SE - Sea Limited Q3 Deep Analysis: Adrift At Sea The Future Looks Bleak

2023-11-22 13:35:23 ET

Summary

- Sea Limited's Q3 2023 earnings reveal ongoing challenges, with persistent losses in its e-commerce division and operational instability.

- The company's heavy investment in market share raises concerns about the long-term viability of its profitability model.

- Intensified competition and external factors add to Sea Limited's woes, making sustainable profitability difficult to achieve.

- The above sector valuation metrics make the stock a sell in my opinion.

Investment Thesis

Sea Limited's ( SE ) Q3 2023 earnings reveal significant financial and operational challenges, marked by persistent losses in its e-commerce division. The company's strategy, focused on heavy investment in market share during peak shopping seasons, highlights its reliance on future growth amidst current unprofitability. This approach raises concerns about the long-term viability of its profitability model, especially given the intensified competition in key markets like Southeast Asia.

The emergence of new competitors such as GoTo compels Sea Limited to maintain high investment levels to defend its market position. This strategy, while necessary for market consolidation, poses risks to long-term profitability. The company's digital entertainment segment also faces challenges, including fluctuations in user engagement and seasonal variations.

Operational instability adds to Sea Limited's woes. External factors, including the COVID-19 pandemic, have forced the company to pivot operations frequently, leading to financial strain and the need for continuous investment in logistics and efficiency improvements. In the digital financial services sector, the expansion of the credit portfolio and aggressive credit offerings introduce further financial risks.

Complicating these issues is the impact of foreign exchange volatility, which continues to affect Sea Limited's financial stability. This adds another layer of uncertainty to the company's performance.

Q3 Earnings: It’s Clear Why The Stock Plunged

Sea Limited recently reported its third quarter 2023 earnings, which came in significantly below the bottom line estimate and basically met the top line. The company posted a GAAP earnings per share loss of $-0.26 , a significant miss compared to the GAAP Consensus Estimate of $0.00 per share. Meanwhile, revenues of $3.31 billion beat analyst expectations by a minimal 3.04%.

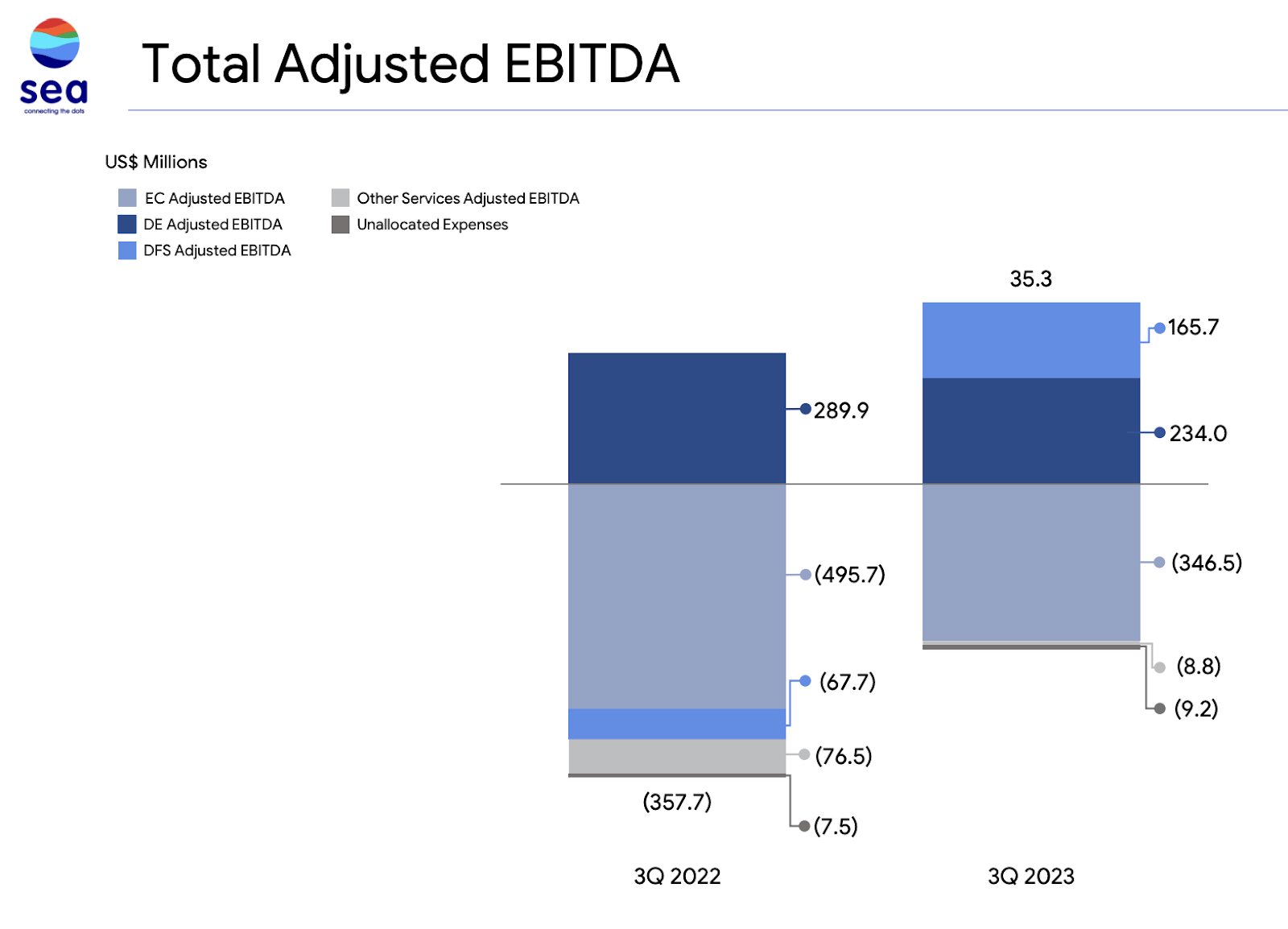

The weak quarterly results reflect ongoing challenges across Sea's core segments. In particular, the e-commerce division saw continued losses, with an adjusted EBITDA loss of $346 million compared to a loss of $496 million a year ago.

{kind=link}

Adjusted EBITDA (Q3 Earnings Presentation)

Tony Hou, Group CFO, stated:

We will continue to invest in the shopping season. It's a holiday season, shopping season as we all know. Q4 in our market, generally is the best time of the year to acquire new users, gain market share, and strengthen our content ecosystem - Q3 earnings transcript

This dependence on investing for growth highlights the difficulties Shopee faces in achieving sustainable profitability. While the overall cash position has improved to over $7.9 billion, reducing reliance on external funding remains a priority according to management (Q3 earnings transcript). However, with new entrants like GoTo intensifying competition in Sea's key Southeast Asia markets, the company feels pressured to keep spending just to maintain market share.

As Forrest Li, Group CEO, explained:

Competition may accelerate market share consolidation, and when markets stabilize, each remaining player will have sustainable profitability. Investing in market share gain now will position us better with even stronger market leadership when that happens - Q3 earnings transcript

But the timeline for this consolidation is unclear, and competition is forcing Sea to boost investment in areas like live streaming e-commerce to capture market share in the meantime.

Rapid shifts in business conditions, such as COVID-19 disruptions, also introduce uncertainty. Sea has had to pivot operations quickly, but this constant change makes stable execution difficult. There are still significant logistical and operational challenges as well in improving efficiency across Sea's e-commerce networks. For example, although Sea has made progress in reducing logistics costs per order by 17% year-over-year, continued focused investment is needed according to management (Q3 earnings transcript).

In digital financial services, credit quality remains a potential concern. While credit losses have trended lower, with NPL ratios of 5.2% and 1.6%, there is inherent risk in the $2.9 billion loan portfolio that requires vigilant monitoring (Q3 earnings transcript). SeaMoney is also expanding credit offerings rapidly, increasing risk if credit standards slip.

Meanwhile, digital entertainment faces risks from seasonal fluctuations and unpredictable user engagement trends that can dampen bookings. This was evidenced by slight declines in active users and digital entertainment bookings quarter-over-quarter despite new game launches. As Yanjun Wang, Group CCO, added:

We also mentioned on the call that in Q3, we saw a lot of school reopening and there are also less holidays. So that does affect the user engagement - Q3 transcript

Moreover, foreign exchange volatility continues to impact reported figures across all business units. Adjusting for currency fluctuations, Sea's operational revenue growth would have been higher based on management's commentary (Q3 earnings transcript).

Sea Limited faces an uphill battle to achieve sustainable profitability and stable growth amidst an uncertain macro environment and increasing competition across its key segments. The stock has sunk just shy of 90% from its highs as profits remain elusive. While Sea has viable long-term opportunities, executing on growth and margin expansion without missteps will be challenging in the quarters ahead. Until clear operating stability is reached, the stock remains vulnerable to selling pressure, which is reassured by the 7.7% short interest.

Forward Outlook

Sea Limited's latest quarterly results and commentary on the earnings call point to a challenging road ahead for the company. While management emphasized investment for growth, the pathway to sustainable profitability remains unclear. Intensifying competition and ongoing losses in the e-commerce segment were noted as key concerns.

In particular, Shopee is still far from reaching profitability, with the e-commerce division needing heavy investments just to maintain market share; this indicates that losses could persist for some time. Forrest Li also explained:

We will prioritize investing in the business to increase our market share and further strengthen our market leadership - Q3 transcript

However, this strategy sacrifices short-term financial health. Sea's rapid shifts between growth and profitability objectives also introduce uncertainty and make stable execution difficult. The company has yet to find an optimal balance between the two priorities. Sea's continued dependence on funding for growth casts doubt on the business model.

There are also no imminent catalysts for a recovery in Sea's gaming segment. Quarterly active users and bookings trends suggest a maturing business with limited upside. User engagement could weaken further as the reopening of schools and post-pandemic normalization continue, which simply promotes seasonality within the corporation’s customers. SeaMoney, while posting strong growth, carries inherent credit risk that could lead to higher loan loss provisions down the line.

In essence, Sea Limited's vision of developing an "all-in-one" consumer ecosystem is alluring but unproven. The synergies between business segments like e-commerce, gaming, and financial services remain largely hypothetical. This underscores the need for flawless execution at scale across diverse markets. Until Sea can demonstrate sustainable high growth and profitability, the stock will likely remain under selling pressure.

The global macroeconomic environment only adds to the headwinds facing the company. Rising interest rates, inflationary pressures, and the possibility of a worldwide recession do not bode well for discretionary consumer spending. Sea caters heavily to price-sensitive, middle-to-low income segments that could pull back further on e-commerce and gaming purchases.

Sea Limited faces a challenging path ahead given the combination of internal execution risks and external economic uncertainty. Significant improvements across metrics would need to materialize before considering an upturn in shares. Until then, Sea Limited remains in a precarious position, making the bears' thesis compelling.

Bullish Perspectives On Sea Limited's Business Strategy

Sea Limited's approach to e-commerce and overall business strategy offers a compelling case for optimism. The company has adeptly navigated changing market conditions, demonstrating a keen ability to pivot its operational focus as needed. During the pandemic, Sea's emphasis on growth allowed them to capitalize on the surge in e-commerce demand, establishing a strong market presence. As the economic landscape evolved, they adeptly shifted towards profitability, a move underscored by their recent investments in market share and leadership, particularly in the burgeoning area of live streaming e-commerce.

Sea reported a notable increase in GAAP revenue, up 5% year-on-year, driven largely by its e-commerce and digital financial services arms. This is a significant turnaround, evidenced by the group's adjusted EBITDA of $35 million, compared to the previous year's loss (Q3 earnings transcript). The growth in Shopee's active buyers and GMV further bolsters confidence in Sea's e-commerce strategy.

In the realm of digital entertainment and gaming, Sea's Garena platform, particularly the flagship game Free Fire, has maintained a stable and engaged user base, contributing positively to the company's overall performance (Q3 earnings transcript). The focus on enhancing player experience and diversifying the game portfolio underpins a solid foundation for future growth.

The Digital Financial Services ((DFS)) segment, led by SeaMoney, has shown impressive revenue and profit growth. The expansion and diversification of the credit portfolio underscore a strategic approach to capturing market opportunities in the financial services sector.

Looking ahead, Sea's commitment to continuing investment in e-commerce, especially during key shopping periods like the holiday season, reflects a strategic approach to solidifying market share and enhancing its content ecosystem. This, coupled with a balanced focus on operational efficiency, suggests a well-rounded growth strategy.

However, despite these bullish indicators, there remain significant uncertainties that cast doubt on the long-term viability of this investment. The persistent losses in the e-commerce segment, despite growing revenues, highlight a challenging path to profitability. Intensified competition, both in e-commerce and digital gaming, requires continuous, substantial investment to maintain market share, potentially eroding profit margins. Moreover, the reliance on credit business growth within the DFS segment introduces financial risks, especially considering the inherent volatility in lending markets.

While Sea Limited's strategic maneuvers and recent financial performance present a potentially attractive investment opportunity, the risks associated with competitive pressures, operational losses, and financial uncertainties in its key segments suggest that the potential risks may outweigh the rewards for cautious investors.

Valuation Outlook for Sea Limited: A Comparative Analysis

The Forward Price to Book (FWD P/B) ratio for Sea Limited stands at 3.37x, which is significantly higher than the sector median of 1.76x, indicating a 92.02% premium. This metric, which measures market valuation to the company's book value, is graded C-, suggesting that Sea Limited's assets are potentially overvalued compared to its sector peers. A high P/B ratio can imply that investors are expecting high growth and profitability in the future, but it also raises concerns about overvaluation, especially if the company's asset base isn't expected to generate proportional future earnings.

Similarly, the Forward Price to Sales (FWD P/S) ratio of 1.64x, exceeding the sector median of 1.12x by 45.96%, receives a C- grade (SE Seeking Alpha Valuation Metrics). This valuation indicates that investors are willing to pay more for each dollar of Sea Limited's sales than they are for the sector average. A higher P/S ratio can be justified if the company's growth prospects are robust compared to the sector, but it can also reflect overoptimistic expectations, which is where I stand.

Most notably, Sea Limited's Forward Price to Earnings (FWD P/E) GAAP ratio is at a staggering 71.46x, which is a 321.90% increase over the sector median GAAP forward P/E of 16.94x, earning a grade of D- (SE Seeking Alpha Valuation Metrics). The FWD P/E GAAP ratio evaluates what investors are willing to pay today for expected future earnings, and the exceedingly high ratio for Sea Limited could suggest that its earnings are not anticipated to be strong enough in the near term to justify its current share price, or it may indicate investors' high expectations for growth, which I believe could be challenging to meet.

In summary, I think the valuation of Sea Limited reflects over optimism in the face of less than expected performance, with the company's forward metrics indicating a significant premium over the sector median. While this implies above sector confidence in Sea Limited's growth trajectory, the rich valuation raises questions about sustainability and potential market corrections if the company's future performance does not align with these optimistic valuations. I think investors should weigh the higher risk due to its overvaluation compared to the potential for growth, especially in a market where sector peers are valued more conservatively.

Takeaway

Sea Limited's financial and operational landscape presents significant challenges that cast doubt on its ability to achieve sustainable profitability in the near future. The company's persistent losses, particularly in its crucial e-commerce segment, alongside the necessity for substantial investment to maintain market share in the face of rising competition, particularly from new entrants in Southeast Asia, signal a precarious path ahead. Operational instabilities, compounded by external factors like the COVID-19 pandemic, further exacerbate the company's difficulties. Additionally, the risks associated with the expansion in digital financial services and the inherent volatility of foreign exchange rates add layers of complexity to its financial stability. Considering these multifaceted challenges, the substantial decline in stock value, and the prevailing investor sentiment, a "sell" rating seems prudent. Sea Limited's journey towards profitability and stable growth appears fraught with too many uncertainties to confidently recommend investment at this time.

For further details see:

Sea Limited Q3 Deep Analysis: Adrift At Sea, The Future Looks Bleak