WDC - Seagate: It's Unit Demand Not Gigabyte Demand That Will Drive The Stock

2023-08-02 12:35:33 ET

Summary

- We’re downgrading Seagate Technology Holdings plc to a sell, as we now see less upside potential for the stock into 1H24.

- We previously anticipated investors would turn positive on Seagate Technology stock as they believe the company's financial performance will bottom and begin to improve into 2024. We're now less optimistic about Seagate Technology stock.

- While we think end demand will improve in 2024, we believe the HAMR-based HDD transition will result in less unit demand from its cloud customers.

- Additionally, while we still believe generative A.I. will result in higher storage demand, we think this thesis will take time to play out.

- Seagate Technology jumped more than 7% overnight post fiscal Q4 FY2023 earnings results; we recommend investors take profits as we now see a less favorable risk-reward for the stock through 2H23.

We're downgrading Seagate Technology Holdings plc ( STX ) to a sell following its fiscal Q4 2023 earnings results ; we're less optimistic about the stock's upside in 2023. We now see muted cloud storage capex recovery and slower demand recovery in the PC client market and expect this to weigh on the stock in the near-term. We previously expected investors to turn more positive on STX as financial performance bottoms and begins to improve in 2024.

Management now expects inventory digestion and demand recovery to take more time to play out, noting on the earnings call , "We project it will take another couple of quarters for inventory levels to normalize." Our bearish sentiment is driven by our belief that unit demand rather than Gigabyte demand will drive the stock higher, and we don't see unit demand picking up in 2H23. We expect end-market demand to improve in 2024, but we believe the HAMR-based HDD transition will result in less unit demand from its cloud customers; the HAMR tech transition allows for increased HDD capacity growth that could outrun current cloud storage demand.

For 4Q23, the company reported a Non-GAAP EPS beat of -$0.18 and revenue of $1.6B, down 39.2% Y/Y and 14% sequentially, missing estimates by $90M. STX is a storage company with heightened exposure to HDD revenues, accounting for roughly 86% of revenues this quarter; our bearish sentiment is driven by our belief that the company won't experience revenue growth due to weaker unit demand; we see softer cloud demand and contracting PC TAM Y/Y; 2023 PC total addressable market, or TAM, is estimated to -10% to 18% Y/Y to ~240-260M due to weakness in consumer spilling into enterprise client.

While we believe the PC market is recovering, we expect the recovery to be slow in 2H23. We're seeing the higher interest rate environment and inflationary pressures weigh on IT budgets as customers already struggle to work down high inventory levels. We recommend investors exit the stock at current levels.

Revenue by segment analysis:

STX's HDD sales dropped 14% sequentially to $1.39B due to weaker demand for large-capacity HDD from the cloud and enterprise customers. The company's mass storage sales which account for 71% of total HDD sales, declined 20% sequentially to $983M as customer inventory correction cycles continue. Legacy HDD sales were up 8% this quarter sequentially. We now see a more muted cloud storage capex recovery and a slower demand recovery in the PC client market and don't see the stock outperforming meaningfully in the near-term.

The following table outlines STX's quarterly financial trends.

STX 4Q23 earnings presentation

Management now forecasts sales to drop 3% sequentially in 1Q24 to $1.55B, lower than consensus at $1.74B. Deep-diving into end-market demand, the company expects PC Client weakness to continue and tier-1 cloud customers to continue working through high inventory levels. We also saw the muted cloud storage impact Western Digital Corp ( WDC ) earnings this quarter; the company reported revenue of $2.7B, down 5% sequentially as cloud revenue declined 18% QoQ. We think WDC earnings and outlook for next quarter are negatively impacted by muted cloud spending and oversupply in the Flash market.

Additionally, the rising HDD ASP does incite our confidence in better financial demand for HDD supply; the company now expects to ship 32TB HAMR in early 2024. While we're constructive on STX reducing shipments "to several large cloud customers in order to accelerate inventory absorption," we're concerned that the reduced shipments and higher ASP amid a lower unit volume demand will cause the company to lose its economies of scale in factories. Our bearish sentiment is driven by our belief that STX's unit demand will drive the stock, and we don't see unit demand recovering ahead of 2024.

What about A.I.?

Our industry checks also indicate that the current wave of A.I. investments will favor the SSD and result in less cloud HDD storage spend in the near-term. When asked about the impact of generative A.I. on HDD and SSD sales, STX CEO Dave Mosley hinted that "some gen AI discussions that are very transactional and probably don't need a whole lot of HDD." We think the core data point to track here is cloud capex; under a limited cloud capex coupled with the A.I. boom, we'll see more capex spend circulated into SSD in the near-term. We see the lower cloud HDD storage spend harming STX in 2H23 as HDD sales are the company's main revenue stream. We do believe that generative A.I. will benefit the storage and memory space in the long run. However, while we still believe generative A.I. will result in higher storage demand, we think this thesis will take time to play out.

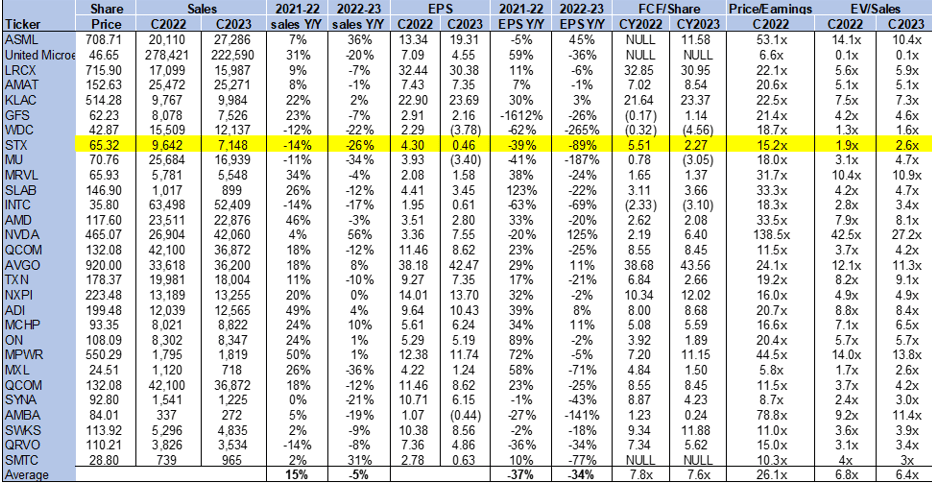

Valuation

STX is relatively cheap, trading below the peer group average on EV/Sales C2023. The stock is trading at 2.6x EV/C2023 Sales versus the peer group average of 6.4x. While the stock's valuation is tempting, we recommend investors not buy the stock on weakness as we think STX won't work in the near-term.

The following chart outlines STX's valuation against the peer group.

{kind=link}

Word on Wall Street

Wall Street shares our bearish sentiment on the stock but leans more towards a hold than a sell. Of the 25 analysts covering the stock, nine are buy-rated, 14 are hold-rated, and the remaining are sell-rated. We recommend investors explore exit points at current levels as we don't see a significant upside for the stock in 2H23.

The following charts outline STX's sell-side ratings and price targets.

TSP

What to do with the stock

We're downgrading Seagate Technology Holdings plc to a sell from a buy; we don't expect the stock to meaningfully outperform in 2H23. We now see softer cloud/enterprise spending in the near-term and expect end-market demand to recover in 2024, driven by demand recovery for HDDs as cloud customers adopt higher-capacity HDDs. The stock is up roughly 26% YTD, outperforming the S&P 500 by around 6%. We think investors should count their profits at current levels and explore exit points out of Seagate Technology Holdings plc stock.

For further details see:

Seagate: It's Unit Demand, Not Gigabyte Demand, That Will Drive The Stock