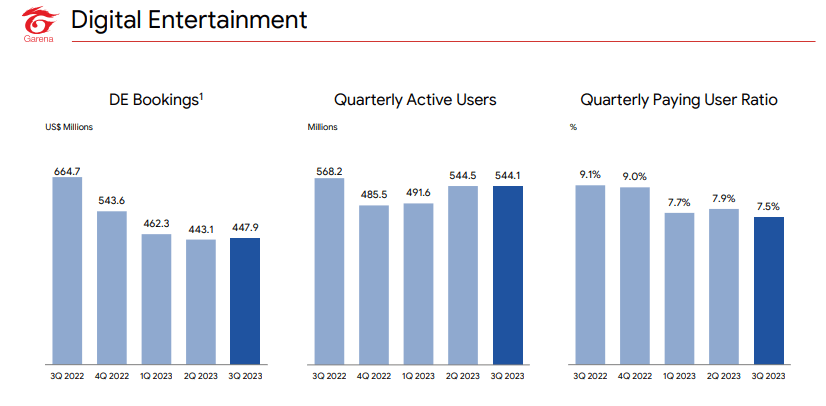

Garena: Bookings Grew for the First Time in Seven Quarters

At the group level, revenue only advanced by nearly 5% (Y/Y), primarily due to a 34% (Y/Y) decline in Garena. However, it is worth noting that the decline in Garena’s revenue has narrowed compared to the previous quarters. Moreover, on a quarter-to-quarter basis, revenue increased by almost 12%.

In 2Q23, quarterly active users (QAU) and quarterly paying user ratio (QPU) were promising, but in the following quarter, QAU was flat and, and there was even a decline in QPU. The management attributed such decline to school reopening and less holidays.

Nevertheless, average bookings per user increased by 1% (Q/Q), marking the first rise since 3Q22. And this was before the widely anticipated relaunch of Free Fire India, which was postponed for “a few more weeks” from its initially scheduled date in early September. According to Sensor Tower, Free Fire is the most downloaded mobile game worldwide in September.

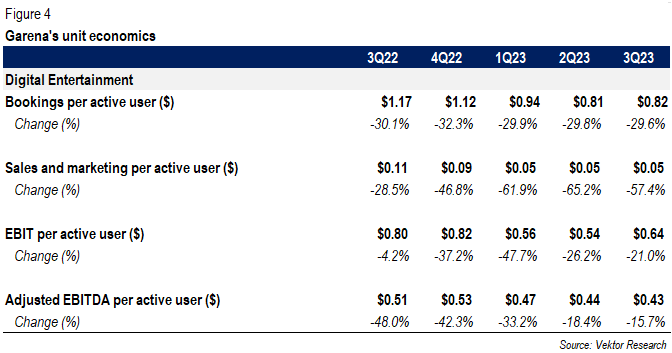

Garena key metrics (Company) Garena' unit economics (Vektor Research)

{kind=link}

{kind=link}

All in all, although it remains to be seen when the relaunch is taking place, we view that Garena’s numbers have already been relatively solid. EBIT margin was 58%, and adjusted EBITDA margin was nearly 40%. In addition, Garena remains Sea’s cash-cow business. During the quarter, Sea's post-SBC free cash flow was $381 million, roughly flat quarter-on-quarter, but up by nearly $1 billion from a year before, despite Shopee’s massive spending in sales and marketing.

Shopee: Laying Out the Rationale Behind the Strategic Shift From Profitability to Growth

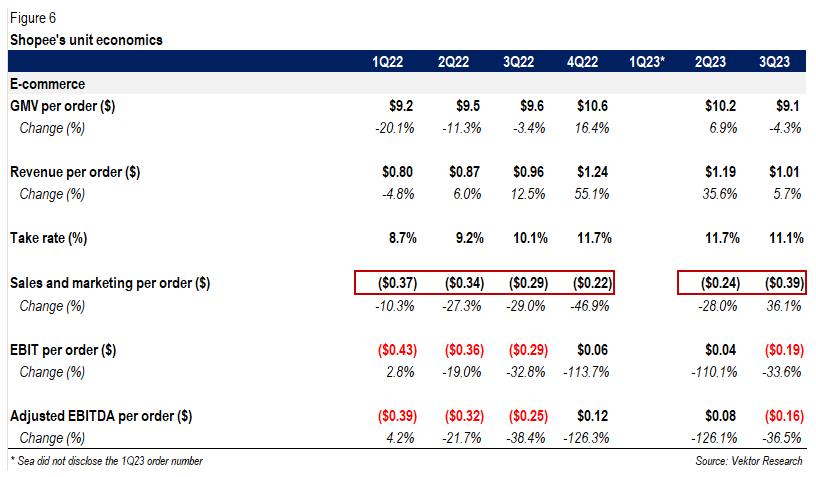

Shopee revenue grew 16% (Y/Y) and 6% (Q/Q). Core marketplace revenue advanced by 32% (Y/Y), while revenue from value-added services retreated by 4% (Y/Y). This was caused by passed-on cost savings resulting from lower logistics costs in Asia markets and free shipping subsidies, as mentioned in 2Q23 earnings call .

Shopee's revenue growth breakdown (Company)

Nevertheless, in 3Q23, e-commerce sales and marketing expenses nearly doubled compared to the previous quarter. This was because Sea shifted its strategy from a focus on profitability to growth. On a per-order basis, sales and marketing expenses was the highest in seven quarters, leading to a $0.19 operating loss per order for the quarter. Additionally, despite significant spending, GMV growth was only at 5% (Y/Y). It is worth noting that Sea has decided to disclose its e-commerce quarterly metrics once again.

Shopee's unit economics (Company)

{kind=link}

However, it is essential to focus on the rationale behind the management’s decision to pivot from profitability to growth. First, the management cited a robust cash position and the ability to swiftly achieve profitability, as the company demonstrated just a few quarters ago. As we wrote in our last article :

So, Sea Limited not only downsized its workforces to achieve profitability but also de-prioritized non core-markets, as well as cut back incentives and sales and marketing expenses. And now it is pursuing growth through free shipping subsidies, a strategy that, in our view, is much easier to pivot from compared to the other two options.

Sea boasted over $7.5 billion in short-term cash and cash equivalents ($7.9 billion including other treasury investments classified as long-term investments), further reinforced by the practice of investing billions of dollars in securities using the free cash flows they generated. The decision not to invest heavily in capital expenditure was explained by the management: Sea’s logistics model is not Capex-heavy. Instead, the strategy involves building small sorting centers to cover broader areas.

We're not looking to build mega warehouses or mega machinery type of logistics in that model. Our model is more about building a large network of small sorting centers, small hubs into many, many neighborhoods, and also build a team capability to expand our last mile coverage across a wider network of areas covered by us.

So it's more OpEx. And for the past few years, we have already been consistently investing in logistics, which is one of the key reasons that has got us to the current position of continue to reduce the logistic shipping fees and also a key competitive advantage that we have.

Second, the heightened competition from TikTok Shop has rendered the company to take a more aggressive stance. As cited in our previous article, a study suggests that the biggest customer shift towards TikTok Shop originated from Shopee. Similarities in the market segmentation might help explain this trend, leaving Shopee had no alternative but to defend its market share. The management emphasized the importance of maintaining leadership in market share:

But as we shared in the Q3, we observed that even with -- even in the market with the higher competition, we are able to gain market shares. The key is investment efficiencies. This is what allows us to gain market share while having better economics , unit economics than our peers , competitors in our market. The key for that is our competitive advantage we have built over the past many years. I think number one, if you think about this, will be scale . As a clear market leader, we have a bigger scale that translate to a much better monetization capabilities and also better cost efficiencies , of course.

In addition, the ban on TikTok Shop should act as a tailwind for GMV growth in the fourth quarter. According to Momentum Works, TikTok Shop held an estimated 5% market share in Indonesia in 2022, equating to approximately $2.6 billion in GMV. The share figure is likely to have increased since then. Hence, assuming a 10% market share would result in an estimated GMV of at least $5 billion, all things equal. That is equivalent to 7% of Shopee’s annual GMV.

Nevertheless, we believe that other players are also keen on defending their market share. GoTo CEO emphasized on the 3Q23 earnings call the importance of maintaining “tactical flexibility to preserve our GTV healthiness,” considering a previous focus on profitability that led to a market share loss. Although Tokopedia GTV was down 11% (Y/Y), it saw a 6% quarter-on-quarter growth due to increased marketing efforts and reduced platform fees. We believe that competition will intensify in the fourth quarter, as this period historically proves robust due to holiday season. Shopee raked in over $1 billion GMV during the 11/11 promotional period.

Tokopedia GTV growth (GoTo)

When asked about when spending will begin to normalize, Sea’s management expressed a commitment to being “nimble and flexible,” adjusting their approach based on “market conditions.” Yet, in contrast to the deterioration of unit economics in Asian markets, we note a gradual improvement in unit economics in the Brazilian market. The contribution margin loss per order was $0.1, an improvement from $0.24 per order in the previous quarter and slightly above $1 per order a year ago.

Only if timing and opportunity align, the company will be aggressive to seize market share. Therefore, our guess is that elevated marketing spending will likely persist into the fourth quarter, given the intensified competition and the company’s strategy to balance between market share gain and profitability. But sooner or later, they are likely to revert to a profitable state once again, in our view.

Contribution margin loss in Brazil (Company)

However, it is important to consider the possibility that TikTok Shop will not be completely out of the picture for an extended period. The ban currently prohibits the operation of social media and e-commerce within the same platform. So, there is a chance that TikTok Shop will re-enter the competitive landscape as a separate entity from its social media platform. Thus, we view Sea’s strategy to aggressively seize market share as fitting given the circumstances.

Finally, Shopee is ramping up its investment in live streaming, focusing on high-margin categories such as fashion, health, and beauty. Again, the rationale behind this strategic move is understandable, given the size of the market. According to the management, 20% of average daily active users in Indonesia engaged in live streaming in October. In Southeast Asia, the average daily orders on Shopee Live accounted for 10% of the total order volume in October. Looking forward, the management believes that live streaming will make up 20% to 30% of total GMV in Indonesia.

Shopee continues to maintain its leadership in the Indonesian live streaming shopping market. A survey conducted by Snapcart suggests that 57% of the respondents in Indonesia picked e-commerce as their primary platform for engaging in live streaming. Indeed, the recent ban on TikTok Shop, which held a significant market share among social media platforms for live streaming, paves the way for Shopee to solidify its dominant position.

In the meantime, Tokopedia has expressed interests for a partnership in live shopping space. But they still emphasized their commitment to maintain their core identity as a search-based e-commerce platform. As cited in the 3Q23 earnings transcript :

I think we will continue to be an E-commerce platform where people come with an intention to purchase. We are not coming from a platform with the DNA of content creation or live streaming , if you will. So we have a lot of things to catch up to be able to offer a similar or close to similar experience for people who are more accustomed to this type of experience on different platforms.

SeaMoney: Robust Growth Without A Deterioration in Credit Quality

Lastly, SeaMoney reported a robust 37% (Y/Y) revenue growth. Although gross loans receivable continued to grow (+5.3% Y/Y), non-performing loans more than 90 days as a percentage of revenue improved to 1.6%, compared to its historical average of around 2%. In the fourth quarter 2022, the NPL ratio, without the shortened loan write-off period, would have been 5%, up from less than 4%. But the company managed to keep the NPL ratio stable afterwards.

Looking forward, the management expressed confidence that the current credit quality is sustainable and anticipates loan growth without compromising quality. Additionally, the company is actively expanding its third-party funding source for its credit business.

Allowance for credit losses as a % of gross loan receivable (Company)

Conclusion

We believe the stock is a buy at 15 times of its 2025 earnings, especially with its cash and cash equivalents around 35% of its market capitalization. The last time the stock traded below $40, Sea was still operating at a loss. Since then, they have taken measures to cut excess fat such as downsizing and de-prioritizing non-core markets. We believe that offering subsidies is a strategy that is much easier to pivot from compared to the other two mentioned alternatives.

We conclude that there is no significant deterioration in fundamentals. First, several key metrics might have been disappointing, but average bookings per user have finally shown growth since 3Q22. In addition, we have not seen the impact of Free Fire India relaunch. Second, while Shopee is in a growth-seeking phase again, it is essential for them to gain market share, especially post TikTok Shop ban. Shopee remains the market leader in Southeast Asia. Furthermore, unit economics in Brazil showed a gradual improvement. Lastly, we believe that our thesis on Sea’s financial services remains intact, given the substantial underbanked and unbanked populations. The NPL ratio improved during the quarter.

However, it is likely that Shopee will continue its spending in sales and marketing in the fourth quarter, especially as the competitive landscape intensifies. Moreover, it is also possible that TikTok Shop will re-enter the competitive landscape as a separate entity from its social media platform. Therefore, we view the company's strategy to seize market share as fitting. Our fair value estimate is $88 per share. Maintain BUY. If you have any thoughts, please do not hesitate to comment below.

For further details see:

Sea Limited: Q3 2023 Earnings, Shopee's Return To Loss, But Still A Buy