S - SentinelOne: A Valuation Update On My Top Pick Of 2023

2024-01-09 07:37:29 ET

Summary

- SentinelOne has performed reasonably well in a tough macro environment, with sustained above-market top-line growth and improvement on operating losses.

- The stock has seen a significant rally over the past month to make up for earlier underperformance.

- I continue to see long-term upside if the company can execute, but question in the prospective return is enough to justify the risk.

SentinelOne (S) has been a strong stock performer amidst a broader tech stock recovery. The company has sustained above-market top-line growth while making meaningful progress on reducing its operating losses. All things considered, the company has performed reasonably well in spite of a tough macro environment. When tech stocks crashed in 2022, the market may have been expecting unprofitable tech stocks like SentinelOne to struggle greatly between decelerating top-line growth and ongoing losses. SentinelOne has debunked these concerns, but the last many quarters have highlighted competitive risks relative to larger peers. While the stock may still deliver market-beating returns over the long term, I am concerned that the stock has delivered too much and too fast, with the stock now pricing in nearly a decade of flawless performance. I am now downgrading the stock with a neutral rating.

S Stock Price

Unlike many tech stocks which saw a strong recovery by the middle of 2023, SentinelOne did not see its own stock take off until the last month of the year.

I last covered SentinelOne in November where I rated the stock a strong buy on account of the net cash balance sheet, fast growth, and cheap valuation. The stock has delivered 46% returns since then (and slightly better returns since I named it my top pick of 2023 ), but this rally appears to have been spurred by unusual optimism in the tech sector that has me remembering the hysteria that preceded the 2022 tech stock crash. I do not trade on momentum and this is not the time for me to change tune.

S Stock Key Metrics

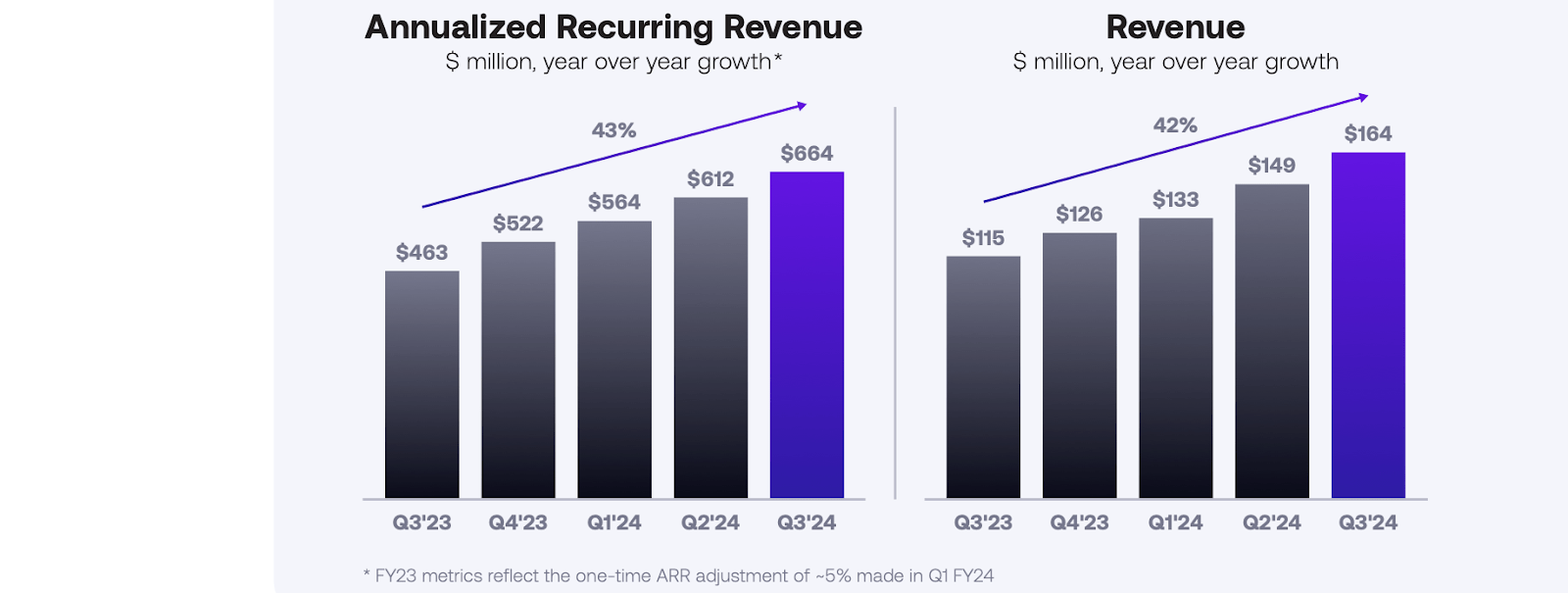

In its most recent quarter, SentinelOne generated 42% YoY revenue growth to $164 million, comfortably surpassing guidance for $156 million.

{kind=link}

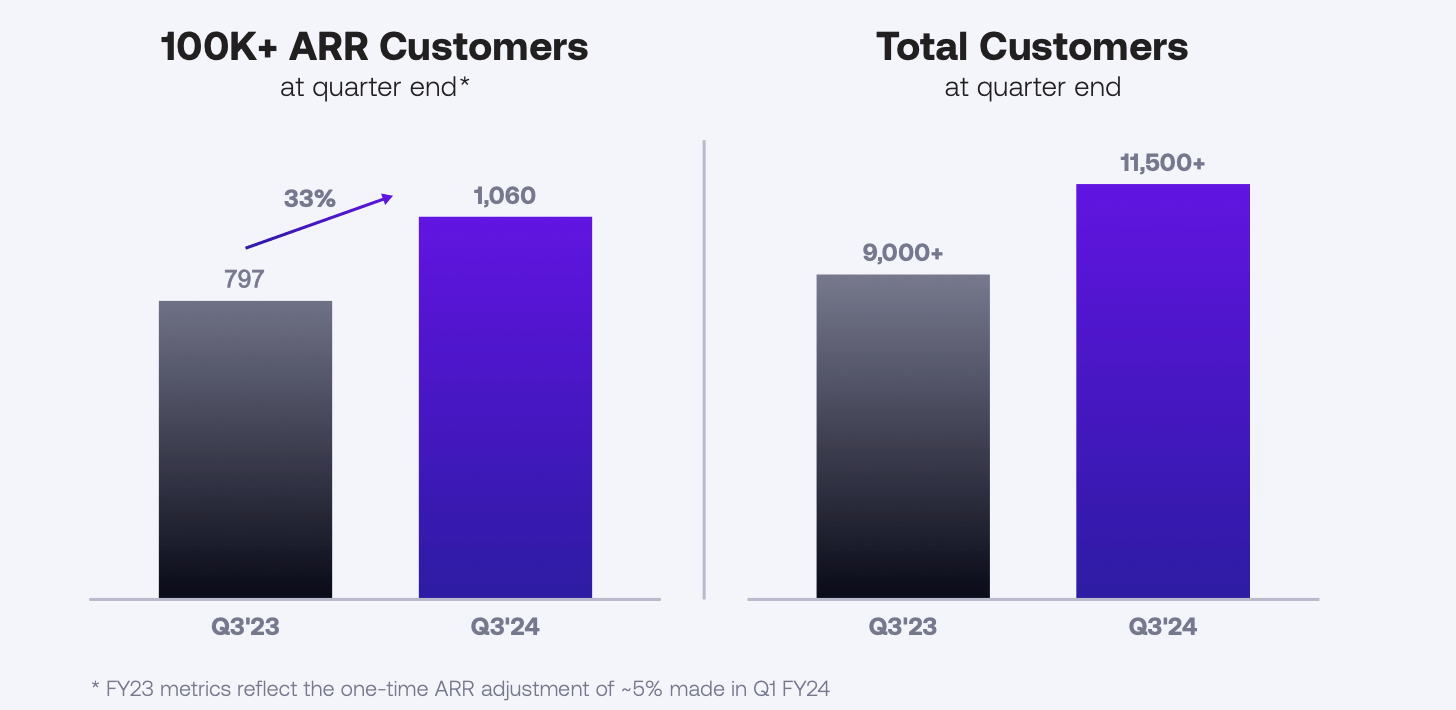

The company has been able to grow its customer base at a healthy clip (albeit slower than pre-2022 levels) in spite of the tough macro environment as many customers have been heavily scrutinizing IT budgets. SentinelOne grew its larger customer base by 33% YoY and 6.6% QoQ.

{kind=link}

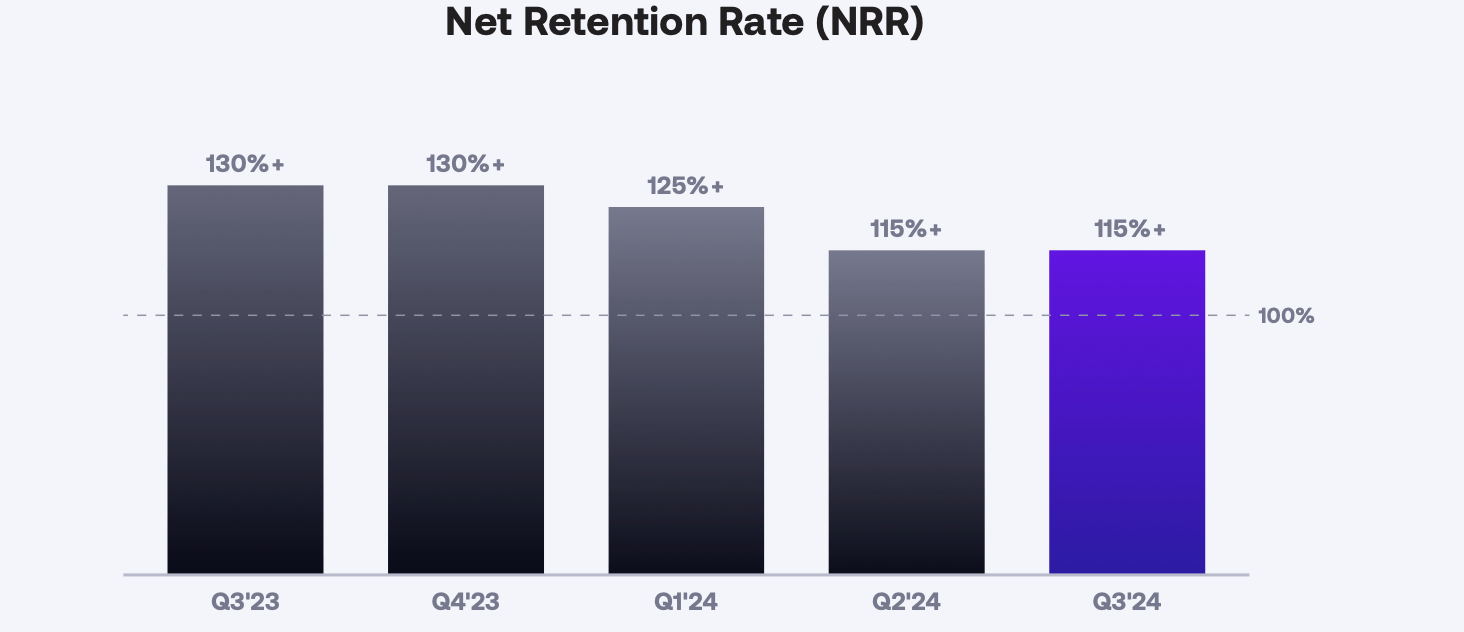

After two straight quarters of sequential deceleration, SentinelOne saw its net retention rate remain steady at 115%. The deterioration of this metric is a key driver of my waning bullishness for the stock. Heading into 2023, I had underestimated the ramifications of SentinelOne being a "point product" in relation to cybersecurity peers with more complete product portfolios. SentinelOne stock has performed well regardless due to its valuation having been too cheap prior, but it is nonetheless concerning to see direct peer CrowdStrike ( CRWD ) and cybersecurity peers Zscaler (ZS) and others post stronger retention rates in spite of larger revenue bases.

{kind=link}

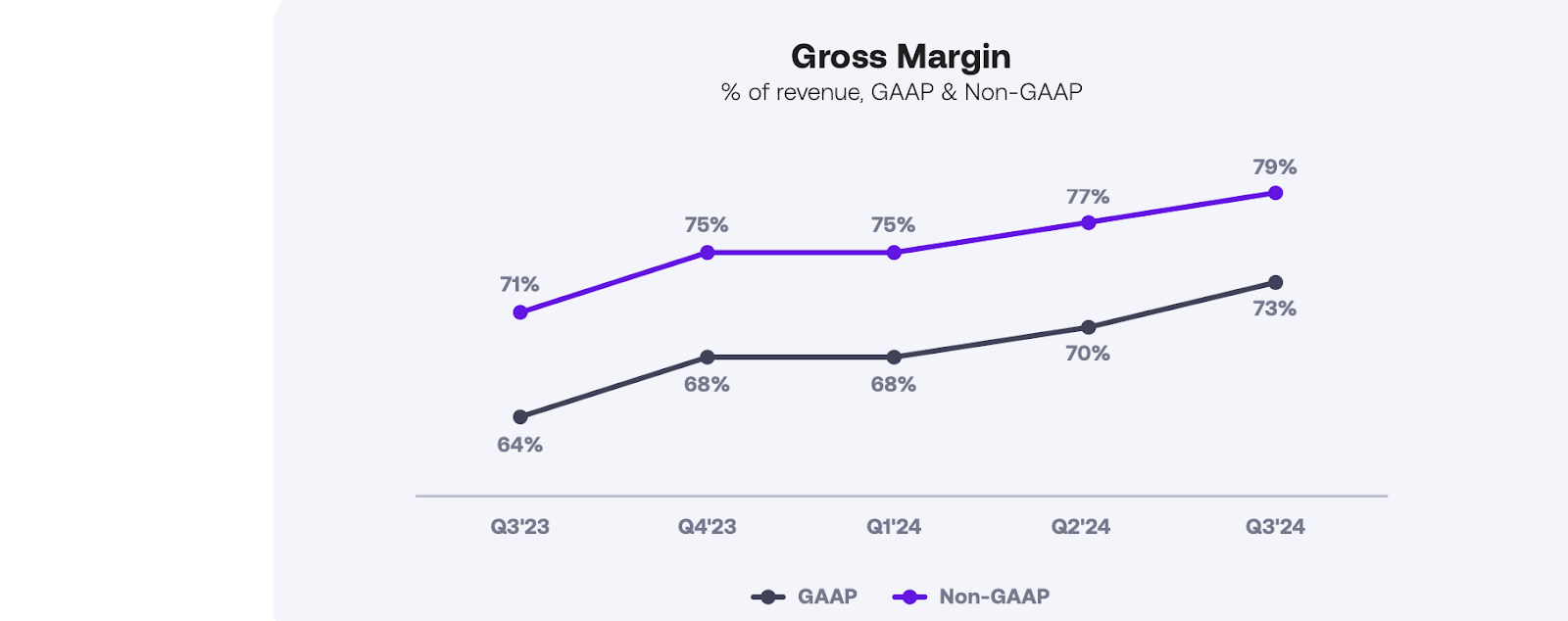

SentinelOne has been able to generate significant unit-level margin leverage. The company had come public in 2021 with gross margins standing at just 51% , but it makes sense to see gross margins converge closer to tech peers as it grows the revenue base.

{kind=link}

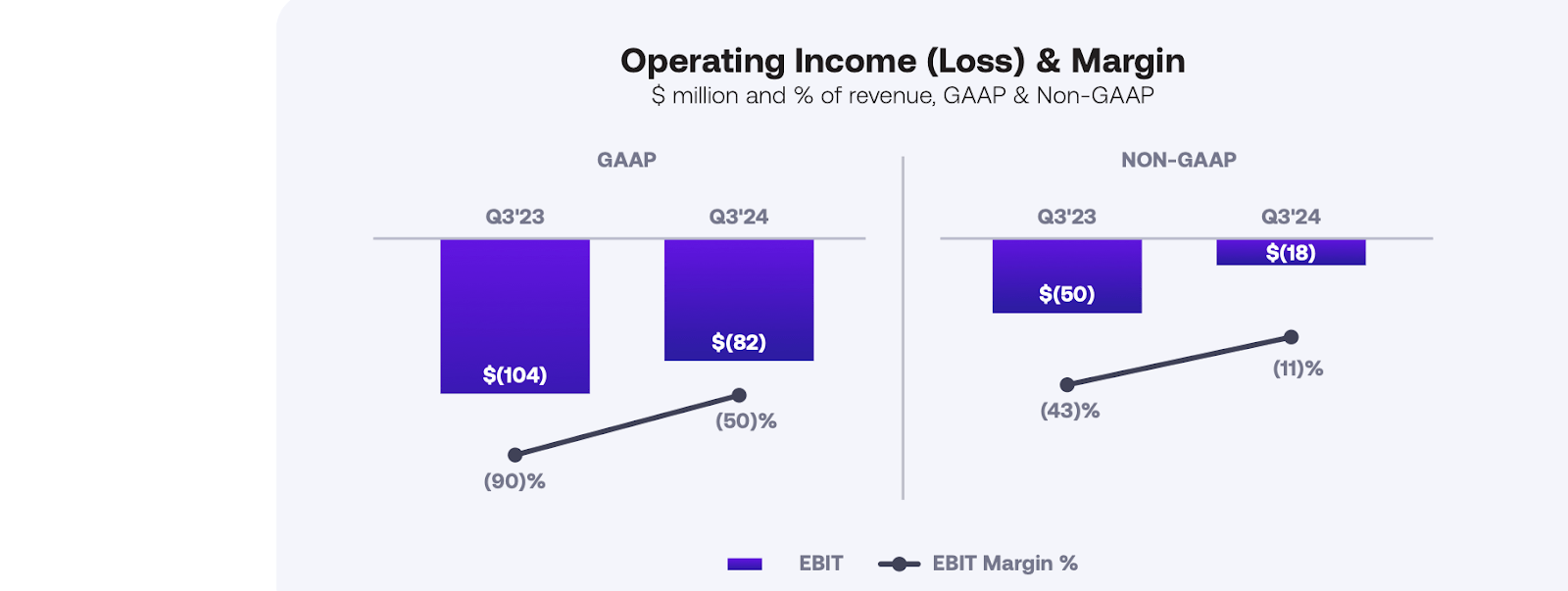

SentinelOne continues to be unprofitable, but the company has made meaningful progress on driving that loss number lower. In this past quarter, SentinelOne saw the non-GAAP operating loss margin come in at 11%, beating guidance for 22%. This marks the company's 9th consecutive quarter of more than 25% of margin improvement.

{kind=link}

SentinelOne ended the quarter with $1.1 billion of net cash. While this cash balance is no longer so significant relative to the higher stock value, it still remains a significant source of financial strength that can help fund ongoing operating losses.

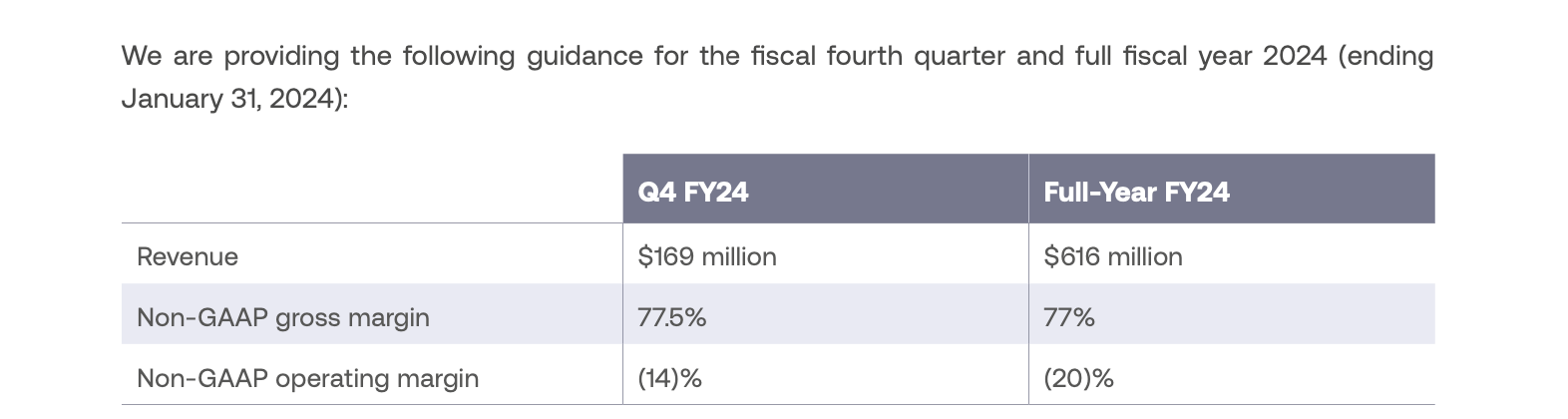

Looking ahead, management has guided for the 4th quarter to see $169 million in revenues, representing 34% YoY growth.

{kind=link}

On the conference call , management reiterated their commitment to achieving positive free cash flow generation "in the second half of the next fiscal year." Management once again highlighted their partnerships with managed security service providers ('MSSPs') which has become a popular way for enterprise customers to implement cybersecurity. With Broadcom ( AVGO ) having completed its acquisition of VMWare, news has surfaced discussing the potential for AVGO to sell off their cybersecurity unit Carbon Black. Carbon Black is a direct competitor to SentinelOne and management believes that these headlines may allow it to win customers from this competitor due to Carbon Black not having a complete solution for both endpoint protection and EDR.

Is SentinelOne Stock A Buy, Sell, or Hold?

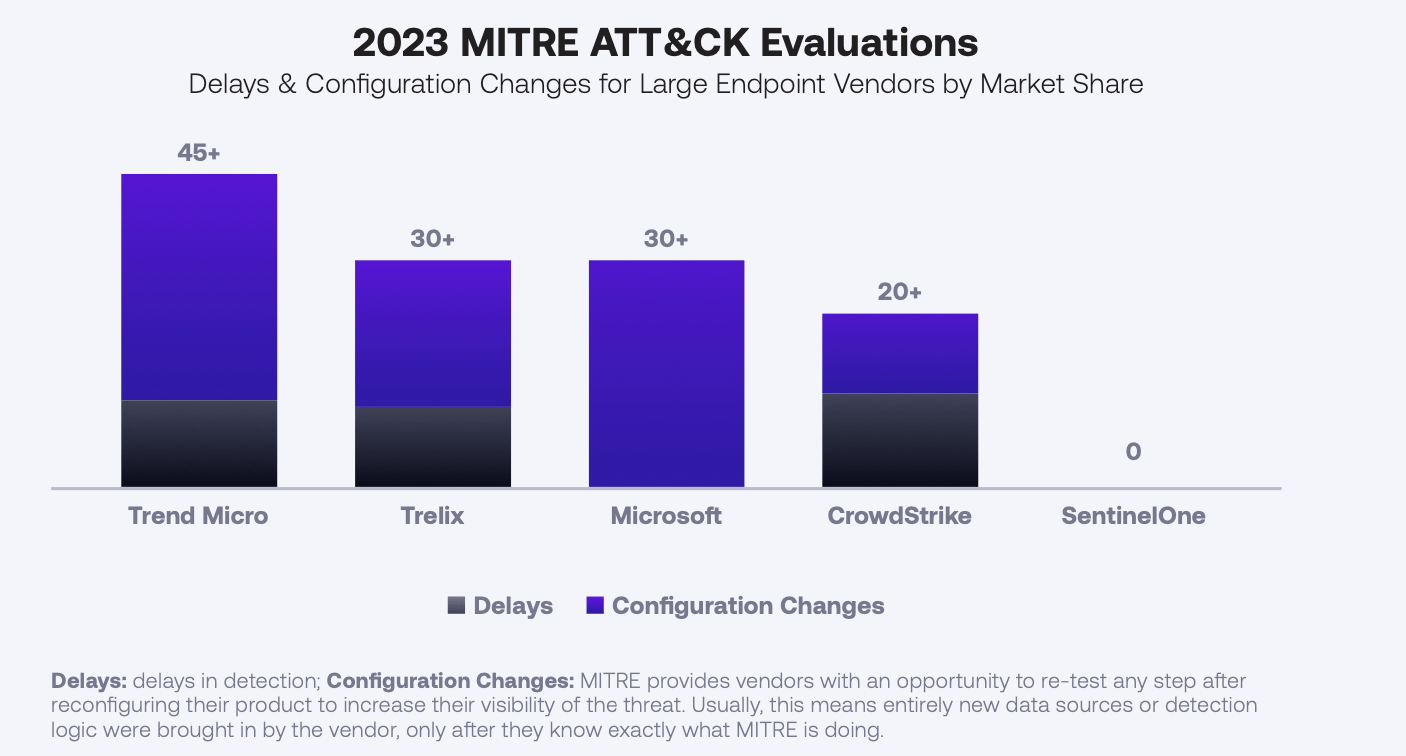

SentinelOne is a fast-growing cybersecurity operator focused on endpoint protection. It is difficult to determine which operator has the best technology, as even the MITRE ATT&CK evaluations frequently referenced by SentinelOne often favor certain operators depending on the evaluation.

{kind=link}

I view SentinelOne as having clearly superior technology to Microsoft (MSFT) and other legacy operators, but it is not entirely clear if it is superior to CrowdStrike.

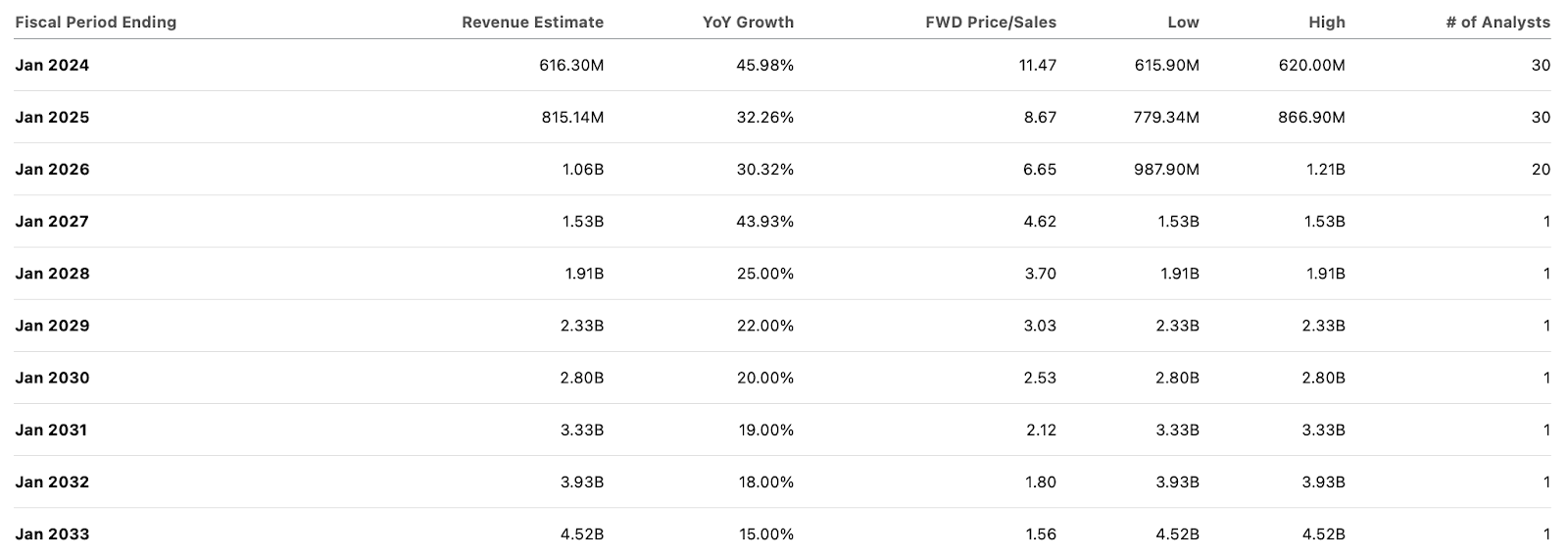

Management did not give guidance for the next fiscal year given that they typically only do so in the fourth quarter, but did comment that "even within the bad macro, obviously, you still see us grow 40%-plus." My hunch is that barring a significant macro improvement, consensus estimates may prove too aggressive. Consensus estimates call for an eventual recovery to around 44% top-line growth, with slow deceleration over the next decade.

{kind=link}

It is difficult to call consensus estimates conservative for two reasons. First, SentinelOne is already projecting quarterly growth to decelerate to the 34% level, which might even imply that the next 3 year's estimates of 44%, 32% and 30% growth may prove aggressive. Second, as discussed earlier, SentinelOne's point product portfolio has meant that it felt greater pressure on net retention rates in comparison to peers as of late. While larger peers may be able to delay deceleration in top-line growth due to strong net retention rates, I question whether SentinelOne can do the same given its smaller product portfolio.

Let's nonetheless use consensus estimates anyways. Based on 15% 2033e growth, a 1.5x price to earnings growth ratio ('PEG ratio') and 20% long term net margins (management has previously guided towards 20% long term operating margins), I could see the stock trading at around 4.5x sales by 2033, implying 12.5% annual return potential over the next 9 years. Between the point-product risk and still-distant path to profitability, those prospective returns do not look adequate. If we instead assume 25% long term net margins, then the potential upside rises to around 15.5%. While that would likely outperform the broader market by a significant sum, I would prefer to see more execution on the profitability front and an acceleration on top-line growth prior to investing on such aggressive assumptions, if at all. I note that we have also not yet factored in ongoing shareholder dilution, which stood at around 6% YoY in the latest quarter. The drag from shareholder compensation (which is not compensated by free cash flow generation given the GAAP losses) further dilutes my view of the prospective return potential. My guess is that, due to the furious rally in speculative growth stocks and growth stocks overall over the past month, stocks like SentinelOne have been re-priced to these aggressive levels. It may be difficult, but we must remember to not focus so much on the prospective return potential while ignoring the execution risks to achieving those projected returns. I am downgrading SentinelOne to a neutral rating given the lower risk-reward proposition and my more cautioned view on the execution risks.

For further details see:

SentinelOne: A Valuation Update On My Top Pick Of 2023