SNOW - Selling Snowflake: Consumption Model Highlights A Macro Vs. AI Conundrum

2023-12-04 14:56:06 ET

Summary

- Snowflake Inc. stock has been a strong gainer in software after posting outsized fiscal Q3 results and a raised outlook for the current period.

- The combination of emerging AI tailwinds, as well as new product launches have been key drivers of growth reacceleration at Snowflake in recent quarters.

- However, we remain cautious of Snowflake's inherent sensitivity to a potentially extended macroeconomic downturn given its consumption-based revenue model, which remains an offsetting risk to near-term growth prospects.

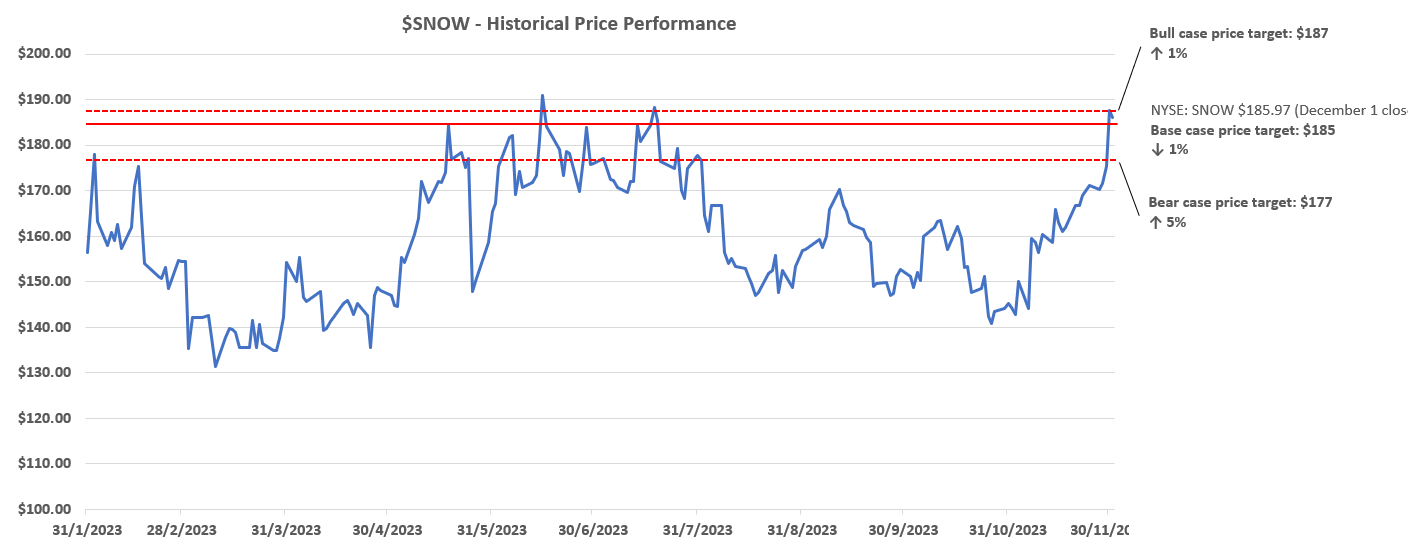

Snowflake Inc. ( SNOW ) stock jumped following the underlying business’ delivery of a stellar fiscal third quarter (ending October 31), alongside a stronger than expected outlook for the current period. Despite recently pared gains, the stock has stayed resiliently above the $180-range, and continues to boast a valuation premium relative to peers with a similar growth trajectory.

Much of market’s optimism over Snowflake’s prospects in the second half of fiscal 2024 comes from a “broadly stabilizing macro environment” as observed by management, which has translated to higher consumption volumes in recent periods. The company has also benefited from surging artificial intelligence, or AI, interest – despite having no direct generative AI product – thanks to its mission critical role in cloud-based data analytics and storage solutions. The company’s results this year has been largely in line with our previous discussion that that Snowflake’s forefront role in the growing adoption of a consumption-based model across the software industry has made it more recession-prone, despite also being first in line to benefit from an eventual recovery.

However, we expect limited upside potential for the Snowflake stock in the near term as it continues to trade at one of the highest multiple premiums in the software category. Although Snoike’s year-to-date valuation gains have lagged the overall industry’s average, the stock’s premium at current levels have likely already been adjusted for the combination of impending macroeconomic recovery tailwinds, as well as incremental AI-driven growth opportunities in the near-term, offset by continued conservatism in the overall software spending environment. This is in line with the limited expansion observed in Snowflake’s remaining performance obligations (“RPO”) and stabilization in the current realizable portion at 57%, which underscores a moderate pace of new bookings. With the fiscal fourth quarter being likely to benefit from a seasonal boost as management expects a large volume of expiring contracts due for renewal, we expect the current period’s RPO to be a telltale of longer-term demand at Snowflake, which will be critical to the sustainability of the stock’s valuation premium at current levels.

The Data Cloud and the AI Era

Unlike its software peers, Snowflake has sought to capitalize on emerging AI tailwinds through an indirect approach. “There is no AI strategy without a data strategy” – that has been the playbook Snowflake has gone with in terms of capitalizing on emerging AI tailwinds, rather than introducing its own generative AI solution like the majority of its software peers have over the past year.

As mentioned in the previous analysis , Snowflake has revved up its new product roadmap in recent quarters to better address data demands in the AI era – including Snowpark , Snowpark Container Services , Snowflake Dynamic Tables and Streamlit . The company has also recently introduced a solution for the seamless integration of Apache Iceberg table formats – an industry standard data table format for “procession on large datasets stored in data lakes” – into the Snowflake platform in private preview. The new feature aims at further addressing compute and storage optimization demands from customers by integrating Iceberg data to customers’ data storage accounts on Snowflake without incremental moderations required to the data itself or the incurrence of additional ingestion costs. The new introduced solutions will be progressing to public preview and general availability (“GA”) in the current period, which is likely to be accretive to existing capacity consumption levels in the data cloud, and reinforce Snowflake’s near-term growth outlook.

However, the concentrated volume of new product deployments is expected to be a cost factor heading into fiscal 2025, given the “half a year to nine months” timeline post-GA estimated by management for normalizing the associated operating expenses. Meanwhile, strengthening partnerships with hyperscaler marketplaces are expected to remain a key driver of improvements in consumption levels at Snowflake. Not only do these strategic go-to-market partnerships help improve Snowflake’s exposure to end-market users, but they also help the company optimize sales and marketing costs by relying on “self-serve purchases” where applicable.

We believe the strategy will continue to improve overall business profitability at Snowflake, especially as its product gross margins approach the long-term guidance with limited upside potential anticipated by management even as consumption levels are expected to improve. The focus is likely to gradually shift from growth to operating leverage once the impending consumption recovery narrative settles in for Snowflake.

Macroeconomic Considerations for the Consumption-Based Model

As discussed in the previous coverage, Snowflake’s consumption-based business model is inherently sensitive to macroeconomic uncertainties. Consumption-based models are typically the first to get hit during an economic downturn, given the flexibility offered to customers to scale up / down usage amidst times of uncertainty. This is in line with the consistent deceleration of growth at Snowflake over the past year, as the measured software spending environment continues to take a toll on consumption levels. However, the consumption-based model is also first to benefit from an economic recovery, as it bypasses wait-times associated with re-hiring and annual contract renewal periods linked to the typical subscription-based SaaS (Software as a Service) model employed by Snowflake’s software peers.

During the latest earnings call , management has largely attributed the outsized growth in consumption levels observed during the fiscal third quarter to stabilizing macroeconomic conditions. However, we believe the emerging AI tailwinds have taken precedence in helping Snowflake recapture some of the macro-impacted consumption volumes as discussed in the earlier section. It is also the first quarter of restored sequential growth in product revenue at Snowflake following significant declines observed during the July quarter, which makes it too soon to tell on whether the improved consumption volumes are fully indicative of a sustained economic recovery. Specifically, aside from optimization – which has stabilized relative to earlier in the year and remains an inherent consideration in IT budgets – ongoing uncertainties over the global economic outlook remain of concern across the tech industry.

The spending sentiment across boardrooms, though improved, have remained at a measured pace due to the elevated cost of capital environment. This has inadvertently slowed capital investments, including the migration of legacy IT infrastructures to the cloud, across the enterprise segment since the advent of the latest monetary policy tightening cycle until the AI-enabled spending cycle kicked in. The “higher for longer” narrative employed by the Federal Reserve on interest rates could potentially elongate the measured spending cycle, and impact the overall demand environment for data solutions outside of AI-related opportunities.

Signs of progressively slowing consumption at the household level also adds pressure on incoming corporate earnings, and further impact the cost of capital conundrum in the enterprise spending segment. Meanwhile, markets are starting to price in rate cuts in mid-2024 on the back of an imminent recession. Although rate cuts mean a lower cost of capital, which improves the appeal of future profits and benefits corporate valuations, recession sentiment could potentially weaken demand and, inadvertently, harbinger headwinds to Snowflake’s consumption-based business model again.

Hence, elevated risks remain over the durability of emerging signs of a “broadly stabilizing macroenvironment” as cited by Snowflake’s management. For now, we view AI tailwinds as a bridging factor for growth as the broader software industry continues to navigate through a potentially extended measured spending environment due to ongoing macroeconomic challenges. However, the relevant growth prospects associated with the nascent technology trend has likely already been priced into the Snowflake stock at current levels given its restored premium to peers. This is in line with surging volumes of initial migrations to the cloud – or “re-platforming” – observed at Snowflake in recent quarters, highlighting the resilience of demand for data solutions in the AI era which management has already considered in the recently offered guidance.

Fundamental and Valuation Considerations

Adjusting our previous forecast for Snowflake’s actual F3Q24 performance and forward prospects based on the foregoing analysis, we expect the company to finish the fiscal year with revenue growth of 35% y/y to $2.8 billion. This would imply product revenue growth of 37% y/y to $2.7 billion, which corroborates management’s raised guidance for the segment’s FY 2024 gross margins driven by improved consumption volumes, offset by impending new product ramp up costs in the current period. Our forecast expects strong growth reacceleration heading into fiscal 2025, as Snowflake is expected to benefit from incremental consumption volumes associated with the GA of recently introduced products, as well as near-term AI tailwinds.

However, the pace of growth is expected to moderate thereafter, considering impending recession risks. Our forecast assumes a more durable pace of growth reacceleration heading into fiscal 2026 instead when Snowflake’s consumption-based model is expected to benefit from maturing adoption of the pricing strategy, as well as broader economic recovery tailwinds.

{kind=link}

On the cost front, we expect Snowflake’s product gross margins to stabilize at current levels, with impending headwinds associated with new product roll-outs expected to be offset by gradual consumption volume improvements. Our forecasts expects a greater level of operating leverage improvements beginning late fiscal 2025 / early fiscal 2026 when product fine-tuning and other ramp up costs associated with the recently announced features start to normalize.

{kind=link}

Nvidia_-_Forecasted_Financial_Information.pdf

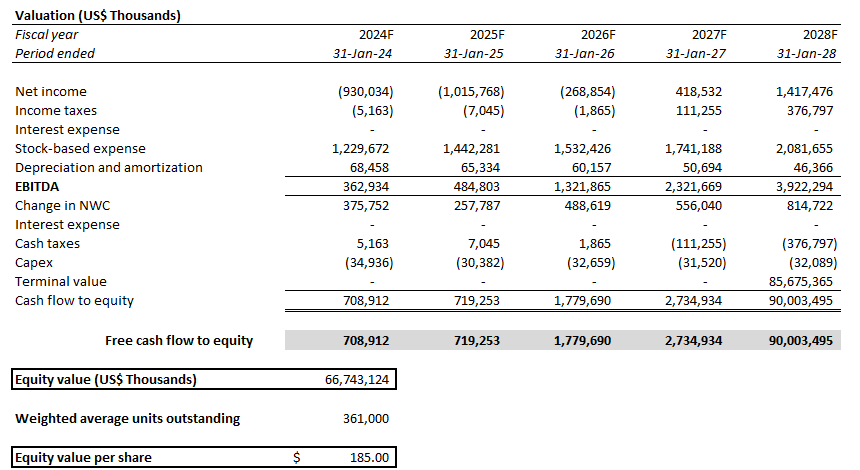

We are increasing our base case price target for the stock to $185 considering recent improvements to Snowflake’s forward fundamental prospects.

{kind=link}

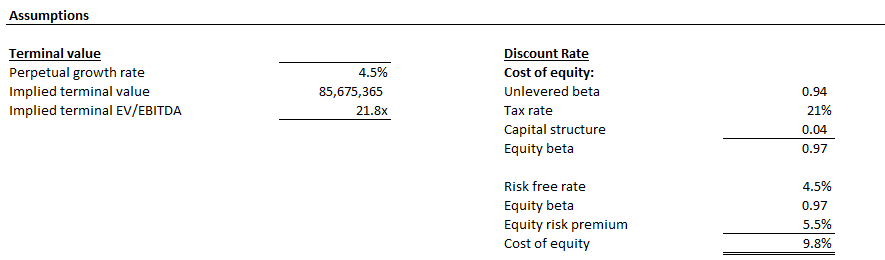

The price target is derived using the discounted cash flow ("DCF") approach, which considers cash flow projections taken in conjunction with the foregoing fundamental analysis on Snowflake. A 9.8% WACC in line with Snowflake’s risk-profile and debt-free capital structure is applied, alongside a perpetual growth rate of 4.5% on projected fiscal 2028 EBITDA. The perpetual growth assumption applied is equivalent to 2.5% on projected fiscal 2033 EBITDA when Snowflake’s growth profile is expected to normalize in line with the pace of estimated economic expansion across its core operating regions.

{kind=link}

{kind=link}

Final Thoughts

Snowflake has demonstrated consistent strength in mitigating some of its consumption-based model’s risk exposure to near-term macroeconomic uncertainties, while also capitalizing on emerging AI-driven data opportunities in recent quarters. Looking ahead, management’s optimism on near-term growth expansion is reinforced by the upcoming public preview and GA of newly introduced data products and solutions critical to facilitating the development and deployment of AI strategies across the enterprise segment. The impending approval of FedRAMP certification would also be a growth tailwind for Snowflake, as it permits greater participation in opportunities across the public sector.

However, considering ongoing macroeconomic uncertainties, particularly the elevated cost of capital environment, we believe incremental growth tailwinds ahead have already been priced into the stock at its current premium. This is corroborated by the stock’s limited gains relative to the broader software industry this year, as well as its persistent multiple premium relative to peers despite a lowered normalized growth trajectory.

While we remain confident in Snowflake’s prospects as a key beneficiary from the data- and AI-first environment, its consumption-based revenue model’s inherent sensitivity to macroeconomic uncertainties remain a key near-term roadblock to profitable growth, which diminishes the sustainability of the stock’s rich valuation at current levels.

For further details see:

Selling Snowflake: Consumption Model Highlights A Macro Vs. AI Conundrum