ZS - SentinelOne: Fast-Growing Cybersecurity Small Cap $1 Billion Of Net Cash Cheap Valuation

2023-11-03 17:10:13 ET

Summary

- SentinelOne continues to grow rapidly despite challenges from the macro environment.

- The company has made progress in reducing operating losses and has a large cash position.

- The stock remains undervalued and its cybersecurity products are increasingly important in the generative AI era.

- I reiterate my strong buy rating for this up-and-coming cybersecurity operator.

SentinelOne ( S ) continues to be one of the faster-growing names in the tech sector even as it experiences headwinds from the tough macro environment. The company has made great progress on reducing operating losses though it still has more work to do moving forward. The company has a large net cash position that should give it plenty of time to boost margins - as well as making the stock look even cheaper. While S is clearly seeing a disproportionately larger impact from the macro environment than larger competitors, the valuation continues to remain compelling. I reiterate my strong buy rating as its cybersecurity products have only increased in importance in the generative AI era.

S Stock Price

Unlike many tech peers, S has not bounced that strongly off the lows. This is in part due to the company still generating operating losses even on a non-GAAP basis, as Wall Street appears to still retain some doubts about pure-growth plays.

I last covered S in August where I discussed the stock amidst acquisition rumors. While management has since downplayed these rumors, the stock continues to look compelling as one of the faster growing stories in the sector today.

S Stock Key Metrics

In its most recent quarter, S delivered 46% YoY revenue growth to $149 million, coming in well ahead of guidance for $141 million.

FY24 Q2 Shareholder Letter

The tough macro environment has disproportionately benefited the fortunes of tech companies with more complete product portfolios, which in this case refers to competitors like CrowdStrike ( CRWD ) or Microsoft ( MSFT ). Even so, S was able to grow its customer count at a healthy pace.

FY24 Q2 Shareholder Letter

Instead, much of the weakness has come from continued deceleration in the net retention rate, which stood at just 115% in the latest quarter. S notes that the NRR includes legacy products from their acquisition of Attivo Networks. On the conference call , management noted that NRR would have been closer to 120% excluding those legacy products. Tech companies across the board have seen a steep deceleration in NRR in large part due to the tough macro environment, as companies have been either optimizing their data usage, slowing down headcount growth, or both.

FY24 Q2 Shareholder Letter

S has continued to make progress in increasing unit-level margins, with gross margins standing at 70% in the quarter. I expect gross margins to continue working higher as the company grows its revenue base.

FY24 Q2 Shareholder Letter

S delivered 2,500 bps of operating margin improvement, with its non-GAAP operating loss coming in at 22%. Like other tech peers, S has sought to offset decelerating top-line growth with operating margin expansion, though the company is admittedly still a ways off even non-GAAP profitability. I note that operating margin does not include interest income - due to the higher interest rate environment, S was able to generate $11 million of interest income, helping to offset much of the $33 million non-GAAP operating margin loss.

FY24 Q2 Shareholder Letter

S ended the quarter with $1.1 billion of cash and no debt. With their free cash flow burn at just $15 million this past quarter (down from $67 million YoY), the company has plenty of cash on its balance sheet to support ongoing losses.

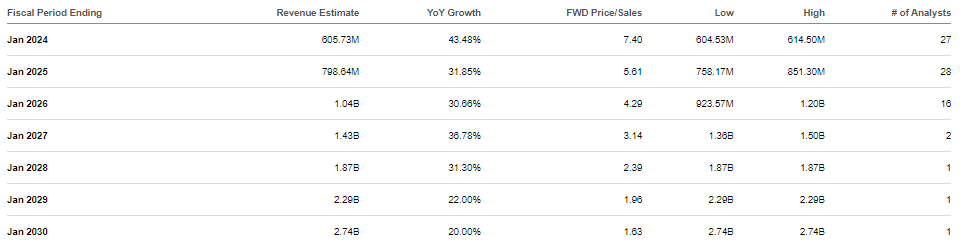

Looking ahead, management slightly raised full-year guidance from $600 million to $605 million in revenue. Third quarter revenues of $156 million implies 35% YoY growth as well as 32.4% YoY growth in the fourth quarter.

FY24 Q2 Shareholder Letter

Right before the print, reports surfaced that S had scrapped their partnership with Wiz. However, on the call management noted that they had merely canceled a re-selling agreement and still work with the company. Management reiterated expectations in achieving positive free cash flow in the second half of FY25 - that looks achievable if the company can continue their trend of improving operating margins by over 2,000 bps and if interest rates remain high (due to higher interest income).

Whereas in prior quarters where management implied that NRR of 120% should be considered a floor, management hinted that due to the tough macro environment (and aforementioned weakness from Attivo legacy products) that may no longer be the case. Over the long term, however, I continue to be of the view that cybersecurity is a mission-critical product with some of the strongest secular growth tailwinds.

Management reiterated their view that “win rates remain strong” even against larger competitors. However, management also appeared flustered in discussing comments made by CRWD, going as far as calling their assertions a “blatant lie.” Judging by the resilient revenue growth rates at CRWD, it is clear that S is being negatively impacted from a competition standpoint due to the macro environment. Even so, management declared that they “believe we can do that the best as possible as a public independent transparent company.” For long term investors that may be no surprise but investors hoping for a quick sale may be disappointed.

Is S Stock A Buy, Sell, or Hold?

As of recent prices, S was trading at just around 7.4x sales. That would imply some relative discount to peers on a growth adjusted basis, as CRWD is trading at around 14x sales with 28% projected growth, Zscaler ( ZS ) at 11x sales with 25% projected growth, MSFT at 10x sales with 13% projected growth.

{kind=link}

In my view, there are two reasons for the discount. First, S is often thought of as a “point product” in relation to those peers who have wider and in general more complete product portfolios. Some believe that customers are seeking to consolidate their cybersecurity services with fewer vendors. The second potential reason for the discount is the company’s lower profit margins. Whereas the three peers listed above are solidly profitable at least on non-GAAP metrics, S is still at least a year away from breakeven. That said, S is expected to deliver rapid operating leverage over the coming years.

Seeking Alpha

Again using my prior estimates of 25% revenue growth, 20% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see fair value hovering around 7.5x sales, implying solid forward upside potential from ongoing revenue growth.

What are the key risks? The cybersecurity tailwinds for endpoint protection look long and increasing in relevance due to the potential for generative AI cyberattacks, so I am not concerned with difficult macro conditions impacting results in the near term. However, it is possible that new and existing customers begin to prefer competitors with more complete product portfolios or better name recognition. S may need to lower prices in order to stay relevant, which would pressure gross margins and delay its path to profitability. The company has a lot of net cash on its balance sheet which by my estimates can endure nearly a decade of losses at the current rate. However, if these competition risks were to materialize, then I would expect the growth rates to slow, and for the stock to re-rate lower. For example if growth rates were to decelerate and stabilize to the 15% level, then the stock might trade at just 4x sales, implying considerable downside. In today’s environment that would arguably be at the low end of the fair value range, but it is still a possibility.

I reiterate my strong buy rating for the stock as one of the cheapest names in the tech sector still growing at envious rates.

For further details see:

SentinelOne: Fast-Growing Cybersecurity Small Cap, $1 Billion Of Net Cash, Cheap Valuation