MELI - Sea Limited: Swapping Unsustainable Growth For Profitability

2023-03-16 14:00:00 ET

Summary

- SE proved us wrong and showed that it was able to pivot to GAAP profitability just within two quarters, demonstrating its highly competent management.

- However, anyone looking to add here will also be looking at more stock volatilities in the short-term, attributed to the region/country's prolonged inflationary pressures through 2023.

- Therefore, it may be wiser to let the rally fade a little and enter in the mid $50s.

Growth At All Cost Is No Longer A Viable Investment Thesis

For FY2022, Sea Limited ( SE ) remained unprofitable, with -13.3% in net income margins and -$2.96 in EPS . However, it was apparent that the management had been determined to achieve profitability, due to the drastic improvement during FQ4'22.

The company has competently cut out -$0.71B of fats from its operating expenses QoQ by the latest quarter, comprising -$542M in SG&A expenses and -$176M in R&D expenses. This suggests a massive reduction by -39.6% and -41.9% QoQ, respectively. Otherwise, by -45.1%/ -$678M and -14.6%/ -$42M YoY, respectively.

Combined with the massive improvements in its COGS and gross margins of 49.2% (+10.3 points QoQ/ +8.5 YoY), SE had almost instantaneously steered its business towards GAAP profitability just within two quarters.

The company reported exemplary GAAP net incomes of $422.8M and net income margins of 12.2% in FQ4'22, though this was partly attributed to multiple one-off items. Then again, based on adj basis, the sum of $270.8M/ 7.8% remained impressive, in comparison to FQ3'22 levels of -$569.3M/ -18% and FQ4'21 of -$616.28M / -19.2%.

SE 1Y Stock Price

{kind=link}

If that didn't deserve the 21.7% stock rally the day after SE's recent earnings call, we're not certain what does during this time of an uncertain macroeconomic outlook. This was especially true when its more mature e-commerce peers, such as Shopify Inc. ( SHOP ) and Amazon ( AMZN ), have been struggling with rising inflationary pressures and growing operating expenses.

SHOP reported compressed gross margins of 46% and operating margins of -2.3% in FQ4'22, against FY2021 levels of 53.8% and 8.3%, respectively. AMZN had a similar experience, with FQ4'22 gross margins of 42.6% and operating margins of 1.8%, compared to FY2021 levels of 42% and 5.3%, respectively.

Nonetheless, while SE's recent developments were highly encouraging, it was also apparent these came at the cost of growth, with its top-line notably decelerating since FQ2'22. The company only reported a minimal expansion of +7.1% YoY in its combined revenues by FQ4'22, against the historical cadence of +17.4% in FQ3'22 and +105.7% in FQ4'21.

If we were to look closer, its digital entertainment business had experienced notable setbacks as well, with FQ4'22 revenues of $948.85M, indicating an impact of +6.2% QoQ and -33% YoY. While this performance was built upon a tougher YoY comparison of +104.3% in FQ4'21, minimal game pipeline, and the ban of Free Fire in India, the deceleration was a major concern, since the segment used to be the cash cow of the company.

SE's gaming segment only reported 27.2% of adj EBITDA margins in FQ4'22, compared to 32.4% in FQ3'22 and 43% in FQ4'21. These naturally translated as -$344.4M YoY in EBITDA headwinds for the quarter, or up to -$1.5M for the whole fiscal year.

Furthermore, the same deceleration in growth was observed in the e-commerce segment, with its GMV remaining somewhat in line YoY at $18B in FQ4'22, compared to $19.1B in FQ3'22 and $18.2B in FQ4'21.

We were additionally concerned by the SE management's statement, "We will discontinue any quarter-on-quarter disclosure of operating metrics like GMV and orders and then we'll move to an annual disclosure in line with global peers." This came as odd to us, due to the importance of GMV to most e-commerce/ fintech companies, such as SHOP and MercadoLibre ( MELI ), though we had to highlight that AMZN interestingly chose not to report this as well.

On the other hand, we might also view this phenomenon as a normalization in its GMV growth, due to the immense expansion SE had enjoyed over the past three years at a CAGR of 61.04%. The same was reflected by most e-commerce companies' performance thus far, with AMZN only reporting 8.6% YoY growth in the latest quarter against its 3Y CAGR of 22.4%, SHOP at 25.7%/ 52.5%, and MELI at 40.9%/ 66.2%.

In addition, the South East Asia region has experienced rising inflationary pressures, with a regional inflation rate of 6.1% by December 2022. Singapore did not fare well either, with a January 2023 CPI of 6.62%, against 2022 levels of 6.1% and 2021 levels of 2.3%. Therefore, the deceleration in GMV might also be attributed to the tightened discretionary spending in the region, as similarly reported in the US.

Nonetheless, SE has proven highly competent in executing on its profitability target by a large margin and in a relatively hassle-free manner. A feat that might be envied by many struggling companies indeed. Particularly, the management reported that their focus would be on sustainable and profitable growth moving forward, as emphasized by Forrest Li, CEO of SE, in the recent earnings call:

Given the macro uncertainties, we pivoted decisively late last year to focus on efficiency and profitability... As we continue this transition and manage sustainable growth going forward, we have adopted the approach of doing less, but doing this better... The key question presented to us at this stage is how much of these underserved needs for online consumption we can sustainably address? ( Seeking Alpha )

The same trend towards profitability has been observed in the deceleration of SE's Share-Based Compensation expenses to $191.02M in FQ4'22, relatively in line at -2.4% QoQ and +3.7% from FQ2'22 levels, suggesting a visible cost control by the management. Combined with a robust cash/ short-term investments of $6.89B, it appears that the company may have more than sufficient liquidity through its strategic transition over the next few quarters.

So, Is SE Stock A Buy , Sell, or Hold?

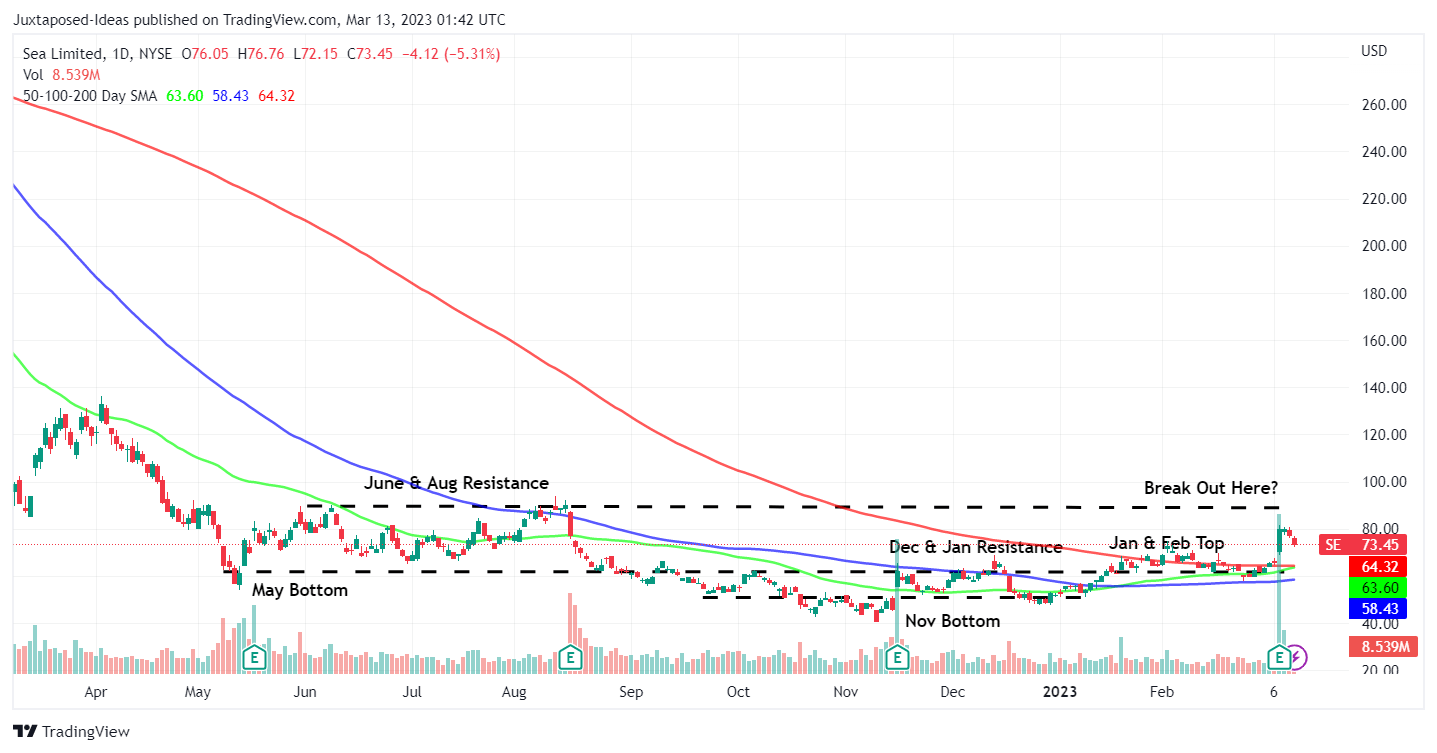

Now, the biggest question will be, is it still a good idea to add to SE stock here, due to the massive rally it has enjoyed of 79.4% since the November 2022 bottom? It really depends on individual investors' cost basis and risk tolerance.

However, we reckon it may be more prudent to be patient here and wait for the recent optimism to fade. Particularly, the Monetary Authority of Singapore expects the inflation to remain elevated at between 4.5% and 5.5% through 2023, suggesting prolonged e-commerce/ gaming headwinds in the intermediate term.

Therefore, we reiterate our $50s level entry point for improved long-term prospects for portfolio growth. There is no need to chase this rally.

For further details see:

Sea Limited: Swapping Unsustainable Growth For Profitability