SE - Sea Limited's Dominance May Be Chipped Away By TikTok/GoTo's Monopoly

2023-12-26 09:00:00 ET

Summary

- For now, SE remains the largest e-commerce player in Indonesia, albeit with uncertain long-term prospects attributed to the intensifying market competition.

- TikTok's partnership with GoTo may pose headwinds for SE's e-commerce prospects, worsened by BABA's intensified investments into Lazada.

- The SE management has made the strategic pivot to "prioritize investing in the business to increase the market share and further strengthen the market leadership."

- However, this also means that the e-commerce segment is unlikely to be profitable, temporarily buoyed by the Digital Entertainment/ Digital Financial Services' profitability.

- While SE may be well-supported at the $30s, the stock may trade sideways over the next few years as it grows into its pulled-forward upside potential.

We previously covered Sea Limited (SE) in September 2023, discussing its promising prospects in Indonesia attributed to the immediate ban of TikTok's S-commerce platform.

We had reckoned that TikTok's estimated 2023 GMV of $8.4B might be up for grabs, allowing pure-play e-commerce companies like SE's Shopee to benefit, naturally triggering our reiterated Buy rating.

In this article, we shall discuss the latest developments on the e-commerce scene in Indonesia, with SE seemingly left out as TikTok chooses to partner with GoTo, with the new monopolistic Super App presence likely to trigger headwinds in the former's near-term prospects.

While we maintain our previous confidence that SE may be able to retain its large market share, it is also apparent that its profitability may be lumpy moving forward, triggering further volatility in its stock prices/ valuations, worsened by the elevated short interest of 7.09% at the time of writing.

The SE Investment Thesis Is Showing Cracks, As Monopoly Occurs In Indonesia

Thanks to the recent market events, SE's stock prices have been drastically corrected along with its prospects, with it temporarily well-supported at the $30s.

Was its stock correction warranted?

To a certain extent, yes. This is because TikTok's new partnership with GoTo inherently creates a monopolistic Super App presence in Indonesia, of which the latter already commands a leading mindshare.

For context, GoTo was formed in 2021 after the merger of Gojek (a ride-hailing, grocery, delivery, services, and fintech company) and Tokopedia (a local e-commerce giant).

As of FQ3'23, GoTo reported 6T IDR of revenues or the equivalent of $387M based on the FX at the time of writing ( +3.4% QoQ / +1.6% YoY ), albeit with a declining Active Transacting Users [ATU] of 52M ( -1M QoQ / -14M YoY).

Combined with GoTo's lack of profitability with -0.9T IDR of adj EBITDA (+25% QoQ/ +75.6% YoY), we can understand why the management has opted to woo TikTok with the partnership to enhance its e-commerce capabilities, with the latter also obtaining a controlling stake in Tokopedia .

This is especially true when ByteDance (BDNCE) expects its overall sales to hit over $110B in 2023 (+37.5% YoY), of which $8.4B may be from Indonesia.

It is also apparent that Alibaba (BABA) is not sitting on its laurels, with the cash-rich parent company investing another $634M in Lazada , building the YTD sum to over $1.8B, in order to remain competitive in Asia's e-commerce market.

Again, for reference, SE remains the largest e-commerce player in Indonesia, with 239.2M monthly visits (-4.3M MoM) compared to Tokopedia at 94.2M (-1.3M MoM) as of November 2023.

While SE does not break down its GMV by specific countries, with an annualized GMV of $80.4B (+5.2% YoY) in FQ3'23, we believe that while its long-term dominance is uncertain, its near-term prospects remain positive for now.

And this is why we can understand why the SE management has made the strategic pivot to "prioritize investing in the business to increase the market share and further strengthen the market leadership," in the face of the intensifying and unprofitable e-commerce business in Indonesia.

If anything, SE's foray into live-streaming has already taken off extremely well, with its average daily orders on live-streaming already reaching over 10% of its October 2023 total order volume in the Southeast Asia region, giving it an opportunity to emulate TikTok's S-commerce success ahead.

As a result of these intensified investments, it is unsurprising that SE reports growing e-commerce revenues of $2.2B ( +4.7% QoQ / +15.7% YoY ), albeit with widening adj EBITDA losses of -$346.5M (-330.5% QoQ/ +30% YoY) by the latest quarter.

However, investors need not fret, since the overall company remains somewhat profitable with adj EBITDA of $35.3M (-93% QoQ/ +109.8% YoY).

This is mostly attributed to the higher margin Digital Entertainment segment with adj EBITDA of $234M (-2.2% QoQ/ -19.2% YoY) and Digital Financial Services with adj EBITDA of $165.7M (+20.9% QoQ/ +344.7% YoY).

Combined with SE's robust balance sheet with a net cash position of $2.55B (+10.8% QoQ/ -19% YoY), we believe that the company remains well-positioned to grow its market share in the intermediate term.

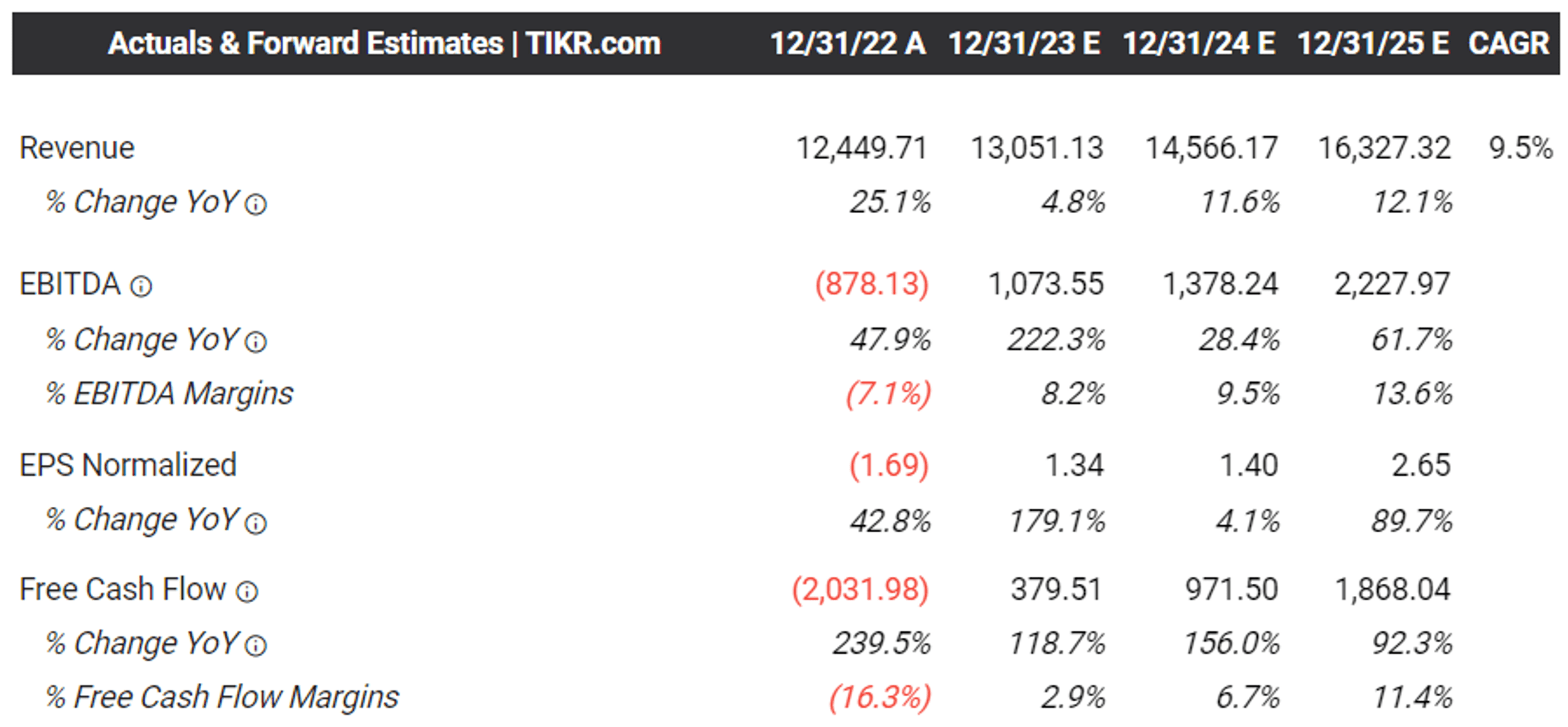

The Consensus Forward Estimates

{kind=link}

For now, the consensus has downgraded SE's forward estimates with a top and bottom line CAGR of +9.5% and +40.6%, compared to the previous projections of +14.2% and +70.82%, respectively.

Then again, the company is still expected to be profitable enough on a Free Cash Flow basis, implying that it may be able to fund its own operations and growth opportunities without having to increase its reliance on capital funding/ debt over the next few years.

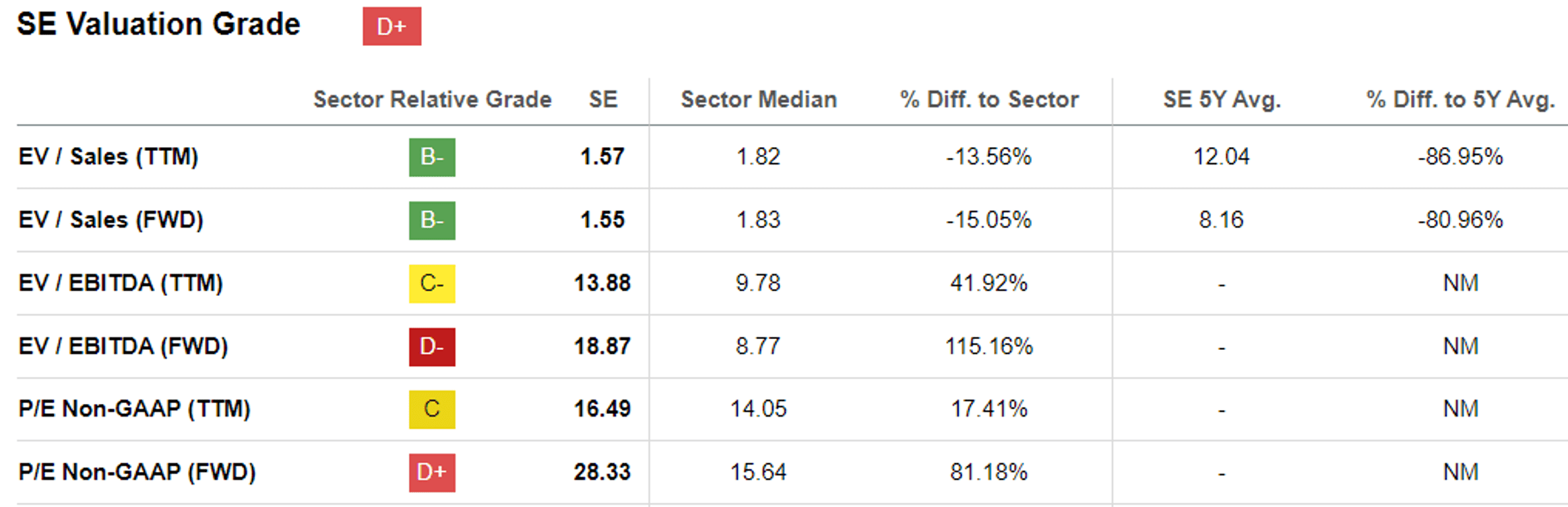

SE Valuations

{kind=link}

However, we also believe that SE's FWD EV/ EBITDA valuation of 18.87x and FWD P/E valuation of 28.33x appear to be rather inflated, compared to its 1Y mean of 17.70x/ 15x and the sector median of 8.77x/ 15.64x, respectively.

This is especially true since we expect its profitability to be lumpy moving forward, with any loss in market share and/or bottom-line misses likely to trigger further volatility in its stock prices/valuations.

So, Is SE Stock A Buy , Sell, or Hold?

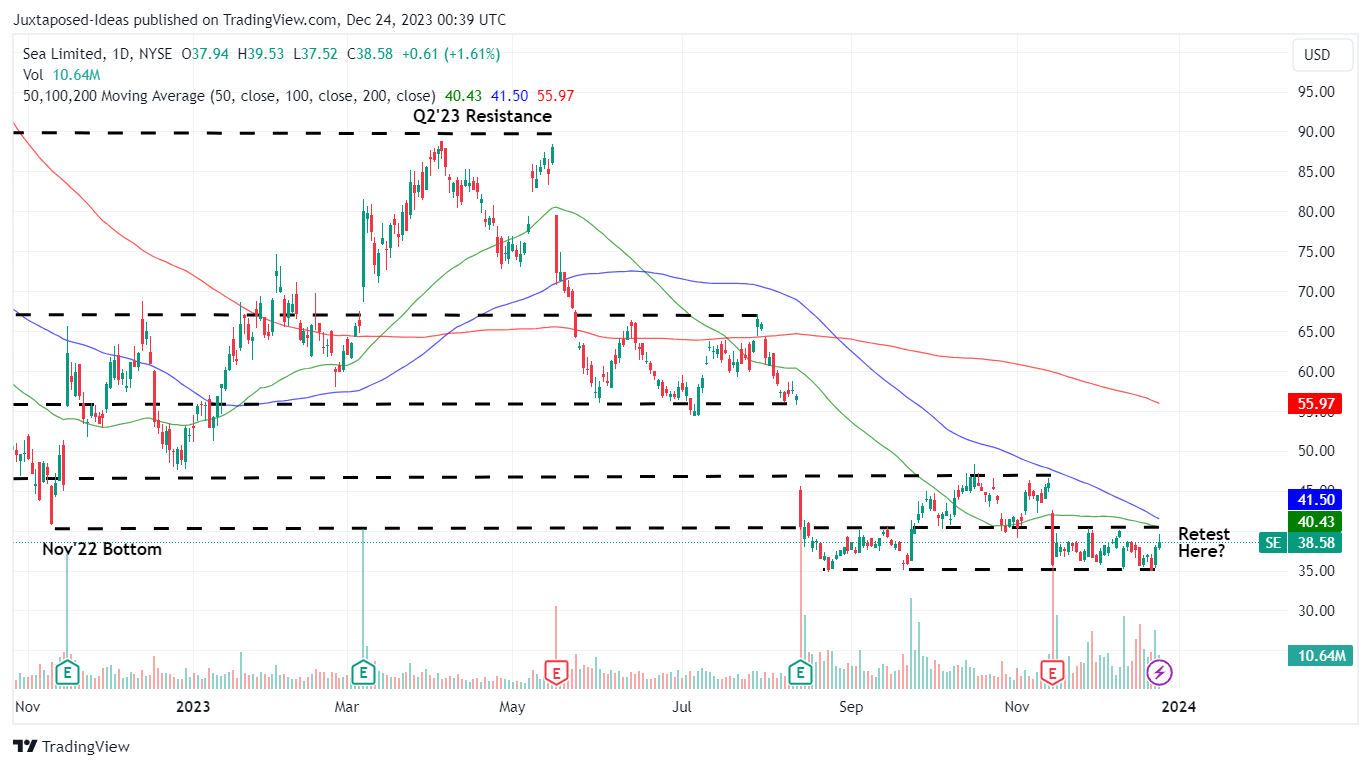

SE 1Y Stock Price

{kind=link}

For now, SE has already dramatically retraced by -55.3% since its April 2023 top, with it currently meeting great resistance at the $40s and bullish support at the $30s.

While we have been previously confident about its eventual reversal, it appears that the management has their work cut out for them.

It remains to be seen when FQ3'23's elevated sales/ marketing costs of $1.22B (-8.2% QoQ/ +2.5 YoY) may return to the FQ4'22 optimized levels of $825.9M and Indonesia's e-commerce competition may be consolidated.

Therefore, while we believe that the $30s bottom may hold, the SE stock may trade sideways over the next few years as it grows into its pulled-forward long-term price target of $41.40, based on the consensus FY2025 adj EPS estimates of $2.65 and the sector median P/E of 15.64x.

As a result of the reduced margin of safety, we prefer to downgrade our rating to a Hold (Neutral) here.

For further details see:

Sea Limited's Dominance May Be Chipped Away By TikTok/GoTo's Monopoly