SE - Sea Limited: Speculative But A Clear Buy

2023-11-22 08:05:50 ET

Summary

- Sea Limited reported mediocre quarterly results and the stock lost about 90% of its previous value.

- While growth rates declined in the last few quarters, the company is rather focusing on becoming more profitable and gaining market share.

- Despite competition from big players like Alibaba and ByteDance, the Southeast Asia market should enable high growth rates in the years to come.

- Despite being a rather speculative buy, SE stock is clearly undervalued.

So far, I covered Sea Limited ( SE ) twice and my last article was published about 15 months ago – in August 2022. At the time my last article was published, the stock has already declined steeply from its previous all-time high and has lost about 80% in value. In my article I asked if the stock was already cheap enough and answered the question with a “Yes”.

My bullish rating was not great – and that is an understatement. The stock declined another 50% in the meantime, but to save my honor a little bit – I also wrote in my last article:

Although Sea Limited might be undervalued at this point, we should not ignore that a bear market and recession is most likely still upon us. I expect the next few years to be rather challenging for stocks and when the recession will hit the economy earnings per share will decline and many stocks will go much lower. Despite an already 75% decline for Sea Limited, the stock could go lower. When remembering the Dotcom bubble and stocks declining 90% or 95%, we get a feeling how low technology stocks could go.

Now, 15 months later a lot has changed about the business, and it certainly is time for an update. As always, let’s start with the quarterly results that were published recently.

Quarterly Results

The company generated $3,310 million in revenue and compared to $3,156 million in revenue in the same quarter last year it results in a 4.9% year-over-year growth. Sea Limited had to report an operating loss once again (after the company reported an operating income in the last three quarters). Nevertheless, instead of an operating loss of $496 million in Q3/22, the company only had to report an operating loss of $128 million in Q3/22. And net loss also improved from $596 million in Q3/22 to $144 million in Q3/23.

Switching From Growth To Margins

One of the problems we can point out – and which was most likely one of the reasons for the collapsing share price – was top line growth slowing down drastically in the last few quarters. While Sea Limited grew in the triple digits in 2021 and still in the high double digits in some quarters in 2022, it was only growing in the single digits in the last few quarters.

However, management pointed out that it switched from high growth rates in the previous few years to rather focusing on improving profitability. During the last earnings call , management stated:

During the pandemic, we focused on growth first, ramping up rapidly to meet surging demand for e-commerce despite the great operational difficulties created by lockdowns. This allowed us to achieve significant scale and strong market leadership when growth was very efficient. Subsequently, capital became very expensive and less available. So we made a rapid turn to achieve immediate profitability for Shopee as a first priority, while sustaining the platform’s scale and market leadership. In both cases, we believe we made the right decisions in response to the shifting business environment.

And while it might take a few more quarters or years to determine if Sea Limited made the right decision, we certainly can see the decreasing spendings and expenses as one of the positive signs and trends we are seeing in the last few quarters. The platform logistics costs per order for the Asian market decreased by 17% year-over-year in the third quarter.

Sea Limited Q3/23 Presentation

{kind=link}

And as consequence of lower expenses the company is getting more and more profitable, and margins are improving. And since early 2019, the gross margin improved from only 1.78% back then to 46.56% right now. Operating margin also improved from -120% in early 2019 to 7.13% right now (all numbers are trailing twelve-month numbers). It is also a good sign that the margins in the last five years increased with a steady peace, and we don’t see much fluctuation. This is indicating pricing power (but of course we only have data for about 5 years).

Light and Darkness: Financial Services and Entertainment

When looking at the different segments, Digital Entertainment continues to struggle. Revenue for the segment declined from $982.9 million in the same quarter last year to $592.2 million this quarter – resulting in 33.7% YoY decline.

Sea Limited Q3/23 Presentation

{kind=link}

Almost every metric in the last few quarters declined. Quarterly active users declined from 568.2 million in Q3/22 to 544.1 million in Q3/23 and the quarterly paying user ratio also declined from 9.1% in the same quarter last year to 7.5% in this quarter. But when trying to mention something positive – Free Fire was the most downloaded mobile game in the third quarter on a global basis (according to management during the earnings call).

Sea Limited Q3/23 Presentation

{kind=link}

The biggest driver of growth right now is Digital Financial Services . Revenue for this segment increased 36.5% year-over-year from $326.9 million in Q3/22 to $446.2 million in Q3/23. And instead of an operating loss of $67.7 million in Q3/22 to an adjusted EBITDA of $165.7 million in Q3/23. And at the end of the third quarter, the company had a total credit portfolio of $2.9 billion (including $2.4 billion of gross loans receivable on the balance sheet). And about $1.4 billion in the total credit portfolio were SPayLater consumption loans.

And while the segment is a huge contributor to growth and profitability for Sea Limited, it is also creating risks we should not ignore. Similar to a bank, Sea Limited now needs to make provision for credit losses and in Q3/23 these were already $143.5 million. Sea Limited is still calling the quality of their loan book healthy, but 5.2% of loans were past due more than 30 days and 1.6% of loans were past due more than 90 days (both metrics improved quarter-over-quarter).

E-Commerce: Growing Market Share

But while SeaMoney is driving growth and contributing to profitability, e-commerce (Shopee) continues to be the most important segment for the business. And although grow slowed down, gross orders still increased 13% year-over-year and gross merchandise volume increased 5% year-over-year. Average monthly active buyers grew 11% quarter-over-quarter with improved buyer retention.

Sea Limited Q3/23 Presentation

{kind=link}

The next step for Sea Limited – according to management during the earnings call – is to focus on growing market shares. And while management stated several times during the earnings call that it will focus on growing market shares, management also acknowledged that new players have entered the market and competition increased. Sea Limited wants to invest to consolidate the market share the business already has. Additionally, Sea Limited will also use its $7.9 billion in cash and cash equivalents to not only consolidate market shares but also try to gain market shares. Especially in Q4 the company will invest in the shopping season, which is the best time to acquire new users (but competitors will try to do the same).

The company will especially focus on live streaming, which has become increasingly popular among sellers, buyers, and creators. For starters the product categories that do well in live streams usually tend to be high-margin categories leading to better monetization capabilities for the platform. Additionally, live streaming is driving engagement. Management stated during the last earnings call:

Second one is, typically, live stream is also a good tool for sellers to drive more engagement with their buyers or potential buyers, increasing conversions and also drive more sales during -- for particular products or testing a new product or for the leftover stock, etcetera. So it's -- generally, it's a good channel for the seller to invest themselves to market that businesses. I think all-in-all, if you put everything together, we do believe that the e-commerce EBITDA potential that we shared before will stay.

When talking about competition and about companies that could be a threat, TikTok (or its parent company ByteDance) is the one mentioned most often. TikTok Shop is rolled out in different countries – about two months ago also in the United States . And the move is not really surprising as other companies are trying similar moves. YouTube and its parent company Alphabet ( GOOG ) is also trying to make the video content platform an e-commerce and shopping platform as well. And Douyin – the Chinese counterpart of TikTok (also owned by ByteDance) generated already a merchandise volume of $200 billion in 2022 and we must acknowledge that TikTok and Douyin are not only a social network but can be a powerful e-commerce platform as well.

And not only TikTok is competition for Sea Limited. We should also not ignore Amazon.com ( AMZN ), which is also trying to enter the Southeast Asia market – however it seems like the company can’t gain much market share so far (mostly in the low-to-mid single digits ). And one of the major competitors is probably Alibaba ( BABA ) with its platform Lazada – the number two in the Southeast Asia market behind Shopee.

But in early October TikTok announced it will halt e-Commerce transactions in its TikTok Shop in Indonesia after the country announced a ban on e-Commerce trade on social media. And although this is positive news for Sea Limited and one competitor that is temporarily defended in one market, the competition will continue.

Growth Opportunities

Despite all challenges Sea Limited is already facing (or will be facing in the years to come) there are many growth opportunities for the business in the years ahead. First, SeaMoney has significant growth opportunities. Not only is Fintech still expected to grow with a high pace (see here for example)– as it can take market share from traditional banking, but it can also make people enter the banking system that weren’t using a banking account before (especially in less developed countries). Management stated during the last earnings call:

To sum up, SeaMoney has become an increasingly important pillar of our core businesses. It is contributing meaningfully towards both our top line and bottom line. It has enjoyed a healthy and improving risk profile and strong ecosystem synergy. Under SeaMoney, we will continue to strive to develop more comprehensive products and services to meet the financial needs of our users across the market.

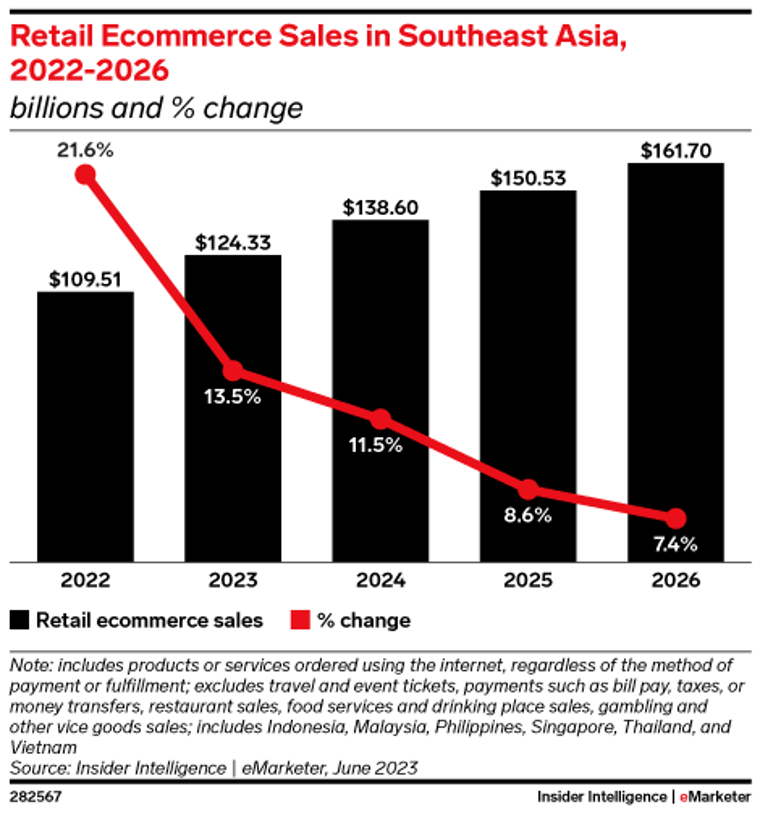

And not only SeaMoney – the fintech business – can contribute to growth. e-Commerce sales in Southeast Asia are also expected to grow with a solid pace in the years to come. Insider Intelligence for example is expecting growth in the high single digits in the years to come for retail ecommerce – but it is expecting growth to slow down.

{kind=link}

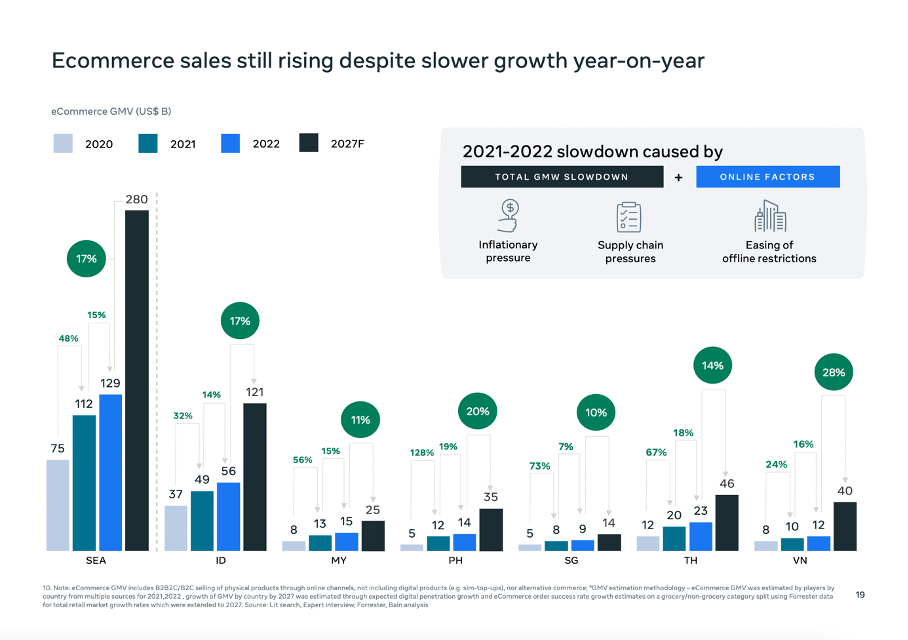

But other studies and analysis are expecting higher growth rates. A study conducted by Bain & Company and Meta Platforms ( META ) is expecting e-Commerce gross merchandise volume to grow with a CAGR of 17% between 2022 and 2027 in Southeast Asia and reach $280 billion in four years from now.

Bain & Company and Meta Platforms Study

{kind=link}

McKinsey & Company also see long-lasting growth in Southeast Asia, but are pointing out that growth rates in Indonesia, Vietnam or Thailand will not come close to past growth rates. McKinsey writes:

Using China as a reference point, Southeast Asian markets could sustain robust double-digit annual growth of between 15 and 25 percent for the next five years (…) Currently, the average e-commerce penetration rate (excluding food and beverage) in Southeast Asia is 20 percent, which suggests a long growth runway before it matches China’s penetration rate of 47 percent. Between now and 2026, the Southeast Asian market is projected to triple at a compound growth rate of 22 percent and will reach around $230 billion in gross merchandise volume.

And management of Sea Limited also remains optimistic and pointed out during the earnings call that e-Commerce penetration is still rather low in the markets Sea Limited operates in. Additionally, management is also pointing towards growth opportunities in Brazil. During the last earnings call, management stated:

In the third quarter, Brazil continues to enjoy strong growth. At the same time, our user economics in Brazil improves. We will continue to invest in category expansion and user acquisition in this market. And we will take a balanced approach of investing in growth while driving improvements in operational efficiency, especially in logistics. Our results in Brazil for the quarter speak to our success on both fronts. While we believe we already achieved sufficient scale and cost efficiency to be profitable in Brazil, our focus remains on capturing the growth opportunity there.

Overall, there is plenty reason to be optimistic for Sea Limited. The market seems to offer a lot of growth potential and even with competition increasing it seems possible for several different companies to grow together.

{kind=link}

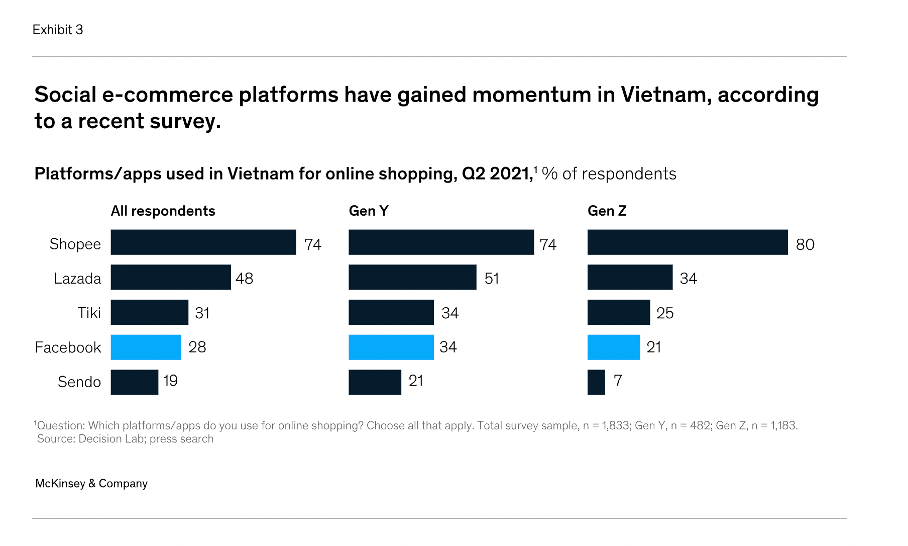

And at least according to McKinsey, Shopee seems to be well positioned and being the number one platform in Vietnam where e-Commerce platforms are taking off right now. By the way, the Bain & Company and Meta Platforms study is expecting a CAGR of 28% for Vietnam.

Intrinsic Value Calculation

And while growth rates by themselves are not enough as we must also consider competitors in any business, it is also not enough to just look at the fundamental business to make an investment decision. We also must calculate an intrinsic value to determine if a stock is a good investment or not. I was already bullish in my last article and now with the stock cut in half again in the meantime, we should be (especially) bullish.

Right now, Sea Limited is trading for a price-free-cash-flow ratio of 10.50 and for a business that might be able to grow in the mid-single digits or even in the double digits, such a valuation multiple is not justified.

In almost every article I use a discount cash flow calculation to determine an intrinsic value for a stock. However, it is rather difficult for Sea Limited to make assumptions about the years to come as we see little consistency among the reported numbers.

We can start by looking at the free cash flow. The last reported number was $2,121 million in free cash flow. When comparing this amount to the revenue of $12,899 million, about 16.4% of revenue end up as free cash flow. This is a good free cash flow margin for a young business, but it is not like such a margin seems unreasonable.

Another problem is the number of outstanding shares. It is difficult to find accurate information about the current number of shares outstanding. Y-Charts for example is claiming 553 million, Sea Limited is reporting 597.7 million in diluted shares outstanding on average in the last nine months. This would imply Sea Limited has bought back shares in the last few months. But I could neither find any announcement nor any hint in the available cash flow statements. It is clearly a problem that Sea Limited is only reporting selected results in its quarterly releases as this makes it difficult to find information. However, we find the following information on Sea’s IR page.

Sea Limited Investor Relations

{kind=link}

When dividing the market capitalization by the stock price we get 567 million outstanding shares. So, let’s calculate with that amount although I remain a little sceptic.

Additionally, we take a 10% discount rate (as always), and we assume 5% growth from now till perpetuity – a growth rate Sea Limited should manage to achieve easily considering the expected growth rates for the Southeast Asia market. Calculating with these numbers, we get an intrinsic value of $74.81. When even calculating with 10% growth for the next ten years followed by 6% growth till perpetuity, the intrinsic value would be $124.12.

Bottom Line

I think it comes down to a simple decision every investor has to make for him- or herself: Are we expecting Sea Limited to be able to fend off its competitors and all the companies trying to enter the market. And are we expecting Sea Limited to profit (at least a little bit) from the growing e-Commerce market in Southeast Asia? If that is the case, the stock is a clear “Buy” at this point.

But, Sea Limited is a really speculative “Buy” and I get it if people remain sceptic. It is speculative as the “small” company Sea Limited (about $21 billion market cap) has to compete with e-Commerce giants like Alibaba and Amazon as well as shopping on Platforms like TikTok and Facebook. On the other hand, this could be an “Amazon 2003” moment. Or it could be a company we won’t remember in 10 years from now. Or, with a market capitalization of $21.8 billion, it could be an acquisition target for companies like Alibaba, ByteDance or Meta Platforms. This is what makes it a speculative “Buy” – but it is a “Buy” in my opinion.

For further details see:

Sea Limited: Speculative, But A Clear Buy