S - SentinelOne: Initiate Long For Its Strong Growth And Huge TAM

2024-01-09 01:01:56 ET

Summary

- I am positive about S due to its potential for continuous strong growth in the large TAM.

- The company operates in a large TAM that is set to continue growing as businesses become more digitalized and vulnerable to cyberattacks.

- Recent performance suggests strong underlying demand, with revenue and total ARR showing significant growth.

Investment overview

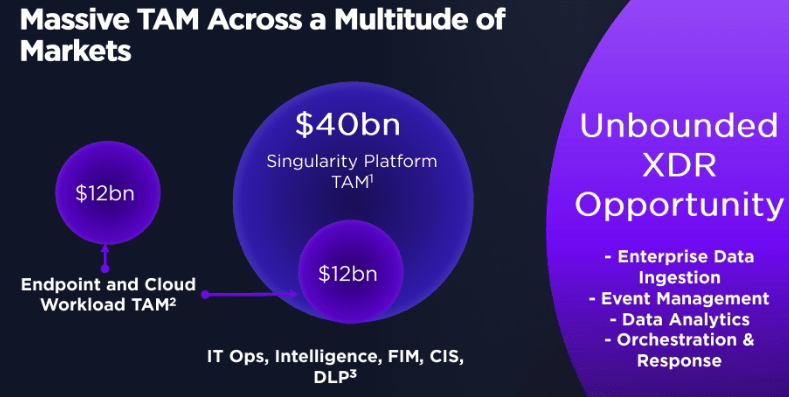

I give a buy rating for SentinelOne ( S ), as I believe there is plenty of room for S to continue growing and capturing share in this large $40 billion total addressable market [TAM]. As long as the world becomes more digitalized, cybersecurity is here to stay, and it will only get larger from here given the nature of cyberattacks. Looking ahead, I expect the business to accelerate growth as it reinvests in sales and marketing, and there is a potential for valuation to rise if it shows better-than-consensus-expected profitability.

Business description

S offers cybersecurity business to customers, specifically in defending endpoints, IoT, and workloads from adversaries. Notably, the platform is autonomous and enables customers to defend against cyber attacks in real-time. Over the years, since FY20, the business has showcased fantastic growth, which has increased more than 10x its revenue from $46.5 million to $573 million over the last 12 months. Despite the macro weakness, the business has continued to show strong growth (>40%) in recent quarters. S also retains a strong balance sheet with near $800 million in cash and equivalents and minimal debt, which eases concerns about S’s cash burning profile.

A large TAM that supports long-term growth

{kind=link}

S operates in a very large TAM that is set to continue growing in the coming years and decades as the world becomes increasingly digitalized and computerized. As of today, S is directly addressing a market size worth $12 billion (endpoint and cloud workload), but is expected to expand up to $40 billion as it addresses adjacent opportunities like data analytics, event management, enterprise data ingestion, and orchestration and response. As more businesses aim to stay ahead of their competitors, it is inevitable that they invest more in digital solutions (take AI, for example). The problem is that it makes businesses more vulnerable from a security perspective. This need for security is inevitable and extremely important. Failure to have a strong guard exposes businesses to potential threats like ransomware, which has seen increased frequency in recent years. Hence, cybersecurity is paramount. Given the nature of how hackers have continuously found new ways to cause damage to businesses, cybersecurity will continue to grow for the long term as it involves defending against more threats. This implicitly means that the TAM will keep expanding for as long as businesses rely on digital tools to function.

Recent performance suggests strong underlying demand

I believe the demand for cybersecurity is also quite resilient, as this is a necessity and not a good-to-have service or solution. S recent 3Q23 performance is quite evident on this, as it reported revenue of $164.2 million, representing 42% y/y growth. Total ARR also grew 43% y/y to $663.9 million. Notably, ARR per customer grew 15% y/y with dollar-based net retention sustaining above 115%, indicating that the existing customer base is seeing value from S solutions and is willing to spend more despite the weak macro environment.

Taking a step back, I think a major reason contributing to the slowdown in growth recently (from >100% to >50%) was due to S managing its losses as investors are looking for profits instead of growth-only businesses. S did well on this front, as the EBITDA margin has improved from -126% in FY22 to $43% in FY23 and is expected to turn positive in FY25. Looking ahead, I think there is a good chance for growth to accelerate. The reason I say this is because the Fed seems to incline towards rate cuts, which will be positive for a profitless company’s valuation and also for investors' appetite for risk. As the interest rate comes down and the company becomes profitable, S will have more flexibility to invest more in marketing to drive growth. Remember that S is addressing a $40 billion TAM, which implies that S only has a market share of a little more than 1%. It does not make sense for S to pivot to profits at this stage when there is so much room to grow ahead. I also highlight the fact that S got a new Chief Marketing Officer [CMO] in 1Q24, which I believe implies that management is not taking their attention away from investing in sales and marketing. Aside from reinvestments in marketing, S’s new products are also doing very well. For example, the newly released Pinnacle One product, which aims to provide security consulting services to enhance customer outcomes, has attracted a lot of demand interest, and management has also mentioned that the combined cloud and data lake solutions have grown by triple digits.

PingSafe acquisition is positive

A few days ago, S announced their intention to acquire PingSafe (a deal expected to close in 1FQ25). The acquisition makes sense for S, as it would strengthen its platform by improving its agentless Cloud Security Posture Management [CSPM] technology. With the ability to provide both agent-based and agentless solutions, S should see improvements in its competitive position in the industry. From a financial perspective, I think there will be marginal improvement to S’s financials given that PingSafe is relatively small in size (deal consideration is only $100 million).

Another implication from this acquisition is that management is not shy about deploying cash to enhance its technology. In my opinion, M&A is a fast and sensible way to enhance S’s product vs. deploying hundreds of millions into R&D. As I called out earlier, hackers are always finding new ways to cyberattack businesses; as such, speed is important. Acquiring offers the speed that a company like S needs. This acquisition also shows that management is not shying away from deploying capital for M&A. Given the myriad of point solutions available (which have inherent challenges that are pushing for more consolidation ), I expect management to continue acquiring them whenever the opportunity arises.

Valuation

May Investing Ideas

Based on my research and analysis, my expected target price for S is $23.67. Revenue should grow by 46% as guided in FY24 (management guided this in December, so there is high visibility). This 46% guidance is also a 400 bps acceleration from 3Q24 growth, which I am using as a benchmark for FY25 growth (another 400 bps acceleration). While I expect growth acceleration, I am taking a conservative approach in assuming what multiples S should trade at, as I expect S to start reinvesting in sales and marketing to drive growth. This could put some near-term pressure on profitability, which the market might not like. Nonetheless, as 8x forward revenue, which is where S is trading today, I still see a 16% upside. From a relative perspective, comparing S to other cybersecurity peers like CrowdStrike ( CRWD ), I would not think that S's valuation is demanding either. CRWD is trading at 14x forward revenue but is growing at the same rate as S. The major difference between the two is that CRWD has turned profitable while S has not. As S turns profitable (as consensus estimates in FY25), there is a good chance for multiples to go up from here.

Risk

Reputation for a cybersecurity firm is extremely important, as businesses only trust a product that does not fail. Take OKTA, for example. The firm has faced multiple breaches, leading to weak demand sentiment (declining growth) and drop in share price. If this happens to S, it is likely a similar pattern will follow.

Conclusion

I recommend a buy rating for S as I believe the business has potential for continuous strong growth within the expanding cybersecurity market. In fact, I see potential for growth acceleration if interest rates decrease, which should give management more flexibility to step up investment in sales, marketing. The recent PingSafe acquisition should also further strength S competition position and I like this M&A approach to enhancing its technology.

For further details see:

SentinelOne: Initiate Long For Its Strong Growth And Huge TAM